Arthur Hayes's fund Maelstrom has sold off all AI stocks, reduced its holdings in cryptocurrencies, and increased its investments in energy production companies.

Written by: Arthur Hayes

Translated by: Luffy, Foresight News

Is all this just my illusion, or do we really only need to subscribe to Citrini Research and blindly buy all the stocks they recommend to invest in artificial intelligence now?

Am I dreaming? Or have oil prices already lost their influence on the economy and politics? This is why Trump and the Iranian Islamic Revolutionary Guard Corps are able to clash across social media, while numerous ships are stranded in the Strait of Hormuz.

The yield on two-year U.S. Treasuries is 0.5 percentage points higher than the effective federal funds rate, sending such a clear signal from the market. Will the Federal Reserve really remain unchanged in the upcoming meeting and refuse to raise interest rates?

Will the entire dividend created by artificial intelligence in the U.S. really only fall into the hands of a few tech practitioners?

This chaotic world compels me to perform a reality check to confirm whether I am awake or deeply trapped in a dream. Once the test results prove that everything is just an illusion, I will immediately adjust my investment portfolio. This article is my testing process. After typing these words and sorting through my thoughts, my holdings will undergo significant changes, or they will remain unchanged.

I will first throw out my core judgment: the current state of the market resembles a dream. Within the entire investment system, the prices of oil and other hydrocarbon energy are the core variables that have a reverse transmission effect. The essence of how humanity perceives the world is to transform energy into biological intelligence, and the logic of artificial intelligence is similar. This rule will never be broken. The market might deviate from this common sense in the short term, but reality will ultimately counter it.

This article will start with oil prices and ultimately focus on the U.S. elections. The current situation is likely to trigger a burst of the AI stock bubble and drag down the entire crypto market. Once the dust settles, Bitcoin will have a chance to rebound from the bottom. I previously asserted that Bitcoin would never touch the $60,000 mark again, but now it's clear that I misjudged. This is also the norm in market predictions. I always adhere to one principle: opinions can be distinctive, but they do not have to be dogmatic.

Next, we will analyze.

Negotiation or Not, the Core Question Now

Politicians always act around their own interests. Trump has launched military action against Iran for no apparent reason, the reasons for which he alone knows. Faced with the various statements he and his staff throw out at every moment, the outside world cannot discern the truth. At this point, it is pointless to twist over the cause; the real question is whether Trump and the Iranian Islamic Revolutionary Guard Corps will choose to ceasefire and how they will end the standoff.

This conflict is entirely led by Trump now, and for him and the Republican camp, provoking war in an election year puts them in a passive position.

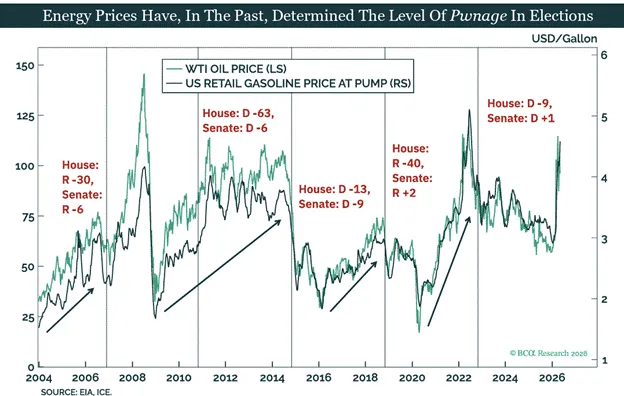

In the U.S., the prices of gasoline, food, and other necessities often directly determine the election results. Currently, shipping through the Strait of Hormuz is obstructed, energy and food inflation continues to rise, and the root of all this is the hasty action against Iran initiated by the Trump administration without public consultation. Some may point fingers at Israel, but this claim does not hold water. Understanding U.S. history makes it clear that local forces will never listen to external arrangements.

As long as the flames of war do not affect their lives or result in casualties among family and friends, American people are not averse to fighting abroad. Trump has also repeatedly emphasized that only thirteen U.S. soldiers have died in this special military operation. This is also why the U.S. is keen on using high-tech long-range weapons and launching "game-like wars." Even if this Middle East conflict lacks a clear victory strategy, it contradicts the expectations of many supporters, yet his basic support still chooses to stand with the Republican side. Some Republican legislators, due to their wavering stance, have faced pressure from within Trump’s party and lost their seats, which confirms this fact.

The core risk for Trump is not that basic voters are unwilling to vote in the November election, but that soaring prices could push a large number of centrist voters toward the Democratic Party. The issue of living costs has become the biggest problem in Trump’s election prospects.

