On April 21, 2026, when the news broke that SpaceX had reached an agreement with Cursor, Sam Altman was the quietest person in Silicon Valley. This news could be the biggest tech merger announcement of the year, but Altman did not publicly comment.

He had enough reason to stay silent. Three years ago, he led an $8 million seed round investment in Cursor's parent company, Anysphere, in the name of OpenAI, which was the first institutional investment this company received. Later, he attempted to acquire the company, but was turned down. He then pivoted and acquired Cursor's competitor, Windsurf, for $3 billion. On April 21, he watched as Musk locked in the asset he once desired at a price 20 times greater.

Six days later, he was set to meet Musk in a court in Oakland, California.

This $60 billion deal is interpreted by almost everyone at face value. But there are five layers of truth systematically obscured behind it: Musk is not a strong player, $10 billion is not a breakup fee, the integration began before the announcement, the computing rent came before the agreement, and the entire scheme serves a larger IPO bill.

Extravagant Defense

Let’s start with the layer "Musk is not a strong player."

xAI currently owns the world's largest AI computing cluster, the Colossus supercomputing center, with 100,000 NVIDIA H100 chips, planning to expand to 200,000. This is the number that appears most frequently in mainstream reports about the company and is also the easiest number to form the intuition that "Musk has already won the computing war."

However, shortly after the Colossus was completed, an internal memo quietly circulated to the media. The memo was written by Michael Nicolls, who had just been assigned from his position as Senior Vice President of SpaceX's Starlink project to serve as President of xAI. In the memo, he harshly evaluated that xAI was "clearly lagging" in the AI competition, and provided specific numbers to support this judgment: the model floating-point usage rate (MFU) for xAI was about 11%, while the industry average is between 35% and 45%.

Colossus supercomputing center in Memphis, Tennessee, USA

This means that more than 60% of those 100,000 H100 chips are idle. The world's largest computing cluster is performing at less than one-third of the industry average efficiency.

The timing of this memo’s delivery came with an even more awkward backdrop. All 11 co-founders of xAI had left, and Musk publicly admitted that xAI "did not build well the first time and is being rebuilt from scratch." The company’s most ambitious all-purpose AI agent project, "Macrohard," was stalled due to the departure of its core leader. Nicolls was brought in to transplant SpaceX’s extreme efficiency engineering culture, to get that massive machine running at high speed again.

Locking in Cursor for $60 billion is not a purchase made casually by a strong player expanding its territory. It is an AI company that is technically being rebuilt and suffering from significant inefficiency, using money to buy time while searching for a sufficiently large commercial load for that idling machine. And all of this groundwork began 40 days before the official announcement.

