Original author: danny (X: @agintender)

This article does not represent the views of Wu Shuo and does not constitute any investment or financial advice. Readers are advised to strictly comply with local laws and regulations.

Who would have thought that the modern multinational tax information system was actually triggered by a "toothpaste"? A UBS banker stuffed diamonds into a toothpaste tube to smuggle them across borders. This Hollywood-style scene unexpectedly sounded the death knell for Swiss banking secrecy laws. Today, the wheels of history are mercilessly grinding toward the crypto world — the once secret "tax haven" is about to face its reckoning.

This article will unveil the mystery of CARF: this is a global tax hunt gathering. From Binance's strategic gamble of "relocating" to the UAE to gain time by changing space, to the cruel reality that "crypto-to-crypto transactions" are no longer tax-exempt; from the compliance countdown in Hong Kong to the shattered illusions of mainland investors.

This is not only a reshaping of the industry landscape but also a survival guide that every crypto asset holder must face — after all, in this algorithmically woven cage, no one can continue to play the ostrich with their heads buried in the sand.

Introduction: What is CARF?

The full name of CARF (Crypto-Asset Reporting Framework) and its core mechanism is that reporting- obligated crypto asset service providers (RCASPs) collect tax-related information about customers and related transactions and report it to the tax authorities in their jurisdictions, which will ultimately lead to automatic international information exchange between tax authorities. This is similar to the traditional financial world's CRS but specifically focuses on the buying, selling, exchanging, custody, and transfer of crypto assets.

In simple terms, in the past, when users traded coins on exchanges, tax authorities in their resident countries found it hard to grasp relevant information comprehensively. Now, CARF connects the user's tax residence country and the exchange's jurisdiction; once they establish a CARF cooperative relationship, the user's tax residence country can obtain detailed information about its residents trading coins abroad and act accordingly for tax administration.

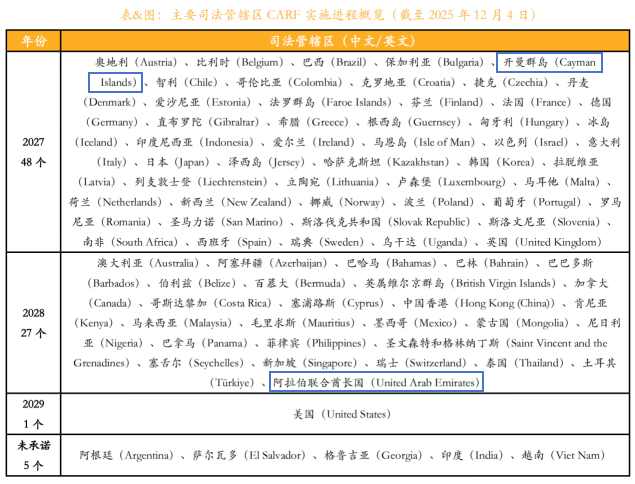

By the end of 2025, over 75 jurisdictions have committed to implement CARF in 2027 or 2028, with more than half already signing agreements with the relevant authorities. Starting January 1, 2026, the CARF framework will take effect in the first batch of 48 jurisdictions, covering the United Kingdom, the EU, Japan and South Korea, Singapore, and more.

1. Diamonds in the Toothpaste, The End of Secrecy, and The Arrival of CRS

To understand CARF, this "new sickle," we first need to look at the "old fishing net" — CRS (Common Reporting Standard).

The protagonist of the story is Bradley Birkenfeld, a former senior account manager at UBS. In order to covertly bring back his client — American real estate mogul Igor Olenicoff's $200 million tax-evaded assets at UBS to the United States.

Birkenfeld came up with a plot that only a Hollywood screenwriter would dare to use: he bought diamonds, stuffed them into a tube of regular toothpaste, evaded customs' X-ray machines, and then boldly flew across the Atlantic to hand the diamonds to Olenicoff for cashing out.

In 2007, when Birkenfeld realized in an internal bank report that he might become a scapegoat in the internal compliance cleanup, he made a "betrayal of his ancestors" decision in Swiss banking: to turn whistleblower. He walked into the U.S. Department of Justice with a file containing confidential internal emails and a client list.

Birkenfeld's testimony directly led to UBS paying a staggering $780 million fine in 2009 and unprecedentedly handing over the names of over 4,000 American clients. This marked the death of Swiss banking secrecy laws. (Interestingly, Birkenfeld ultimately took away $104 million in bounty.)

The U.S. Congress realized that relying on informants like Birkenfeld was far from sufficient; an automated monitoring mechanism had to be established. Thus, in 2010, the most overbearing offshore account tax law (FATCA) was born. Its logic is simple and brutal: "All banks in the world that want to do business with the U.S. must report the account balances of Americans to us every year."

