Author: Lin Wanwan EeeVee, Dongcha Beating

Editor: Jack, Dongcha Beating

Coinbase has adopted the Chinese 996 work culture.

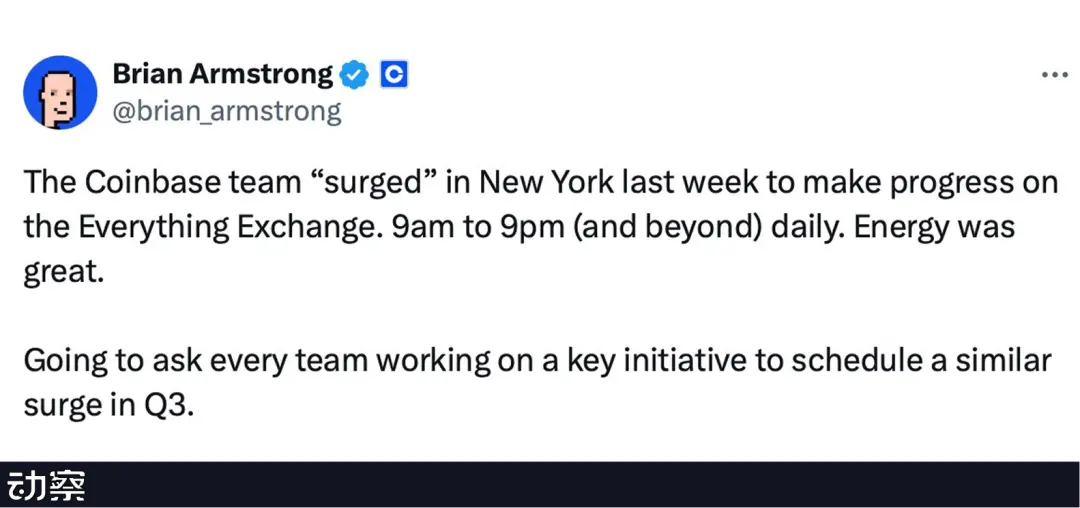

CEO Armstrong boasted on Twitter: The New York team has assembled, working overtime to develop the Everything Exchange, from 9 AM to 9 PM, and even later.

What started as a normal update sparked intense division in the comments. Western and European users criticized it as a pathological overwork culture, while Asian users downplayed it, saying, "It's normal in China, nothing to brag about."

However, the 996 culture is just the surface; behind it lies Coinbase's real anxiety.

In Q1 2025, Coinbase's net profit plummeted by 94% year-on-year, with trading revenue declining across the board; the Q2 financial report showed a net profit of $1.4 billion, which at first glance seems high, but this figure largely comes from paper gains from Circle's investments rather than from its own operations.

Thus, Coinbase's actual spot trading business is still shrinking, and the encirclement by ETFs, on-chain trading, and Robinhood makes this once "king of compliance" increasingly passive.

This is not a unique dilemma for Coinbase; exchanges are all seeking more intense 996 work culture and more profitable transformations.

Because the questions facing Coinbase are becoming sharper: How much longer can the golden age of crypto exchanges last?

From Washington to Wall Street

As early as five or six years ago, Coinbase understood that if it wanted to go further, it couldn't avoid the four words: legal compliance.

One afternoon in 2019, Brian Armstrong walked into Capitol Hill for the first time. He carried slides, ready to explain crypto to the lawmakers like an entrepreneur pitching to investors.

But the questions he faced left him both amused and bewildered, "Oh, so you are the CEO of Bitcoin?"

Some even asked, "Is this a video game?"

At that moment, he realized this was not a debate but a "cross-species communication."

In fact, this was not Armstrong's first encounter with "misunderstanding." Before Coinbase went public, he often recalled the lonely moments of being a founder: during those years when crypto was still in a gray area, almost no banks were willing to cooperate with Coinbase, making even basic payroll and corporate accounts a challenge.

He admitted that every negotiation back then felt like "begging" the traditional financial system for a lifeline.

In the early days of the startup, Armstrong naively thought that as long as he followed the law, he could focus solely on product development. But as Coinbase grew, he realized that the ambiguity of regulation itself was a weapon.

SEC Chairman Gensler used "lack of clarity" as an excuse to fire at the entire industry; Senator Elizabeth Warren even tried to portray crypto as "financial poison."

This experience made him realize the importance of "compliance" earlier and more deeply than outsiders might imagine. Unlike many peers in the industry chasing traffic, Coinbase chose a seemingly slower path from the beginning: actively applying for licenses, implementing KYC/AML, and repeatedly communicating with regulators.

Armstrong then understood that if he did not actively shape the rules, he could only wait for others to bury him.

So, he began to change his approach. In addition to continuing to fly to Washington as an "educator," he formed a policy team, funded the creation of StandWithCrypto.org, provided each lawmaker with a "pro-crypto index," and even invested in the super PAC Fairshake.

