Original Title: "When Stablecoins Target the Payment Market, Can Traditional Payment Giants Still Hold Their Throne?"

Original Author: 100y

Original Translation: Saoirse, Foresight News

Translator's Note: Nowadays, the presence of stablecoins is no longer limited to the realm of cryptocurrency trading. With the potential to change the backend of the financial system, they are quietly knocking on the door of the payment market. You may wonder how this emerging role will disrupt the traditional payment landscape? The article holds the answer: on one hand, attempts are being made to collaborate with card organizations like Visa and Mastercard to embed stablecoin functionality within existing networks; on the other hand, there is a desire to bypass card organizations and banks, creating a new payment system. PayPal's PYUSD and the USDC payment system jointly launched by Shopify are vivid examples of this transformation. Will stablecoins become a threat to traditional payment giants, or will they give rise to a new industry ecosystem? This article will explore the context and direction of this transformation in the payment field with you.

Although the current application of stablecoins is mostly concentrated in the cryptocurrency trading sector, blockchain and stablecoins are expected to change traditional financial systems, such as the securities market and payment systems.

In recent years, the application momentum of stablecoins in payment systems has been increasingly strong, primarily advancing along two directions: 1) integrating stablecoin functionality centered around card organizations; 2) attempting to completely bypass card organizations and issuing banks.

In the latter direction, PayPal's PYUSD and the USDC payment system jointly launched by Shopify, Coinbase, and Stripe are typical cases. As the stablecoin industry develops, it is expected that more companies with a large user and merchant base will build dedicated payment systems, which may pose a threat to banks and card organizations.

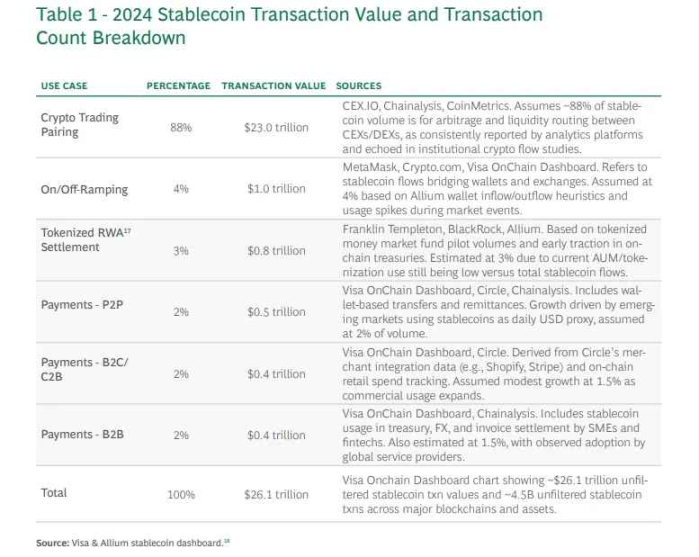

The Use of Stablecoins is Still Dominated by Exchanges

Source: BCG

Whether in the United States or globally, stablecoins are receiving significant attention. Discussions are actively underway regarding their innovative potential in remittances, payments, real-world assets (RWAs), and interbank settlements. However, according to a report by Boston Consulting Group (BCG), 88% of stablecoin transaction volume in 2024 will come from cryptocurrency trading. This data reflects the current limitations of stablecoin usage, which has not yet achieved the widespread application in the real world that we expect.

Stablecoins Can Fundamentally Change the Financial System

Although advancements in financial technology have significantly optimized user experience in the financial system, the backend systems handling actual transactions still face inefficiencies and outdated technology. In this regard, blockchain and stablecoins are expected to bring innovation to the backend of the financial system. This is not merely a supplement to existing infrastructure but can provide a technology that completely replaces the current model, similar to historical transformations in the financial system.

Securities Market

The complexity of the backend system in the securities market stems from the paperwork crisis that erupted in the U.S. securities market in the 1960s and 1970s, along with a series of policy measures introduced to address this crisis. At that time, securities trading relied entirely on paper documents, and with the surge in trading volume, the entire system nearly collapsed. In response, the U.S. Congress passed the Securities Investor Protection Act (SIPA) and amended the Securities Act, establishing a centralized clearing and settlement mechanism and an indirect securities holding system.

