Original Title: Has the Global Recession Begun?

Original Author: Capital Flows

Translation: Peggy, BlockBeats

Editor's note: While the market continues to discuss "is a recession coming," this article shifts focus and examines the underlying constraints. Currently, the interplay between energy shocks, geopolitical issues, and monetary policy is reshaping a more complex macro environment. In this environment, central banks no longer have clear reaction functions, the traditional paths of raising or lowering interest rates are both ineffective, and policy space has been "locked down."

The article redefines recession from an "economic outcome" to a "strategic state," which not only compresses growth and employment but also undermines a country's negotiating power, capital attractiveness, and external credibility, thus losing the initiative in global competition. For this reason, governments are increasingly turning to fiscal, diplomatic, and even geopolitical tools to replace monetary instruments, essentially buying time to avoid forced negotiations during a recession.

Within this framework, the core of the market is no longer the interest rate path itself, but "who can escape the constraints, and who is still trapped." This distinction is first reflected in the foreign exchange and interest rate markets and is further transmitted to asset prices and capital flows. When valuations continue to rise amidst slowing growth, it may not be due to improvements in fundamentals, but rather expectations of policies that "will not allow a recession to happen."

As energy, capital, and power intertwine again, macro issues are no longer just economic problems but a systemic game crossing policy boundaries.

Below is the original text:

This report does not aim to make predictions but seeks to restore a possible structure: if the current energy shocks continue to spill over and evolve into a global recession, what structure would this process present?

This recession is likely to unfold not along the paths we are familiar with, but rather in ways that lack clear historical precedents, transmitting layer by layer through the financial system and gradually amplifying. It is important to emphasize that "whether it happens" and "understanding how it happens" are two entirely different matters, and this article is concerned with the latter.

I should also clarify that I do not believe this scenario is inevitable. Frankly, I am not one of those "smart money" investors who went long on oil and short on stocks over the past month and stuck it out until profits materialized. My largest risk exposure currently lies within the Hyperliquid ecosystem—it has quietly benefited from geopolitical fluctuations and is one of the few assets to record positive returns in recent years, while the "Big Seven" in U.S. stocks and Bitcoin are generally in drawdown territory.

The reason I mention this is simply to illustrate: the most dangerous aspect in the market has never been making directional mistakes but rather having positions established first and then creating a framework for explaining the world afterward.

The problem is that this framework presupposes everything

Supply shocks are one of the few variables that can disrupt conventional economic relationships. In most cases, growth and inflation move in the same direction: the hotter the economy, the higher the prices; the cooler the economy, the lower the inflation. Macro policy is designed around this relationship, and the underlying logic of modern central banking is built on this assumption.

The Federal Reserve's statement is typical: "Our dual mandate is to achieve maximum employment and price stability."

Behind this definition lies an implied premise—that growth and inflation are generally compatible. In the vast majority of circumstances, this premise holds true. However, in certain specific scenarios, they can hedge against each other. Once in this state, the "dual mandate" ceases to be an actionable policy tool and becomes more of an invisible constraint.

