Written by: Delphi Digital

Compiled by: AididiaoJP, Foresight News

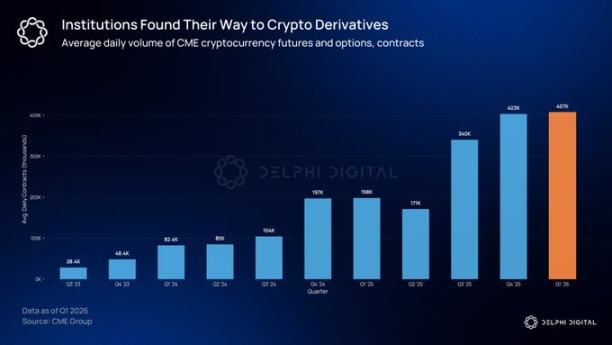

The scale of the cryptocurrency options market far exceeds most people's perceptions. The trading volume of cryptocurrency derivatives on the Chicago Mercantile Exchange (CME) is 46% higher than the historical record set last year. Institutional investors need clear risk management tools to hedge large positions, and options are the only cryptocurrency tool that can provide this functionality.

Restructuring the Landscape

By mid-2025, the total value of Bitcoin options open interest reached $65 billion, for the first time surpassing futures open interest. Futures are leveraged instruments, while options allow funds to set a loss limit for their $500 million Bitcoin position by paying a premium. This turning point indicates that tools with risk definition capabilities are gradually replacing purely leveraged instruments.

This growth is mainly concentrated on two platforms. Deribit has been the mainstream platform for cryptocurrency options trading for years, and after being acquired by Coinbase for $2.9 billion in 2025, it gained institutional-level endorsement. Meanwhile, IBIT options, launched at the end of 2024, have brought traditional financial capital into this field. The options market is rapidly expanding, but the vast majority of trades still need to be completed through intermediaries.

On-chain Options Are Still in Their Infancy

The market share of decentralized derivatives has risen from 2% to over 10% in two years. Hyperliquid has proven that decentralized exchanges (DEX) can match centralized exchanges in speed and transparency. However, on-chain options have yet to see similarly representative projects.

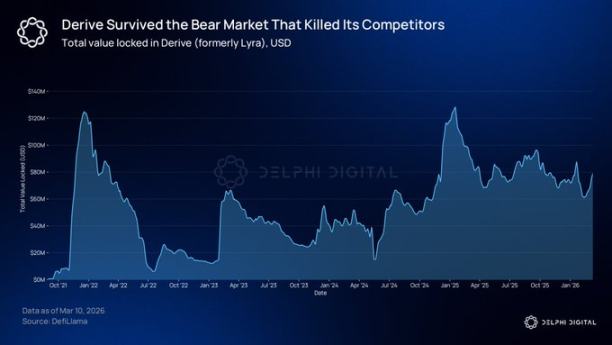

@DeriveXYZ is currently the leading on-chain options protocol, with nominal options trading exceeding $700 million in the past 30 days. Launched in August 2021 under the name Lyra as an options automated market maker (AMM), the protocol was completely reconstructed in 2023 after the bear market, and now features a gas-free central limit order book built on its proprietary OP Stack Layer 2.

This restructuring has fundamentally changed the pricing mechanism. Market makers quote directly on the order book, narrowing spreads, improving pricing accuracy, and supporting larger trades. Traders enjoy zero gas fees and sub-second execution speeds.

Its portfolio margining system has also attracted attention from institutions. The system assesses overall position risk through scenario analysis. For example, if a trader holds both long call and short put options on the same underlying asset simultaneously, the system does not require margin for each leg separately.

The margin required for hedged positions is less than the simple sum of each position, reflecting the universal logic of traditional financial derivative trading desks. Derive also offers perpetual contracts and lending services on the same Layer 2 and supports cross-product margining.

@KyanExchange is progressing in the same direction but in different ways. The platform combines an order book matching engine with on-chain portfolio margining, allowing multi-leg operations to be completed in a single atomic transaction. Traders can deploy iron condor strategies with just a few clicks.

The clearing mechanism adopted by Kyan is also different from most DeFi protocols. When the margin threshold is breached, the platform does not liquidate the entire account, but instead executes partial liquidations, closing only sufficient positions to restore the account to meet margin requirements. Kyan is currently in the Arbitrum testing phase, with mainnet launch imminent.

Who Needs Options?

Asset management companies building structured products urgently need the clearly defined risk-return structure that options provide. For instance, JPMorgan's stock premium income ETF is based on a covered call strategy, making it one of the largest actively managed funds in the world. The overall management scale of derivative-based income products has exceeded hundreds of billions of dollars. As more institutional funds enter on-chain, the corresponding hedging demand will also migrate.

Currently, an increasing number of institutional investors hold or plan to allocate digital assets in the short term. The open interest of IBIT options has surpassed that of the gold ETF GLD. In 2025, CME processed nominal trading worth $3 trillion in cryptocurrency derivatives.

The Timing is Maturing

Most early on-chain options protocols failed to survive primarily due to regulatory uncertainty. For example, Opyn faced penalties from the CFTC for operating a derivatives exchange without a license. At that time, the team could not predict whether the product would be deemed illegal in the next quarter during its development.

This situation is currently improving. In September 2025, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly issued a statement allowing regulated exchanges to conduct spot cryptocurrency trading. The CLARITY Act has passed in the House of Representatives, aiming to place the digital commodity spot market under CFTC regulation. The Senate version is still under negotiation and currently on hold. CME Group will launch around-the-clock cryptocurrency options trading on May 29. Although this does not guarantee that on-chain protocols will necessarily prevail, the overall environment has undergone substantial change.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。