Initially, this system digitized securities ownership and improved settlement efficiency. However, it also made numerous intermediaries, such as brokers, clearinghouses, and custodians, indispensable, leading to structural complexity and cost issues. Today's securities market is essentially a product of policy compromise and gradual improvements to overcome technological limitations. This system has been in place for decades before the emergence of more advanced technologies like blockchain.

Cross-Border Remittances

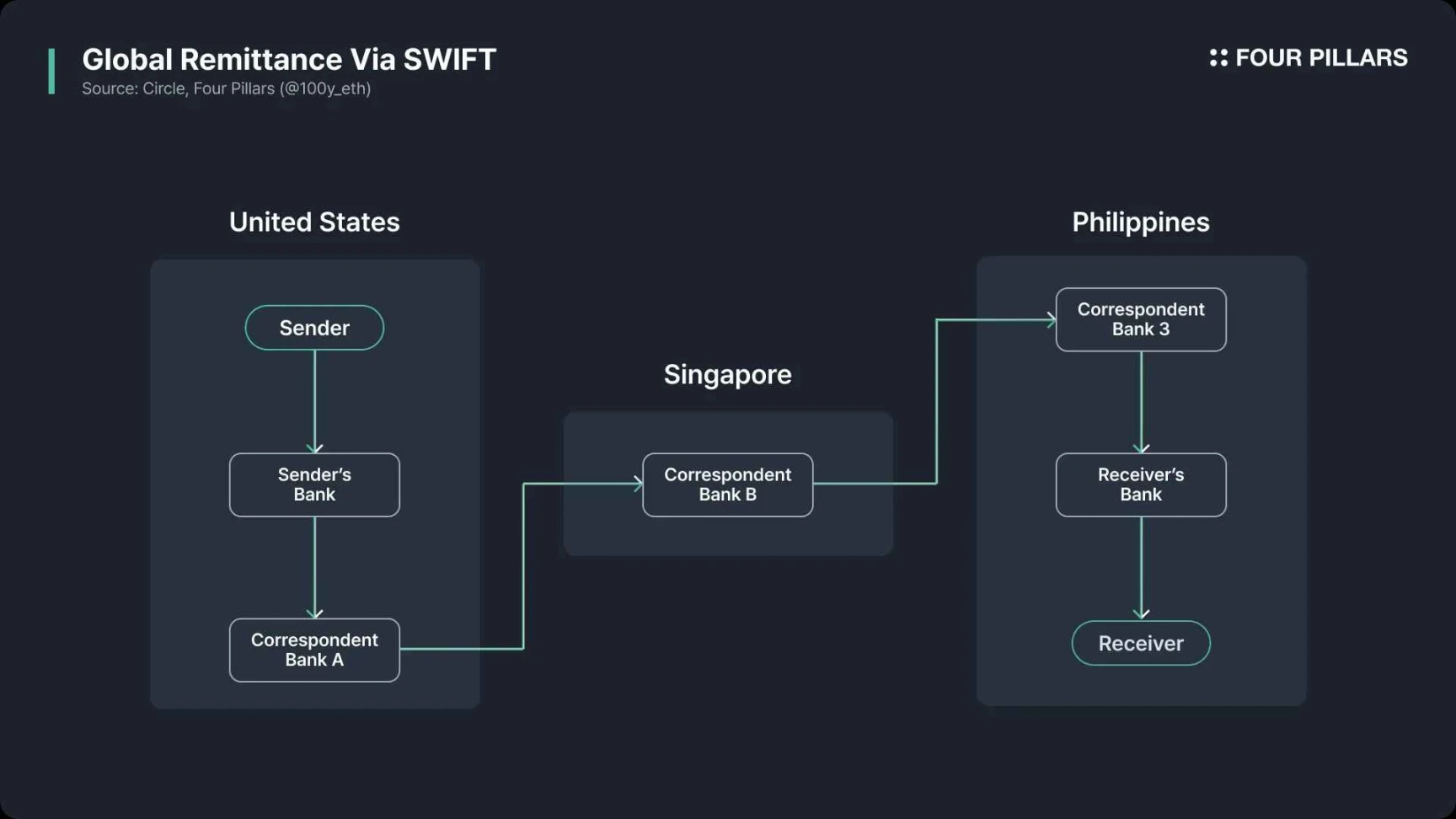

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is currently the most widely used system in the field of cross-border remittances. It was established in 1973 by 239 banks in Brussels as a global messaging network. Its creation aimed to replace the then-existing telex-based international interbank communication system, which was slow and prone to errors, and where each bank used its own communication standards, leading to poor compatibility, inefficiency, and security risks. The emergence of SWIFT was to solve these problems by providing a universal communication standard and secure network.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is currently the most widely used system in the field of cross-border remittances. It was established in 1973 by 239 banks in Brussels as a global messaging network. Its creation aimed to replace the then-existing telex-based international interbank communication system, which was slow and prone to errors, and where each bank used its own communication standards, leading to poor compatibility, inefficiency, and security risks. The emergence of SWIFT was to solve these problems by providing a universal communication standard and secure network.

However, SWIFT itself is only responsible for transmitting information; the actual flow of funds must be completed through correspondent banks or central bank accounts, with settlements handled separately. The entire process involves multiple intermediary banks, each of which can cause delays due to fees, KYC/AML reviews, currency exchanges, time zone differences, and holidays, ultimately resulting in high costs and low transparency for cross-border remittances. If blockchain and stablecoins had been available at that time, information transmission and fund transfers could have been completed on the same unified platform, leading to a qualitative leap in the efficiency of cross-border payment infrastructure.

Can Stablecoins Transform the Payment Market?

Despite the heated discussions about the innovative potential of stablecoins in various fields such as the securities market and cross-border remittances, the next most anticipated application scenario outside of exchange trading is the payment system. In fact, in the payment field, not only Web3 companies but also mainstream Web2 companies like Visa, Mastercard, Stripe, and PayPal are actively exploring new business opportunities.

To determine whether stablecoins can truly change the existing payment system, we first need to understand how the current payment system operates, the root causes of its inefficiencies, and whether stablecoins can address these issues.