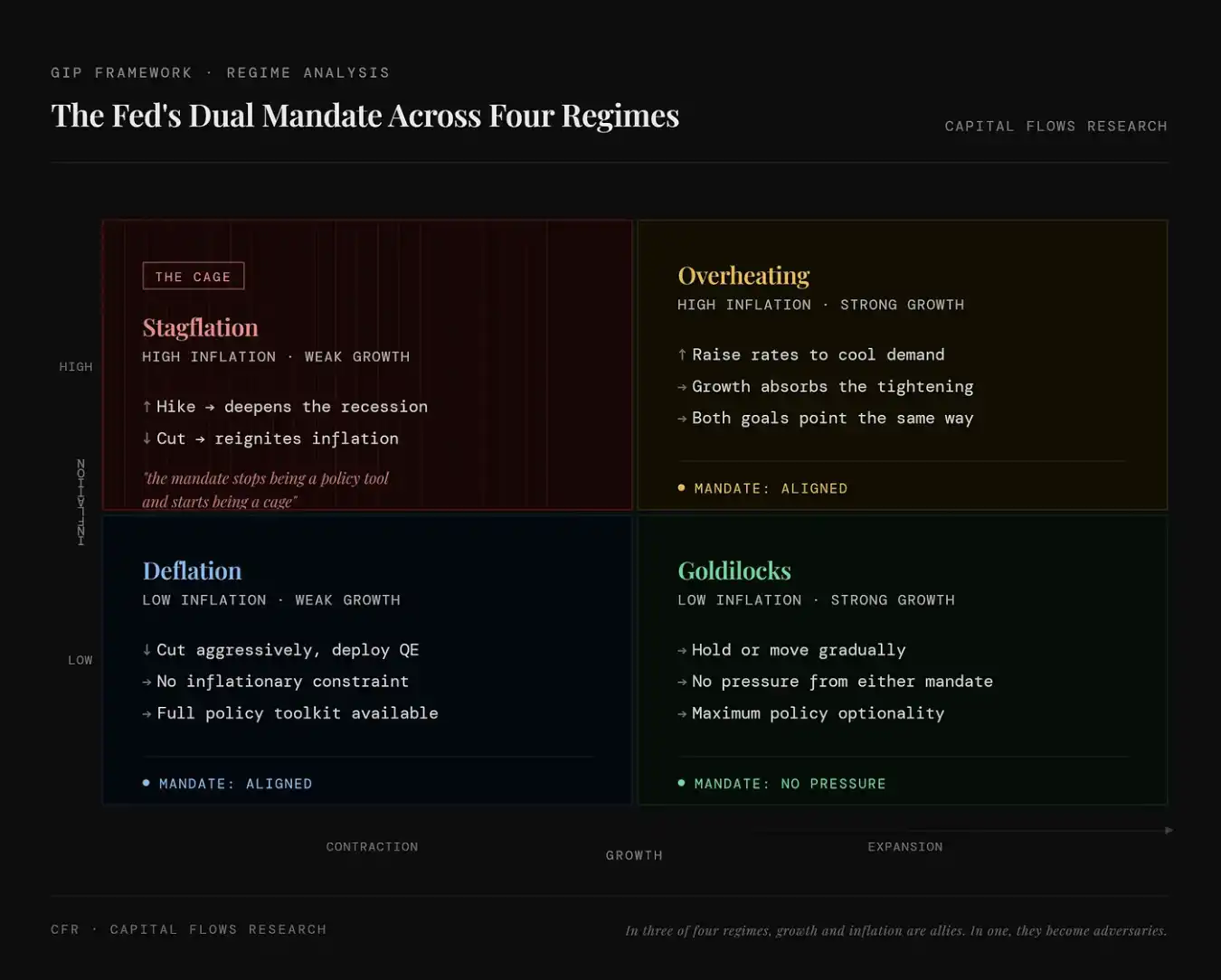

This chart illustrates the performance of the Fed's "employment + inflation" dual mandate under four economic states. The top left (stagflation) signifies the coexistence of high inflation and low growth, where both raising and lowering interest rates create new problems; policy goals conflict, and the dual mandate shifts from a tool to a constraint; the top right (overheated economy) indicates the coexistence of high inflation and high growth, where raising rates can suppress inflation without immediately harming the economy, aligning the goals, making policy relatively easy to execute; the bottom left (deflation) shows the coexistence of low inflation and low growth, where it is safe to lower rates and inject liquidity to stimulate the economy without concerns over inflation; the bottom right (goldilocks) represents the coexistence of low inflation and high growth, where both the economy and prices are in an ideal state, requiring minimal policy intervention, providing the highest flexibility.

This "constraint" is not a theoretical assumption. Since the late 1990s, a stagflationary pricing environment has appeared less than 10% of the time in the market. Among the economic states listed in the table below, it is the rarest of all but corresponds with the worst asset returns—especially for the mainstream assets held by most individuals.

This chart quantifies the frequency of different macro states and their impact on asset prices. Each row corresponds to a market combination: stocks (up/down), interest rates (up/down), U.S. dollar (strong/weak), and provides three key indicators: FREQ (frequency of the state), AVG DUR (average duration), and SPX / 10Y / DXY (performance of stocks, U.S. Treasuries, and the dollar in that environment). The situation pointed to by the red arrow is "Stocks Down / Rates Up / Dollar Up," meaning a decline in the stock market, rising interest rates, and a stronger dollar. This state appears about 9.8% (less than 10%) of the time, with negative stock returns, rising rates implying falling bond prices, while the dollar strengthens, corresponding with classic stagnation or tightening shock environments. This environment, while uncommon, often has the most destructive impact: stocks fall (risk assets are harmed), bonds fall (rates rise), and the dollar strengthens (liquidity tightens), meaning the usual stock-bond combination is under pressure simultaneously. In other words, this is the rarest macro state (about 10%) and often correlates with the worst asset performance, as there is almost no true "safe haven."

This is exactly the moment we are in. The current volatility is so severe, and people are in such a panic, not because a recession is a certainty, but because we are in the unique scenario where any action taken by the Federal Reserve will simultaneously resolve one issue while worsening another.

Transmission Chain

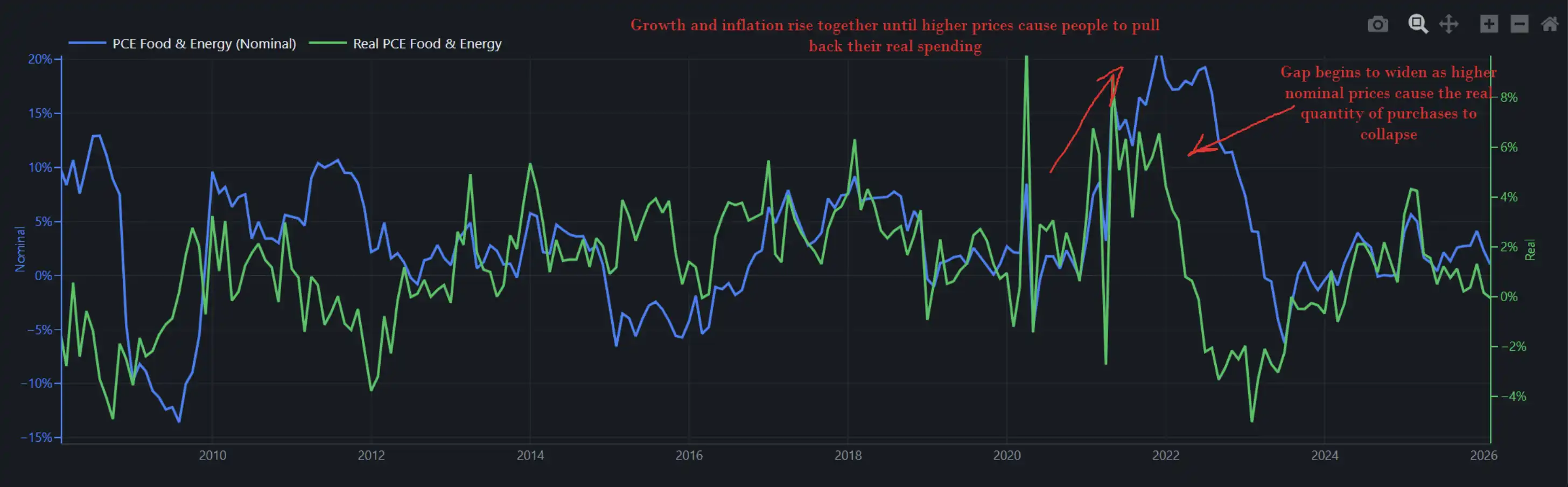

The chart below shows nominal and real changes in food and energy-related expenditures in the economy. In other words, it reflects both "how much American consumers actually spent" (quantity) and "how much they were charged" (price).

When growth and inflation rise simultaneously, higher prices do not immediately destroy demand; people choose to endure, complaining while advocating for raises and continuing to consume. This was the case in 2022, which is why the Fed could continue raising rates in that environment without immediately triggering an economic collapse. At that time, real consumption growth was almost 8%, indicating that the economy had the capacity to absorb shocks.

