Original Title: "‘Crypto Retirement’ Becomes Reality! Trump Brings All Americans to the ‘Gambling Table’"

Original Source: BitpushNews

On August 7, 2025, a significant event quietly unfolded that is destined to leave a profound mark on American financial history.

Trump signed an executive order allowing U.S. retirement savings accounts 401(k) to officially invest in "alternative assets," including cryptocurrencies, private equity, and real estate. From this point on, an asset class that had long been marginalized by the mainstream financial system was officially incorporated into the nearly $9 trillion U.S. retirement plan.

This not only represents a critical shift in regulatory attitude but may also be a turning point for digital assets to achieve true mainstream acceptance.

From Marginal Asset to Mainstream Channel: The Leveraging Effect of an Executive Order

For a long time, the U.S. 401(k) plan—serving 90 million workers—primarily invested in traditional assets: stocks, bonds, and index funds, such as S&P 500 ETFs. Alternative assets, like cryptocurrencies, while increasingly active in the market, had long been excluded from the retirement system, with regulators maintaining a cautious, even hostile, stance.

However, in 2025, everything began to change. Washington released unprecedented goodwill towards digital assets, and the Trump administration actively promoted a wave of "de-regulation," with crypto assets becoming one of the most favored players in this movement.

Trump's new executive order requires the Department of Labor to reassess relevant provisions in the Employee Retirement Income Security Act (ERISA) to "provide a pathway" for the inclusion of digital assets and private investments in 401(k) plans, also leaving room for regulators to "tweak the rules."

According to the Financial Times, Trump's deep ties to the crypto industry played a role: "If it were only private equity, the order might not have advanced; it was cryptocurrency that ultimately led Trump to make the decision."

How Much Allocation? How Much Funding Will It Bring?

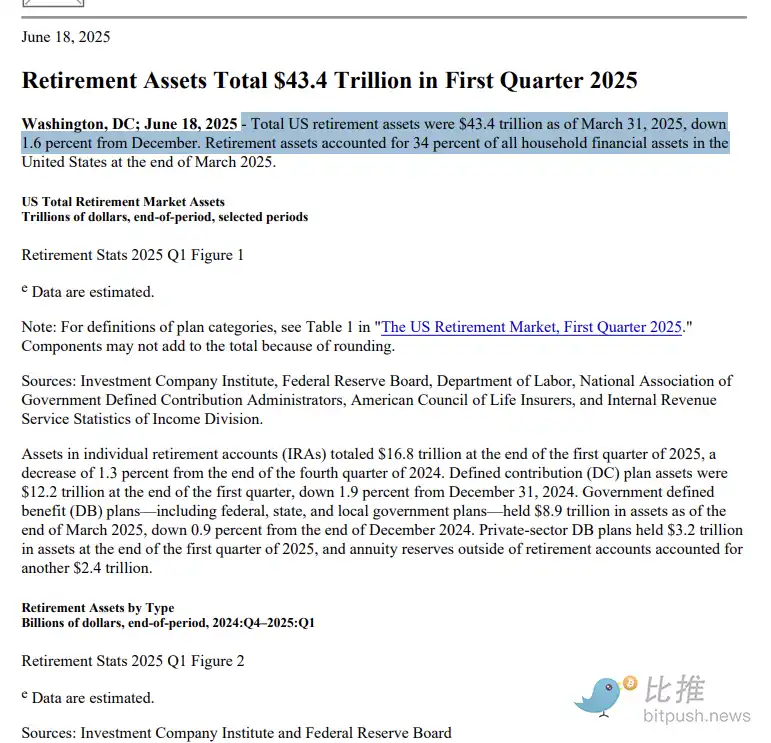

According to the latest data, the market size of U.S. 401(k) plans is enormous. As of the end of the first quarter of 2025, the total assets of 401(k) plans offered by U.S. employers amounted to approximately $8.7 trillion. The total assets of the entire U.S. retirement market (including 401(k), IRA, etc.) reached as high as $43.4 trillion.

So, how much funding could be allocated to cryptocurrencies? There is currently no exact figure.

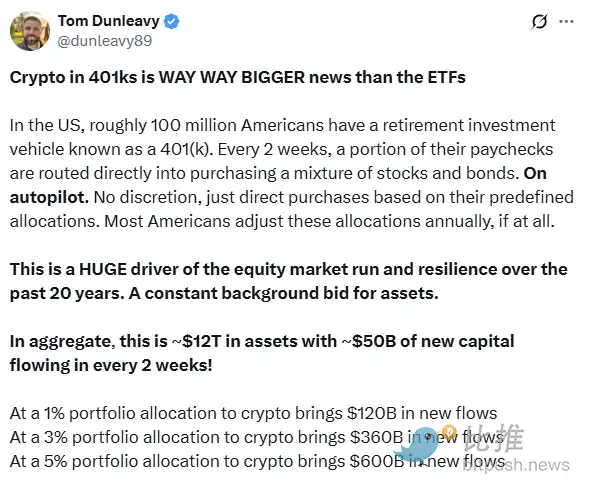

Tom Dunleavy, Director of Venture Capital at Varys Capital, provided a hypothesis:

"If every American's 401(k) account allocated 1% of existing assets to cryptocurrencies, $120 billion would flow into the crypto market. If it were 3%, that would be $360 billion; at 5%, it could reach $600 billion."