How the Existing Payment System Operates

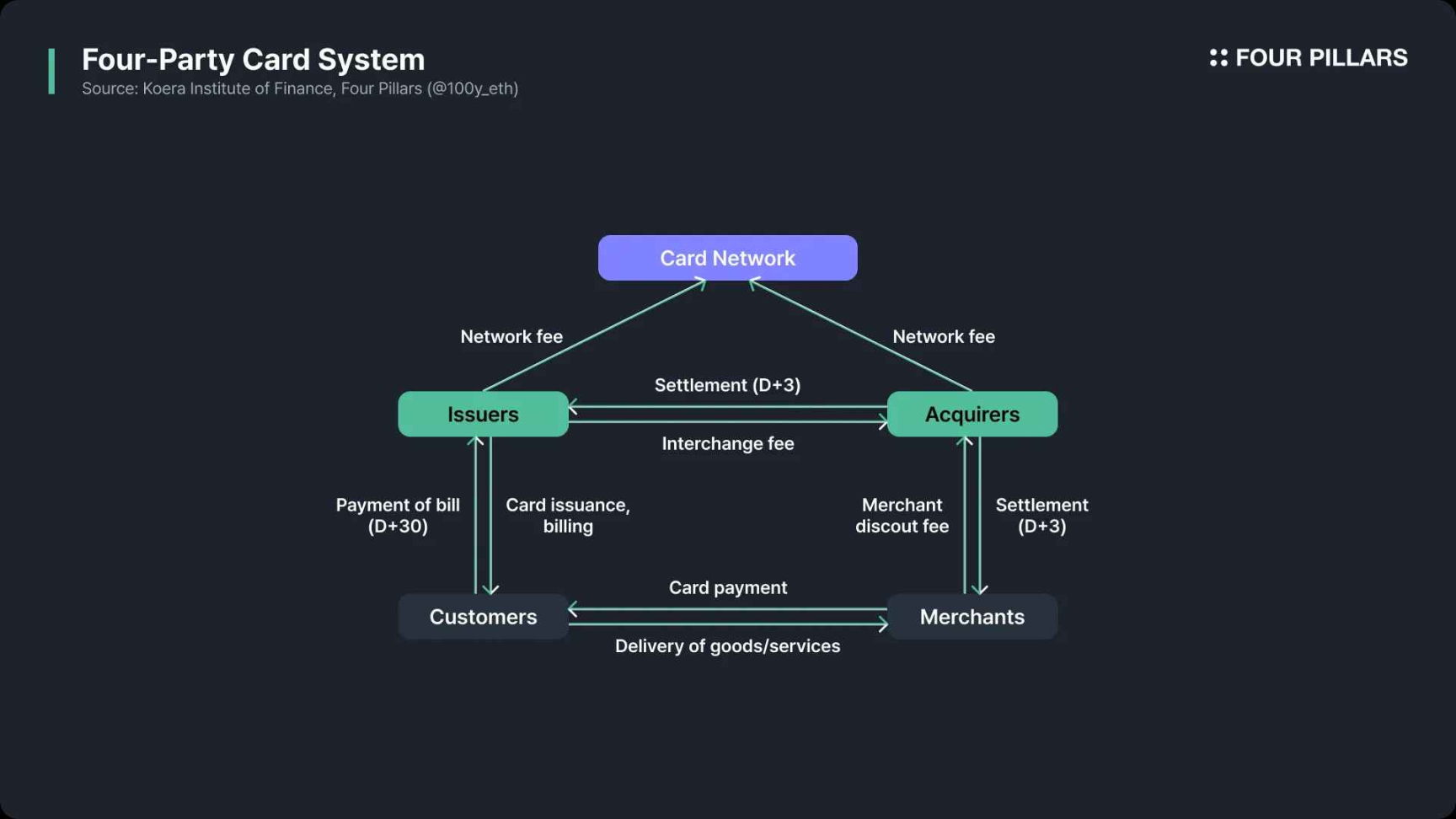

First, let's understand the payment system's operational process. When a customer makes a payment to a merchant, the process is as follows:

Authorization

The customer attempts to complete the payment using a bank card.

The POS terminal or online payment gateway sends an authorization request containing payment information to the acquiring institution.

The acquiring institution forwards the request to the card organization (such as VisaNet or Mastercard's banking network).

The card organization passes the request to the issuing bank.

Verification

The issuing bank verifies the validity of the bank card, account balance, credit limit, and whether there are any suspicious risks associated with the transaction.

Once verification is complete, the approval or denial result is returned to the acquiring institution through the card organization.

If the transaction is approved, the corresponding amount will be temporarily frozen in the customer's account.

If the transaction is denied, the merchant will receive feedback containing the reason for the denial.

Capture Confirmation

- In certain industries such as gas stations, hotels, and online shopping, the final amount is confirmed only after the initial authorization. Therefore, the moment the merchant sends the "capture confirmation request" is the actual completion point of the transaction, and this request is sent to the acquiring institution.

Batching

- Throughout the day, authorized transactions will be aggregated into a batch and sent to the acquiring institution in one go after business hours.

Clearing and Interchange

The acquiring institution sends the batch transaction data to the card organization.

The card organization sends each transaction to the corresponding issuing bank and calculates the interchange fee in the process.

Settlement

- Funds are transferred from the issuing bank's settlement account to the acquiring bank's settlement account. The card organization will summarize daily transactions and generate settlement files to coordinate settlements between both parties, but the actual transfer of funds must be completed through the interbank payment network.

Funding

- The acquiring institution deposits the payment amount, after deducting relevant fees, into the merchant's account, usually completed through Automated Clearing House (ACH) or wire transfer.

Reconciliation

- Finally, the merchant checks whether the funds received match their own records, looking for discrepancies, transaction omissions, or duplicate charges.

What Problems Exist in the Current Payment System?

The two major issues often criticized in traditional card systems are high fees and slow settlement speeds. Are these defects unavoidable, or can they be resolved?

Source: a16zcrypto

Regarding Payment Fees

Let's first look at the composition of fees for card payments. From the merchant's perspective, card transactions involve three main types of fees:

Interchange fee: The largest portion, charged by the issuing bank.

Card organization service fee: The fee charged by the card organization for processing the transaction.

Acquiring institution markup fee: The service fee charged by the acquiring bank.