This image shows the divergence process between nominal expenditures (blue line, price × quantity, representing how much was spent) and real expenditures (green line, purchase quantity, representing how much was actually bought): in the early stages of inflation, both rise synchronously, indicating that rising prices have not yet suppressed demand, and consumers are still "absorbing" the shock; however, as prices continue to rise, nominal expenditures keep increasing while real expenditures begin to decline, showing a significant divergence, meaning high inflation has begun to erode real purchasing power and compress demand. In other words, inflation does not immediately destroy consumption, but once it crosses a certain threshold, it changes from "being absorbed" to "being reduced," thus becoming a critical variable dragging down the economy.

Our current real expenditure year-on-year growth rate is about 2% (whereas during the last round of energy shocks in 2022, this figure was close to 8%).

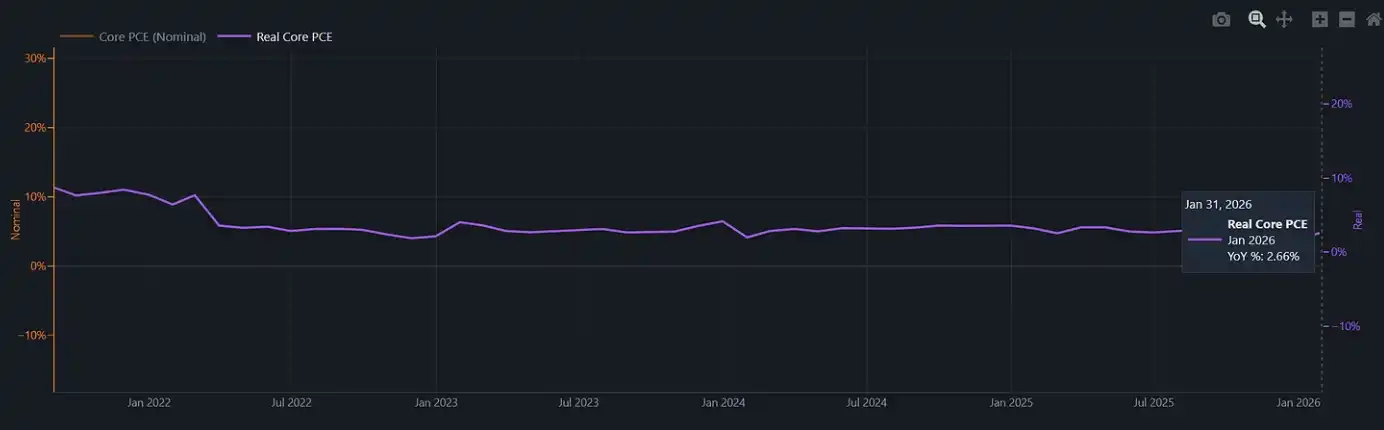

This image indicates the core real consumption (Real Core PCE) excluding inflation.

In 2022, the Federal Reserve raised rates in an economic environment that still had sufficient momentum to withstand financial condition tightening. However, this buffer has now vanished. If another round of inflation shocks occurs at this time, such as food CPI historically typically rising three to six months after energy shocks, the Fed will face a policy environment with almost no "decent exit path": continuing to raise rates with actual consumption at only about 2% may directly crush consumers; choosing to stand still and allowing inflation to rise again essentially means confirming that they are trapped in a "cage."

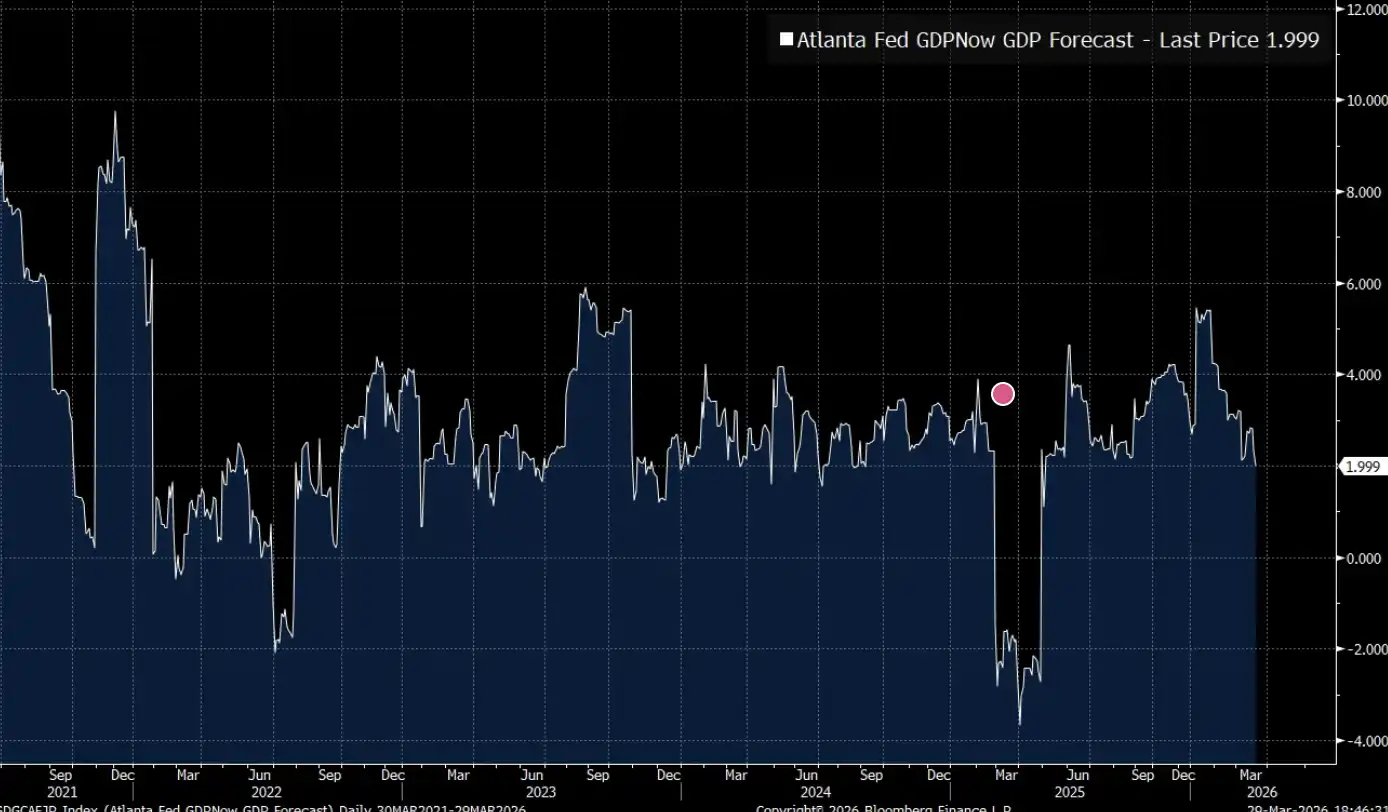

The Atlanta Fed's GDPNow forecast has just fallen below 2%.