To win over centrist voters, Trump must at least stabilize current oil prices. At present, the supply chain has just begun to gradually digest the pressures brought by rising energy and various production material prices; completely curbing inflation is already unrealistic. What Trump can do now is only to control market expectations for inflation rather than change inflation itself.

Whether Trump is willing to reconcile with Iran completely depends on oil price trends. When oil prices continue to rise, his statements will shift towards moderation; but once the market anticipates negotiation between both parties and oil prices fall, he will change his attitude again. After all, from a geopolitical perspective, any agreement reached in this negotiation is likely to be more passive than the agreement signed between the Obama administration and Iran. In the eyes of many voters, this amounts to "defeat," and the Republican Party will pay a price in the election.

Negotiation always requires concessions from both sides, and the Iranian Islamic Revolutionary Guard Corps has similar considerations. If oil prices are too high, its main trading partners will exert pressure, demanding that Iran compromise with the U.S.; however, if Iran sends signals for negotiation and oil prices fall, the pressure from trade partners will also diminish.

Looking at current oil prices, both the U.S. and Iran have no incentive to retreat actively. While oil prices have risen significantly compared to pre-war levels, they have not yet reached a crisis-inducing level. The overall commodity market remains stable; globally, there is no large-scale famine, and most countries can replenish key industrial materials from other channels.

However, this delicate balance is destined not to last long. A significant reduction in global core energy supply, yet prices remain remarkably stable, fundamentally contradicts market laws. Once the global idle capacity is exhausted, spot prices will inevitably surge, and this is a consensus among many commodity analysts. The current crisis has not fully erupted yet simply because there was sufficient global energy stock prior to the war.

If the U.S.-Iran standoff continues until the end of the second quarter, the spot prices for hydrocarbons and various basic commodities in the third quarter of this year will undoubtedly experience a sharp increase.

To quote Churchill's famous saying: Politicians will only make the right choices after exhausting all other options. Only when the situation is completely out of control will Trump and Iran actually sit at the negotiation table. In my view, the current state of shipping being obstructed in the Strait of Hormuz is likely to last until early the third quarter.

Let us assume that oil prices will gradually rise amidst fluctuations. In this context, what kind of mutual influence will continuously rising oil prices and Trump’s campaign rhetoric have?

November Election Clash: Republicans vs. Democrats

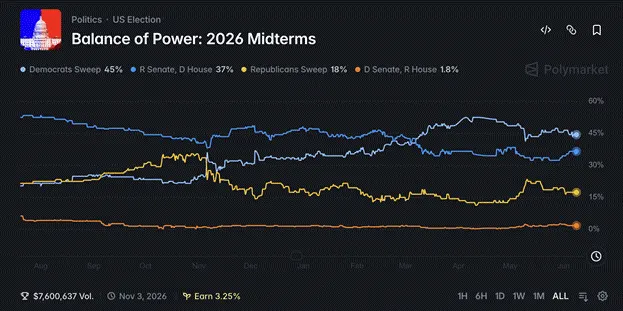

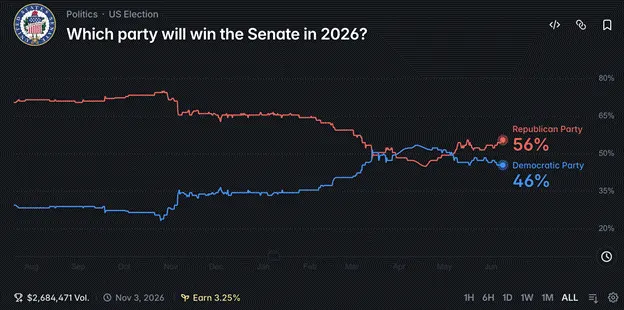

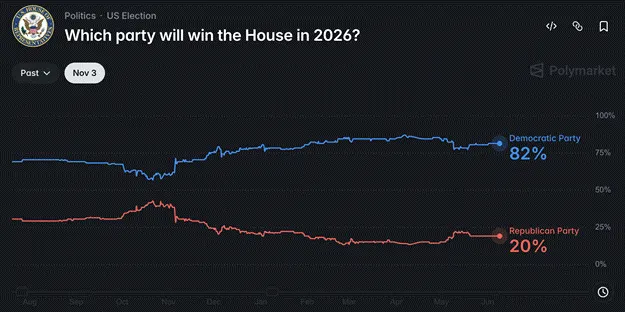

According to the odds in the prediction market Polymarket, the Republicans can currently only hold on to the Senate with a narrow advantage, while they are expected to suffer a significant loss in the House of Representatives.

