Written by: @BlazingKevin_, Blockbooster Researcher

The scarcity of the legislative window determines that this game has no second chance.

In the spring of 2026, the regulatory framework for cryptocurrencies in the United States is at a historic turning point. The legislative window for the "Clarity Act" has entered the final countdown, the compliance requirements of the "Genius Act" are profoundly reshaping the stablecoin market structure, and the financial disclosure of Federal Reserve Chairman nominee Kevin Warsh, with over $100 million in crypto investments, indicates an unprecedented cognitive shift in U.S. monetary policy and digital asset regulation. Three main lines intertwine to collectively form the most important institutional variables for the cryptocurrency industry in 2026.

We systematically analyze five core issues: ① The political economy of the Clarity Act; ② The prudent regulatory logic and market impact of the Genius Act; ③ The essence, compromises, and trends of the stablecoin yield war; ④ The interest structure of the quadripartite game; ⑤ The global chain reaction of passing or not passing the legislation—aiming to provide a comprehensive analytical framework for researchers, practitioners, and policy observers.

Three core conclusions

① The legislative window cannot be missed: If the Clarity Act does not complete marking in the Senate Banking Committee by the end of April, the probability of passing in 2026 will plummet to a very low level, with the bill potentially being shelved for four years, during which the global competitive landscape for crypto regulation will solidify in the absence of U.S. participation.

② Compliance becomes a core competitive advantage: The AML/CFT mandatory requirements of the Genius Act will inevitably drive the stablecoin market toward concentration among leading compliant firms, with USDC and Tether's newly launched USAT being the biggest beneficiaries, while USDT's space in the U.S. institutional market will be structurally compressed.

③ Regulatory cognitive leap across generations: If officials with deep backgrounds in crypto investments, such as Kevin Warsh, lead the Federal Reserve, it will create the most crypto-friendly macro policy environment to date—not just deregulation but a strategic acceptance of integrating crypto assets into mainstream financial infrastructure.

1 Background: From Regulatory Vacuum to Legislative Conclusion

1.1 Historical Roots of Regulatory Chaos

Over the past decade, U.S. crypto regulation has fallen into a deep structural dilemma: the SEC forcibly applies the "Howey test" framework of securities, while the CFTC claims commodity characteristics, resulting in blurred regulatory boundaries between the two agencies that leave firms unable to determine their own compliance until they are sued. This "Regulation by Enforcement" model has accumulated numerous legal uncertainties, causing conservative institutions like pension funds and insurance companies to remain on the sidelines.

1.2 Legislative Evolution: From the Genius Act to the Clarity Act

In July 2025, Congress passed the Genius Act, establishing the first federal prudent regulatory framework for payment stablecoins—100% reserve requirements, mandatory AML compliance, and OCC oversight. In the same month, the Clarity Act passed the House with a bipartisan vote of 294:134, aiming to set up a market structure framework covering the entire digital asset ecosystem. On March 17, 2026, the SEC and CFTC jointly ruled that major assets like Bitcoin and Ethereum would officially be classified as "digital commodities," ending a longstanding jurisdictional dispute. The Clarity Act is the grand finale of this series of legislation.