The Atlanta Fed's GDPNow (real-time GDP forecast) shows that the U.S. economy is currently operating in the "critical growth rate" range of about 2%: not yet in recession, but the capacity to bear new shocks is very limited.

Geopolitics

There is an analytical path that focuses solely on commodity prices: rising oil prices, increasing input costs, constrained central banks, and slowing growth. For many investment portfolios, this framework is already sufficiently complete. However, it must at least be acknowledged that energy shocks do not occur in a vacuum.

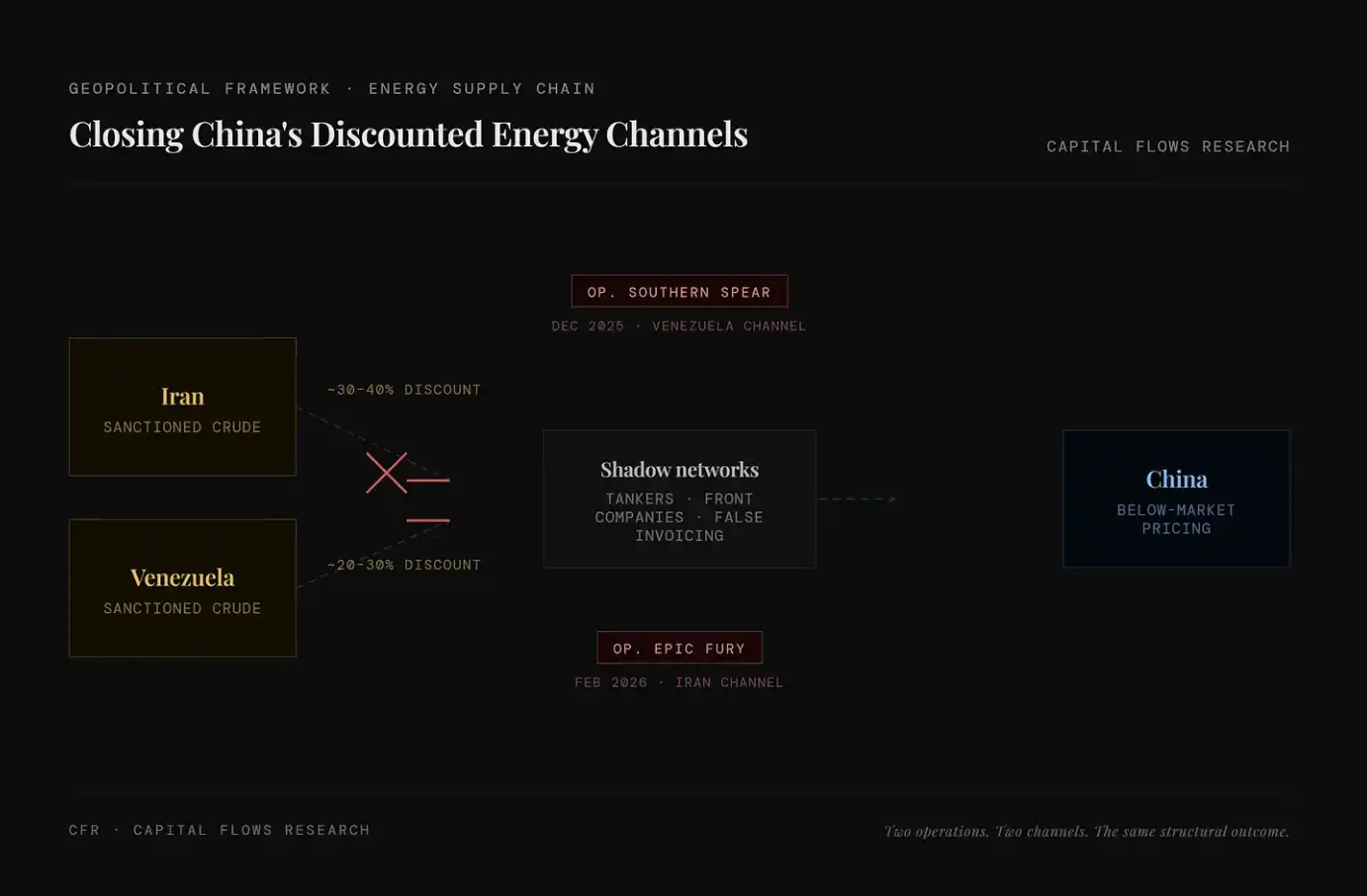

Over the past two years, the U.S. has systematically tightened channels for China to access low-cost energy, including Iranian and Venezuelan oil, resources that previously flowed through a "shadow network" at prices far below market rates. Whether "Operation Epic Fury" had such strategic considerations or merely accelerated existing trends is beyond my judgment. What I can observe is the overall structure presented around this process.

The left side of the chart displays two major discounted energy sources, Iranian oil (approximately 30-40% discount) and Venezuelan oil (approximately 20-30% discount); the middle shows a "shadow network" composed of tankers, shell companies, false invoices, etc., used to bypass sanctions and deliver these low-priced crude oils to the market. The key change is that this system is being systematically severed: "Op. Southern Spear" in 2025 targets the Venezuelan channel, and "Op. Epic Fury" in 2026 targets the Iranian channel, meaning that two major discounted energy pathways are being closed off. The result is a gradual removal of low-priced supply, subsequently raising the global energy cost floor.