Can blockchain and stablecoins reduce these fees? The first potential cost-saving point lies in global transactions. When the merchant and cardholder are in different countries, settlements must go through the SWIFT system, but if this process is replaced with blockchain or stablecoins, costs can be significantly reduced.

The second cost-saving point is bypassing card organizations and issuing banks. The essence of card organizations is to connect the customer's bank with the merchant's receiving bank through a communication network, but if stablecoin payments are fully adopted, customers can transfer directly from their self-custodied stablecoin wallets to the merchant's Web3 account via the blockchain network.

Regarding Settlement Time

Next, let's look at settlement time. The transaction authorization for card payments is almost completed in real-time, and in this regard, the scalability of public blockchain networks may not match that of centralized card organizations. However, in traditional card payments, clearing usually takes an additional 1-2 days, and settlement takes 1-5 days.

There are many reasons for the lengthy settlement times, some of which can be resolved, while others are difficult to avoid:

Clearing Cycle: Card payments typically aggregate daily transactions into batches, with clearing occurring only once a day. In a system fully based on blockchain or stablecoins, there is no need to adhere to this single-day clearing cycle.

Disputes, Suspicious Transactions, Cancellations, and Refunds: Even with stablecoin payments, these issues cannot be eliminated. Since such situations are difficult to avoid during the payment process, there remains a necessity for settlement delays.

Cross-Border Payments: In cross-border transactions, funds must be settled through the SWIFT system, which further exacerbates delays. Clearly, blockchain can provide solutions in this area.

Stablecoin-Based Payment Systems

Recently, various financial institutions and companies have begun to adopt stablecoin-based payment systems. I believe this significant shift is primarily driven by two strategies: the first is led by card organizations like Visa and Mastercard; the second is an attempt to completely bypass card organizations and issuing banks.

Stablecoin Payments Centered Around Card Organizations

As I mentioned in my article "Visa and Mastercard: Designing Next-Gen Payment Systems," Visa and Mastercard are actively exploring ways to integrate stablecoin functionality into their infrastructure.

Crypto Debit Cards: These cards allow customers to make payments using stablecoins stored in Web3 wallets or exchange accounts. Specifically, there are two ways to handle the customer's stablecoins: one is to convert them into fiat currency by the issuing bank and process them through the existing payment system; the other is for the card organization to directly receive stablecoins through a funding account, completing the transaction according to the traditional card payment process.

Stablecoin Settlement: As mentioned earlier, card organizations can receive stablecoins through funding accounts and can also use stablecoins to settle with acquiring institutions.

Essentially, stablecoin payments centered around card organizations merely add support for stablecoin payments and settlements within the traditional system, without changing the participants or infrastructure. Therefore, this model does not offer significant advantages in terms of cost and efficiency. However, for customers and businesses that natively use stablecoins, this model can eliminate the need for fund inflows and outflows, reducing transaction friction; additionally, if the entire payment process is settled in stablecoins, cross-border transactions will benefit significantly.

Attempts to Bypass Card Organizations and Issuing Banks

At the same time, some payment service providers (PSPs) have begun to bypass card organizations like Visa and Mastercard, directly using stablecoins to process payments. Typical cases include PayPal's PYUSD payment and the USDC payment solution jointly launched by Shopify, Coinbase, and Stripe.

PYUSD Payment Solution

PayPal users can complete payments using their PYUSD balance within the app. These PYUSD are not stored in the user's personal wallet but are held by the issuer Paxos. When a PYUSD payment occurs, there is no actual on-chain transfer; instead, the ownership of PYUSD is internally transferred from the customer to the merchant within PayPal's backend system. If the merchant wishes to settle in fiat currency, PayPal will convert PYUSD to USD at a 1:1 ratio and transfer the funds to the merchant's account through bank networks like ACH (Automated Clearing House).

If the customer's PYUSD balance is insufficient, they can recharge through a bank account or debit card (which may incur fees); similarly, if the merchant requests fiat settlement, processing through the bank network will also incur additional fees and time costs. However, if the entire payment cycle is completed in PYUSD, it can significantly shorten time and reduce costs by bypassing card organizations or issuing banks.