It is widely believed that the Republicans will lose the House of Representatives, but I have a different perspective. Trump still has a chance to turn things around, and the breakthrough lies in adjusting the direction of public opinion, specifically through statements regarding data center construction and regulations and taxes related to the artificial intelligence industry.

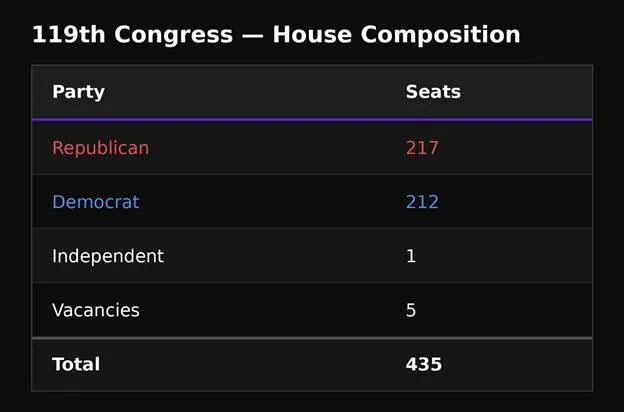

Currently, the distribution of votes between the parties is as follows (a bill requires 218 votes):

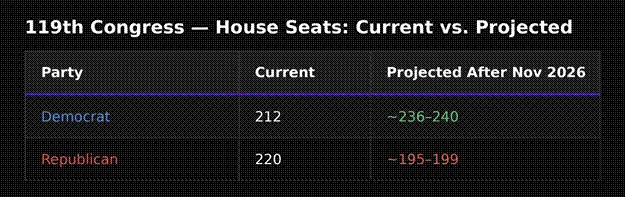

Based on Polymarket’s current odds, here is the expected party composition after the election:

After the election, the Republican Party's position in both chambers does not look optimistic. However, the Republicans can change the situation through district redistricting; when original rules lead to loss, changing the rules becomes a necessity. If Polymarket's predictions are correct, then the Republicans need to gain 19 seats. Redistricting can reduce this number.

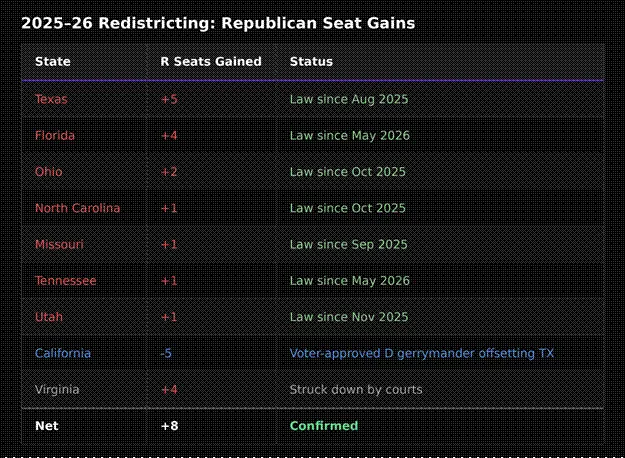

Here are the potential impacts of redistricting:

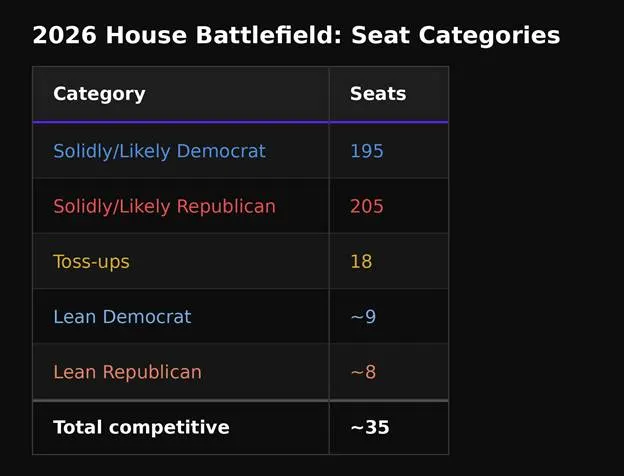

Now the Republicans only need to secure an additional 11 seats. Next, let’s take a look at which electoral battles are closely contested; based on the current polls, within the margin of error, which districts may slightly lean towards the Republicans.

There are 35 seats with significant uncertainty regarding their ownership. As mentioned earlier, high inflation and rising living costs are negative issues that make it difficult for Trump to turn around. Another topic that currently resonates with all voters from both sides is the expansion of data centers and the impact of artificial intelligence on the job market.

