Written by: Grandpa Zuo

In July 2020, the king of DeFi, AC (Andre Cronje), personally launched a fair launch model with "no pre-mining and pre-sale, without team and VC shares," which became a well-known story.

By 2026, internal conflicts within the Aave open team and DAO continued, and Across even proposed to "rewind" back to a corporate system, with tokens to be strategically abandoned and converted into common stock.

If we broaden our perspective, compared to the struggles of DeFi projects, the exchanges that are most profitable are experiencing a wave of high-priced sales.

Coinbase is valued at $10 billion for Bybit's 80 million users, Nasdaq's parent company values OKX's 120 million users at $25 billion, and Forbes prices Binance's 300 million users at $100 billion.

All of this tells us that the crypto market has reached a turning point, the moment for phased selling has arrived, the old generation of entrepreneurs is opting for cashing out, but there is no conclusion on how to move forward.

We must acknowledge the fact that most crypto projects cannot equate network effects directly with user numbers and trading volumes like exchanges; they still need to handle token pricing and governance with caution and choose the appropriate narrative logic for themselves.

The pricing, valuation, and exit issues in the crypto market have also reached a point for periodic summary, the moment to move forward again.

Crypto is a market with only 0 to 1

Peter Thiel despises scale and prefers the monopoly effect after disruption.

When the VC token model of "high FDV, low circulation" collapsed, Binance as the representative of exchanges was met with industry's criticism. The subsequent Binance Alpha somewhat delayed Binance's decline, but it could no longer bear the future of the entire industry.

If we must understand the collapse of VC tokens from the perspective of "narrative," delivering quality is more meaningful than Mass Adoption, leading to a bizarre situation where the "first token, then delivery" model turns into "just issuing tokens, no delivery."

It wasn't always this way; Ethereum's ICO truly brought us infrastructure post-Satoshi Nakamoto, while tokens like $EOS were merely necessary tough explorations and painful reform, and the .com frenzy of the internet did not stop the arrival of the information age.

The history after Ethereum, whether it be the Fair Launch that severely hurt AC or Uniswap initiating user-benefiting retroactive airdrops, is not guided by being listed on Binance; we genuinely believe in the magic of tokens and the significance of governance, whether you believe it or not, at least A16Z truly does.

To be more direct, exchanges, VCs, market makers, and even the recently transitioning KOL agencies have intentionally or unintentionally discovered—twisting the token sales process generates more and faster wealth effects than waiting for user groups to surpass holder groups.

Referencing the investment, listing, and exit logic of Web2, Web3 only divides into three steps: valuation, TGE, and pricing.

Image caption: Crypto valuation system, image source: @zuoyeweb3

A robust market structure formed in the middle, with all parties engaging in spontaneous transactions, which is the most lucrative segment in the entire industry, potentially the only one.

Under normal circumstances, primary valuations should be long-term businesses, counting in years, and even the fastest ETH took 6 years from 2015 to 2021; secondary valuations should be long-term models, where exchanges and market makers should not seize retail investors' long-held returns.

October 11 tore off all false fronts, and the logic of secondary pricing shattered all value investments, leading to twisted market logic, leaving decentralized DAOs unable to maintain the illusion of survival.

Crypto has undergone various forms of resistance, from SAFT to SAFE + Token Warrant dual forms, expanding from the U.S. to establishing foundations globally, but all these efforts are futile when faced with the transaction costs in the intermediate links.

A very interesting example can be cited; Hyperliquid’s Dutch auction mechanism for spot listing ultimately yielded to the paradigm of liquidity sales being limited to mature assets like BTC/ETH or large commodities and precious metals, with no one believing in crypto's asset creation capability anymore.

Without the essence, how could the hair attach? Token economics cannot be maintained, and the position of token holders is precarious.

On one side, VCs and exchanges will take token shares, but holding long and participating in governance do not yield urgently needed financial returns; on the other side, the interests of project teams and DAO members are not absolutely aligned, and no one cares about Uniswap's fee switch anymore.

Image caption: DAO spirit degeneration, image source: @zuoyeweb3

Similar to the effects of stablecoin legislation, more and more DeFi is reverting to corporate systems, and more stocks are being tokenized, both occurring simultaneously in the magical land of America.

After MakerDAO changed to Sky, the interests of the founding team were respected; Jupiter acknowledged that buybacks could not support token prices and expand business; Circle acquired Axelar to focus on people rather than coins; and Gnosis opted to roll back, indicating everyone is feeling calm.

We can summarize that the crypto market only has moments of 0 to 1, before entering the capital operation phase; 1 to N is a daunting and unreal future. Under the FOMO of cashing out, stocks, tokens, people (founding teams, VCs, and token holders), and products have completely split.

Token economics and DAOs possess historical value, where tokens barely bind the complex interests of all parties, becoming a minimal common denominator recognized by many.

However, there are indeed stablecoins and public chains approaching the historical conversion moment of 1 to N; even an increase in headcount will create centrifugal forces on the existing structure.