Reports surrounding Jared Kushner often focus on an "ethical narrative": on one hand, he serves as Trump's chief negotiator in the Middle East, while on the other hand, he raised $5 billion from Gulf sovereign wealth funds, funded by the governments he is negotiating with.

However, compared to ethical concerns, I am more interested in the operational logic reflected by this behavior. Kushner is not acting hastily, nor is his team thrown together on a whim. When the "transaction layer" operates so frequently and intensely in a short period, it often suggests a clear structural arrangement behind it: this government is viewing military action, economic leverage, and capital flows as interconnected tools within the same system.

In other words, this is not a random operation but a sequence of actions designed and being advanced.

Note: The private equity fund Affinity Partners, founded by Kushner, draws major funding from Middle Eastern sovereign wealth funds, and his background in Middle Eastern affairs during his time in the White House continues to raise controversies regarding the boundaries of political relationships and capital flows.

For the discussion in this article, a more critical point is that this round of oil price shocks is not a random "weather event"; it has its drivers and beneficiaries. This will directly influence your judgments about its duration and policy responses.

Recession as a Strategic Vulnerability

The traditional understanding of recession is economic: contraction of output, rising unemployment, central bank intervention. However, the framework adopted here is different—it incorporates geopolitical incentives along with economic logic.

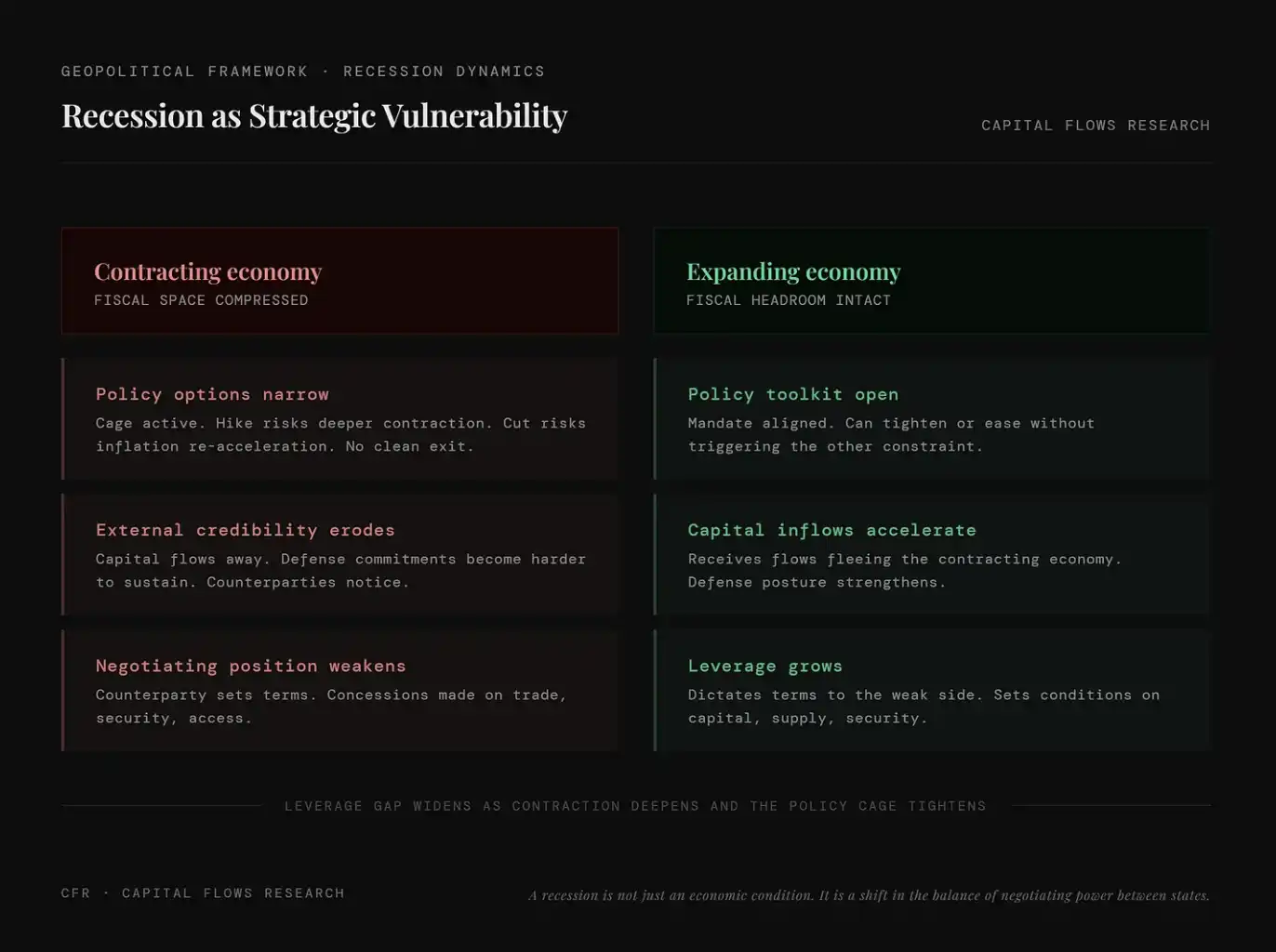

A recession is not just an economic state but a redistribution of negotiating power among nations.

The mechanism is not complicated: once a country succumbs to a recession, its fiscal space, political capital, and external credibility all contract simultaneously. Governments cannot utilize nonexistent resources, and central banks find it challenging to restore normal policy without exacerbating the contraction. Meanwhile, its trading, security, and capital market counterparts will recognize this and factor it into their negotiation conditions.

Conversely, countries that can avoid recession, or are merely "entering recession later," are on the opposite end of the scale: they can dominate the rules, attract capital exiting shrinking economies, and accumulate strategic leverage originally meant to be consumed by opponents in order to operate.

This chart compares the positional differences in geopolitics between contracting and expanding economies: the former faces compressed fiscal space, limited policy choices, decreased external credibility, and weakened negotiating capability; the latter enjoys more abundant policy tools, ongoing capital inflows, and continuously enhanced bargaining power. In other words, a recession is not just an economic issue; it also means that a nation is at a disadvantage in global competition, while growth itself can convert into actual strategic leverage.