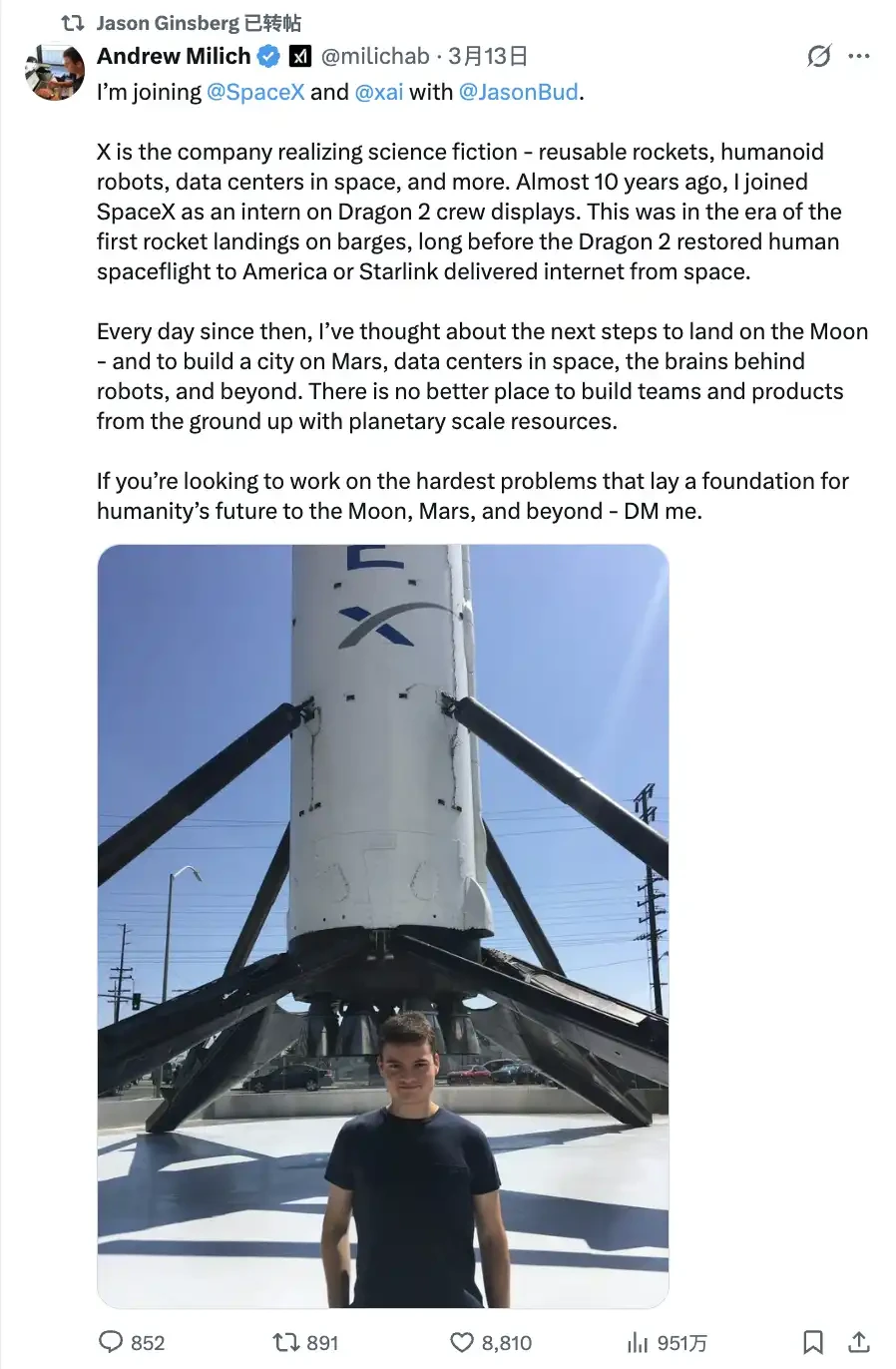

Ginsberg and his partner Andrew Milich are the co-leads of Cursor's product engineering and are responsible for the architecture and iteration of all core product features at Cursor. They were the two key figures on the product side as Cursor grew from zero to an annual revenue of $2 billion, achieving record growth in SaaS history. On March 12, they announced that they would join xAI, reporting directly to Musk, with the task of rebuilding the programming capability of the Grok model from scratch.

Andrew Milich left a statement when announcing his joining xAI: "Nearly ten years ago, I interned at SpaceX and worked on the cockpit display system development for the Dragon 2 spacecraft." The significance of Ginsberg's return can only be understood in the context of his complete trajectory.

The cockpit display system of the Dragon 2 spacecraft was one of SpaceX's most critical human-computer interaction engineering projects, and very few interns could participate in this project. After leaving SpaceX, he and Milich co-founded Skiff, an end-to-end encrypted document collaboration platform, which was acquired by Notion in February 2024. Afterward, the two joined Cursor, pushing it to the pinnacle of the AI programming market. Now, armed with years of product judgment and technical architecture experience accumulated at Cursor, he has returned to the starting point of this path.

When you expand this timeline: Ginsberg's return, Milich's joining, the two clearly tasked with "rebuilding Grok's programming capabilities." The essence of the acquisition was primarily completed 40 days before the formal announcement. The contract is the endpoint, not the starting point.

The Real $10 Billion Bill, and the Precise Shot Before Court

The structure of the acquisition deal is designed so that at some point later this year, SpaceX must make a binary decision: either to exercise the purchase option for $60 billion or pay $10 billion as a "cooperation fee." If the acquisition does not occur, the $10 billion is a one-time payment to settle the cooperation relationship.

Media reports commonly refer to this $10 billion as a "breakup fee," but this definition fundamentally obscures its true nature. To understand why Cursor would accept such a peculiar structure, one needs to first grasp the situation it faces.

