Author: Baheet

Compiled by: Jiahua, ChainCatcher

The construction of institutional financial infrastructure often has a clear trajectory. You cannot start with the most expressive products and then work backwards.

You need to start from the clearing layer, prove that it can operate normally under pressure, and then unlock all the features that depend on it.

The New York Stock Exchange did not add derivatives before it had a well-functioning stock market. The Chicago Mercantile Exchange did not launch options before introducing futures.

This order is by no means arbitrary. The order at the grassroots level determines the possibilities at the top level.

Hyperliquid is well aware of this principle.

The public generally views Hyperliquid as a DEX that continuously delivers products. A perpetual contract exchange that adds spot, tokenized assets, and then prediction markets. A team that acts quickly.

This statement is not wrong, but it completely misses the point.

Hyperliquid did not build a DEX and then continuously add products. What they built is a clearing engine, which is unlocked layer by layer.

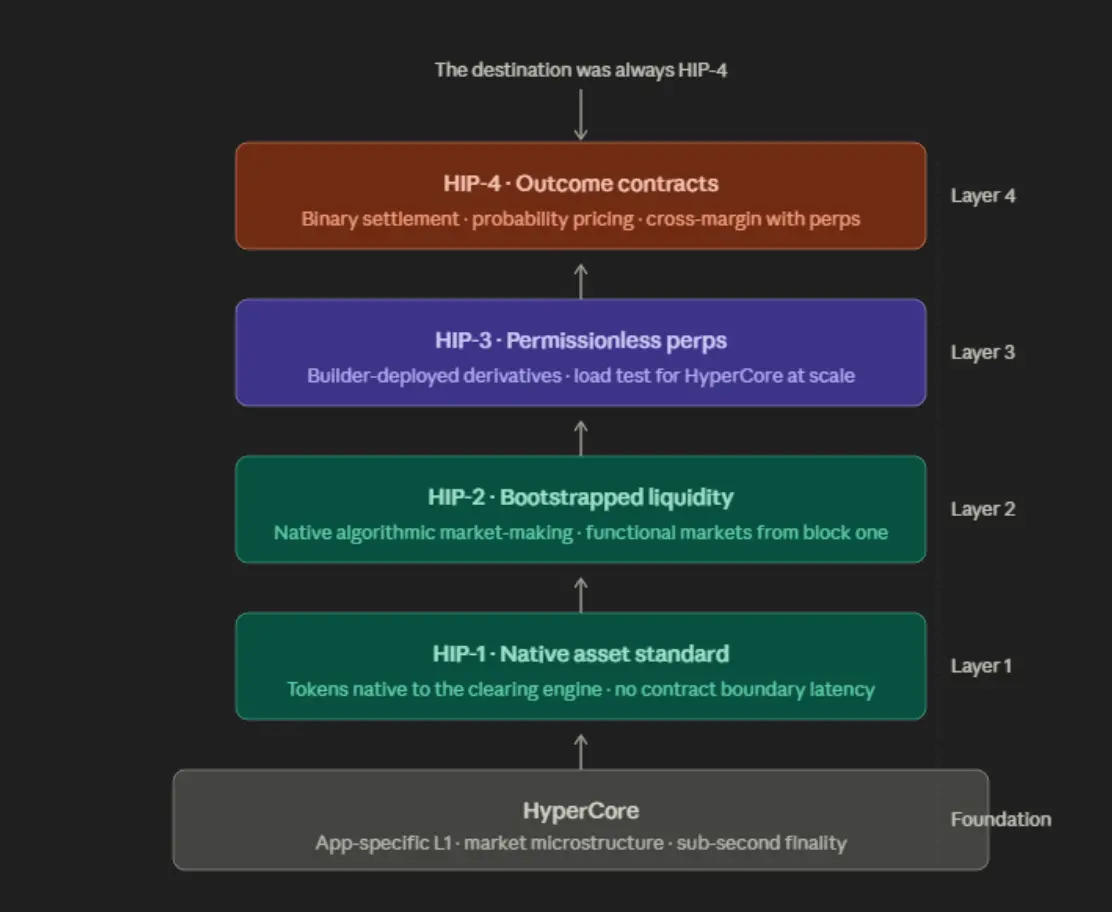

Each HIP is a prerequisite, not simply a feature.