The OECD saw the immediate effect of the U.S. move and began to replicate it one-to-one. In 2014, a global version of the standard modeled on FATCA — CRS (Common Reporting Standard) officially emerged.

That's why the underlying logic of CRS is very similar to bank transaction monitoring: it assumes that wealth ultimately accumulates in bank accounts, generates interest, and creates a balance. It is a monitoring system tailored for the "fiat currency era," designed to leave no hiding place for invisible wealthy individuals through annual "balance snapshots."

Just when everything was progressing toward regulatory hopes, a new phenomenon called Bitcoin was quietly growing. This CRS system, based on "balance monitoring," was about to confront an opponent it had never anticipated.

2. Holes in the Old Hunting Net — Why CARF is Necessary Even with CRS?

Using an AI analogy, CARF functions as a high-definition camera set up at the entrance of every compliant exchange, running 24 hours a day.

The biggest difference between it and CRS is: CRS checks "how much money you have," whereas CARF checks "where you are sending your money."

2.1 The Origin and Strategic Intent of CARF

CARF's emergence stems from the G20 countries' fear of base erosion. Although traditional CRS has been effective in targeting offshore tax avoidance, it primarily addresses traditional bank accounts and custody accounts. Cryptographic assets, due to their decentralized nature and peer-to-peer transfer capabilities without intermediaries, have become CRS's blind spot.

The OECD explicitly states that CARF aims to eliminate this blind spot by including crypto asset service providers (CASPs) in the same reporting obligations as banks. By the end of 2025, over 50 jurisdictions (including the UK, Canada, France, Germany, Japan, Cayman Islands, etc.) have committed to implement CARF. This framework has already quietly commenced data collection in places like the Cayman Islands on January 1, 2026, with an initial information exchange slated for 2027.

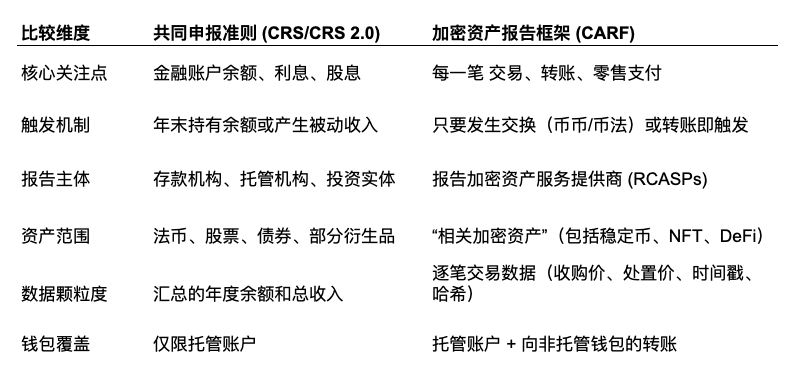

2.2 Comparison of CARF and CRS 2.0: From "Stock" to "Flow"

The core logic of CRS is monitoring "stock wealth," while the core logic of CARF is monitoring the flow of wealth.

Under the CRS framework, other than the year-end balance, tax authorities can hardly see the intermediate processes. But under CARF, if an investor exchanges Bitcoin for USDT or transfers USDT into their cold wallet, or even uses cryptocurrency to purchase a $50,000 $PUNDIAI (retail payment transaction), each action would generate a report record. CARF essentially elevates the perspective from the "static balance sheet" to the "dynamic cash flow statement."

2.3 The Scope of "Relevant Crypto Assets"

CARF's definition of "relevant crypto assets" almost covers most crypto assets:

Stablecoins: Although many stablecoins claim to be substitutes for fiat currency, under CARF, they are explicitly regarded as crypto assets. This means that the exchange between USDT and USD may no longer be "currency exchange" but a transaction, and transactions are taxable events.

NFTs: While CARF mainly focuses on assets used for payment or investment, most high-value NFTs are likely to fall under the reporting scope due to their secondary market trading attributes.

Tokenized securities: Even tokenized stocks or bonds already regulated in traditional financial markets may simultaneously be subject to both CRS and CARF coverage (although the OECD seeks to avoid duplicate reporting through CRS revisions, such overlaps are difficult to avoid according to the principle of "better to kill wrongly than to let go").

3. Retail Investors' Hypocrisy, Luck, and Disillusionment

3.1 Crypto-to-Crypto Transactions: Mandatory "Fair Pricing" Mechanism

CARF mandates that for all exchanges between crypto assets, their fair market value must be recorded in legal currency at the moment the transaction occurs.

