Author: Hedy Bi, OKG Research

Returning to the "survival of the fittest" principle, the United States is set to fire the first shot in a trade war tomorrow morning (April 2, Eastern Time), making it clear that "America First" takes precedence over multilateralism. The global economy hangs by a thread, and the market has already partially priced this in, with gold rising 18% since the beginning of the year, reaching new highs. However, amidst the crisis, there are still opportunities. We seem to sense a glimmer of opportunity from the Trump family's latest foray into the crypto business, despite high mining costs and thin profit margins. From recent stablecoins to the entry of mining machines, the crypto industry appears to be accelerating both "Made in America" and "Trump-made." As Donald Trump Jr. puts it, "The future has no limits."

This article is the seventh piece in OKG Research's special project "Trump Economics 2025," exploring how to find vitality in crisis and analyzing the impact of tariffs on the entire crypto industry's supply chain.

Tariffs, historically known as "customs duties," are taxes levied on goods in transit to manage trade along the Silk Road. As a macroeconomic tool, tariffs directly affect the market prices and circulation efficiency of goods. For the crypto industry, this means not only paying attention to the prices of directly related goods and technologies along the supply chain but also understanding the more profound impacts on overall industry efficiency, supply chain liquidity, and market structure reshaping.

Tariffs Will Directly Increase Bitcoin Mining Costs by 17%

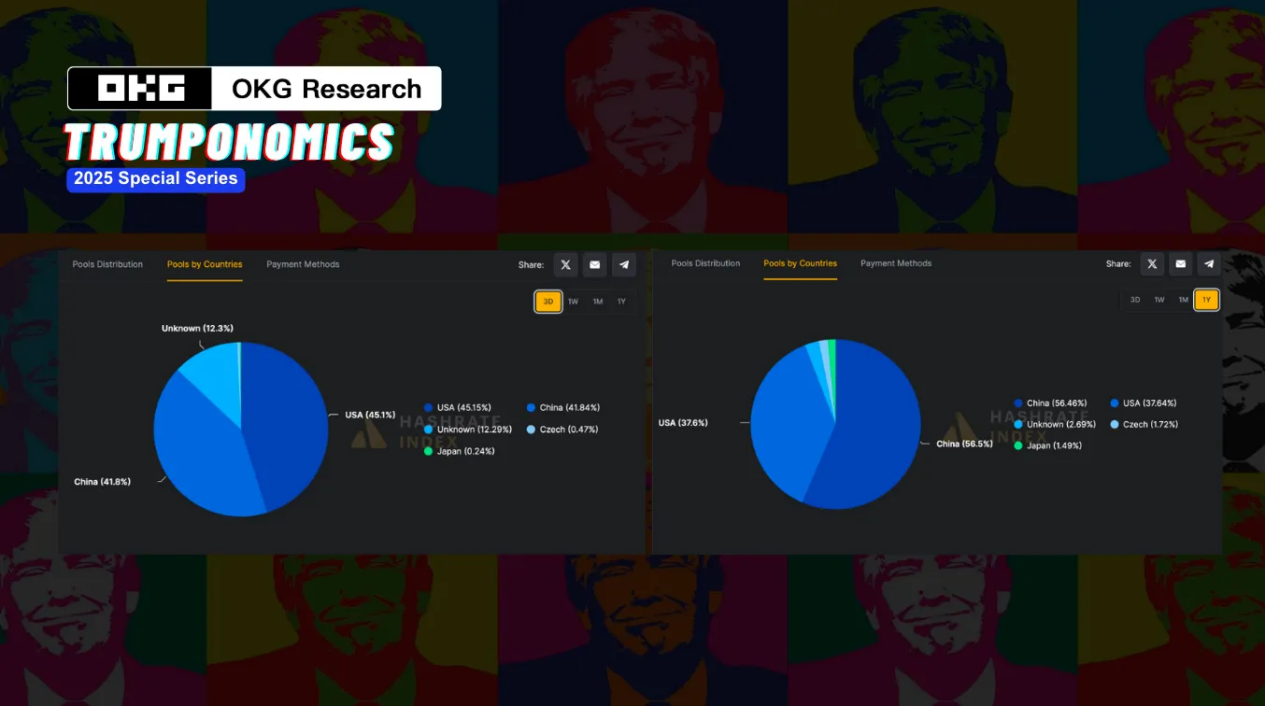

In the cryptocurrency industry, Bitcoin remains the most representative digital asset, dominating the market landscape. According to CoinMarketCap data (April 2, 2025), Bitcoin's market capitalization accounts for 59% of the entire crypto market, far exceeding other digital assets. Bitcoin relies on a proof-of-work (PoW) consensus mechanism, making the price of mining machines and the supply chain key factors in market direction. However, despite the increase in the share of mining power from U.S. pools from 37.64% to 45.15%, the mining machine supply chain is still dominated by Chinese manufacturers, particularly Bitmain, MicroBT, and Canaan Creative, which hold over 70% of the global mining machine market share. Therefore, the Trump administration's goal of "bringing Bitcoin mining back to the U.S." faces significant challenges.

