Author: Saurabh Deshpande

Original Title: Capital Formation in Crypto

Compiled and Organized by: BitpushNews

Coinbase's acquisition of Echo for $400 million, along with experiments like the perpetual put options from Flying Tulip, indicates that financing methods are being completely restructured.

These models may differ, but they share a common goal of seeking fairness, liquidity, and credibility for new projects in raising and deploying funds.

Coinbase's Vertical Integration

Recently, Coinbase acquired the community financing platform Echo, founded by Cobie, for approximately $400 million.

The same transaction also included a $25 million NFT purchase aimed at reviving a podcast, imposing binding obligations on hosts Cobie and Ledger Status to produce eight new episodes of content after the NFT activation. Echo has facilitated over 300 rounds of financing, totaling more than $200 million.

This acquisition follows Coinbase's recent purchase of Liquifi, completing a full service stack for crypto project tokens and investments.

Project teams can use LiquiFi to create tokens and manage equity structures, raise funds through Echo's private groups or Sonar's public offerings, and then list the tokens on the Coinbase exchange for secondary market trading. Each stage creates revenue opportunities:

LiquiFi charges token management service fees, Echo gains value through profit-sharing arrangements, and Coinbase earns transaction fees from the listed token trades.

This integrated service stack allows Coinbase to profit from the entire project lifecycle, not just the trading phase.

This is a good deal for Echo, as generating sustainable income without upward integration with an exchange would be challenging. Currently, the model focuses on performance fees, which may take years to monetize, similar to venture trading.

Why would Coinbase pay such a high price for a product that only assisted in financing half of the acquisition amount (referring to Echo's assistance in financing $200 million while the acquisition price is $400 million)?

Keep in mind that $200 million is not Echo's revenue, but merely the total value of the financing it assisted with.

The consideration Coinbase paid includes the association with Cobie (who is regarded as one of the long-term excellent participants in the crypto space), Echo's network effects, technological infrastructure, regulatory positioning, and its status in the emerging crypto capital formation framework.

Well-known projects like MegaETH and Plasma have raised funds through Echo, with MegaETH opting for a follow-up financing round via Echo's public offering platform Sonar.

This acquisition has earned Coinbase the trust of founders who are skeptical of centralized exchanges, allowing it to tap into a community-driven investment network and gain the infrastructure to far exceed the pure cryptocurrency space, expanding into tokenized traditional assets.

Each project has three to four stakeholders: the team, users, private investors, and public investors. Achieving the right balance between incentives and token distribution has always been challenging. When the crypto space launched ICOs from 2015 to 2017, we viewed it as an honest model for "democratizing" early project investment channels. However, some sales sold out even before you could connect with MetaMask, while private placements adopted whitelist systems, effectively shutting out most retail buyers.

Of course, this model must also evolve due to regulatory concerns, but that's another topic. However, the story here is not just about Coinbase's vertical integration; the focus is on how the financing mechanism itself is evolving.

Flying Tulip's Perpetual Put Options

Andre Cronje's Flying Tulip aims to build a full-stack on-chain exchange that integrates spot trading, derivatives, lending, money markets, native stablecoins (ftUSD), and on-chain insurance into a unified cross-margin system. Its goal is to compete with Coinbase and Binance while contending with rivals like Ethena, Hyperliquid, Aave, and Uniswap at the product level.

The project raised funds using an interesting mechanism that embeds perpetual put options. Investors contribute assets to receive FT tokens at a price of $0.10 each (10 FT tokens for every $1 invested), with the tokens locked. Investors can destroy FT tokens at any time to redeem up to 100% of their initial invested principal. If someone invested 10 ETH, they can redeem 10 ETH at any time, regardless of the market price of FT.

The put option never expires, hence the term "perpetual." Redemptions are managed by an independent on-chain reserve funded by the raised capital, settled programmatically, and equipped with queuing and rate-limiting mechanisms to prevent abuse while maintaining solvency. If the reserve is temporarily insufficient, requests enter a transparent queue and are processed in order once funds are replenished.

This mechanism creates three options for investors and keeps incentives aligned.

- First, investors can hold the locked tokens and retain redemption rights, capturing any upside potential from the protocol's success while maintaining downside protection.

- Second, they can redeem their original principal by destroying the tokens, after which the tokens are permanently destroyed.