Except for a small number of wealthy individuals, almost everyone is worried that the construction of data centers will drive up various costs while fearing that artificial intelligence will take away jobs. Many places have enacted policies to suspend new data center projects and call for higher taxes on artificial intelligence companies to subsidize ordinary citizens. After all, the vast majority of people are neither executives of artificial intelligence companies nor high-salary practitioners.

For voters in competitive districts, these issues are very influential. Trump can completely leverage statements regarding the artificial intelligence industry to secure the remaining key seats. At this stage, it suffices to release relevant statements without needing to implement specific legislation. He only needs to promise ordinary citizens that if the Republican Party wins, they will begin rectifying the artificial intelligence industry after the election.

As a seasoned politician, Trump is always good at making campaign promises but rarely fulfills them afterward. His previous handling of the Epstein-related documents is a typical example: he loudly claimed during the campaign to thoroughly investigate the persons involved but only released a small amount of public information after taking office. Now he could do it again, claiming during the campaign to propose legislation to slow down data center expansion and impose excess profit taxes on artificial intelligence companies, with the taxes used to distribute a new round of relief funds; when the election is over and the Republican Party maintains power, he will gradually retract those statements.

Some might find it hard to understand why Trump would imitate left-wing Democratic politicians. But let’s not forget that he introduced the largest national relief plan since Roosevelt's New Deal, and even when the lower-class citizens used the relief funds for daily consumption, he did not impose any restrictions. To preserve his own political position, temporarily distancing himself from giants in the artificial intelligence field like Elon Musk and creating an image of supporting ordinary civilians is not difficult for Trump.

If Trump really makes tough statements against the artificial intelligence industry, the market will not see it simply as a campaign tactic but will recognize that the U.S. will substantially restrict capital expansion in the artificial intelligence field and increase the tax burden on the industry. Panic will spread immediately, and the artificial intelligence stock market bubble will burst accordingly.

Previously, Elon Musk and Trump publicly clashed on social platforms, with Musk’s department openly questioning Trump; Trump immediately declared he would cancel government cooperation contracts related to Musk’s companies, resulting in Tesla's stock price plummeting 18% in a single day, exemplifying the market's sensitivity to such disruptions. Politics can support industries but can also bring instant blows.

That confrontation was later confirmed to be just a media stunt, and the two quickly reconciled, with Musk even invited to attend the recent summit between Trump and Chinese national leaders in Beijing. Yet at the time, the market took it seriously, triggering massive sell-offs.

This was merely turmoil caused by their personal conflicts. Once Trump, representing the Republican Party, makes a definitive statement planning to impose heavy taxes on artificial intelligence models and related business activities, the impact will far exceed the previous instances. Similar comments have previously been heard in South Korean political circles, leading to a near-limit down on the local composite index the next day until the government issued urgent clarifications, allowing the market to return to an upward trajectory.

The current market's optimistic expectations for the artificial intelligence sector are based on the belief that the industry's revenues will continue to grow exponentially and that the concentration of new technology and wealth will not provoke public backlash. This mindset is already detached from reality, resembling being lost in a dream. And Trump's statements will become a test to shatter that illusion. Whether he will genuinely take action depends fundamentally on oil prices.

The ongoing Iranian situation will continue to push oil prices higher; the inflation problem will become increasingly severe, and Trump will have fewer options for campaign rhetoric, ultimately having to target data centers and the artificial intelligence industry.

The clear reason Trump is trying hard to avoid the Democratic Party controlling the House of Representatives is straightforward. If the Democratic Party takes the House, they can exercise subpoena power, repeatedly calling Trump himself, his family, and key aides to testify, throwing various sharp questions at them. Should the Democrats regain the White House in 2028, the Justice Department, having a wealth of leads, will commence investigations into Trump's business entities.

Let's trace the entire logic chain: If the U.S.-Iran negotiations remain unresolved, oil prices will inevitably rise; rising prices will lead to voter discontent, forcing Trump to court votes through regulations and taxation on the artificial intelligence industry.

From now until the November elections, even if AI-related stock markets plummet, it is an acceptable cost for Trump if it helps him escape the endless investigations by the Democratic Party. After the election, he can readily overturn his previous statements regarding data centers and artificial intelligence, and the industry will return to normal, and the S&P 500 index may even aim for the 10,000-point mark.

But for investors, market movements are interlinked. A drastic drop in the artificial intelligence sector will fundamentally change expectations for its future earnings. After experiencing the shocks of regulation and heavy taxation, investors will no longer blindly have confidence in this sector as they once did.