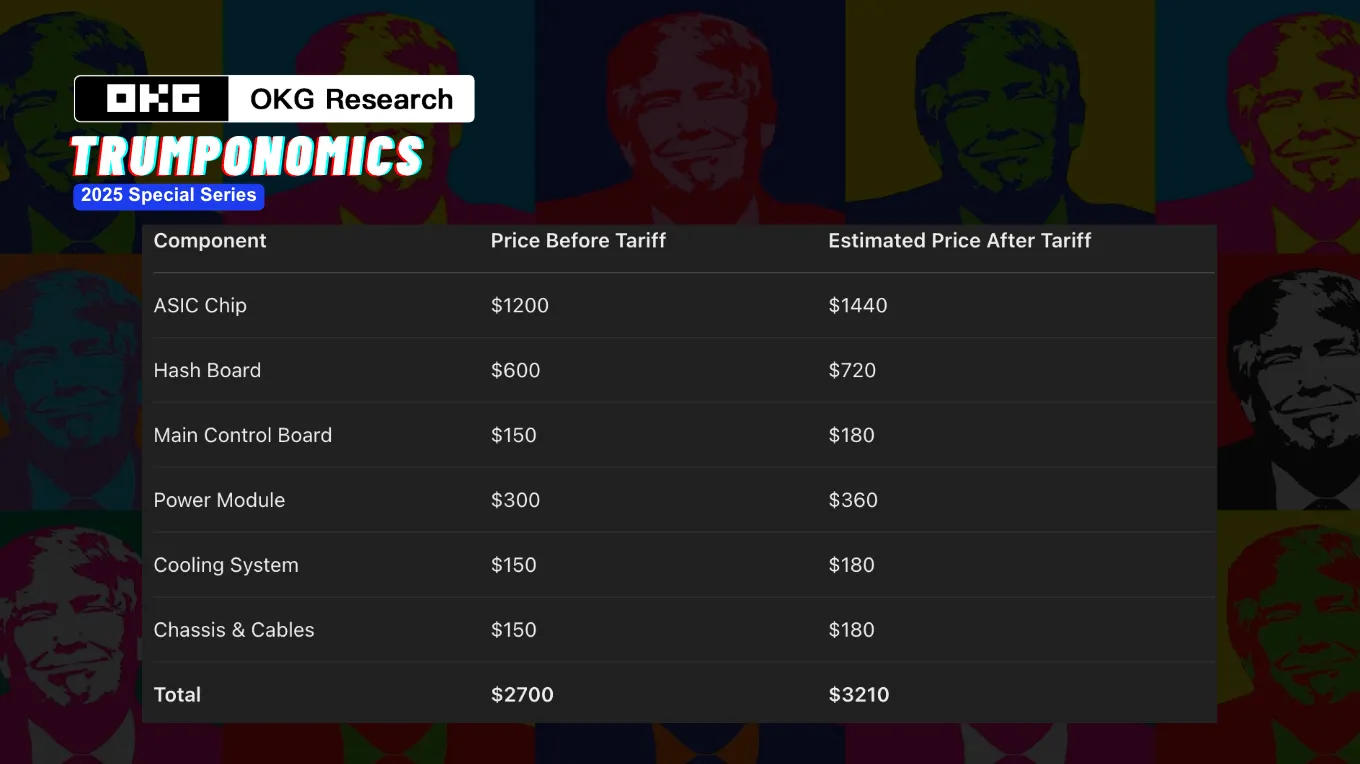

The tariffs imposed by the U.S. on Chinese electronics have exacerbated this supply-demand mismatch. It is estimated that if a 20% tariff is imposed on Chinese electronics, the cost of mining machines will rise by about 17%, directly affecting the return on investment (ROI) for mining operations. This change is particularly critical for new entrants in the mining field, who may need to reassess their profit models. Additionally, while MicroBT and Bitmain have announced the establishment of manufacturing centers in the U.S. and Malaysia to promote the de-China-ization of mining machine production, this transition has also led to delivery delays, with customers potentially waiting 1 to 3 months to receive their equipment, posing a significant challenge for mining operations that rely on timely delivery.

