Original Title: Making Sense of Bitcoin's Changing Market Rhythm

Original Author: Tanay Ved, Coin Metrics

Original Translation: Luffy, Foresight News

TL;DR

· As long-term holders gradually sell off in batches and new participants absorb the supply, the turnover rate of Bitcoin's supply is slowing down, showing a more stable state of ownership transfer.

· Since the beginning of 2024, only spot Bitcoin ETFs and crypto treasuries (DAT) have absorbed about 57% of the supply increment from short-term holders, currently accounting for nearly a quarter of the circulating Bitcoin over the past year.

· Actual volatility continues to stabilize, marking a maturation of market structure characterized by institutional demand dominance and extended cycle rhythms.

After reaching an all-time high earlier this year, Bitcoin has been largely in a consolidation phase, briefly dipping below the $100,000 mark for the first time since June. Macroeconomic headwinds, a weak stock market, and a rare large-scale cryptocurrency liquidation event have collectively suppressed market sentiment, slowing capital inflows and raising doubts about the sustainability of the Bitcoin bull market. Additionally, concerns about large holders transferring or selling early positions have intensified, putting pressure on Bitcoin and the entire cryptocurrency market. Following the recent decline, the total market capitalization of the cryptocurrency market is approximately $3.6 trillion.

Beneath the surface, Bitcoin's on-chain data provides important context. In this article, we will explore how changes in Bitcoin holder behavior and core demand drivers affect market sentiment and define the rhythm of this cycle. By analyzing changes in active supply and demand channels, we will investigate whether recent market fluctuations signal profit-taking at the end of the cycle or a structural shift in Bitcoin ownership.