California Dream: Where Does Liquidity Flow?

Before analyzing the potential impact of the listing of three major giants—SpaceX, Anthropic, and OpenAI—on the global financial market, let me first clarify a question: Since the end of the third quarter last year, the liquidity of the dollar has continued to ease, yet Bitcoin has not experienced a synchronous significant rise. What is the reason behind this?

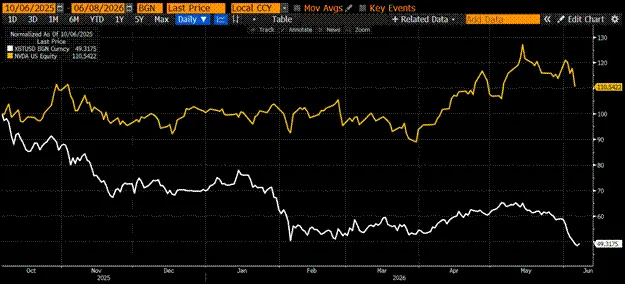

On November 30, 2022, ChatGPT was officially launched to the public, marking the beginning of the artificial intelligence super bubble. Almost simultaneously, the scandal of FTX founder SBF misappropriating user funds was completely exposed. Bitcoin, after hitting a low of about $15,000 that year, surged to $125,000 in October 2025, with a cumulative increase of over six times. But during the same period, Nvidia's stock increased elevenfold, and numerous small and mid-cap tech stocks relying on computing power and converting electricity into intelligence also saw explosive increases. The revenue performance of the artificial intelligence sector greatly outpaced that of the crypto market, and from the end of 2024 to now, the gap continues to widen.

Even when Bitcoin (white) reached its all-time high, Nvidia's (gold) returns were still superior.

Bitcoin (white) has performed worse after setting a new historical high, having since fallen 50%. Nvidia (gold), as the world's largest company by market capitalization, has still risen by 10% since the end of 2025.

According to my previous logic of assessing the crypto market based on fiat currency liquidity, Bitcoin should have experienced a greater rise in the current environment, yet the reality is completely the opposite. Where lies the problem?

I have previously focused on the overall scale of fiat currency issuance but overlooked the specific flow of funds. I initially believed that liquidity would ultimately flow into Bitcoin, driving prices up, but this time my judgment was off.

My conclusion is that nearly all the newly created liquidity in dollars has been absorbed by the artificial intelligence sector. Artificial intelligence is a capital-intensive industry; in order to create large data centers capable of operating artificial intelligence, massive amounts of energy must be consumed. Hydrocarbon energy, nuclear energy, and renewable energy are converted into electricity, which is then transmitted to data centers, where dedicated chips complete model training and inference calculations.

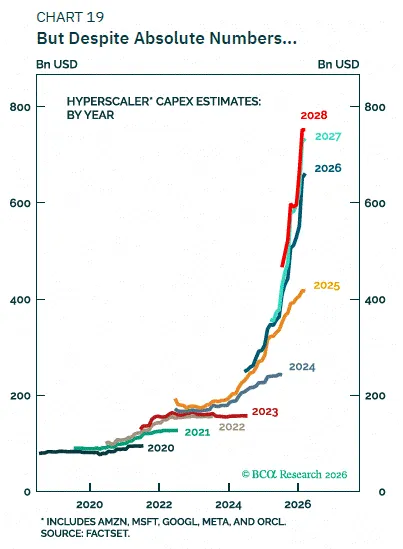

Starting from 2024, global capital expenditure for data centers will begin to surge, increasing further in 2025, leading to a skyrocketing need for industry financing. Based on publicly disclosed data, from November 2022 to now, the total amount of debt financing in artificial intelligence-related fields has reached $1.5 trillion, while during the same period, the increase in the U.S. broad money supply M2 has exactly matched at $1.5 trillion. The answer is now evident: all the newly added dollars have flowed into the artificial intelligence sector, and Bitcoin naturally does not receive any incremental funds.

Bitcoin was able to initiate a strong rebound from the lows of the FTX collapse in 2022 mainly because the large-scale debt expansions in the artificial intelligence sector were primarily concentrated after 2025. Of the $1.5 trillion in debt, approximately $1.3 trillion has been generated since 2025. Coincidentally, Bitcoin's price peak occurred in October 2025 when capital expenditures in the artificial intelligence sector also reached unprecedented levels.

