Written by: @0xfishylosopher

Compiled by: Blockchain Knight

In 2026, artificial intelligence agents will begin to become economic entities.

They will call SaaS APIs, execute transactions, purchase cloud computing resources, and link workflows together, all autonomously.

Just as humans need credit cards as a "banking channel" to transact in the real world, AI agents will also need a bank, which I believe will exist in the form of stablecoins.

This paper is divided into two parts. The first part is "why," why cryptocurrency (rather than credit cards) is particularly suitable to become the banking layer for agents? The second part is "how," assuming we accept cryptocurrency as the banking layer for agents, what exactly do we need to build to achieve this?

Why should agents use cryptocurrency instead of bank cards?

Cryptocurrency Twitter users often ridicule credit cards, with some believing they simply won't work for agents. This viewpoint is overly simplistic and may not be true. Visa and other companies have already made significant progress in the agent business sector.

For example, Visa Smart Commerce creates a payment gateway for agents similar to Apple Pay:

Like Apple Pay, these "agent cards" initially presume that you personally own a credit card.

Visa will then issue a "tokenized credential" with limits, authorization, and validity conditions. Like Apple Pay, these credentials also have a unique virtual card number that you can securely provide to your agent.

When your agent (e.g., OpenClaw) uses the tokenized credential to conduct a transaction, the credential is decrypted on Visa's servers and linked to your actual bank card, after which Visa processes the payment. No cryptocurrency is involved in the entire process.

Some products effectively demonstrate this process in practice. In short, agent cards work well and sometimes even outperform cryptocurrency in terms of security.

So, why opt for cryptocurrency? There are three reasons:

(1) An expanded trust structure;

(2) An internet-native currency for a global audience;

(3) New payment primitives.

1 - Expanded Trust Structure

Credit cards, along with the agent virtual cards derived from them, adopt a rigid and fixed "trust structure."

This structure assumes that, in order to make a payment, users must always have a KYC-verified bank account as a trust guarantee.

Then, users delegate trust and authorization to agents, much like parents opening a supplementary card for their children.

On the other hand, cryptocurrency and stablecoin payments are not bound by such trust assumptions. While you can (and in many cases should) link a stablecoin wallet to a KYC-verified bank account (e.g., at a centralized exchange), you can pay without doing so.

You can link a stablecoin wallet to almost anything, be it a government-issued ID, a social media account (e.g., Google, TikTok, Instagram OAuth), a domain name server, or a headless smart contract.

Many agents may choose a trust structure tied to fiat currency, but there will also emerge from other corners of the internet outside of fiat currency trust structures, as stablecoins are essentially the best (and arguably the only) way to facilitate high-volume transactional funding.

There is an old saying: "On the internet, nobody knows you're a dog." Similarly, in the world of cryptocurrency, nobody knows you're a robot.

2 - An Internet-Native Currency for a Global Audience

Stablecoins are an internet-native currency aimed at global users. The integration of Alipay with Qwen providing pearl milk tea vouchers showcases the future development direction of agent-based commerce.

If you have lived in or visited China in the last decade, you must have experienced the convenience brought by "internet-native currency," which permeates a range of everyday applications (food delivery, ridesharing, salary payments).

However, this system is geographically confined, operating within a closed technological ecosystem maintained by fiat currency authorities.

On the other hand, stablecoins have global reach from the start, able to provide this internet-native currency experience to other regions of the world.

This is crucial for agents, as their initial automated workflows will involve chained SaaS and API calls spanning multiple jurisdictions and service providers.

If an agent needs to coordinate a workflow that accesses an LLM endpoint in the USA, a data provider in Europe, and computing clusters in Southeast Asia, they don't need three different payment channels. One is enough.

3 - New Payment Primitives

In the world of stablecoin payments, everything can become a payment endpoint. The actual situation is paradoxical: for the internet economy, you are increasing the number of users who can transact (by giving anyone, anything a wallet), while also increasing the transaction volume for each new user (because you can purchase more goods).

Since you can have (1) an expanded trust structure for payment methods, and (2) an internet-native currency that runs through SaaS workflows and global supplier chains, you may see new payment methods emerging in succession. For example, anyone creating a Dune dashboard can use stablecoins to charge for request views.

For instance, a few weeks ago, I wrote code for Tokker at the Mistral hackathon, where we demonstrated a brand management AI agent aimed at TikTok creators.

We equipped it with a stablecoin wallet (via the Privy platform) to collect payments from the brands it contacted, thus avoiding payment issues associated with the banking methods used by TikTok creators.

A simple extension is to use the same stablecoin wallet to pay for various computing services, online advertising fees, etc., creating a virtuous cycle of economic output: increasing bank account usage while boosting user spending on the internet.

How to Build an AI Banking Tech Stack?

Now that we have a basic understanding of the "meaning" of cryptocurrency, we next need to figure out how to build this AI banking system based on cryptocurrency.

In the human world, banks play multiple roles. We store, spend, appreciate, and borrow funds here. At the same time, banks also serve as our identity registration, neutral dispute resolution institutions, and a safety barrier against malicious activities through anti-money laundering (AML).

To build a banking system for AI agents, we need more than just a wallet; we require a complete set of security mechanisms to regulate how they transact with funds.