Under a normal structure, the development of things follows a cyclical change of "bubble → growth → SaaS → bubble," for example, from AlphaGo in 2016 to ChatGPT in 2022, we are at the starting point of the second AI bubble.

The problem is that the crypto market is quite abnormal, with "bubble → bubble" being the absolute norm, coupled with the largest liquidity influx in human history, the entire market continues to grow amid bubbles, but we have already reached the point when stablecoins should collaborate with agents to enter countless households.

The entire industry faces a growth crisis; Alpha hunters, who excel in irrational prosperity, cannot answer how all of this began.

Some choose to embrace the wave of institutionalization, using the scale of funds to comfort anxiety; not to mention how the discount rate of such imagination works, simply clarifying unstructured financial standards is a lengthy process.

We also learn from the fat cats in the middle, identifying the lifeblood of the current structure and reorganizing to embark again.

Humans are the subjects of narrative

The structure of the market is changing, but the logic that secondary markets determine primary valuations has never changed. If it's only a market filled with bubbles, comparisons can rely on "I think" to derive ratios; then, facing a stable growth moment similar to SaaS and aligning with existing human narrative logic, we might even evaluate public chains.

Ratio = Pricing x Narrative

But before breaking out of the self-referential anomaly, a self-consistent valuation system must be established for the crypto industry to expand external gains, converting into buying power for Web3 assets rather than diving into the sell orders of Web2 bubbles.

Image caption: After narrative differentiation, image source: @zuoyeweb3

Starting from the narrative of Bitcoin, peer-to-peer electronic cash payments have already proven the crypto industry’s capability to "bootstrap," and external dependencies only require the computational power of personal PCs.

In a sense, this is more scientific than the traditional equity + IPO model because IPOs need to sell the narrative of products and sales to the wider financial market and capital institutions beyond the user base under the long investment of capital.

Bitcoin's users, capital, and financial market are completely equal, without relying on a financial market to convert Bitcoin into fiat; this is even more profound than technical decentralization.

Unfortunately, all of this is becoming extreme in the internal conflicts of equity and token rights, or one may say a simple singular tactic cannot face a complex environment.

- Infrastructure like Ethereum does not need equity but requires token rights to incentivize the development team for long-term maintenance, such as welcoming AI and facing quantum crises.

- Basic protocols like Uniswap do not need token rights; introduced holders are not responsible for the product but must compete with teams, VCs, and LPs for profit-sharing qualifications.

Intermediaries are increasing, stakeholders obscure information, and decentralization necessitates de-intermediation to achieve its goals. Ultimately, PumpFun achieves a spiritual return, where primary valuations are completely "secondary and algorithmic," instead occupying a solid market position.

I have always believed that the significance of PumpFun lies in eliminating intermediate links at an extremely low cost; although this brings new issues for scientists, we can only say there may never be a perfect answer.

However, one thing is certain; Crypto still retains a little possibility for asset creation, with Binance Alpha paving the way, engaging in pre-market trading to conjecture spot prices, while stablecoin wealth management absorbs retail funds, becoming a unique way to participate in new offerings.

Pricing = Pre-market Trading + Stablecoin Wealth Management

This model can also bypass numerous bloodsucking intermediaries, but it still cannot solve the "narrative," the core factor determining valuation multiples.