- Alternatively, they can transfer the tokens to CEX/DEX for withdrawal, but the put option immediately becomes void upon withdrawal, and the released original principal is used by Flying Tulip for operations and token buybacks. This creates strong deflationary pressure: selling tokens means losing downside protection. Secondary market buyers do not receive redemption rights. This protection is only available to participants in the initial sale, creating a dual-token structure with different risk profiles.

The capital deployment strategy addresses an obvious paradox: since all raised funds have perpetual put options, the team cannot actually utilize these funds, making the effective fundraising amount zero.

Instead, the raised $1 billion will be deployed into low-risk on-chain yield strategies, targeting an annual yield of about 4%. This capital can be called upon at any time. This generates about $40 million annually, allocated to operational expenses (development, team, infrastructure), FT token buybacks (creating buying pressure), and ecosystem incentives.

Over time, fees from trading, lending, clearing, and insurance will increase additional sources of buyback funds. For investors, the economic trade-off is to forgo the 4% yield they might earn by deploying capital themselves in favor of obtaining FT tokens with upside potential and principal protection. Essentially, investors will only exercise the put option when the FT trading price falls below the $0.10 purchase price.

Yield is just one component of the income stream. In addition to lending, the product suite includes automated market makers (AMM), perpetual contracts, insurance, and a delta-neutral stablecoin that continuously earns yield.

Beyond the expected $40 million income from deploying $1 billion into various low-risk DeFi strategies, other products may also generate revenue.

Top perpetual contract trading venues like Hyperliquid have achieved monthly fee revenues of $100 million, which is nearly double the income that $1 billion capital could earn through DeFi lending at a 5-6% yield.

The token distribution model is fundamentally different from all previous crypto financing methods. Traditional ICOs and venture-backed projects typically allocate 10-30% to the team, 5-10% to advisors, 40-60% to investors, and 20-30% to foundations/ecosystems, usually with lock-up periods but guaranteed allocations. Flying Tulip allocates 100% of the tokens to investors (both private and public) at launch, with the team and foundation receiving an initial allocation of 0%. The team only gains exposure through public market buybacks funded by a share of protocol revenue, bound by a transparent published timeline. If the project fails, the team receives nothing. The supply starts with 100% owned by investors and gradually shifts to the foundation over time through redemptions, with redeemed tokens permanently destroyed. The token supply has a cap set based on actual raised funds. If $500 million is raised, only 5 billion FT tokens are minted; the fundraising window cap is 10 billion FT tokens (corresponding to $1 billion fundraising).

This new mechanism addresses the issues Cronje himself experienced in the Yearn Finance and Sonic projects.

As he explained in the pitch document: "As a founder who has participated in two large token projects (Yearn and Sonic), I am acutely aware of the pressure that tokens bring. The token itself is a product. If the price falls below the entry price for investors, it can lead to short-term decision-making choices that may harm the protocol for the sake of token interests. Providing a mechanism that allows the team to feel secure, knowing there is a bottom line and that 'in the worst case' investors can also get their principal back, will greatly alleviate this pressure and overhead."

Perpetual put options separate the token mechanism from operational capital, eliminating the pressure to make protocol decisions based on token prices, allowing the team to focus on building sustainable products. Investors are protected but simultaneously incentivized to hold for upside gains, making the token less "make-or-break" for the project's survival.

The self-reinforcing growth flywheel described in Cronje's document outlines the economic model: $1 billion in funds generating $40 million in annual yield at 4% is allocated between operations and token buybacks; protocol launches generate additional fees from trading, lending, clearing, and insurance; these revenues fund more buybacks.

Redemptions plus buybacks create deflationary supply pressure; reduced supply plus buying pressure drives price appreciation; higher token value attracts users and developers; more users generate more fees, funding more buybacks; and the cycle continues. If protocol revenue eventually exceeds initial yields, allowing the project to sustain itself beyond the initial donations, then the model is successful.

On one hand, investors gain downside protection and institutional-level risk management. On the other hand, they face the real opportunity cost of a 4% yield each year, as well as the capital efficiency loss from funds being locked up earning below-market returns. The model only makes sense when the FT price appreciates significantly above $0.10.

