From synthetic assets to CFD contracts and then to actual stock custody, how do compliance, liquidity, and user experience interact?

Imagine this: when you click "Buy" on the TESLA token in your Web3 wallet, an off-chain partner broker simultaneously places an order to buy the corresponding number of Tesla shares; and vice versa.

Does this count as bringing Wall Street's investment logic onto the blockchain?

Looking back at the development of tokenized US stocks, players have emerged one after another, with various models evolving: from the early Mirror and Synthetix entering through synthetic assets, to derivative trading of contracts for difference (CFD), and now platforms like Robinhood and MyStonks attempting actual stock custody, tokenized US stocks have always been exploring different paths.

The latest radical exploration comes from Ondo Finance, which adopts a more direct model of "on-chain instructions, off-chain actual stock synchronous trading"—the buy and sell transactions completed on-chain by investors will be executed in real-time off-chain by partner brokers. This means that tokenized stocks do not need to rely on additional on-chain liquidity pools, naturally possessing the potential for large-scale expansion.

As of the time of writing, Bitget and Bitget Wallet have taken the lead in integrating with Ondo, allowing users to directly trade hundreds of tokenized US stocks and ETFs through the on-chain entry of Bitget Wallet, further lowering investment accessibility and presenting themselves as disruptors.

Synthetic assets, CFD contracts, actual stock custody, and real-time on-chain and off-chain interaction have brought the tokenized US stock sector to a new watershed.

### I. Wall Street on the Blockchain: The 21st Century "American Dream"

In the 19th century, the American Dream was the California Gold Rush, the freedom of the New World.

In the 20th century, the American Dream was transoceanic immigration, the belief that "all men are created equal," and the struggle for a happy life.

In a sense, tokenized US stocks represent the "American Dream" of the 21st century. It is not only a vision of wealth freedom for global investors but also an extension of the influence of the US capital markets—bringing the pulse of Nasdaq to every connected corner of the Earth, strengthening the dollar's settlement position, expanding the radius of capital attraction, and allowing Wall Street to continue to hold the rules in a borderless digital world.

Looking back, from MakerDAO and Centrifuge pioneering the RWA concept and practice, to Polymath and others attempting to bring Wall Street rules onto the blockchain for the first time, tokenized US stocks have always been seen as the RWA form closest to public investment habits and the easiest to implement. However, limited by regulatory uncertainty, insufficient liquidity, and weak technology, the STO boom quickly receded.

The turning point occurred in 2020, when DeFi Summer proved the feasibility of on-chain liquidity, and the popularity of stablecoins provided a solid anchor for cross-border settlement and asset pricing.

Mirror Protocol and Synthetix launched on-chain synthetic assets for US stocks.

FTX and Binance partnered with licensed brokers to launch tokenized US stock trading anchored to real US stock prices.

However, with the collapse of FTX and the tightening of global regulations, on-chain liquidity gradually dried up, forcing most tokenized stock businesses on CEX and DeFi to go offline.

In 2023, the Federal Reserve began the most aggressive interest rate hike cycle in 40 years, US Treasury yields soared, and funds returned to favor high-yield, low-risk assets. MakerDAO shifted to an RWA model based on US Treasury bonds, regulatory frameworks were established in places like Hong Kong, and traditional financial institutions began to test compliant tokenized securities.

Today, RWA has made breakthroughs in regulation, technology, and product levels, and tokenized US stocks are re-entering a growth curve. According to data from RWA.xyz, as of August 13, the total value of tokenized stocks is approximately $362 million, with 167 asset categories and a monthly trading volume of about $290 million, with over 60,000 holders.

This number may not seem large, but it marks a trend—the liquidity edge of US stocks is quietly being rewritten by the on-chain world.

### II. Who is Tokenizing US Stocks?

After several years of trial and sedimentation, the participants in the tokenized US stock sector are gradually taking shape, forming differentiated patterns in compliance paths, technical architecture, and liquidity strategies. Currently, there are four major representative platforms in the market:

Bybit TradFi

Currently, Bybit's MT5 Gold & FX platform has launched the CFD function for US stocks, initially supporting 78 US-listed company targets, offering up to 5x leverage. CFDs are derivative contracts that allow investors to trade and profit from price differences without actually holding the underlying asset, which is relatively high-risk and volatile.

For crypto users, registering on Bybit and completing KYC Level 2 certification is sufficient. However, Bybit MT5 only holds a license issued by the Mauritius Financial Services Commission and currently cannot cover major markets such as the EU, UK, and US.

https://www.bybit.com/future-activity/en/mt5

MyStonks

MyStonks is a decentralized RWA trading platform that officially launched an on-chain US stock token market supported 100% by Fidelity on May 10. After users deposit USDT/USDC into MyStonks, the platform will convert it into USD and purchase the corresponding stocks, then mint ERC-20 tokens on Base at a 1:1 ratio. MyStonks supports direct login with Web3 wallets. Recently, MyStonks completed compliance filing for US STO and can issue compliant security tokens.