And HIP-4, the proposal that everyone calls the Polymarket killer, is the ultimate proof of that clear goal from the very start.

Foundation

Before any HIP appears, a design decision determines everything that follows.

Hyperliquid built HyperCore as a specific application L1 entirely optimized around market micro-structure. It does not pursue general programmability. It does not pursue the execution of arbitrary smart contracts.

It focuses solely on market micro-structure. Sub-second confirmations, predictable execution, clear state management, and a matching engine capable of handling the throughput needs of professional derivatives trading.

This is a deliberately set constraint. By refusing to build a general chain, Hyperliquid relinquished the breadth of developers that Ethereum and Solana compete for.

In return, they obtained a clearing engine that could reliably support institutional-level markets from day one.

This performance guarantee is what AMM-based DEXs and general L1s have spent years trying to retrofit but have still not fully achieved.

Each subsequent HIP was made possible precisely because HyperCore was built this way first.

Constraints themselves are strategic.

HIP-1: Asset Standard

The first layer is the most fundamental, and also the least talked about.

HIP-1 introduced Hyperliquid's native token standard, which is the protocol's response to ERC-20, but with a key structural difference.

Tokens under HIP-1 do not exist as smart contract balances on a general virtual machine. They are the native units of the HyperCore engine itself, capable of being traded directly within high-performance matching infrastructure from the moment they exist.

This distinction is far more important than it sounds.

On Ethereum, assets and the exchanges trading those assets are independent systems that must communicate across contract boundaries.

On Hyperliquid, assets and exchanges are the same system. There are no bridges, no delays introduced by cross-contract calls, and none of the execution risk space that plagues DeFi protocols built on general chains.

HIP-1 resolved the asset availability issue.

But its deeper functionality is that it established HyperCore as a native home for financial primitives, not just an execution environment for arbitrary code.

Without this proof, everything that follows will be untrustworthy.

HIP-2: Guiding Liquidity

Assets without liquidity are meaningless. This is the cold start problem, which has killed far more promising protocols than any technical failure.

You need liquidity before traders appear, and you need traders before liquidity providers appear.

Most projects mitigate this contradiction through incentive programs, token release schedules, and market maker subsidies. These are not solutions. These are delays.

HIP-2 introduced Hyperliquidity, a native algorithmic market-making mechanism that is directly built into the protocol layer.

Unlike AMMs that passively wait for volume and force liquidity providers to face inevitable impermanent loss when the market settles, Hyperliquidity automates the provision of liquidity for spot assets in a way that gives sustainability to the economic model from the very first block.

Any asset launched on Hyperliquid can immediately have a functional market. Not "will eventually have." But immediately.

The significance of HIP-2 is not only in operational terms. It proves that HyperCore can natively solve the cold start problem without outsourcing liquidity guidance to external market makers or incentive programs.

This proof laid the foundation for future developments. Permissionless perpetual contracts would face the same cold start problem at a larger scale. HIP-2 indicates that the engine is entirely capable of managing it.

HIP-3: Stress Testing

It is from here that this argument becomes indisputable.

HIP-3 broke the monopoly on listing assets. Before this, every market on @HyperliquidX was deployed and managed by the core team, and this centralized model ensured quality but limited diversity.

HIP-3 introduced perpetual contracts deployed by builders, allowing external teams to deploy perpetual markets for any asset without permission.

Meme coins, indices, pre-trade tokens, niche trading pairs. Anyone who can stake one million HYPE can list a market and operate within HyperCore's infrastructure.

The results were immediate. The open interest grew from less than $200 million to over $1.26 billion. Daily trading volume reached $5.9 billion.

Early participants occupied up to 85% of the market share in their respective categories. By any standard, HIP-3 was an explosion.

But the most important thing HIP-3 did was not to create trading volume.