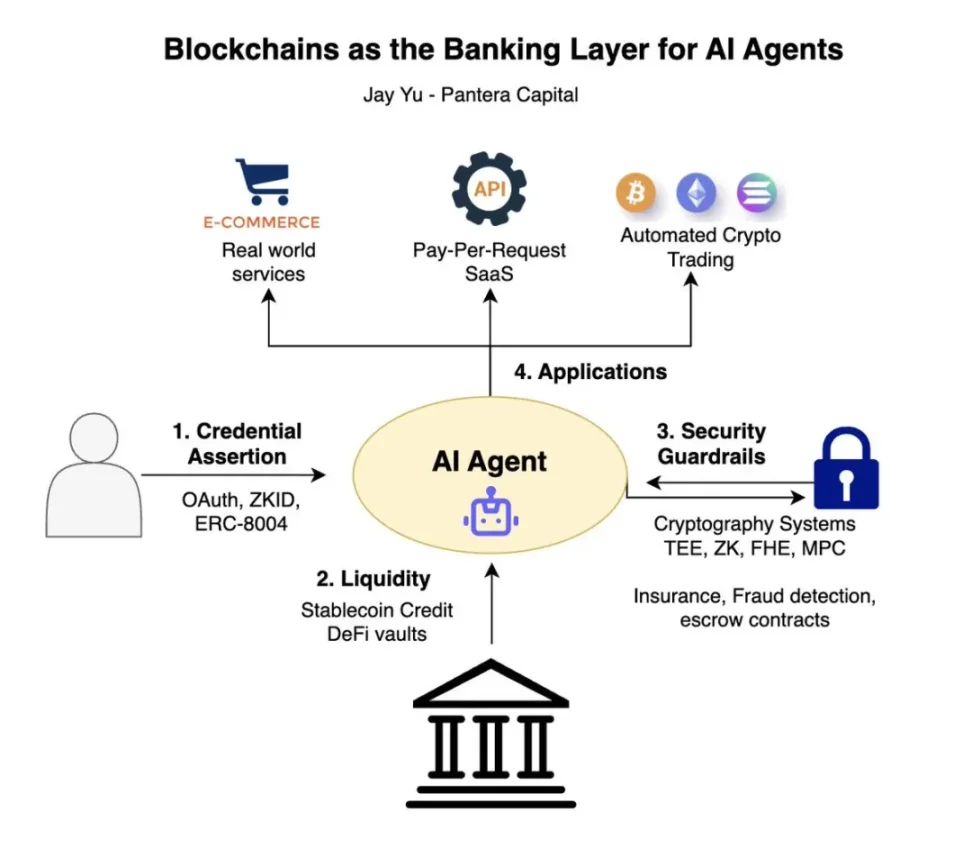

I believe it will consist of several interconnected components: (1) identity and authorization, (2) purchasing liquidity, (3) security measures, and (4) an application "store" for AI agents to purchase from. Blockchain excels in all four areas compared to traditional payment methods.

1 - Identity and Authorization

The first aspect is identity and authorization, who the transaction agent is representing. There are various design options for this layer.

You can take inspiration from Visa's approach and create an ID linked to your fiat card. You can also associate a wallet with an email or social media. For example, I created a hackathon prototype on how to create a ZKID for agent payments using an email domain.

You can also directly inscribe agent identity information onto a public blockchain like Ethereum. Standards like ERC 8004 achieve this by creating an "agent registry."

2 - Procure Liquidity

The second aspect is ensuring agents can genuinely pay for the required costs. Funds do not appear out of thin air just because you created a stablecoin wallet.

Most agent platforms currently provide "sponsored" points, but this is not sustainable at scale. The entry point for fiat to cryptocurrency, prepayments, buy now pay later (BNPL), and other authorization mechanisms will become critically important components of the agent economy.

In addition, we need to ensure that blockchain infrastructure operates correctly. Currently, agents primarily engage in cent-scaled microtransactions on the chain (with an average size of $0.09, as scale and transaction volume increase, we will need design measures like batch processing, payment channels, and pre-authorization to ensure these small payments do not clog public blockchains.

3 - Security Barriers

Just as banks need to guard against malicious actors' money laundering activities, agent banks also need to guard against malicious activities such as rapid injections, API fee spikes, and credential leaks.

Coincidentally, the blockchain space has been dealing with private key theft for years and has developed a robust cryptographic immune system, with technologies including trusted execution environments, multi-party computation, multi-signature formation, zero-knowledge proofs, and other security measures.

We should directly set these protection measures around agent payment systems and credential storage—in many aspects, the wallet private key is just a more sensitive API key; therefore, a complete "private key" protection mechanism should be applied to agent skills and API credentials to ensure AI agents can securely interact with the online economy.

4 - Application Store

Finally, at the application level, we arrive at the "Application Store Wars, where smart trading has entered the "agent business" era.

From Merit Systems to ATXP, to Sponge and Sapiom, many service providers have developed skills management mechanisms similar to "application stores," allowing agents to perform a variety of tasks from scraping LinkedIn information to sending emails to trading on Hyperliquid.

Whether it's through e-commerce payments for real-world service fees, accessing pay-per-use SaaS services, or automatically trading cryptocurrency tokens, agents need a "discovery tool" to determine which services to call, which wallets to use, and how much to pay for each service.

Underlying protocols like Coinbase's x402 provide agents with a universal, permissionless way to access real-world services, ultimately enabling agents to actively participate as independent financial actors in economic activities.

Conclusion

The agent era of the internet economy has only just begun; Claude Code and OpenClaw's rise to prominence has yet to reach six months.

In the past decade, the blockchain infrastructure has proven its capability to support a multi-billion dollar on-chain economy. I believe these two factors will quickly converge, and blockchain and stablecoins will become the banking foundation for the agent economy.

The banks for AI agents look nothing like banks, but rather resemble blockchains.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。