In 2024, the U.S. elections brought "crypto voters" to the forefront for the first time. Anti-crypto lawmakers were voted out, and pro-crypto newcomers were successfully elected. Washington finally realized: there are actually 50 million Americans who have used crypto wallets. It turned out this was not a marginal topic but a manipulable voting machine.

On Wall Street, Armstrong played another card: compliance.

On the eve of the 2021 IPO, Armstrong mentioned in a media interview that Coinbase was able to knock on Nasdaq's door not just because of its business achievements but also because it was ahead in compliance.

This was also the true meaning of the IPO in his eyes, not just a fundraising event but a "rebranding," a milestone that allowed the crypto industry to move from the margins to the mainstream.

In 2025, he pushed for the implementation of the "Genius Act," which requires stablecoins to be 100% backed by cash or U.S. Treasury reserves. This was not only a legislative victory but also Coinbase's "moat." As a shareholder of Circle, it shares in the interest income from USDC. In 2024, Circle's reserve interest income was approximately $1.68 billion, of which about $910 million was paid to Coinbase.

Stablecoins became a story that both Wall Street and Congress could agree on: for the government, it maintained the dollar's hegemony; for capital, it provided stable cash flow.

In this way, Coinbase completed an identity transformation. In Washington, it is a lobbying machine shaping rules; on Wall Street, it is a compliance gateway connecting capital.

Armstrong once said, "As long as you grow big, even if you don't care about the government, the government will care about you."

This statement serves as a footnote; Coinbase's new battlefield has long surpassed the exchange itself.

The "CEX Crisis" in Financial Reports

Being legal and compliant is far from enough for exchanges.

Despite still being one of the largest crypto trading platforms in the world, Coinbase's financial report for the first half of 2025 was filled with anxiety.

In Q1, total revenue reached $2 billion, a year-on-year increase of 24.2%, which sounds decent, but against the backdrop of a 94% year-on-year drop in net profit, this figure almost lost its meaning. The net profit of $66 million not only fell far below market expectations but also made investors truly feel for the first time: the old model of centralized exchanges is collapsing.

The decline in spot trading revenue is particularly noticeable.

Institutional trading fell by 30% year-on-year, and retail trading decreased by 19%. Behind this, there are certainly factors related to the cooling market. Since 2025, the volatility of Bitcoin and Ethereum has sharply decreased, and the market has shifted from a "roller coaster" to "flat ground," causing both institutions and retail investors to lose the impulse to frequently enter and exit.

But the deeper pressure comes from the restructuring of the market landscape.

The launch of ETFs directly rewrote the paths for investors. After Bitcoin, Ethereum, Solana, and XRP all applied for ETFs, which were originally Coinbase's core trading tokens.

Compared to the trading fees of 0.5% for CEX, the annual management fees of 0.1%–0.5% for ETFs seem much cheaper, naturally leading funds to flow toward Wall Street.

At the same time, the wealth creation effect on-chain has kept more users on-chain.

The craze for memes and DeFi has led native investors to form new habits: CEX is no longer a trading venue but merely a "cross-chain bridge for deposits and withdrawals" and a "temporary wallet for stablecoins." The rise of decentralized derivatives has further accelerated the outflow of funds.

New platforms like Hyperliquid, with flexible listing mechanisms, higher leverage, and more extreme experiences, have quickly attracted traders from regions with strict regulations like the U.S. In the eyes of these users, Coinbase's "rule-following" has become a constraint.

The most lethal competition comes from the heartland of traditional finance.

Robinhood announced a full-scale entry into crypto, opening the battlefield in Coinbase's most valuable young retail investor demographic. For them, Robinhood offers a more familiar interface, lower fees, and a more seamless one-stop experience for U.S. stocks and crypto. For large funds, the "brokerage halo" of Robinhood is even more attractive than Coinbase.

This multiple pressure was starkly magnified in Coinbase's Q2 2025 financial report. Coinbase disclosed that total revenue for the quarter was approximately $1.5 billion, a 26% decrease from the previous quarter; the GAAP net profit reached $1.4 billion, which looks impressive at first glance, but most of it came from Circle's investments and paper gains from crypto asset holdings.

Once these one-time factors are excluded, the adjusted net profit is only $33 million. More critically, the core spot trading revenue was only $764 million, a year-on-year decline of 39%.

The surface may seem lively, but the reality is bleak. Coinbase's profits no longer rely on trading but on stablecoin revenue sharing to sustain itself. This is a brutal report card, and it may also signal the end of a golden era.

When Trading Platforms No Longer Rely on Trading Business

In the face of adversity, Coinbase proposed a new vision.

In a recent interview, Coinbase CEO Brian Armstrong outlined a plan: all assets will eventually be on-chain, so they aim to create the Everything Exchange.

To him, crypto is not an isolated industry but a technology that can upgrade the entire financial system.

Armstrong specifically mentioned the current state of U.S. stocks: today, if an Argentine wants to open a U.S. brokerage account, they face a very high wealth threshold. For ordinary investors in most countries, U.S. securities are almost a "rich person's exclusive market."

But if stocks are tokenized and moved on-chain, it can break down these barriers, allowing anyone in the world to buy and sell U.S. assets at any time.