This linkage is crucial. Once the artificial intelligence stock market crashes, there will be no surplus funds left in the market to position themselves in Bitcoin. Banks will tighten lending, and many institutions will realize that loans given based on false revenue data carry huge risks. When the stock prices of leading tech companies drop by over fifty percent, bank credit personnel will begin to worry that these companies will be unable to repay their debts, leading to a contraction in credit volumes, and overall market liquidity will further tighten. Coupled with the negative attitude of the U.S. political arena towards the artificial intelligence industry, the sector will find it difficult to attract substantial funding in the short term.

Even if the government subsequently intervenes to rescue financial institutions, based on current developments, such measures will only take effect after the November elections.

The relationship between Bitcoin and the stock prices of artificial intelligence companies indicates that we must make judgments on whether there’s a bubble in the artificial intelligence market, when it will burst, and what the underlying causes are.

Artificial Intelligence Bubble: Hard to Escape Triple Hits

Three major factors will burst the current artificial intelligence bubble: rising energy costs, the market’s inability to absorb the colossal IPOs of SpaceX, Anthropic, and OpenAI, and Trump's policy statements against the artificial intelligence industry.

The core logic of artificial intelligence is to maximize the efficiency of "turning energy into intelligence." Humans rely on consuming food to convert energy into wisdom, and artificial intelligence relies on electricity. Currently, the new electricity usage for data centers mostly depends on hydrocarbons like natural gas. Rising energy prices mean that the costs of operating artificial intelligence and the output of computing power will increase simultaneously, directly squeezing the profit margins of companies like Google, Anthropic, and OpenAI.

As costs rise, companies will choose to increase service prices, which will slow down the growth rate of users utilizing computing power and models. The ongoing geopolitical confrontation between the U.S. and Iran continues to push oil prices up, ultimately eating into the profitability of artificial intelligence companies. When the market starts to question the rationality of continued expansion of data centers, the turning point for the industry will arrive, and projected price-to-earnings ratios will shrink significantly, marking the formal onset of a bear market.

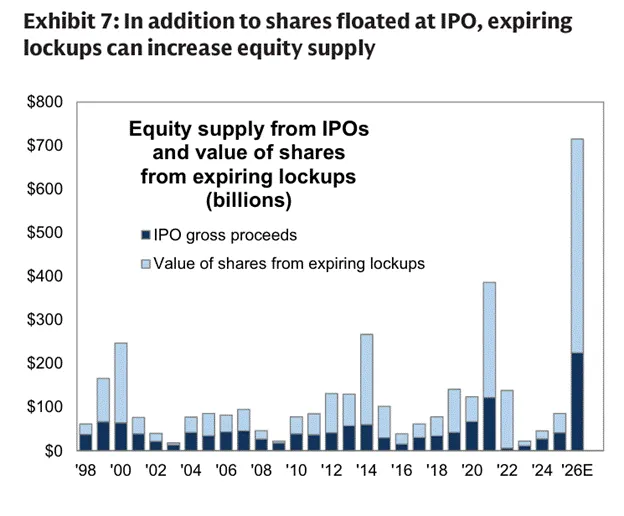

In addition, the unlocking of shares from SpaceX, Anthropic, and OpenAI, along with other tech companies, is happening sequentially, coupled with large-scale IPOs, leading to an overall financing scale that even exceeds the total financing of all new stocks during the dot-com bubble, achieving unprecedented volume. Whether the market can absorb such massive selling pressure from stocks remains a big question mark.

In recent years, the artificial intelligence sector has been on a continuous rise, predicated on investors firmly believing that industry profitability will accelerate growth. Once the market wavers regarding the industry’s prospects, investors will begin to lower their valuations for future earnings. The performance of the IPOs of these giants will become a sentiment barometer for the market. If the IPOs fall short of expectations, investors will conclude that the industry has peaked, thus starting a collective sell-off.