This is not a new insight but rather the oldest logic in state governance. The uniqueness of the current moment lies in the fact that this mechanism is operating within a specific environment: the central banks of major importing economies are constrained by what we previously referred to as "the cage."

In such an environment, the G10 is not a homogenized whole but is differentiated by energy structures. The United States, Canada, and Norway are net oil-exporting countries; when oil prices rise, their energy sectors expand, and the inflation structure faced by their central banks is drastically different from other countries. In contrast, Japan, the UK, Germany, France, Italy, and most Eurozone countries are net importers, and every increase in oil price directly transmits to their production costs, trade balances, and overall inflation levels. In a world where oil is utilized as a geopolitical tool, they are essentially on the "short side" of energy.

This "cage" manifests differently between the two types of countries. For net exporters, even if faced with global stagflation pressures, they can rely on energy revenue and related jobs as a buffer; for net importers, however, they endure inflation shocks without income hedges. Their central banks cannot ease (since inflation has not receded) and cannot tighten further (as growth is already weak). Structurally, this constraint exerts far greater pressure on net energy-importing countries than it does on Washington.

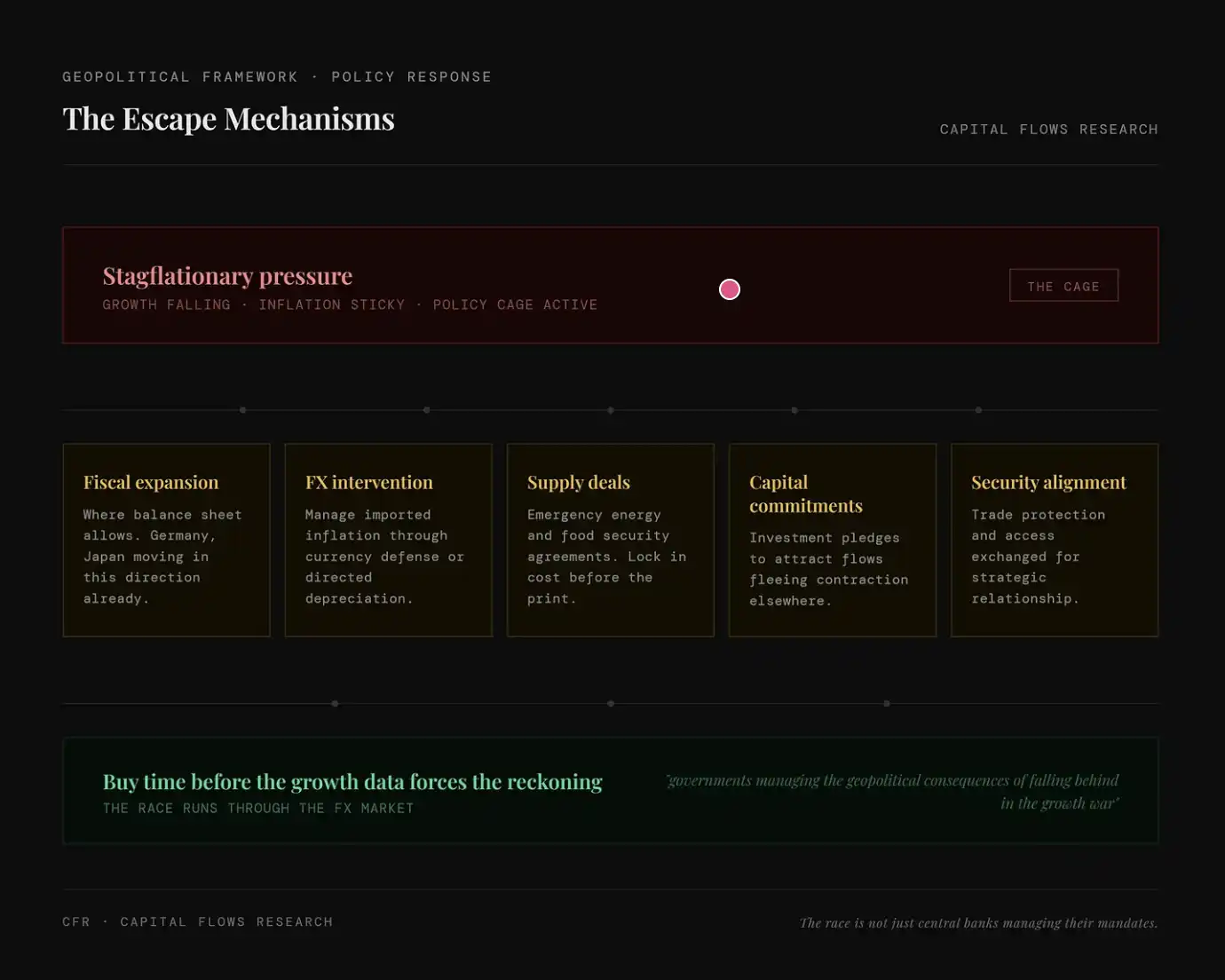

In an environment of "stagflation + policy constraints," countries are not without measures but are seeking alternative paths to "bypass the central bank." For instance, fiscal expansion, using government balance sheets to backstop (like Germany, Japan); foreign exchange intervention, hedging imported inflation via exchange rates; supply locking, signing energy/food agreements in advance to lock in costs; capital commitments, attracting capital inflows through investments to hedge against economic contraction; security binding, using security/political relationships in exchange for trade and resources.

Geopolitics, Economy, and Central Bank Constraints, and the Incentive Mechanisms Intertwined

On the geopolitical level, the key lies not in the competition among various importing economies, but in their relationship with those powers that benefit from their weakening. A country in recession becomes a more "amenable" trade partner, a more unreliable security guarantor, and more easily targets for patient, long-term subtly influential strategies—specifically, China, which shows a willingness to adopt such strategies. China does not need to actively "hit" a weakening economy; it need only wait, provide financing, lock in supply relationships, and gradually gain structural dependencies during the negotiation process as the counterpart shifts from strong to weak. Recession is precisely what makes all this possible. Thus, avoiding recession is not only an economic goal but a strategic objective. All governments in the camp of net energy importers actually understand this, though they may not express it that way.