Funding management risks include DeFi yields dropping below 4%, yield protocols (like Aave, Ethena, Spark) failing, and whether the annual $40 million is truly sufficient to fund operations, competitive products, and meaningful buybacks. Additionally, for Flying Tulip to surpass peers like Hyperliquid, it must genuinely become a liquidity hub, which is a tough battle given that existing participants have already gained a head start and captured the market with excellent products.

With a team of 15 people, building a full-stack DeFi system to compete with mature protocols that have a significant first-mover advantage carries execution risks. Few teams can match the execution power of Hyperliquid, which has generated over $800 million in fees since November 2024.

Flying Tulip embodies the evolution of lessons learned from Cronje's previous projects.

Yearn Finance (2020) pioneered a fair launch model with zero founder allocation (Andre had to mine his YFI), skyrocketing from $0 to over $40,000 within months and reaching a market cap of over $1.1 billion in just one month. Flying Tulip adopts the same zero team allocation but adds institutional support ($200 million, while Yearn was self-funded with $0) and investor protections that Yearn lacked.

The unexpected beta release of Keep3rV1 in 2020 (where the token surged from $0 to $225 in a few hours) highlighted the risks of unverified, sudden releases; Flying Tulip implemented audited contracts and clear documentation before its public sale. Experiences from the Fantom/Sonic projects regarding token price pressure directly shaped the put option model.

Flying Tulip seems to combine the best elements—fair distribution, no team allocation, structured launch, and investor protection achieved through a novel perpetual put option mechanism. Its success depends on the quality of the product and whether it can attract liquidity from strong users who are already accustomed to competitors like Hyperliquid and centralized exchanges.

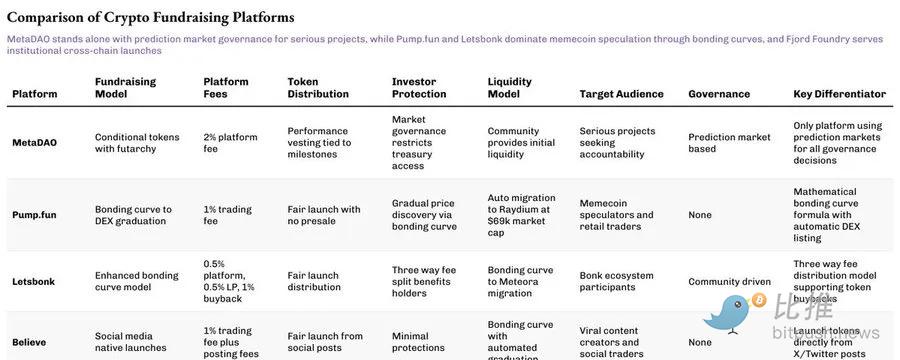

MetaDAO Financing Supported by Futarchy

If Flying Tulip reimagines investor protection, then MetaDAO reexamines the other half of the equation: accountability.

Projects raising funds through MetaDAO do not actually receive the capital they raise. Instead, all capital is stored in an on-chain treasury, with market conditions validating each expenditure. The team must propose how they intend to spend, and token holders bet on whether these actions will create value. Only if the market agrees will the transaction proceed. This rewrites financing as governance, where financial control is distributed, and code replaces trust.

Umbra Privacy is a groundbreaking example. This Solana-based privacy project secured over $150 million in committed investments, while its market cap was only $3 million, with allocations made proportionally and excess amounts automatically refunded by smart contracts. All team tokens are locked until after price milestones, meaning founders can only realize value when the project truly grows. The result was a 7x performance post-launch, proving that even in a seasoned market, investors still crave fairness, transparency, and structure.

The MetaDAO model may not yet be mainstream, but it restores what the crypto space once promised: a system where the market, not managers, decides what is worthy of funding.

Current cryptocurrency financing is entering a reflective phase, with many inherent perceptions being challenged:

- The Echo case proves that even without direct access to exchanges, financing channels with quality community resources have significant valuation potential;

- The Flying Tulip experiment is validating whether new investor protection mechanisms can replace traditional token economic models.

These explorations are reshaping our understanding of the value logic in the crypto market.

The success of these experiments hinges not on how perfect the theory is, but on actual execution, whether users are willing to pay, and whether these mechanisms can withstand the pressures of the market.

The continuous innovation in financing models fundamentally stems from the unresolved core contradictions between project teams, investors, and users.

Each new model claims to better balance the interests of all parties, but ultimately must face the same reality test—whether it can establish a foothold in the real market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。