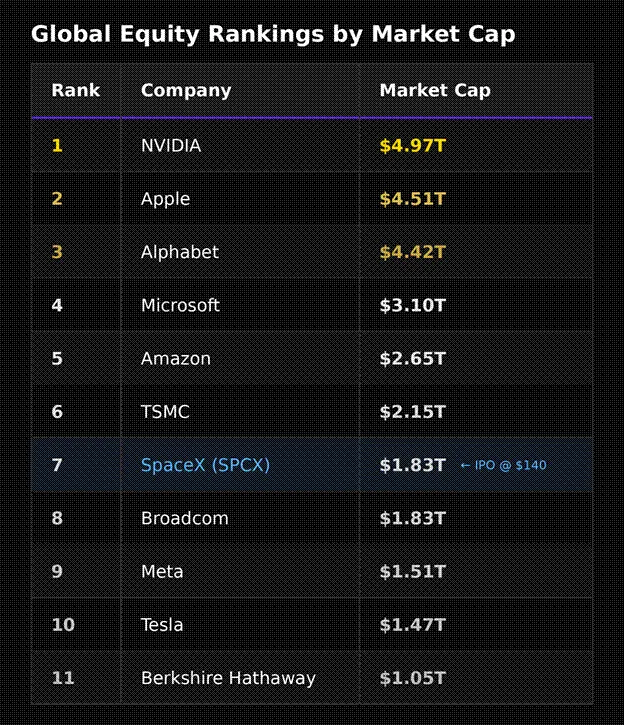

Let’s analyze using SpaceX, which has relatively complete disclosure of information, as an example. The capital market always follows the rule of "the first mover advantage," and Elon Musk, well-versed in marketing, opted to go public first, allowing the company and early shareholders to maximize their cash-out. Participants in the crypto market can easily understand this model: a very low circulating supply, fully diluted valuations yet remaining high, resembling the operational logic of some altcoins.

According to the listing documents filed by SpaceX with the U.S. Securities and Exchange Commission, this listing will be valued at nearly a hundred times its revenue. What's more noteworthy is that the company will initially release only 4% to 5% of its shares. In the current heated environment of the artificial intelligence sector, stock prices will likely surge on the first day but such high market expectations also mean it will be difficult to continue meeting investors' imaginations.

After its IPO, SpaceX's market capitalization will reach $1.8 trillion, making it the seventh largest company globally by market value. If the stock price rises another fifty percent, its market value will surpass Amazon's to rank fifth globally, though its profitability will not match that value band. Nvidia maintains its high valuation due to impressive gross margins and revenue scale, whereas SpaceX's focus on the space data center business has industry analysts pointing out that the construction and operational costs of such facilities are four times that of ground data centers, and it is expected to take a decade just to reach breakeven. If the initial valuation of the IPO was more rational, the subsequent stock price trajectory would fare even better. Participants in the crypto market are well aware of the logic: if secondary market investors cannot profit, the internal shareholders’ unlocked shares will go unsold, leading stock prices to fall continuously.

Looking at the pace of share unlocks, from now until early September, SpaceX's circulating supply will expand fivefold, flooding the market with a large number of shares, posing immense upward pressure on stock prices. Compounding the issue is that Anthropic and OpenAI also plan to initiate their IPOs in September, both targeting trillion-dollar valuations.

Between June and September this year, SpaceX may still have a brief window for price increases, but when three highly valued companies go public and a large supply of new shares floods the market, disappointment among investors is bound to spread. Investors expect explosive stock price increases, while marginal, wavy upticks will simply not meet their expectations.

In summary, rising energy prices, large IPO concentrations, and Trump's regulatory statements against the industry—a triple negative catalyst—make it difficult for these companies to perform to market expectations upon their IPOs. Once investors stop believing that AI-related companies can maintain exponential profitability growth, the entire sector's valuations will be readjusted, and stock prices will weaken collectively.

Currently, there is a significant amount of stock pledge loans in the artificial intelligence sector, and banks have provided massive credit to support industry capital expansion. Following a downturn in the sector, the banking system will suffer from massive bad debts.

In a climate of a global artificial intelligence bubble burst, where various risk assets experience a widespread downturn, Bitcoin will also find it hard to escape an independent market trend. Once the market fully clears, Bitcoin will likely hit bottom first. At that moment, in order to salvage the overall economy, the market will welcome a new round of massive monetary easing, and Bitcoin will begin to rise again. But for the time being, the primary task is to protect the principal of crypto assets.

Before sharing Maelstrom Fund's strategies regarding stocks and crypto asset holdings, let us analyze the direction of the Federal Reserve's monetary policy.

The Federal Reserve Chairman's Dilemma

The new Federal Reserve Chairman Kevin Warsh finds himself in a very delicate position, and the external evaluations of his style of acting are mixed, all depending on how he responds to the current contradictory circumstances surrounding the Federal Reserve.

The difference between the yield on two-year U.S. Treasuries and the effective federal funds rate visually reflects market sentiment; the chart also denotes the near-month WTI crude oil futures prices.

Trump nominated Kevin Warsh to serve as Federal Reserve Chairman with the intention of having him promote interest rate cuts, and Warsh previously sent signals indicating that the inflation caused by geopolitical conflicts is a short-term phenomenon, whereas productivity increases brought by artificial intelligence are a long-term trend, and the Federal Reserve could take this opportunity to lower interest rates.