On the economic level, the core incentive is: to "buy time" as much as possible before growth worsens further, forcing policies into more disorderly reactions. This can be through supply agreements, locking in costs before the next round of inflation data is released; through investment commitments, attracting capital that might flow out due to expectations of economic contraction; through trade arrangements, replacing existing failed pricing mechanisms. These methods cannot be called "clean" solutions, but they are better than another situation—being forced to negotiate during a recession.

At the central bank level, constraints are the most evident and the hardest to resolve. Hastily lowering rates while inflation has not receded risks further entrenching inflation; remaining still in response to continuous weakening growth could lead to a collapse in demand, making the costs of the next round of easing even higher. For net energy-importing countries, the situation is even more complex: their inflation path partly depends on the decisions of the Federal Reserve rather than being completely directed by their own policies. As interest rate differentials shift, fluctuations in their currencies relative to the dollar adjust imported inflation, leading the tension of this "policy cage" to partly depend on Washington's choices rather than Frankfurt, Tokyo, or London.

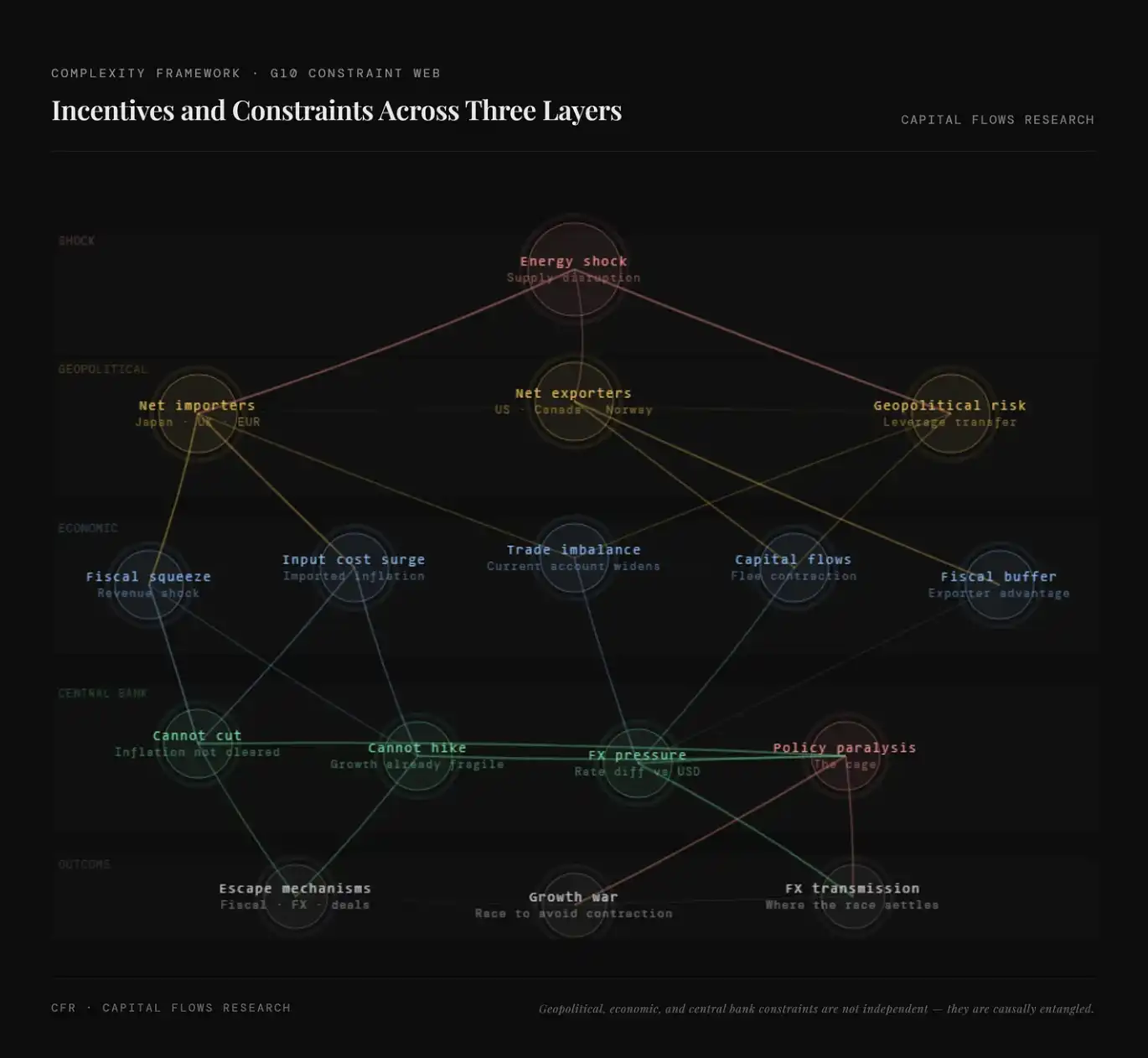

This chart systematizes the multi-level transmission relationships triggered by energy shocks: starting from supply disturbances, transmitting through geopolitical factors (differentiation between net importers and exporters, leverage shifts), economic variables (rising costs, fiscal pressures, trade imbalances, and capital flows), all the way to the central bank level's policy constraints (neither able to cut rates nor raise them), ultimately evolving into policy paralysis and a "growth race." Its core implication is that the current shock is not merely an inflation issue but a systematic repricing process interwoven with energy, capital, and power structures.

Combining the above framework, a clear environment emerges: traditional central bank reaction functions have failed, governments are replacing monetary policy with fiscal and diplomatic tools, and the resulting capital flows are no longer driven solely by interest rate differentials but rather depend on which economies succeed in escaping constraints and which remain trapped. This distinction of "who is inside the cage and who has found an exit" is first reflected in the foreign exchange market. The foreign exchange market essentially prices a gap: the distance between "where policy should go" and "where it is actually allowed to go." And when this gap simultaneously widens among multiple major importing economies, cross-border capital allocation ceases to be a secondary issue and becomes a core issue.