Supply Distribution and Institutional Absorption

Active Supply

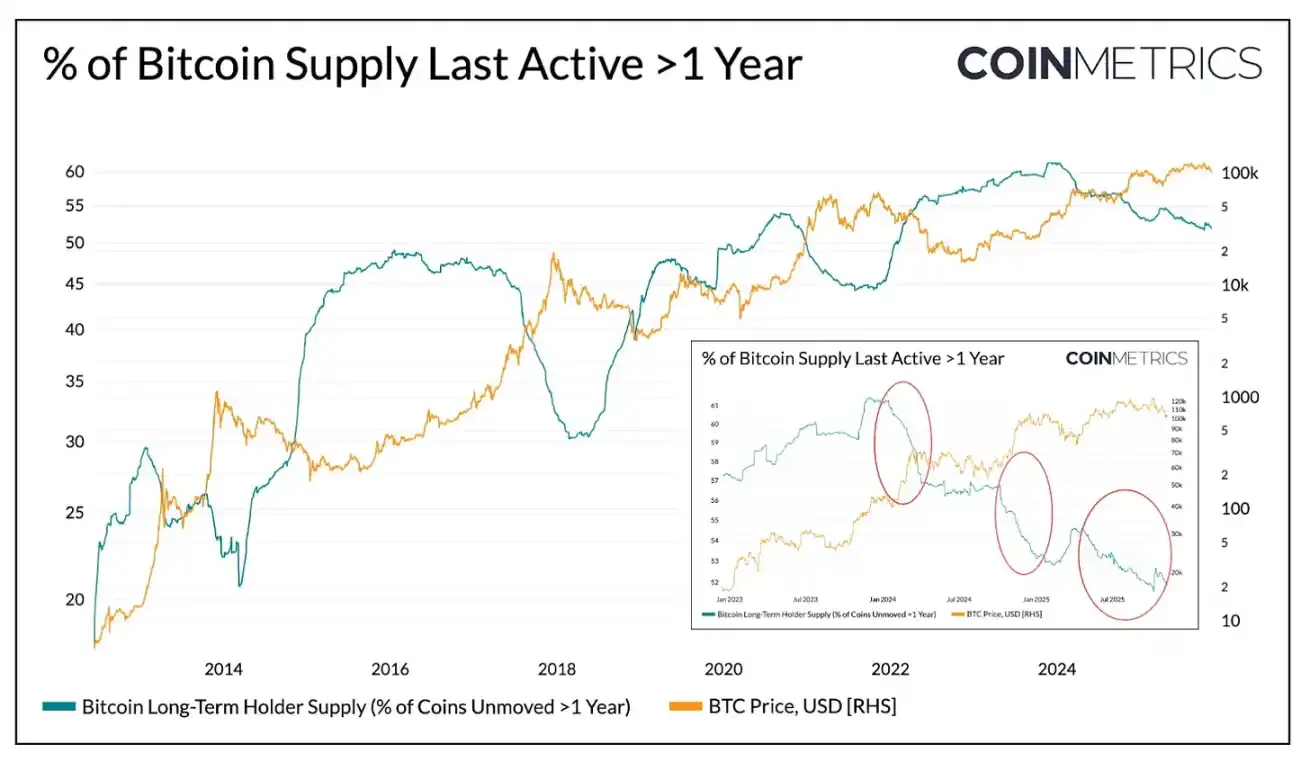

First, let's look at Bitcoin's active supply, which is categorized by "the duration since the last on-chain movement," reflecting the liquidity of tokens held for different lengths of time and clearly showing the distribution of supply between "dormant tokens" and "recently moved tokens."

The chart below specifically lists the proportion of Bitcoin supply that has not moved for over a year, which can serve as a proxy for the holdings of long-term holders (LTH). Historically, this ratio tends to rise during bear markets (tokens concentrate among long-term holders) and fall during bull markets (long-term holders begin to move tokens, take profits, and sell at highs).

Data Source: Coin Metrics Network Data Pro

As of now, among the 19.94 million circulating Bitcoins, approximately 52% of the tokens have not moved for over a year, down from 61% at the beginning of 2024. Both the increase during bear markets and the decrease during bull markets have clearly flattened. In the first quarter of 2024, the third quarter of 2024, and recently in 2025, there has been a trend of batch selling. This indicates that long-term holders are selling tokens in a more sustained manner, reflecting that the cycle of ownership transfer is extending.