This represents a long-term and stable inflow of funds: most Americans automatically transfer a portion of their paycheck into their 401(k) every two weeks, and once digital assets are included in the asset pool, it means a continuous passive buying behavior.

For a market still known for its volatility, this is not just about funds; it is also about emotional support. "This will provide a more stable price support range for Bitcoin and Ethereum," Dunleavy stated.

Ryan Rasmussen, Head of Research at Bitwise, added:

"In the short term, this executive order sends a signal to the market: crypto assets have moved from the margins to institutional recognition."

ETF: The Best Bridging Method

In addition to directly incorporating digital assets into the 401(k) asset pool, crypto ETFs have become the most favored channel.

As of mid-2025, Bitcoin and Ethereum-related ETFs have attracted over $13 billion in net inflows. BlackRock's iShares Bitcoin Trust (IBIT) and VanEck's Ethereum ETF (ETHV) achieved year-to-date returns of 20% and 11%, respectively.

The benefits of ETFs are evident:

- No need to open a crypto wallet;

- No need to operate on decentralized exchanges;

- Issued by regulated fund companies;

- Can be included in portfolios alongside traditional assets.

Just as buying a GLD gold ETF is far more convenient than purchasing physical gold bars, ETFs have become the preferred tool for retirement investors to enter the crypto space.

How Far Is Actual Implementation?

Trump's executive order can signal direction, but there are multiple real-world barriers between "written on paper" and "appearing in accounts." The reform of incorporating crypto assets into 401(k) plans is caught in the gap between "policy intent" and "execution reality."

We can analyze the complexity of this implementation path from three dimensions:

Regulatory Barriers Have Not Been Completely Cleared

Although the president signed the executive order, the order itself does not have the immediate effect of changing regulations. Its role is to instruct the U.S. Department of Labor (DoL), the Securities and Exchange Commission (SEC), and other agencies to "reassess and amend" current regulatory rules.

According to CNBC, the current 401(k) plans are governed by the Employee Retirement Income Security Act (ERISA), which explicitly requires plan fiduciaries to adhere to the "prudent man rule" to maximize participant interests. However, the high volatility, poor liquidity, and opaque valuation of crypto assets make it difficult to pass prudence tests. In 2022, Fidelity launched a 401(k) Bitcoin allocation option, which was immediately publicly questioned by the Department of Labor and faced scrutiny. Although the policy direction changed in 2025, detailed rules have not yet been released, and fund providers that act rashly still face potential compliance litigation risks.

Real Concerns of Plan Providers: Not Wanting to Be the "Scapegoat"

401(k) plans are mostly operated in collaboration between employers and third-party service providers, involving large platforms like Vanguard, Fidelity, and Empower. However, many platforms currently hold a cautious wait-and-see attitude towards crypto options.

The main reasons include:

- High legal liability: If investors incur losses, fund managers and employers may be sued for "breach of fiduciary duty."

- Lack of investor education: Most 401(k) users lack understanding of crypto assets and may misjudge risks.

- High costs of technical integration: Introducing a new asset class requires reconfiguring risk control systems, reporting logic, and KYC processes, which is no small task.

Therefore, even if policies allow it in the short term, most crypto investments will still need to rely on "Self-Directed Brokerage Window" channels, which currently exist mainly in the 401(k) plans of some large companies. This method is typically used only by a few employees with in-depth investment knowledge. As a core investment option, the most likely vehicles will be spot Bitcoin and Ethereum ETFs, as these products are relatively mature and more highly regulated.

The Uncertainty of the Crypto Market Remains the Biggest Variable

Even if regulations are relaxed and there is a willingness to execute, whether the crypto market is truly ready to absorb long-term capital remains unknown.

- Bitcoin and Ethereum have rebounded significantly this year, but still experience over 30% daily volatility;

- Leveraged ETFs and on-chain contract products are emerging one after another, further amplifying retail risks;

- The shadows of platform collapses like FTX have not completely dissipated, and rebuilding investor trust is still ongoing;

- For many regulators, crypto assets still lack predictability and stable return logic.

In CNBC's "ETF Edge" program, Teucrium Trading President Sal Gilbertie pointed out: "Leveraged crypto ETFs are aggressive products and are not suitable for retirement portfolios—they are designed for day trading."

"From Margins to Core," It Took Sixteen Years

From the mining of the first Bitcoin by Satoshi Nakamoto in 2009 to its inclusion in the U.S. pension system in 2025, it took 16 years.

This transformation from "margins to core" is not accidental but the result of multiple forces—political motives, investment consensus, market logic, and technological advancements—intertwined.

One undeniable fact is that the Trump family and its core circle have close business ties with the cryptocurrency industry. Public data shows that their family assets include billions of dollars invested in cryptocurrencies and related enterprises. The process of cryptocurrencies moving from the margins to the mainstream reflects not only a shift in regulatory attitudes but also sparks discussions about the relationship between power and capital.

Now, with cryptocurrencies being incorporated into 401(k) pension plans, their role has fundamentally changed—not just a speculative asset but gradually becoming a component of the national financial system. However, this transformation has only just begun. Can cryptocurrencies truly become a reliable choice for pension investments? Currently, it still faces multiple tests regarding market volatility, regulatory frameworks, and long-term value. Ultimately, this experiment is not only about investment returns but may also reshape the future landscape of the financial system.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。