It proved that creating permissionless markets on HyperCore can operate at scale under real conditions and withstand real funding risks.

The matching engine held up. The state management held up. The fee mechanism held up.

HyperCore has now passed stress tests for permissionless derivatives trading across dozens of assets simultaneously.

HIP-3 is the exam. HIP-4 is the meaning of the exam.

HIP-4: Ultimate Goal

Outcome contracts appear to be predictive market products. In reality, they are the closed loop of the entire architecture.

HIP-4 introduced fully collateralized, binary settlement contracts, which trade between 0 and 1 and settle to one of those values based on verifiable event outcomes.

There is no clearing; entering establishes a fixed risk exposure, settled in USDH.

On the surface, this makes Hyperliquid a direct competitor to Polymarket and Kalshi. This framework is not wrong, but it underestimates the substantial changes that are occurring.

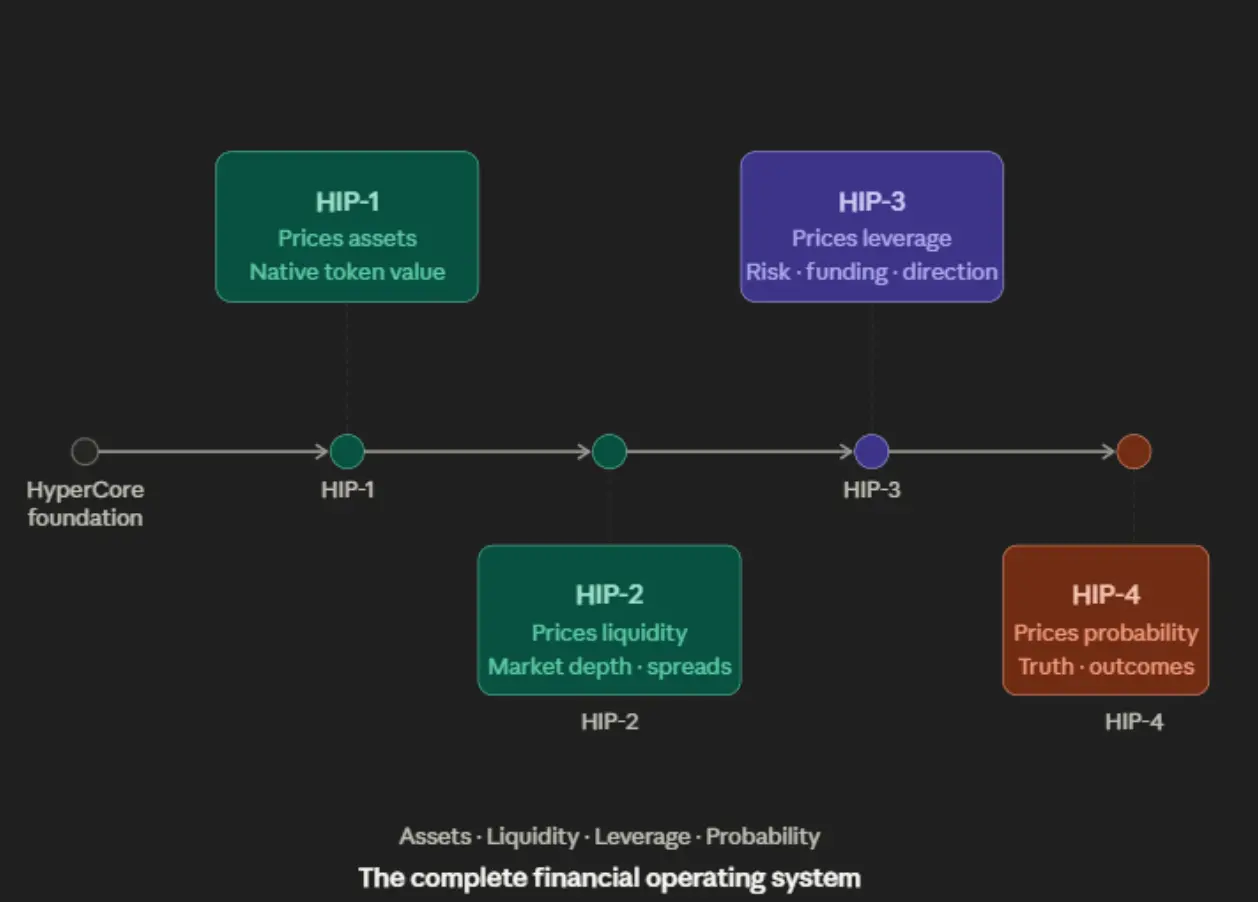

The deeper function of HIP-4 is to extend HyperCore's pricing capabilities from assets and leverage to probability itself.

Before HIP-4, HyperCore could price the value of an asset and how much leverage the market could support. After HIP-4, it can price whether something will happen.

This step completes the last link of the financial operating system.

Price direction, leverage, and probability are the three fundamental dimensions of financial risk. HyperCore can now natively express these three dimensions in a unified margin environment on the same clearing engine.

This is why full margin capability is the most important function of HIP-4, rather than merely a surface-level predictive market.

Traders can use the same collateral to hold both a leveraged perpetual contract position and purchase a result contract.

The idle capital at the prediction market level transforms into active capital at the perpetual contract level.

These two systems are not adjacent products sharing a balance sheet. They are the same system expressing different dimensions of risk against the same clearing infrastructure.

No existing predictive market can offer this, because no existing predictive market is built on a verified derivatives clearing engine.

Polymarket and Kalshi are settlement layers for binary bets. And HyperCore is a financial operating system that now conveniently supports binary betting as one of its many primitives.