Connecting All the Threads

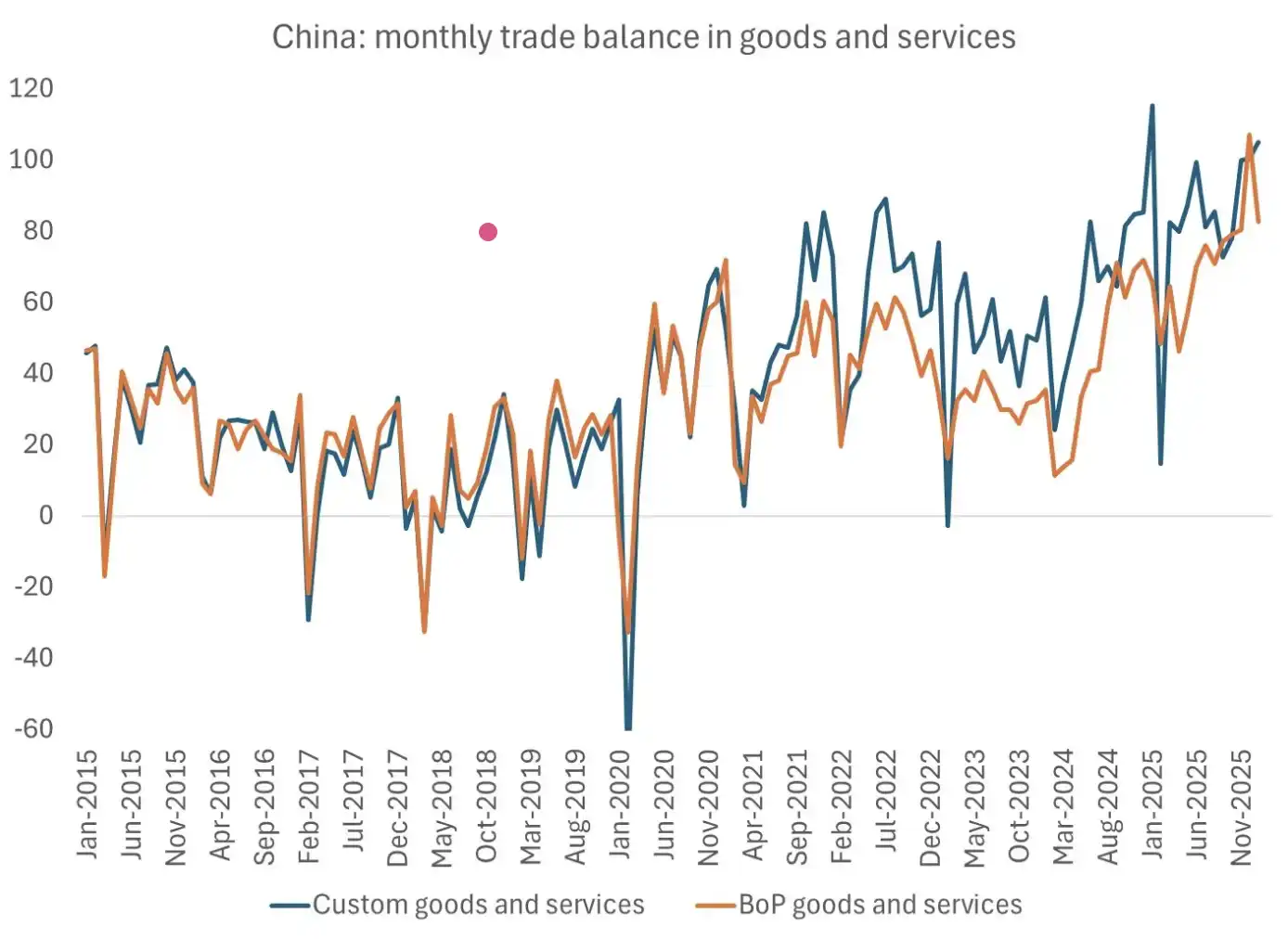

The truly thought-provoking question is not whether a recession will come, but whether the governments and central banks of major importing economies will "allow" a recession to occur. The last time a demand shock of this scale opened a window, China seized the opportunity. The recession of 2020 was a crucial point in establishing China's dominant position in global commodity exports. This position was not achieved through coercive means but rather because, while other countries were busy dealing with crises, China executed a clear strategy.

This chart shows China's trade surplus has continued to expand over the past few years and recently reached a high point. This indicates that, during the shock cycles of the past few years, China not only has not been weakened but has instead solidified its global export dominance through a continuously expanding trade surplus. Chart source: Brad Setser

Central banks currently residing in a "policy cage" are well aware of this history. Therefore, the more significant question is not whether they will continue to raise rates under supply shocks, thereby risking a recession, but whether they will, without explicitly stating so, relax liquidity conditions, tolerate rising prices of financial assets, and allow valuation expansions to avoid the political and strategic costs stemming from economic contractions.

This stock valuation chart can be seen as a way to interpret this choice. In some sense, the market may already be pricing this answer.

Note: This chart compares the P/S (price-to-sales ratio) changes of major stock markets in the U.S., Europe, Japan, and the UK, showing that amidst weakening growth, global equity market valuations are generally rising, with some markets nearing or breaching historical ranges. Its implication is that the current rise in stock prices is more driven by liquidity and policy expectations rather than improvement in earnings, reflecting that the market is pricing a policy orientation of "avoiding recession, tolerating asset price rises."

I believe that once the market reaches a consensus, and macro commentators in the media realize they are "missing the forest for the trees," there will be a dramatic repricing: first impacting the foreign exchange and interest rate markets, then spreading to aggressive pursuits of gold and silver. At that point, the "inaction" of central banks will carry more weight than any statements made at press conferences.

In my view, we are entering the final stage of this "endgame" of macro and geopolitical affairs.

Tomorrow, part two. Foreign exchange and interest rates are the core tools for pricing the aforementioned constraints and incentives. The implicit premiums and discounts in these markets are the most direct signals we have for determining which economies are "emerging from the cage" and which are still trapped within it. Next, we will start from here.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。