Shopify and Coinbase, Stripe Joint Payment Solution

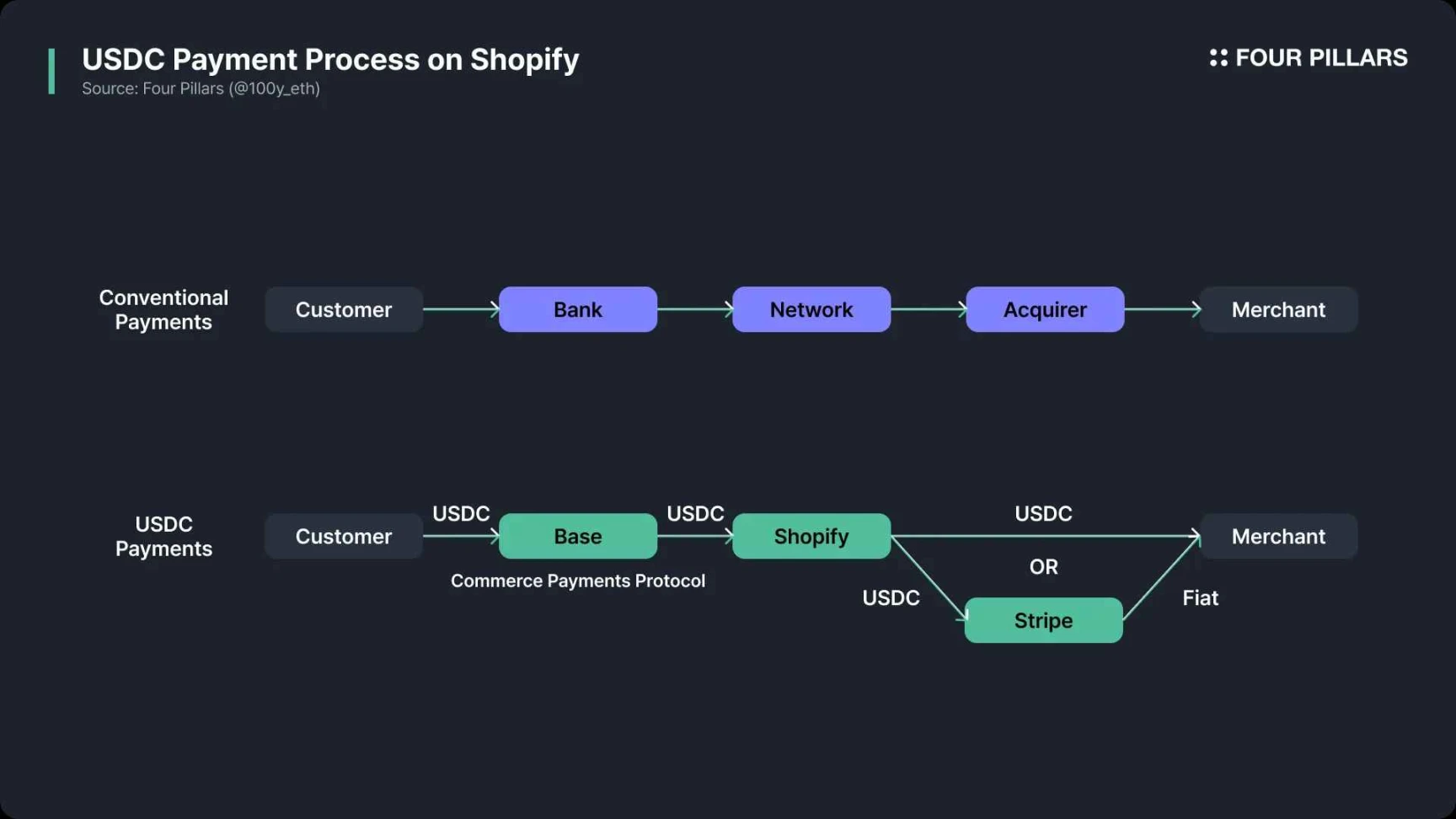

Unlike PayPal, which uses stablecoins in the payment process without directly involving the blockchain network, Shopify's USDC payment solution goes a step further.