Comparison

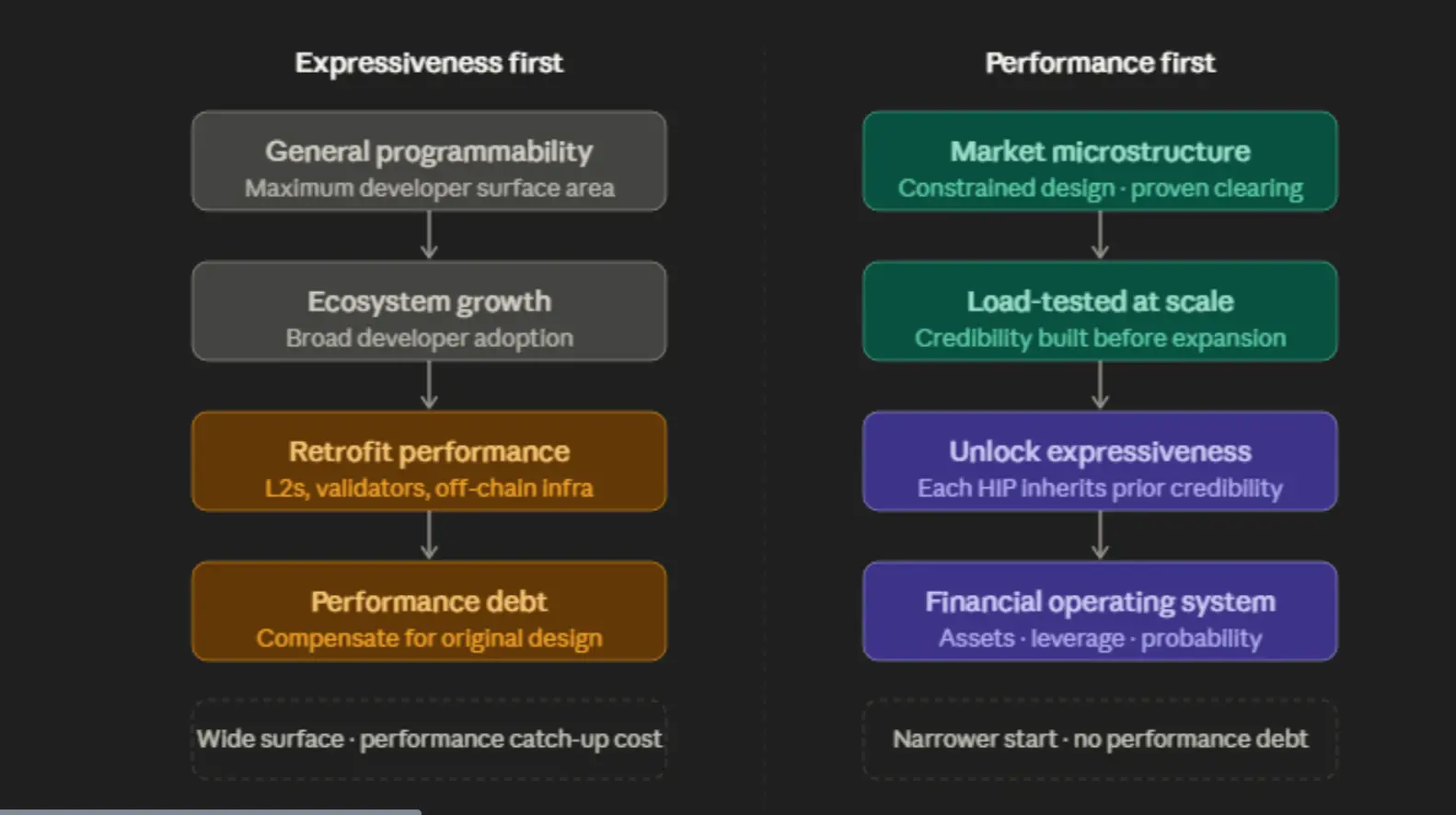

When you observe how the broader ecosystem handles the same problems, the sequential choices made by Hyperliquid become clearer.

Most blockchain infrastructures are designed around a core belief: granting developers the maximum programmable space first, and performance will follow.

This is not wrong. Given the demands of the early days of the industry, it was a rational bet.

Ethereum's programmability unlocked an entire class of financial experiments that would otherwise not be possible. Solana's throughput demonstrated that on-chain systems could meet the speed demands of real financial applications.

Both chains have achieved real breakthroughs and continue to host some of the most important applications in the crypto space.

However, prioritizing programmable space over performance creates a specific form of technical debt.

When applications built on general-purpose chains grow complex enough to require institutional-level execution, the chain must retrofit the performance guarantees that it did not prioritize when building its foundation.

This retrofitting is difficult, expensive, and can never be completely clean-cut.

Execution environments are not designed around market micro-structure, and no amount of Layer 2 scalability or validator optimizations can fully compensate for the initial design choices.

Hyperliquid made the opposite bet. It completely restricted the design space at the foundational layer to market micro-structure and then unlocked programmable space on top of a clearing engine that has already been validated under real conditions.