ETF and DAT: Core Demand Drivers

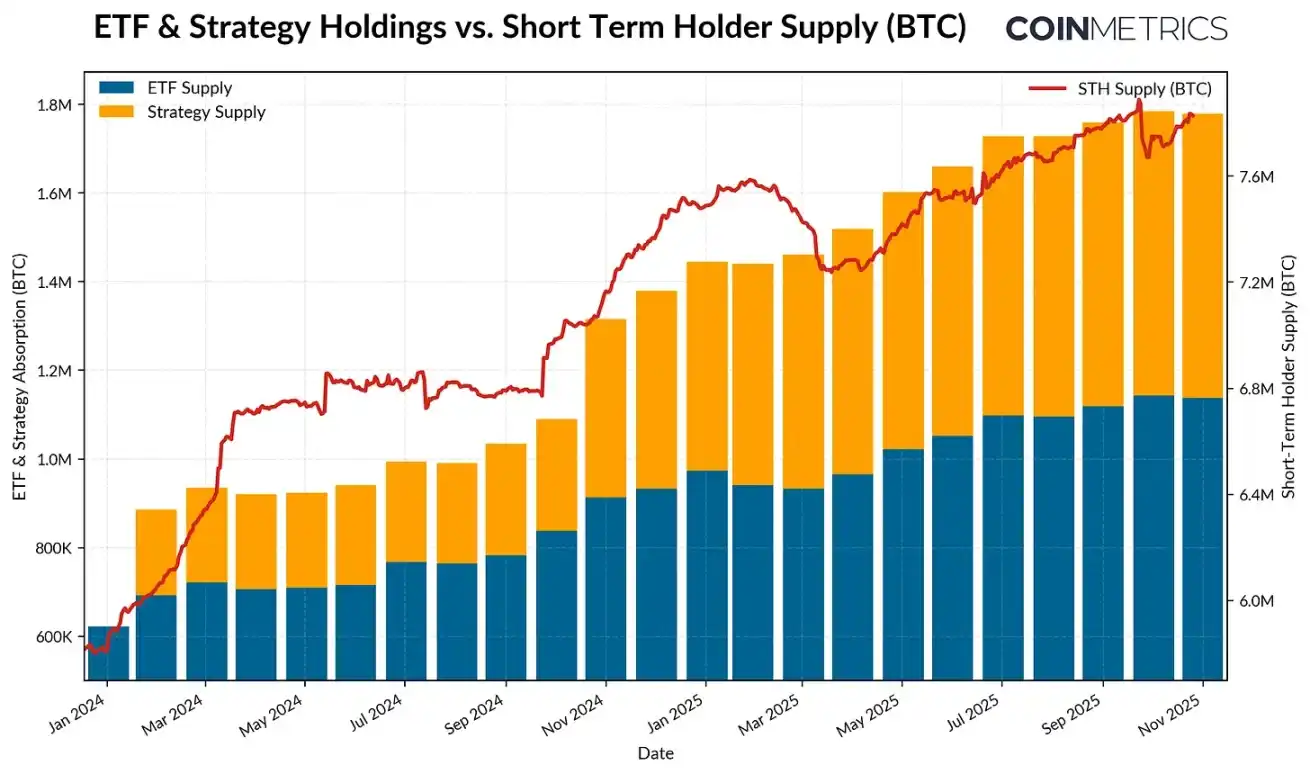

In contrast, since 2024, the supply from short-term holders (tokens active in the past year) has been steadily increasing due to previously dormant tokens re-entering circulation. At the same time, the launch of spot Bitcoin ETFs and the acceleration of crypto treasury (DAT) accumulation have brought new, sustained demand, absorbing the supply distributed by long-term holders.

As of November 2025, the number of active Bitcoins in the past year is 7.83 million, an increase of about 34% from 5.86 million at the beginning of 2024 (dormant tokens re-entering circulation). During the same period, the asset holdings of spot Bitcoin ETFs and Strategies increased from about 600,000 Bitcoins to 1.9 million, absorbing nearly 57% of the net increase in supply from short-term holders. Currently, these two channels account for about 23% of the supply from short-term holders.

Although capital inflows have slowed in recent weeks, the overall trend shows that supply is gradually shifting towards more stable, long-term holding channels, which is a unique characteristic of the market structure in this cycle.

Data Source: Coin Metrics Network Data Pro & Bitbo Treasuries; Note: ETF supply does not include Fidelity FBTC, DAT supply includes Strategy