Being on-chain also means more possibilities: 24/7 trading, support for fractional shares, and even the design of new governance logic, such as "only shareholders who have held for over a year can vote," to encourage long-term investors.

In his vision, Coinbase is no longer just a platform for matching trades but a "universal exchange" that handles all assets on-chain, an open, inclusive, and always-operating financial operating system.

For this reason, Coinbase has begun to take a series of actions to align with Armstrong's vision: over the past six months, it has acquired Spindl, Iron Fish, Liquifi, and Deribit.

The first three serve the Base chain: Spindl provides an on-chain advertising stack, allowing developers to directly acquire users; Iron Fish brings a zero-knowledge proof team to build privacy modules on Base; Liquifi offers token management and compliance services and plans to integrate with Coinbase Prime to facilitate institutional and RWA projects.

Together, these three have lowered the barriers for developers on Base, creating a complete tool stack.

The most significant acquisition is Deribit. Futures trading is more stable and profitable than spot trading, but Coinbase has long been constrained by U.S. regulations and has been absent for a long time. Spending $2.9 billion to acquire Deribit allows it to gain a leading share in the options market and a large institutional client base.

Less than a month after the acquisition was completed, Coinbase launched perpetual contracts under CFTC regulation, effectively "seamlessly taking over" Deribit's capabilities.

If the acquisition is a violent breakthrough for Coinbase against the ceiling of trading revenue, then the ongoing business expansion is a deeper identity transformation.

It is focusing on "heavy lifting": stablecoins, wallets, public chains, and institutional services. These seemingly basic pieces are sketching out a new Coinbase: not just a trading platform, but a Web 3 version of Apple + Visa + AWS.

The first step is stablecoins. Coinbase does not directly issue USDC, but through profit-sharing with Circle, it takes a significant interest margin. A contradiction arises: Circle is dissatisfied with Coinbase's "high earnings and low contributions." Coinbase realizes it must integrate USDC into more scenarios.

Thus, it began subsidizing USDC deposits and partnered with Shopify to launch a payment API, embedding stablecoins into real-world cash registers and financial systems, allowing USDC to truly become a payment tool. Behind this is the push from a16z, which has always viewed stablecoins as the "TCP/IP of internet finance."

The second step is wallets. Coinbase Wallet has been upgraded to a smart wallet, eliminating the need for seed phrases, allowing one-click creation, and integrating NFT displays, on-chain identities, and social features. It even connects to Lens and Farcaster, turning the wallet into a "crypto social circle."

Once users' funds, identities, and social relationships are bound, the wallet becomes Coinbase's traffic entry point. Coupled with the Base chain, this system increasingly resembles iOS: Wallet is the App Store, Base is the operating system, and USDC is Apple Pay. Coinbase no longer relies on market volatility for profits but can extract "on-chain taxes" from the cycle of "identity + funds + social."

The third step is the institutional entry. Coinbase Prime already serves over 500 funds and asset management companies and is the main platform for USDC custody. In the future, if RWA, STO, and other assets are truly scaled onto the chain, Prime could completely evolve into the on-chain Goldman Sachs and BlackRock, becoming a stable source of income.

Unlike most platforms, Coinbase no longer relies on retail sentiment and trading heat to sustain itself. What it wants to control are the more fundamental elements: the funding entry (USDC), the account entry (Wallet), the trading entry (Base), and the institutional entry (Prime).

The future of Coinbase is not a noisy trading hall but a "universal exchange," a financial operating system capable of handling all assets and operating around the clock.

The role of the settlement layer gives it the opportunity to transcend short-term noise and volatility, making crypto the underlying layer, turning trading into a public service, and transforming users into network nodes. This may be the next Coinbase that Armstrong envisions.

"996" Sweeps the Exchanges

Exchanges have never lacked "intensity."

In the past, the competition was about who could list coins faster, who could offer bigger subsidies, and who had lower fees. That was a lively, surface-level competition: when traffic comes, profits follow.

Today's competition, however, is entirely different. ETFs have taken the incremental growth of major coins, on-chain DeFi and memes have kept native users on-chain, and brokerages like Robinhood have siphoned off the new generation of retail investors. With the market pie shrinking, relying solely on spot trading can no longer support the future of a platform.

Thus, the methods of competition have been forced to upgrade. OKX is intensifying its wallet to lock in users; Binance is enhancing its ecosystem, converting Alpha incentives into traffic returns; Coinbase is intensifying its infrastructure, using acquisitions, stablecoins, wallets, and institutional services to build a framework for a "universal exchange."

This is a heavier and more profound form of 996. It is not a short-term promotional battle but a long-term infrastructure overtime. They are no longer competing for immediate trading volume but for who can control the funding entry, identity entry, and clearing network in the next decade.

The past competition was about land grabbing and traffic stealing; now, the competition is about building strongholds and engaging in protracted battles.

Exchanges understand that the traffic feast has already ended. The winning hand for exchanges is no longer in the ups and downs of spot contracts but in who can sit in the advantageous position on the ecological chessboard.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。