In June 2025, Shopify announced a partnership with Coinbase and Stripe to integrate USDC payments into Shopify Payments. Customers can choose USDC as a payment method when checking out in Shopify stores and complete the payment through a crypto wallet holding USDC connected to the Base network.

In this process, the smart contract "Commercial Payment Agreement" on the Base network adopts the traditional "authorize first, then capture" model to complete payment authorization in advance, while the actual fund transfer is delayed. Shopify and Coinbase will aggregate the day's USDC transaction data and complete the clearing on the Base network.

The default method for the settlement phase is that Shopify converts USDC into the local fiat currency of the merchant through Stripe's infrastructure and deposits it into the merchant's account via bank payment networks like ACH or SEPA. Merchants can also choose to receive settlement funds directly in USDC, allowing for faster access to funds.

Summary and Thoughts

The most frequently asked question about stablecoin-based payment systems is: "Since blockchain transactions are essentially irreversible, how do we handle cancellations or refunds?" Although a fully peer-to-peer payment system may eventually emerge between customers and merchants, issues such as fraud detection, chargebacks, and refunds will always exist, thus necessitating the presence of intermediaries in the payment process. This indicates that the roles traditionally played by card organizations and issuing banks will not completely disappear.

However, in the aforementioned cases of PayPal and Shopify's stablecoin payments, intermediaries like PayPal and Stripe act as payment service providers (PSPs), responsible for handling fraud detection, transaction cancellations, refunds, and other issues. Specifically, PYUSD transactions are not processed on-chain but are completed within PayPal's backend system, leaving room for dispute resolution; in Shopify's case, the "Commercial Payment Agreement" smart contract on the Base network does not immediately approve payments but introduces a buffer time to handle potential disputes. Additionally, the issuer of USDC, Circle, has launched a "Refund Agreement" for non-custodial dispute resolution in stablecoin payments.

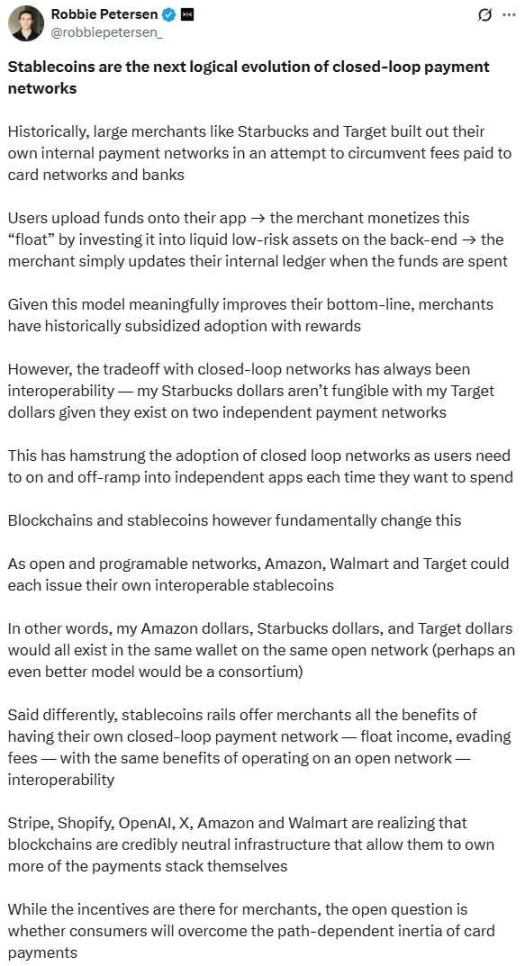

Source: X (@robbiepetersen_)

Stablecoin-based payments are an inevitable trend for the future. The issuance phase is crucial, and the circulation phase should not be overlooked. As Robbie Petersen from Dragonfly pointed out, companies with a large merchant and user base will increasingly adopt stablecoin payments, thereby bypassing card organizations and issuing banks. Stablecoins may even enable interoperability between such closed-loop payment systems. Given these trends, stablecoins may pose a real threat to card organizations and issuing banks, which need to explore new opportunities in the unstoppable wave of stablecoins.

[Disclaimer] The market has risks, and investment should be cautious. This article does not constitute investment advice, and users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances. Responsibility for investments made based on this rests solely with the investor.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。