Behavior of Short-term and Long-term Holders

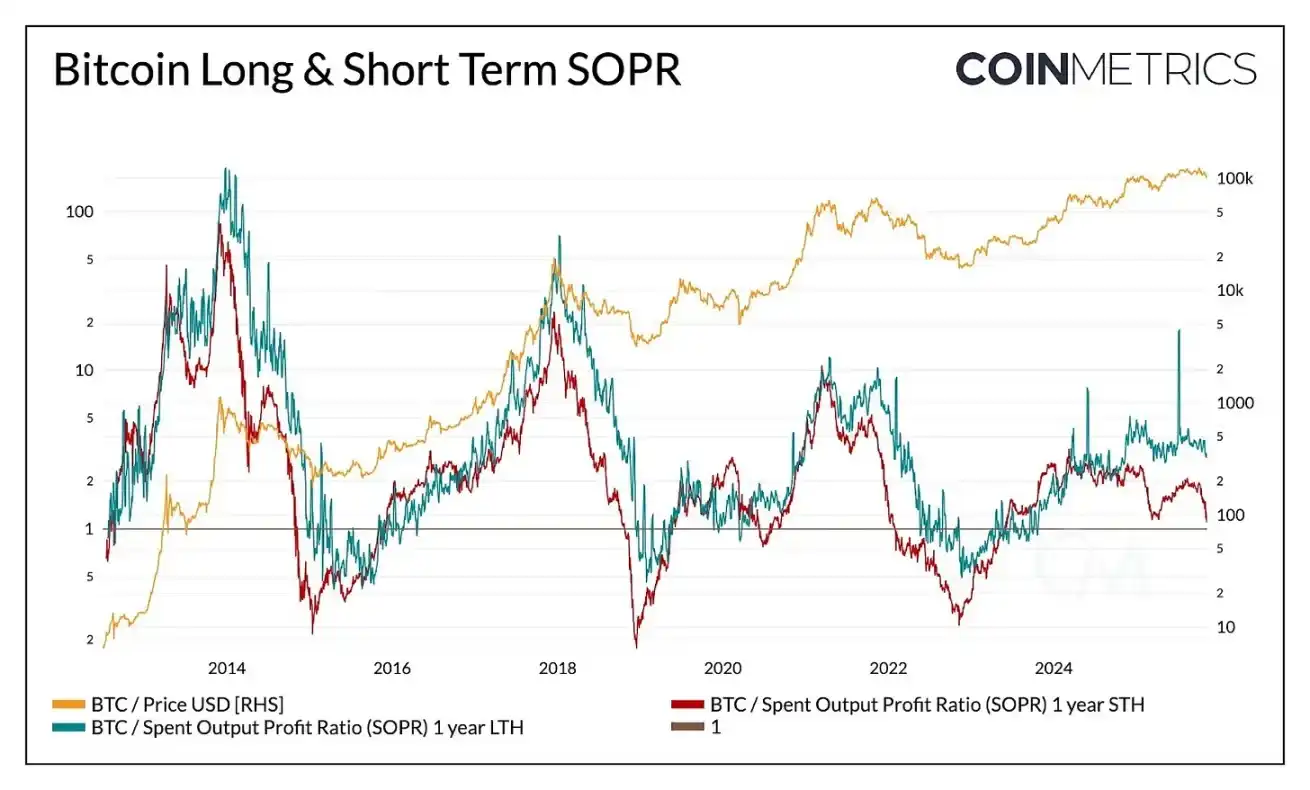

The actual profit trend further confirms the stable characteristics of Bitcoin's supply dynamics. The Spent Output Profit Ratio (SOPR) is used to measure whether holders are selling tokens at a profit or a loss, clearly reflecting the behavior patterns of different holder groups in the market cycle.

In past cycles, the profit and loss realizations of long-term and short-term holders often exhibited sharp, synchronous fluctuations. Recently, however, this relationship has diverged: the SOPR for long-term holders remains slightly above 1, indicating that they are steadily realizing profits and selling moderately at highs.

Data Source: Coin Metrics Network Data Pro

The SOPR for short-term holders hovers around the breakeven line, which also explains the recent cautious market sentiment, as many short-term holders' positions are close to their cost price. The divergence in behavior between the two types of holders reflects that the market is in a more stable phase: institutional demand is absorbing the supply distributed by long-term holders, rather than repeating the past's dramatic ups and downs. If the SOPR for short-term holders continues to break above 1, it may indicate that market momentum will strengthen.

Although a comprehensive correction will still compress the profitability of all holder groups, the overall pattern shows that the market structure is becoming more balanced: supply turnover and profit realization are gradually advancing, extending the cycle rhythm of Bitcoin.