1.3 Why the Time Window is So Scarce

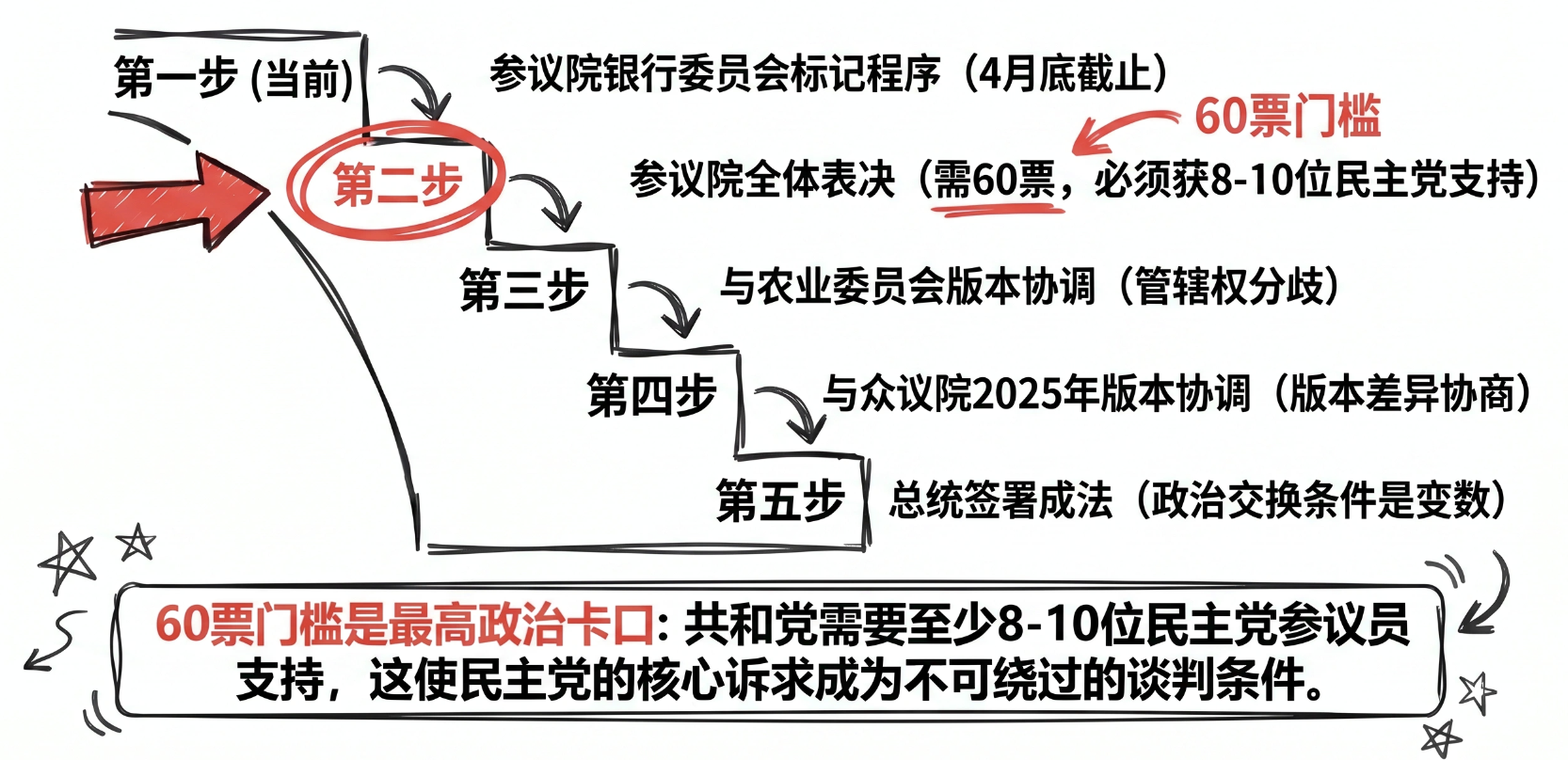

The midterm elections in November 2026 constitute a hard political deadline: if the House changes hands, the pro-crypto Republican legislative coalition will dissolve, removing the political basis for the Clarity Act. Senator Lummis gave the most straightforward warning on April 11—"Pass it now, or wait until 2030." Senator Moreno further clarified that if the bill is not sent to the full Senate by May, digital asset legislation might not be taken seriously for years.

J.P. Morgan's latest assessment states: "Negotiations have entered the final sprint phase, with points of contention reduced from several to only two or three."

J.P. Morgan predicts: if the bill passes in mid-2026, the scale of institutional entry into digital assets will significantly accelerate in the second half of the year, with pensions and insurance funds gaining a clear compliance path.

2 Genius Act: Prudent Regulatory Logic and Market Restructuring

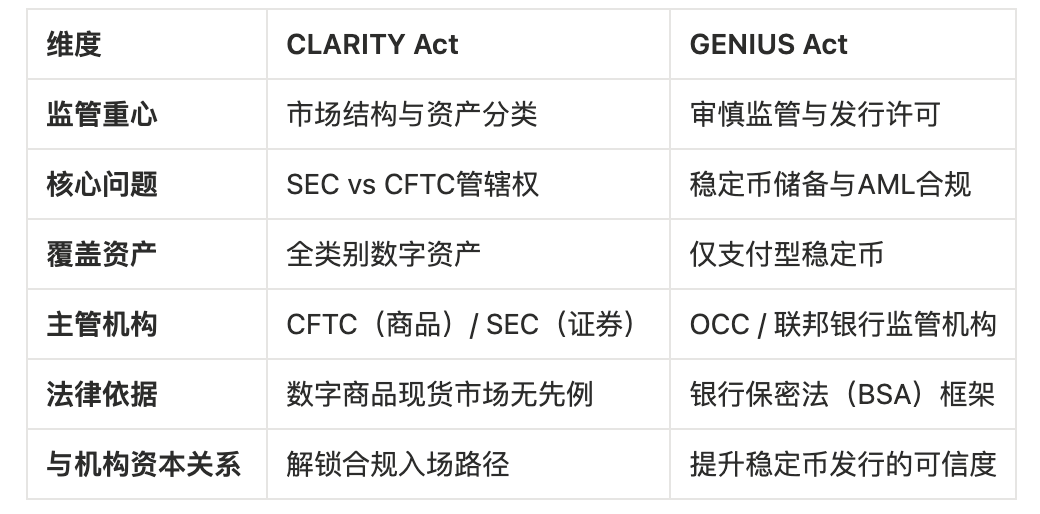

2.1 Regulatory Logic: Genius Act vs. Clarity Act

The regulatory logic of the two bills has essential differences. The Clarity Act focuses on market structure, addressing asset classification and trading platform regulation issues; whereas the Genius Act emphasizes prudent regulation, placing payment stablecoins under a compliance framework similar to banks.