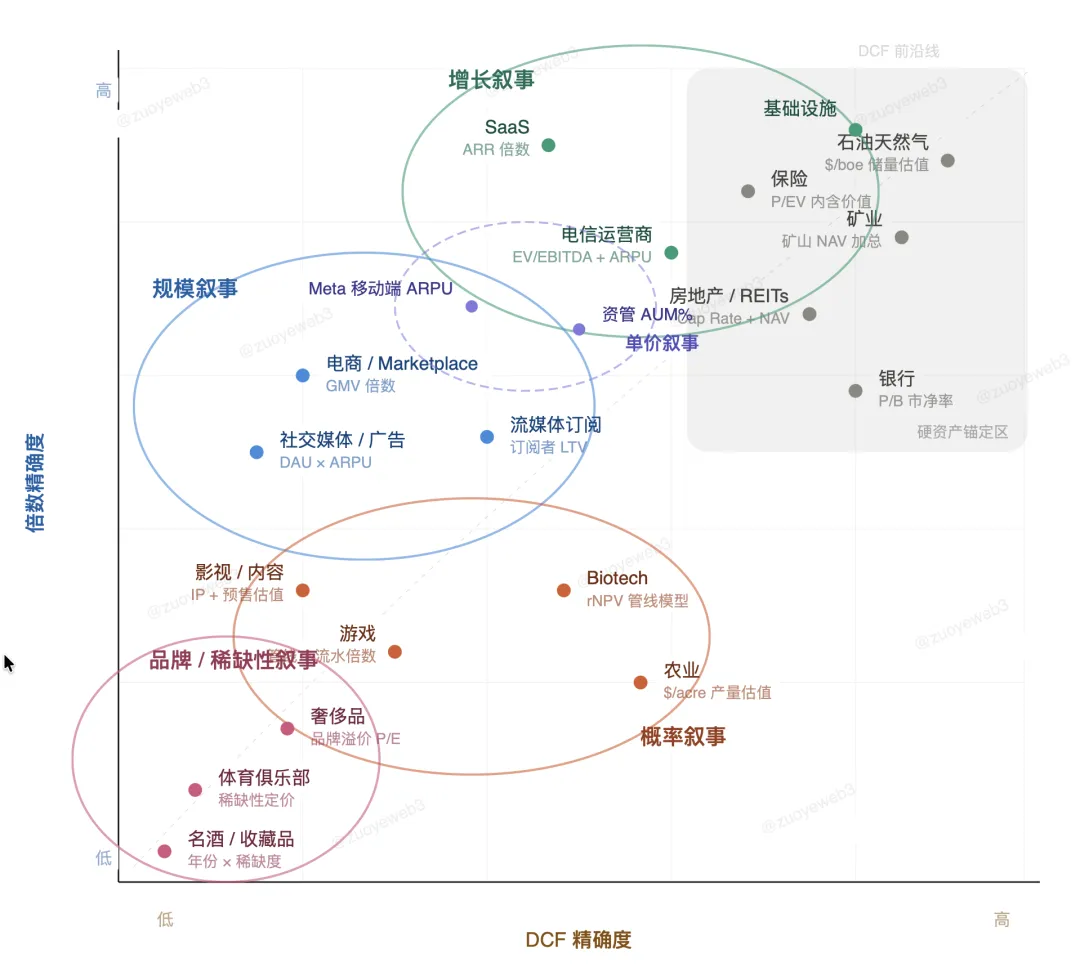

Fortunately, the traditional DCF (Discounted Cash Flow) model has been in operation for many years, and its applicability to various human industries is basically clear. Pure memes can ignore DCF, but any project facing market tests must articulate their narrative.

Image caption: Narrative categorization, image source: @zuoyeweb3

This is not complicated; financial narratives can be roughly divided into five categories:

- "Growth" is more important: for example, the ARR (Annual Recurring Revenue) of the SaaS industry is relatively fixed, so the key is to expand the growth rate of ARR.

- "Scale" is more important: for instance, internet information flow ad revenue entirely depends on traffic scale; with billions of users, a 0.01% conversion rate is still terrifying.

- "Price" is more important: this is a hybrid of growth and scale narratives, and the secret of the past decade in mobile internet, exemplified by Netflix and Apple's streaming subscriptions, competing to capture the scale and speed of traditional television, cinema, and production companies.

- "Probability" is more important: for example, pipeline models in the biotech sector competing on the success rate of new drug approvals; this isn't a scalable market, nor can it profit from imitation, but rather must rely on luck.

- "Brand" is more important: luxury goods aren't about quality; anyone who understands gets it; the crypto circle can temporarily only rely on fat penguins.

Narrative = DCF model + Adaptation Rate

What's suitable is the best; following Socratic teachings, the overall framework of human narrative is determined; the crypto industry belongs to human narratives, so it should find a model that suits itself.

For instance, among the many L2s, Arb, Polygon, and OP choose Hyperliquid, Polymarket, and Base, which in the Gas model can collectively correspond to the "price" narrative, but the issue is they all face the awkward situation of losing major clients, being kicked back to the SaaS industry, and descending into a tragic future merely pursuing growth with only existing scales.

Meanwhile, in the upcoming wave of RWA, credit, and stablecoin adoption, it's not about competing for product user scale and capital handling, but rather choosing narratives and pricing sales strategies aimed at capital markets that are more important.

For example, the emerging 2B model of Circle USDC + Canton resembles the "old-fashioned" public chain ETH + YBS’s To Everyone model, but both are enduring tough moments under pressure from token and stock prices, with the outcomes still uncertain.

For instance, SpaceX chooses Goldman Sachs to manage institutional investors' subscriptions, Citibank for individual shares sales, and UBS for handling overseas clients’ subcontracting patterns to accomplish a record-breaking $1.5 trillion IPO.

We all need to embrace future changes; irrational prosperity will no longer exist. We must choose a narrative and pricing strategy to sell ourselves, whether it be tokens or products.

Conclusion

The essence of cryptocurrency is a consumer good, which is also the historical journey of currency.

Intermediate links (VC/CEX/MM/KOL Agency) sever the flows of information and capital, as well as the complete experiences on-chain and off-chain. The pricing (listing) strategies of Hyperliquid, Polymarket, and PumpFun are all aimed at minimizing the insider trading and arbitrage caused by information asymmetry, though the strategies slightly differ.

Polymarket does not exclude insiders but even encourages insiders to disclose information, as maintaining market trading balance is more important, while PumpFun outright negates the necessity of value investing, setting all tickers purely based on PvP pricing, and Hyperliquid has correctly chosen the pre-market trading path to determine prices.

However, Binance still holds the largest liquidity, but we must not forget that the crypto industry has been driven from the very start by geeks standing at the wave's crest.

I am truly looking forward to how the AI wave will continue to unlock possibilities for ordinary people to participate in creation, and to what extent this will change human finance when combined with the future of finance—the blockchain industry.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。