Backed Finance (Swiss Compliance License + DeFi Access)

Backed Finance is a tokenized asset issuer headquartered in Zurich, Switzerland, holding a Swiss compliance license. Its issued tokens correspond 1:1 with real assets and are custodied by a Swiss bank. Currently, Backed has launched the tokenized stock product xStocks, which users can trade on CEXs like Bitget and Kraken, as well as on Solana DeFi. xStocks tokens support cross-chain use and can be utilized on ETH, Base, Gnosis, Arbitrum, Avalanche, Optimism, BSC, Sonic, and Polygon. Backed does not require user KYC and currently requires whitelist access.

Helix

Helix is a DEX within the Injective ecosystem that has launched iAssets synthetic assets and recently opened trading markets for 13 synthetic US stocks. iAssets are essentially on-chain derivatives that do not require physical stock support, achieving price tracking with US stock assets through smart contracts and oracle pricing. Users need to use USDT stablecoins as collateral, providing up to 25x leverage.

Unlike the above platforms, Bitget Wallet is the first Web3 wallet to enter the tokenized US stock space. It combines trading entry and asset management functions, simplifying the onboarding process for Web2 users while aggregating multi-chain DeFi, allowing users to trade US stock tokens directly with on-chain identities without complex KYC.

More importantly, Bitget Wallet collaborates directly with Ondo to introduce a real asset custody path and partners with professional market makers to provide liquidity depth close to traditional brokers.

### III. The Diverging Paths of Tokenized US Stocks

From an overall perspective, the current competition among tokenized US stock platforms mainly presents differentiation in three dimensions: asset support and compliance, liquidity, and user accessibility.

1. Real Assets and Compliant Custody

First, there is the synthetic asset model that started with Synthetix and Mirror. This solution offers high flexibility, but there is no real asset backing it, and users must bear counterparty risk themselves. Ultimately, price anchoring does not equal asset ownership; the US stocks minted and traded under the synthetic asset model do not represent actual ownership of those stocks in reality.

If the oracle fails or the collateral assets collapse (as Mirror did during the UST crash), the entire system faces risks of liquidation imbalance, price decoupling, and loss of user confidence.

On the other hand, the CFD model like Bybit leans towards high leverage and derivative trading, resembling traditional forex trading, with limited license coverage and existing gray areas.

The Bitget Wallet model has a distinct advantage—by collaborating with Ondo and US-registered brokers, it links tokens to real US stocks at a 1:1 ratio, with daily audits, avoiding the "paper token" risks present in some platforms, making it more resilient under regulatory trends.

2. Liquidity Optimization Capability

Liquidity directly determines user experience. Platforms like Backed and MyStonks rely more on on-chain DEX spot pools, which can be limited by the volume of single trading pairs and slippage, leading to insufficient trading stability.

Helix's iAssets lean more towards a leveraged derivatives market, which can indeed attract a certain level of trading activity in the short term, but this high volatility and high leverage model still raises questions about long-term stability.