The global semiconductor shortage and U.S. technology export restrictions on China have forced mining machine manufacturers to establish production bases in multiple countries to mitigate risks. This change has led to instability in mining machine supply, with potential supply bottlenecks in the short term, further impacting the expansion and operational capacity of mining farms. As mining machine prices rise and delivery delays worsen, the mining industry may gradually trend towards centralization. Large mining companies, leveraging their financial advantages, will capture more market share, while smaller mining farms may face greater survival pressure, with extended investment return periods prompting them to exit the market.

Overall, tariff policies and supply chain fluctuations are profoundly impacting the Bitcoin mining industry. Rising costs, delivery delays, and supply chain instability are extending the investment return periods for mining farms while accelerating the industry's centralization process. Large mining companies may dominate the market, while smaller farms will face more severe survival challenges. Beyond Bitcoin, other blockchain projects relying on imported non-U.S. electronic hardware (such as AI) will also face similar cost pressures.

Off-chain Blockades and On-chain Openness

The U.S. tariff policy not only directly affects the cost of goods but also has a more profound impact on the reshaping of the global financial order. In recent years, the rapid rise of U.S. dollar stablecoins has become part of America's financial strategy—building barriers off-chain while accelerating openness on-chain.

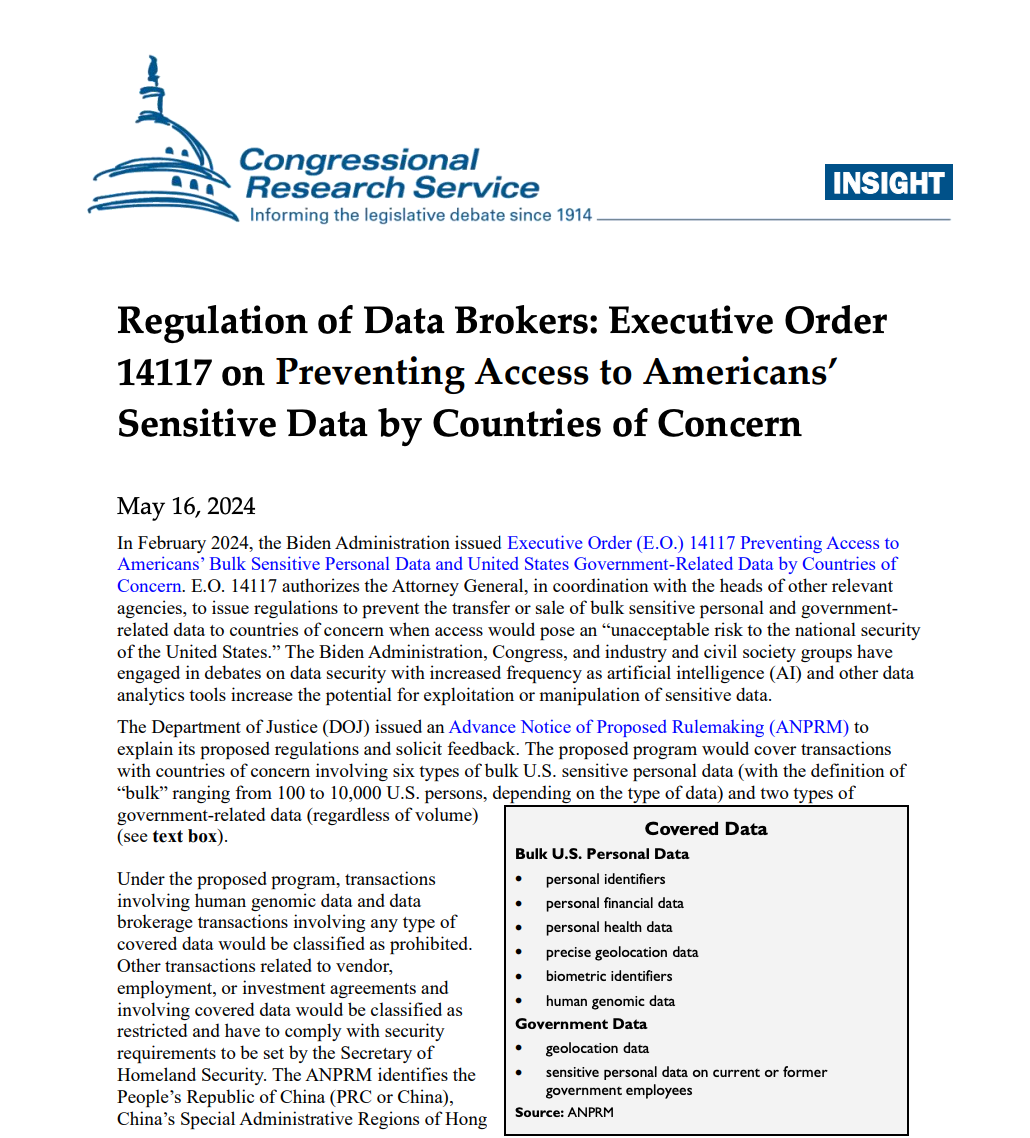

For a long time, the global trade settlement system has relied on banking networks, with systems like SWIFT and CHIPS dominating international capital flows. However, as geopolitical conflicts intensify, the U.S. has not only imposed tariffs but also restructured global trade through data decoupling and financial regulation. A typical example is the executive order 14117 signed by President Biden in 2024, aimed at restricting "concerned countries" from accessing U.S. data. The "14117 Executive Order" will officially take effect on April 8, requiring companies like PayPal to adjust their operations concerning mainland Chinese companies. This policy ostensibly targets the cloud computing and chip industries but effectively cuts off data sharing in multinational supply chains, triggering a chain reaction in trade financing and payment settlements.

In this context, U.S. dollar stablecoins have become a new channel for global capital flows. This means that when traditional banking networks are under regulatory constraints, stablecoin networks can still provide dollar liquidity to global markets. For instance, financial companies in Argentina, exporters in Southeast Asia, and even some Middle Eastern traders have begun to bypass the banking system, directly using USDC or USDT for supply chain payments. The low cost and instant settlement features of stablecoins make them ideal tools for cross-border trade. Traditional bank transfers may take 2-5 days and incur high fees (with SWIFT transfers averaging $20-40), while transferring via USDC typically costs less than one cent and can be completed in seconds.

More symbolically, in countries like Argentina and Nigeria, where strict capital controls are implemented, the demand for stablecoins is becoming increasingly urgent. In 2024, Argentinians had to pay a 30% premium to purchase stablecoins, while Nigerians faced a 22% premium. These premiums stem from the blockage of traditional financial channels and the depreciation of local currencies, making stablecoins a key tool for residents and businesses to bypass banking networks and protect their wealth.