However, the market has sent entirely contrary signals. The yield on two-year U.S. Treasuries is 0.5 percentage points higher than the effective federal funds rate, indicating that the market believes that due to sustained high inflation, the Federal Reserve ought to raise interest rates in the monetary policy meeting on June 16-17, rather than cut rates.

At present, the most probable outcome is that the Federal Reserve will maintain rates. However, the market will closely interpret the post-meeting press conference and any adjustments to the reserve management plan. Even if they maintain the status quo, it will be regarded by the market as either hawkish or dovish.

Hawkish interest rate stability will have effects similar to raising rates. On one hand, the U.S.-Iran conflict remains unresolved, and oil prices continue to increase; on the other hand, the three major artificial intelligence giants are going public, while the market faces supply pressure. Multiple negatives will cause all risk assets to experience varying degrees of adjustments.

The worst-case scenario would be if Trump directed Warsh to align with market calls and raise rates immediately, attempting to win voter support by suppressing prices. However, unless the Federal Reserve raises rates significantly while also selling bonds to reduce its balance sheet, it cannot keep pace with the rhythm of inflation. This situation is reminiscent of the scene in the 1970s: although the Federal Reserve raised interest rates aggressively, the increases were never sufficient to curb inflation.

Under the current environment, the possibility of the Federal Reserve lowering interest rates is extremely low. Whether they ultimately choose to raise rates or maintain them, the market will interpret it as a signal of tightening liquidity, further undermining the confidence of bulls in the artificial intelligence sector.

Combining all of the above, the rising trend of oil prices will ultimately evolve into a negative for all categories of risk assets. Next, let’s talk about the specific holdings of the Maelstrom fund.

Investment Portfolio Layout

The operation of all things in the world relies on energy. Since I judge that energy prices will rise in the future, it is inevitable to lay out energy-related assets.

At this stage, the U.S. and Iran remain at a standstill, shipping through the Strait of Hormuz is obstructed, and the daily losses in crude oil and natural gas supply are continually increasing. Market sentiment remains somewhat stable, but if this standoff continues, rising energy prices will become an inevitable result.

All types of industry data point to the same conclusion: affected by geopolitical conflicts, global energy stocks have dropped to their lowest levels in recent years and continue to decline. Once stockpiles drop below the critical threshold, the entire energy supply system will face problems, and prices will enter a runaway increase.

Even if the best outcome occurs—both parties immediately ceasefire and shipping through the Strait of Hormuz returns to normal—countries will still increase purchases due to replenishment and strategic reserve needs, keeping oil prices elevated.

Considering both scenarios, in the next three to six months, regardless of whether oil prices temporarily recede after a short-term peace agreement, the upward trend of crude oil and natural gas prices has already been established. Based on this, we are heavily investing in U.S.-listed energy production companies.

The energy sector possesses upward potential under various scenarios, and its current valuation is advantageous compared to the highly energy-dependent tech industry. In contrast, assets relying on cheap energy to maintain high valuations face an unfavorable outlook.

If oil prices rise to $150 per barrel, it will be challenging for the artificial intelligence industry to sustain its previous strong performance. Therefore, we have liquidated all relevant AI stocks.

Incremental funds have continuously flowed into the artificial intelligence stock market, and once this sector declines rapidly, even if cryptocurrencies have relative defensive qualities, it will be difficult to attract new funds. On this basis, we have reduced our holdings of all non-core cryptocurrencies. Last week, we sold HYPE, NEAR, and WLD, and due to issues with the Orchard Pool, we liquidated ZEC. At this moment, protecting capital is more important than seeking yields.

Currently, we are only holding Bitcoin and Ethereum. There are no significant cash-out needs for Ethereum, so we continue to hold. I firmly believe that the burst of the artificial intelligence bubble will trigger a new round of financial turmoil, and at that time the world will once again enter a cycle of monetary easing, with Bitcoin falling first and then rising.

In the face of market fluctuations, we will hold core positions for the long term while utilizing derivatives for short-term shorting operations to seize stage-dependent market opportunities. After all, I am reluctant to give up the joy of trading.

If it turns out that the reality of market movements does not align with my judgment and everything is just a false alarm, that’s fine as well. Securing profits before embarking on a journey in the Mediterranean is indeed a prudent choice. I will reassess the market movements and my previous judgments in early September and determine the opportunity to re-purchase shares based on the market conditions at that time.

Unlike investment institutions that need to realize fixed income every year, Maelstrom Fund places greater emphasis on long-term compounding growth, and therefore has ample leeway to calmly respond to the intertwining changes in the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。