The cost is that early developers have a narrower touchpoint. The return is that every product built on HyperCore inherits the reliability of the underlying clearing layer.

This is not a criticism of general chains. It is an observation: when financial infrastructure is designed from first principles, centered around markets rather than programmability, what possibilities arise.

Two different starting points, two different endpoints.

Final Thoughts

The team is not trying to build a better Binance. That kind of landscape has always been too small.

Hyperliquid is actually building the minimum viable tech stack of a financial operating system, and it has been assembled in the only structurally sensible order.

Clearing first. Assets second. Liquidity third. Leverage fourth. Probability fifth.

Each layer is a proof of concept for the next layer. Each HIP is a prerequisite, not a function.

The evidence is in this order itself.

HIP-3 did not follow HIP-2 just because the team had a good idea for permissionless perpetual contracts. It followed closely because HIP-2 already proved that HyperCore can solve the cold start problem natively.

HIP-4 did not follow HIP-3 just because prediction markets are trendy. It followed closely because HIP-3 already tested the clearing engine at scale across dozens of assets under real funds.

This order itself is the best argument.

HyperCore can now price assets, maintain liquidity, express leverage, and settle probabilities.

This is not a list of functions cobbled together by a quick-moving team over time. This is an architecture with a clear goal.

The endpoint has always been HIP-4. It just took four prerequisites to get there.

That’s all!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。