"Crypto-to-crypto transactions" are equated with "selling first, buying later" in the eyes of tax authorities. Many people have a misunderstanding: "If I exchange Bitcoin for Ethereum, as long as I haven't changed it into fiat currency (USD/CNY), it doesn't count as selling and I don’t have to pay taxes." But that's just wishful thinking for retail investors ~

CARF requires exchanges to record: "On some year, some month, some day, Zhang San exchanged 1 Bitcoin for 20 Ethereum, and at that time, this 1 Bitcoin was worth $50,000." In the eyes of the tax authority, this constitutes a taxable event of "selling Bitcoin for $50,000." Although you may not have cash in hand, your tax bill has already been generated.

CARF completely ends the tax avoidance strategy of "using coin to generate coins." After 2026 (or 2027 in some areas), each crypto-to-crypto exchange will be recorded as an asset disposal event, leaving a definite "fiat gains record" in your tax files, regardless of whether you cash out to fiat/stablecoin.

3.2 Wallet Penetration: Transaction Hash and Address Cleaning

In CARF's XML Schema, RCASPs are required to report the specific types and values of transactions. Although the final rules removed the mandatory requirement to report all non-custodial wallet receiving addresses under strong industry lobbying, the internal system must collect and retain this address and its associated beneficiary information for at least 5 years. (aka "retention rules").

This means tax authorities have the right to access the data at any time. If tax authorities discover that a taxpayer has significant withdrawal records in 2026 but has not reported subsequent gains, they can issue bulk information requests to exchanges to accurately obtain these external wallet addresses.

When you withdraw coins from an exchange to your wallet plugin or cold wallet, the exchange must record and report (if requested) "to which address it was withdrawn." This is akin to withdrawing cash from a bank, where the bank not only records how much you withdrew but also sends someone to follow you and note which safe you stuffed the money into. Once your wallet address is linked to your real identity in the tax authority's database, all your DeFi operations on-chain will essentially be "exposed."

3.3 Standardization of Valuation Anchoring

If the transaction involves two obscure cryptocurrencies (for example, exchanging "air coin A" for "air coin B"), what if there are no fiat trading pairs? CARF specifies the "cascading valuation method": if asset A has no fiat price, the fiat price of asset B should be referenced; if neither has one, the service provider must use reasonable valuation methods for strict pricing. In short, the system must generate a fiat value sent to the tax authorities. This eliminates the space for users to report ambiguously based on price fluctuations during tax filing.

3.4 Mandatory Taxpayer Identification Number (TIN)

CARF mandates that RCASPs must collect users' tax residency status and the corresponding taxpayer identification number (TIN), but if users only declare a lower tax jurisdiction (such as Dubai), yet the exchange discovers their frequent activities in a higher-tax jurisdiction (like France) through IP addresses, phone codes, or login logs, the exchange is obligated to question the validity of the self-certification.

4. The Trap of Retrospectivity: 2026 as the "Exposure Year"

Many old OGs believe that as long as they manage their assets before the first information exchange in 2027, everything will be fine, which is incorrect. This is because everyone has overlooked CARF's "retrospective effect," meaning that the 2027 information exchange entails submitting 2026 information.

4.1 "Beginning Balance" and Historical Audits

When tax authorities receive the CARF data for the entire year of 2026 in 2027, they will first focus on the "beginning balance" or "total annual transactions."

Scenario simulation:

Assuming a Chinese national named Mr. Nakamoto sold $10 million worth of $PUNDIAI token through a compliant platform in Hong Kong in 2026. The platform will report the data to the tax authorities according to CARF. The tax authority's AI system will immediately compare Mr. Nakamoto's individual income tax return records from 2025 and earlier. If Mr. Nakamoto has never reported holdings of overseas crypto assets before, then the source of this $10 million will become an enormous question mark.

The tax authority will trace back the hash value of this transaction to ascertain when these $PUNDIAI tokens were bought. If they were purchased in 2024, then all the unreported appreciation from 2024 to 2026 will be fully exposed.

It is worth noting that many countries' tax authorities have deployed AI-based big data analysis systems specifically designed to identify discrepancies between asset stock and reported income. We expect a "tax recovery heist" for wealthy crypto holders in 2026.

4.2 The Compliance Window in 2026

For investors who have not yet complied, 2026 is effectively the last window period. Before the data doors close, investors face tough choices:

Actively declare historical assets to tax authorities, often granting chances for penalty reductions.

Reorganize asset holding methods under compliant structures (such as family trusts or offshore companies), or seek assistance from professional tax institutions for rational planning of crypto assets. (This is where an ad should go, advertising space is hotly bidding ~)

5. Behind Binance's Move: Exchanging Space for Time

Among a range of regulatory-friendly jurisdictions, why did Binance ultimately choose Abu Dhabi? Besides local policy support and funding channel advantages, an important factor lies in compliance time differences.

Binance’s original location in the Cayman Islands is among the jurisdictions that have committed to implement CARF in the first batch, with the initial information exchange expected in 2027. This means that crypto service providers (RCASPs) obligated to report under CARF must begin collecting and preserving the information for reporting starting in 2026. If Binance remained in the Cayman Islands, it would have to immediately kickstart a comprehensive CARF compliance system.