Cursor's rise relied on the foundational model provided by Anthropic. Claude is its most core technology base. Then, Anthropic launched Claude Code, a programming AI tool that directly competes for the same user base as Cursor, turning the supplier into a competitor. But that is not the worst part.

Internal analysis at Cursor shows that the highest monthly subscription fee for Anthropic's Claude Code is $200, but the actual computing cost incurred for each heavy user by Anthropic reaches about $5,000. Last year, that figure was $2,000, a 1.5-fold increase in a year. This means that Anthropic is providing this service to the market at a loss of about $4,800 per user per month.

It uses venture capital ammunition to wage a pricing war that leaves competitors economically cornered. Any tool company that continues to rely on the Anthropic model and provide users with equivalent experiences cannot cover API costs with subscription fees.

Faced with this situation, Cursor's CEO Michael Truell stated, "Our strategy is to comprehensively use the best technology provided by partners along with the technology we develop ourselves." This is the clearest statement the founder could make in public. The other side of this is that Cursor must train its own model and must find a source of computing power independent from its competitors.

xAI's Colossus cluster is currently the largest independent source of computing power available for Cursor’s use. The $10 billion "cooperation fee" wraps the prepaid value of this computing rental relationship. Cursor's situation also just happens to make it the most suitable piece in a larger game.

The relationship between OpenAI and Cursor has a complete three-year arc that mainstream reports have never pieced together in full.

The story begins in October 2023. OpenAI led Anysphere's $8 million seed funding round, becoming Cursor's first important institutional investor. At that time, Cursor was still a fledgling AI programming tool company, and OpenAI's money was both funding and endorsement.

Two years later, the situation had completely reversed. In November 2025, Cursor completed a $2.3 billion Series D round, with a valuation of $29.3 billion. OpenAI began to seriously discuss the possibility of acquiring Cursor, with the former investor wanting to buy back the seed they had initially invested. Cursor declined. OpenAI then turned to acquire Cursor's competitor, Windsurf, which was previously known as Codeium, for $3 billion. The $30 billion unicorn refused, ending up having to settle for a suboptimal choice at one-tenth the price.

Then came April 21. On the day SpaceX announced the $60 billion deal, there were still six days until Altman and Musk would face off in federal court in Oakland. The lawsuit stemmed from Musk's accusation that Altman betrayed OpenAI's original non-profit mission, leading to the most public confrontation of years of grievances.

There is no evidence to suggest that April 21 was a deliberately selected date. But the dramatic timing cannot be ignored: six days before going to court with Altman, Musk publicly locked in the company that OpenAI had previously invested in and was later turned down for acquisition at a price of $60 billion. The seed invested three years ago for $8 million is now worth $60 billion. This calculation is very clear in Altman's mind.

However, the calculation Musk is making is not just aimed at Altman.

The Underlying Card for the IPO

On April 1, 2026, SpaceX secretly submitted an IPO application to the U.S. Securities and Exchange Commission with a target valuation of $17.5 trillion. The core narrative supporting this figure is SpaceX's grand plan to deploy up to one million data center satellites in space, using solar power and the natural cooling of space to replace the electricity and water cooling needs of ground data centers, providing cheaper infrastructure for AI computing. Musk has claimed on multiple occasions, "Space will be the cheapest place to run AI."

However, according to disclosures from Reuters and other media regarding the S-1 filing, SpaceX acknowledged in the legal documents submitted to regulators that this plan involves "unproven technology," and its commercial viability carries uncertainty. The company's official assessment of its biggest AI bet is a question mark.

This question mark explains the real logic behind acquiring Cursor. Whether SpaceX’s space computing plan can materialize depends on an unverified physical and engineering hypothesis. Cursor generates 150 million lines of code daily for global enterprises, representing a concrete and clearly defined real demand. If the future of the space computing plan is uncertain, the most important thing is to find a sufficiently large and stable commercial load for that idling Colossus cluster on the ground.

With an annual revenue of $2 billion, Cursor is one of the fastest-growing SaaS products globally. Integrating it into SpaceX's ecosystem offers not just an outlet for monetizing computing power but also a real case to demonstrate to capital markets that "AI infrastructure has already landed." In an IPO roadshow, this is more convincing than any projections about space data centers.

Acquiring Cursor is SpaceX’s way of using a certain software asset to underpin an uncertain hardware vision.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。