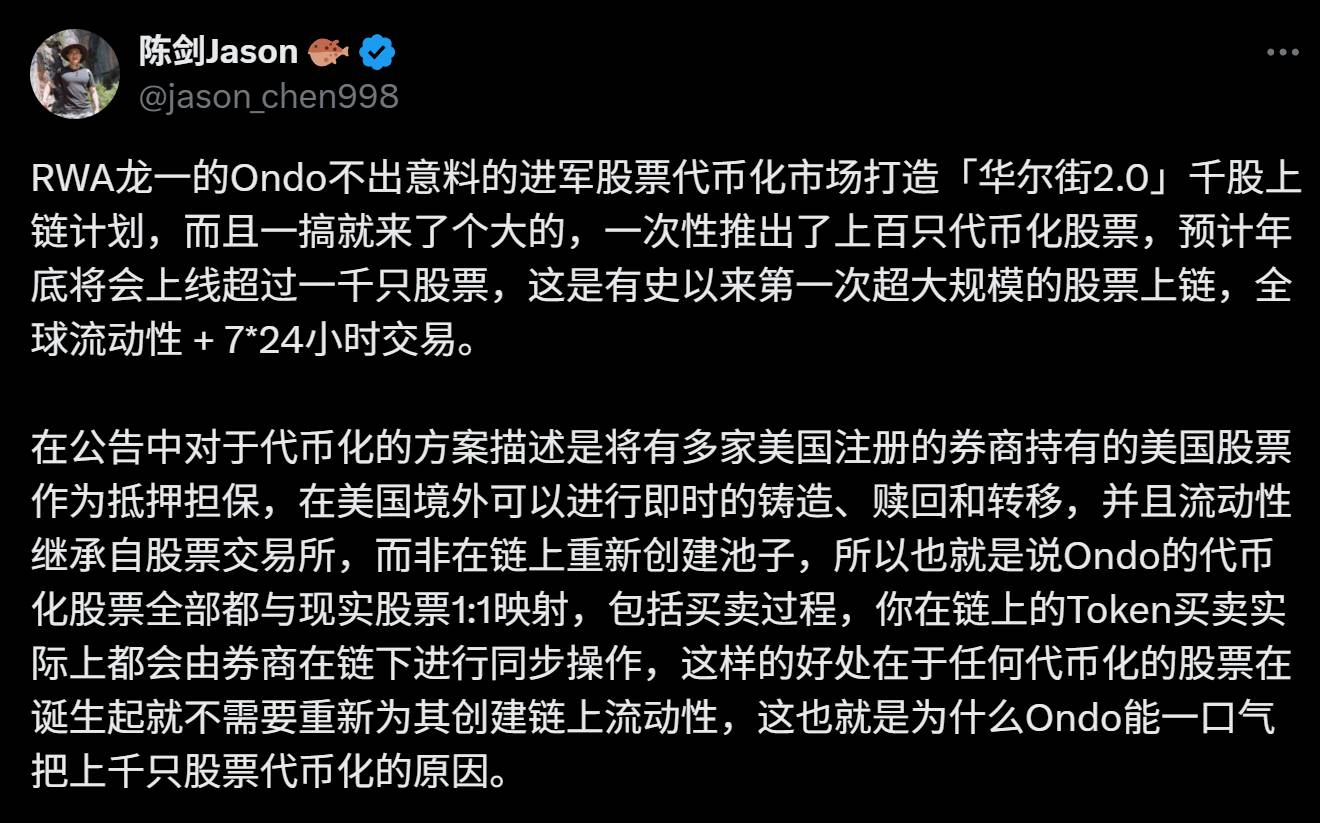

Interestingly, Bitget Wallet's integration of TradFi allows for immediate minting, redemption, and transfer based on the previously mentioned Ondo "on-chain instructions, off-chain actual stock synchronous trading" model, enabling transactions outside the US. As researcher Chen Jian stated: "The benefit here is that any tokenized stock does not need to create on-chain liquidity anew from the moment it is born, which is why Ondo can tokenize thousands of stocks at once."

At the same time, it leverages market makers like Jump Crypto to provide on-chain depth and spreads (0.3%) close to traditional brokers. This dual mechanism of "off-chain actual stock synchronization + on-chain institutional liquidity" allows users to enjoy lower trading friction while avoiding common liquidity shortages and slippage issues found in DeFi models.

3. User Threshold and Global Accessibility

For emerging market investors, the user threshold and global accessibility of the synthetic asset model are naturally the lowest: trading requires only an on-chain wallet, with no identity verification needed. However, the price of this convenience is the lack of real asset backing, with risks fully borne by the user.

The Bitget Wallet model follows closely behind. It offers an entry point of "no KYC + trading with USDT + investment starting from $1," significantly lowering the entry barrier while ensuring asset security through Ondo's actual stock custody.

In contrast, while Bybit has certain advantages in liquidity, its CFD nature and mandatory KYC limit user coverage; Backed supports multi-chain cross-chain but still requires whitelist applications, resulting in limited openness.

It can be said that at this stage, Bitget Wallet, with its combination of "real asset custody + higher liquidity + low threshold," has carved out a path distinctly different from synthetic asset DEXs, CFD platforms, and traditional RWA protocols. This model not only responds to regulatory compliance trends regarding asset security but also considers the convenience of participation for global users to a certain extent.

However, Ondo's advanced actual stock custody model combined with Bitget Wallet's traffic entry, while achieving a good balance between asset security, liquidity, and accessibility, and forming certain differentiated advantages, still faces three major challenges:

Uncertainty of Cross-Border Regulation: Even with US broker custody, cross-border sales of tokenized securities may still trigger compliance requirements from different jurisdictions.

Market Education and Liquidity Guidance: How to get more traditional investors to accept on-chain US stock products and maintain stable liquidity depth is a long-term operational challenge.

Gray Areas of Tax Rules: Taxation is an invisible but important variable. The recognition of capital gains and dividend taxes for on-chain US stocks varies by country. There is still uncertainty regarding whether and how the IRS will track on-chain transactions. This means that platforms not only need to provide compliant trading services but also offer clear tax guidance to users to truly lower the participation threshold.

Overall, the tokenized US stock sector is transitioning from the "experimental stage" to "model differentiation." Those who can simultaneously address the three major issues of compliance, liquidity, and accessibility are more likely to break through.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。