Post-Tariff Landscape: Liquidity Expansion Beyond the Federal Reserve

After the tariffs, the market demand for U.S. dollar stablecoins will increase, more accurately reflecting the rapid expansion of a "shadow dollar market" that bypasses Federal Reserve regulation.

In addition to their "de-banking" circulation paths, the issuance of dollar stablecoins like USDT and USDC relies on U.S. Treasury bonds as collateral. This model is still indirectly influenced by Federal Reserve policy—after all, the yield on U.S. Treasuries determines the cost of stablecoin issuance. However, the liquidity creation mechanism of stablecoins is not directly controlled by the Federal Reserve. When demand for dollars surges, stablecoin issuers can quickly increase supply without needing Federal Reserve approval. This means that even if the Federal Reserve seeks to tighten liquidity through contractionary policies, the stablecoin market can still "indirectly ease" and continue to expand the supply of dollars globally.

In the past, the Federal Reserve could adjust the speed of dollar supply through the banking system, but now, these "on-chain dollars" have completely detached from the banking network, rendering the Federal Reserve's traditional control methods nearly ineffective in the stablecoin market.

The liquidity of stablecoins is primarily concentrated within the crypto market. DeFi platforms, centralized exchanges (CEX), and on-chain payment systems form an "internal cycle" for stablecoins. A significant amount of capital has not flowed back into the Federal Reserve-regulated financial system but remains trapped in this emerging on-chain dollar economy. Moreover, many DeFi platforms offer deposit rates for dollars that far exceed those of traditional banks, further weakening the Federal Reserve's interest rate transmission mechanism. Even if the Federal Reserve adjusts benchmark interest rates, the flow of funds in the stablecoin market continues to operate according to its own logic, becoming a relatively independent dollar financial system.

Demand from the stablecoin market has also driven up the market demand for U.S. Treasuries and lowered their yields. Notably, with the introduction of RWA (Real World Assets), the liquidity of stablecoins is beginning to enter a broader asset pool, further exacerbating this trend. This means that the interaction between the stablecoin market and the U.S. Treasury market will become more complex and may even influence the pricing logic of global capital markets in the future.

The day the tariffs were announced, dubbed "Liberation Day," will bring restrictions in terms of both cost and circulation, but the U.S. is quietly reshaping the global financial architecture by strengthening off-chain blockades and expanding on-chain dollar liquidity. From decoupling supply chain data to limiting bank settlements and the rapid rise of stablecoins, we seem to be witnessing a financial revolution.

Do you remember the original intention written in the Bitcoin white paper? A complete peer-to-peer electronic cash system should allow online payments to be sent directly from one party to another without going through a financial institution. Perhaps we are already standing on the threshold of this vision.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。