In contrast, the UAE, according to the CARF implementation timetable, is in the second batch of jurisdictions, planning to initiate information exchange in 2028.

From the Cayman Islands to the UAE, Binance secured a strategic buffer period of one year. For Binance, which serves over 300 million users, this timeframe is significant:

First, avoiding initial risks. It can observe how first batch jurisdictions like the UK and the Cayman Islands operate, learning from the experiences and lessons of other exchanges to optimize its own compliance plan.

Second, participating in rule-making. Currently, local CARF legislation and implementation details in the UAE are still being formulated, and as a prominent exchange, Binance has the opportunity to voice opinions and consult with authorities, exerting a favorable influence on the shaping of localized rules.

Third, completing system upgrades. This year provides ample time for Binance to deploy and debug a data reporting and management system that meets CARF's complex requirements.

This is what's called "exchanging space for time."

6. CARF in China: Impact and Trends

As one of the largest crypto asset user markets globally, China’s situation is somewhat special.

Some say that because mainland China is not on the OECD's initial signatory list for CARF, trading crypto in Hong Kong means that the mainland tax authorities cannot see it — this is actually a misunderstanding.

Mainland China has not yet joined or committed to implementing CARF, so the mainland tax authorities will not obtain crypto asset trading data of Chinese tax residents based on CARF mechanisms. However, this does not mean that mainland crypto billionaires can rest easy. Aside from being an active participant in CRS, even if CARF specifically targets crypto assets, if these assets are converted into fiat currency and deposited in banks, or held in financial asset forms (like ETFs), they are already within the monitoring network of CRS. Moreover, the consulting document also mentioned that CARF information will be exchanged with "partner jurisdictions."

Attentive readers will notice that Hong Kong is placed in the second tier for implementing CARF and has already initiated legislative consultation regarding revisions to CARF and CRS, establishing a clear implementation roadmap, planning to complete legislative preparations by 2027 and conduct information exchanges by 2028.

In the context of a "dual-track" regulatory approach for crypto, the impact of CARF landing in China also requires nuanced consideration:

Crypto users with Hong Kong identity are obligated to submit self-certification materials to exchanges under the CARF framework, after which their crypto asset trading data on offshore exchanges will be automatically reported and exchanged with the Hong Kong tax authorities. This means increased asset and transaction transparency, making it difficult for users to evade tax obligations based on characteristics such as decentralization and anonymity of crypto transactions.

At the same time, Hong Kong crypto exchanges, as RCASPs, must strengthen KYC in accordance with CARF requirements and build data collection and reporting systems. Any failure to register, report, perform due diligence, or submit inaccurate information could trigger legal liability, with fines reaching up to a million Hong Kong dollars.

In contrast, the short-term impact of CARF on mainland China is relatively limited. This is not unconnected to the mainland's characterization of crypto assets as "illegal." However, the trend toward tax transparency for cryptocurrencies is undeniable, and tax residents in mainland China are indeed unlikely to "rest easy." As Hong Kong connects to the CARF global information exchange network, it is not ruled out that mainland China may obtain relevant crypto trading data from Hong Kong through other channels or even join CARF in the future.

For mainland investors, the era of relying on Hong Kong as a "safe haven" has ended. Although automatic exchanges may have a time lag of several years, the "on-demand exchange" channel is open, and the data retention rules ensure that historical records can be scrutinized at any time.

7. Survival Guide — Don't Be an Ostrich with Your Head in the Sand

If you ask a Korean oppa what three things in the world are unavoidable: birth and death, Samsung, and tax.

As individuals swept along in the tide of this era, what should we do?

Pay attention to the tax consequences of "crypto-to-crypto transactions": Don't naively think that as long as you don't cash out, you won't owe taxes. From now on, every time you click "buy/sell," there could be tax implications. (In countries with capital gains tax)

Organize your accounts: Those "zombie accounts" on unknown small exchanges, or those registered with messy identities, should be cleaned up immediately. Either cancel them or withdraw the coins. Once the CARF grand net falls, these accounts will be the first targets of risk control.

Understand cold wallets: Cold wallets are still your last data fortress, but the bridges in and out have been monitored. When you transfer from Binance to a cold wallet, that action itself is a record. Although tax authorities may not see everything inside the cold wallet, they know: "This address belongs to Mr. Nakamoto, and he transferred 10 bitcoins to it in 2027."

Pay attention to the timetables of the UAE and Hong Kong: Both the UAE and Hong Kong are in the second batch (2028 exchange) of implementation areas. This means you have about one or two more years to adapt and plan. Use this time to learn how to comply or seek professional tax advisors; it's much more practical than searching for the next "tax haven."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。