Decline in Bitcoin Volatility

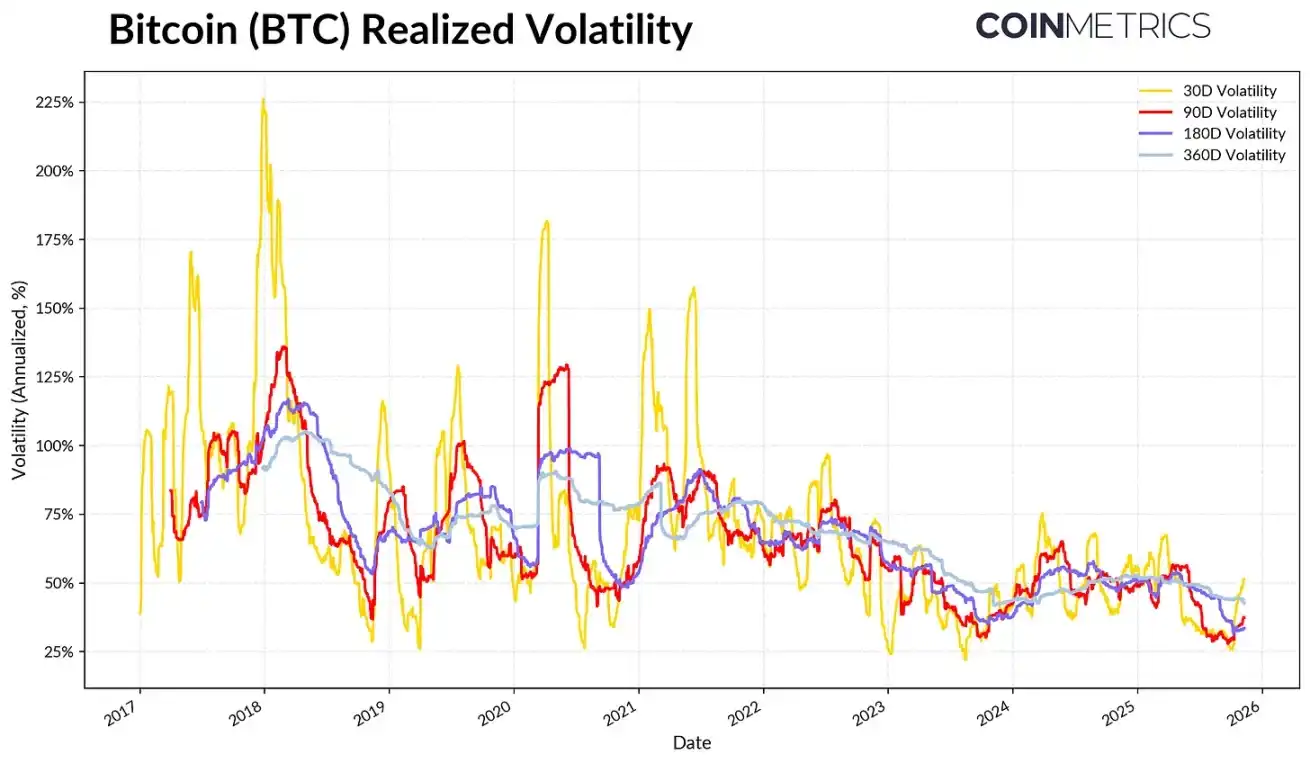

This structural stability is also reflected in Bitcoin's volatility, which has been on a long-term downward trend. Currently, Bitcoin's 30-day, 60-day, 180-day, and 360-day actual volatility stabilizes around 45%-50%, whereas in the past, its volatility was often explosive, leading to significant market fluctuations. Now, Bitcoin's volatility characteristics are increasingly resembling those of large tech stocks, indicating that it has matured as an asset. This reflects improved liquidity and a more institutionally dominated investor base.

For asset allocators, the decline in volatility may enhance Bitcoin's attractiveness in investment portfolios, especially as its correlation with macro assets like stocks and gold remains dynamically changing.

Data Source: Coin Metrics Market Data Pro

Conclusion

Bitcoin's on-chain trends indicate that this cycle is progressing at a more stable and longer phase, without the frenzied surges seen in previous bull markets. Long-term holders are selling off in batches, with most being absorbed by more sustainable demand channels (ETFs, DAT, and broader institutional holdings). This shift marks a maturation of market structure: declining volatility and turnover speed, and extended cycles.

Nevertheless, market momentum still depends on the sustainability of demand. The flattening of ETF capital inflows, pressure on some DATs, recent market-wide liquidation events, and the SOPR for short-term holders being near the breakeven line all highlight that the market is in a phase of readjustment. The continued rise in supply from long-term holders (tokens held for over a year without movement), SOPR breaking above 1, and renewed inflows into spot Bitcoin ETFs and stablecoins could all become key signals for the return of market momentum.

Looking ahead, alleviation of macro uncertainty, improved liquidity conditions, and regulatory progress related to market structure may accelerate capital inflows again, extending the bull market cycle. Although market sentiment has cooled, after recent deleveraging adjustments, supported by the expansion of institutional channels and the popularization of on-chain infrastructure, the market foundation is healthier.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。