The CPI to be announced on Wednesday is expected to approach 4.2%, the bond market is pricing in interest rate hikes in advance, while Trump is calling for rate cuts.

Written by: Zhao Ying

Source: Wall Street Journal

Newly appointed Federal Reserve Chairman Kevin Walsh is facing the toughest policy test since taking office: inflation is expected to exceed 4% this week, and the bond market has already priced in rate hike expectations, while Trump is publicly pressuring for rate cuts ahead of the monetary policy meeting. The outcome of this three-way game will determine whether Walsh can carve out an independent policy path between the will of the White House and the trust of the market.

The consumer price index (CPI) for May in the U.S. will be announced this Wednesday, and the market expects a year-on-year increase of 4.2%, up from last month's 3.8%, significantly exceeding the Fed's 2% target. Meanwhile, a strong May employment report released last Friday caused tech stocks to plummet and pushed bond yields higher, shifting market worries about uncontrollable inflation from expectations to substantial asset price pressure.

In an interview with NBC's "Meet the Press" on Sunday, Trump stated clearly: "There is no reason to raise rates. We actually should be cutting rates." He also expressed that "Kevin is great and hopes he acts on his own judgment," but quickly added that when a country is doing well, "it shouldn't immediately raise rates to punish it."

His statement both gives Walsh face and clearly communicates the White House's policy preference. The Federal Reserve will hold a rate meeting from June 16 to 17, which will be the first FOMC meeting chaired by Walsh since his formal appointment.

Inflation pressure has become a "given issue"

The market's tolerance for inflation is rapidly narrowing. PGIM Chief Investment Strategist Robert Tipp stated on Monday: "Inflation is no longer a question, but an accepted given issue." He pointed out that earlier, Fed officials hoped inflation would subside on its own, "but that judgment has not come true."

Energy prices are a significant driver of current inflation pressure. The Iran conflict has lasted for over 100 days, and since the beginning of the year, oil prices have risen about 60%. Economists note that its impact is more reflected on the inflation side rather than the growth side, reshaping the Fed's policy considerations.

Neil Dutta, head of economic research at Renaissance Macro Research, wrote in a client report on Monday that "preemptive rate cuts" by the end of 2025 "seem redundant" in the current economic environment. He believes that short-term Treasury yields will continue to rise, as "the labor market weakness that prompted the initial rate cut seems to no longer exist."

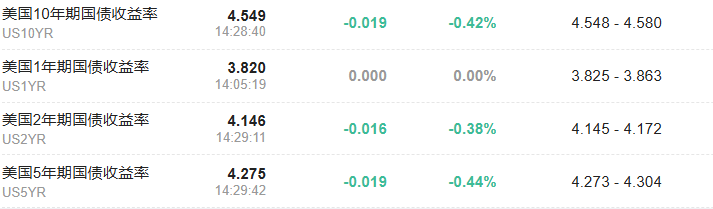

The bond market is ahead, and rate hike expectations are priced in

The bond market is ahead of Fed policy. The two-year U.S. Treasury yield, which is most sensitive to interest rates, approached 4.15% on Monday, the highest point since 2026, clearly above the Fed's current policy rate cap of 3.75%. The ten-year Treasury yield is near 4.55%, and the thirty-year yield has risen above the 5% mark again.

Tipp stated that the market will not resist the Fed's "very slow and cautious rate hikes to ensure price stability" since "higher rates have already been partially absorbed by the market."

Brad Conger, Chief Investment Officer at Hirtle & Co., pointed out that if the Fed ultimately chooses to raise rates, long-term Treasuries may actually benefit. "This would indicate that the Fed does not have a unilateral inclination," he said, "and the market will respond positively to this."

AI narrative becomes the last bulwark for the stock market

Despite high inflation and interest rate risks, stock market investors are still tightly holding onto the AI theme. On Monday, semiconductor stocks rebounded across the board, with Marvell Technology rising about 9.6%, Micron Technology increasing about 9.9%, the iShares MSCI South Korea ETF (EWY) rising about 6% with heavy holdings in Samsung, and the Philadelphia Semiconductor Index (SOX) overall increasing by more than 5%, partly offsetting the declines caused by last Friday's employment data shock.

However, Conger remains vigilant. "What we are most worried about is the AI capital expenditure cycle," he said. If long-term Treasury yields rise further, it will increase the financing costs of AI infrastructure in the debt market, while large tech companies have only recently begun to consider introducing equity financing as a supplement. "Given the current intensity of sentiment, any disturbance could shift the story from excitement to fleeing," he said.

Walsh's debut: three signals determine the policy shift

Michael Gapen, Chief U.S. Economist at Morgan Stanley, stated, "One of the key outcomes of the meeting is to see how much Walsh aligns with hawkish views." Analysts will focus on three dimensions: whether the policy statement removes "accommodative bias" wording, whether the dot plot shows rate hike expectations, and whether the risk distribution chart tilts towards inflation. If the above signals appear simultaneously, it will mark a significant shift in the Fed's easing cycle since late summer 2024.

The Fed officials have now entered a quiet period. After the June 17 statement is released, Walsh will host his first press conference since taking office. The market also expects him to provide clear signals regarding communication mechanism reforms—one of his core promises during his campaign for Fed Chair.

The choice facing Walsh is unavoidable: between inflation data, bond market pressures, and the will of the White House, his first policy statement will provide the external world with the first answer to judge his independence.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。