The core of the Genius Act is to explicitly define stablecoin issuers as "financial institutions" under the Bank Secrecy Act, requiring them to establish effective AML/CFT plans, a mandatory sanctions compliance program, 1:1 reserve support, and to be subject to strict regulation by federal agencies like the OCC. New regulatory requirements proposed by FinCEN and OFAC necessitate the establishment of complex technical control systems to freeze or refuse non-compliant transactions and conduct independent compliance testing.

These fixed compliance costs—professional AML compliance officers, enterprise-level monitoring systems, independent audits—pose a significant barrier to entry for small issuers, inevitably pushing the market toward concentration among leading compliant firms. Forbes analysis points out: "Compliance costs will lead to market consolidation."

2.3 Strategic Divisions in the Stablecoin Market

USAT, issued by Anchorage Digital Bank with Cantor Fitzgerald as the custodian, fully complies with the strict standards of the Genius Act. Tether enters the U.S. institutional market through this highly compliant sub-brand while maintaining USDT's global dominance—this is a carefully designed "dual-brand divergent strategy": using USDT to guard global retail and emerging market liquidity, while competing for U.S. institutional funds with USAT.

3 The Stablecoin Yield War

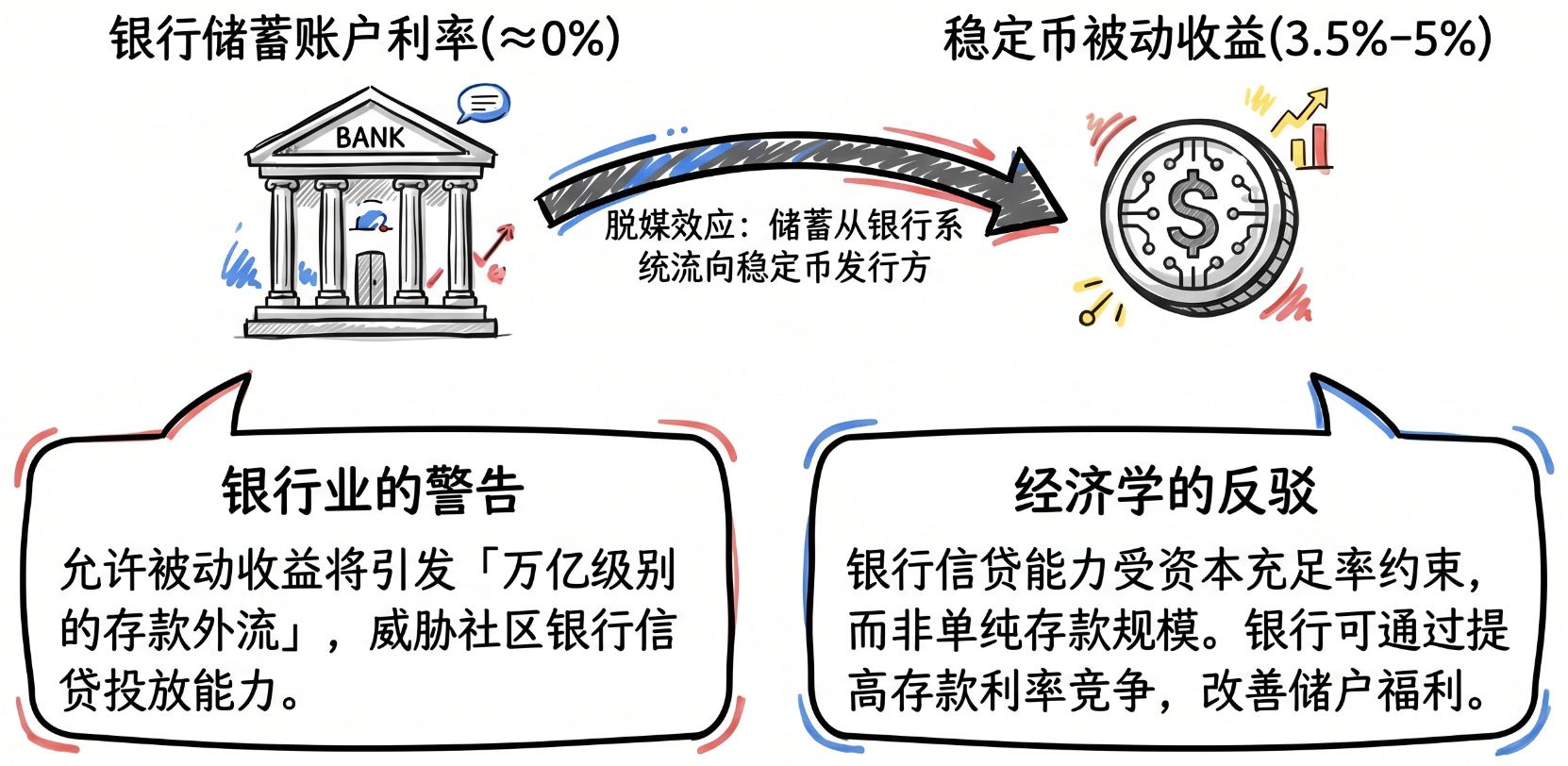

3.1 The Essence of the Controversy: Deposit Disintermediation and Interest Rate Competition

The economic core of the stablecoin yield controversy is the deposit disintermediation effect: if holding stablecoins can yield passive returns close to short-term Treasury yields (historically ranging from 3.5% to 5%), while bank savings account rates are nearly zero, a strong incentive for fund migration is created. Bank of America CEO Brian Moynihan warned in February 2026 that allowing passive yields from stablecoins could trigger "trillions in deposit outflows," threatening the lending capacity of community banks.

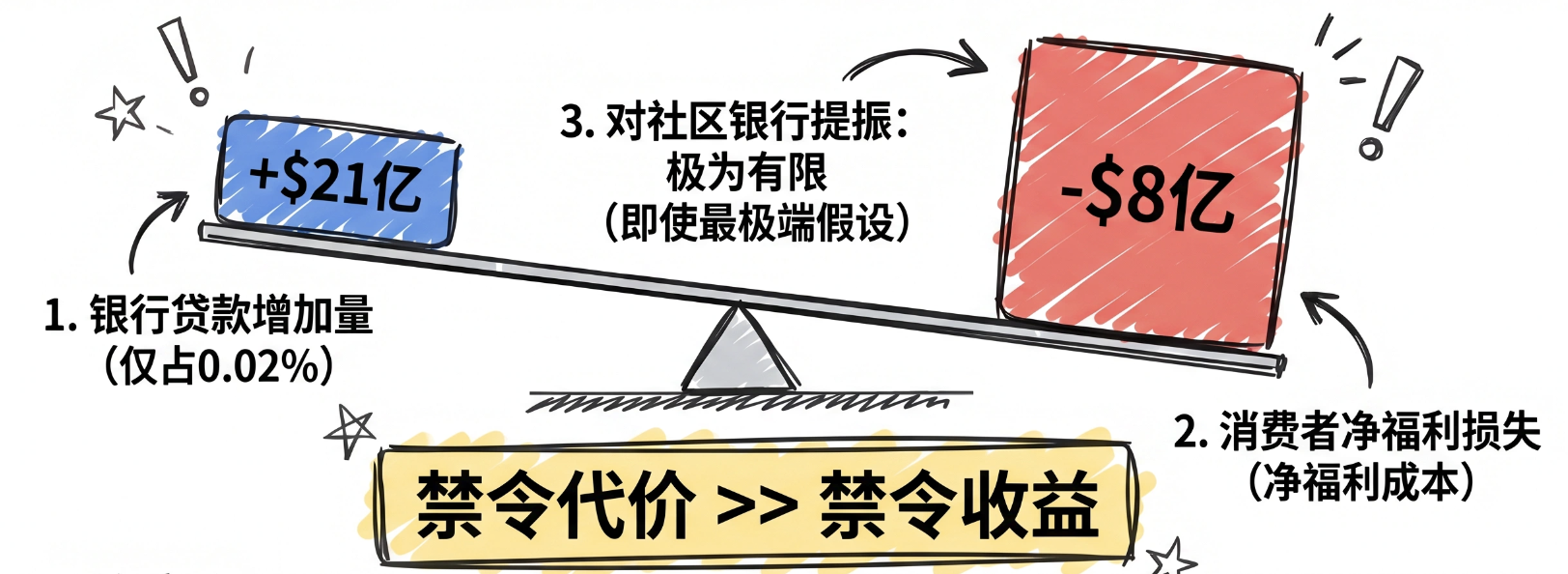

However, the report released by the White House Council of Economic Advisors (CEA) on April 8, 2026, directly challenges the banking industry's argument: an outright ban on stablecoin yields would only increase bank lending by about $2.1 billion (accounting for only 0.02%), while simultaneously inflicting a net welfare loss of $800 million on consumers. Even under the most extreme assumptions, the boost to community bank lending would be very limited. This internal government data report provides the most powerful policy lobbying tool for the crypto industry.

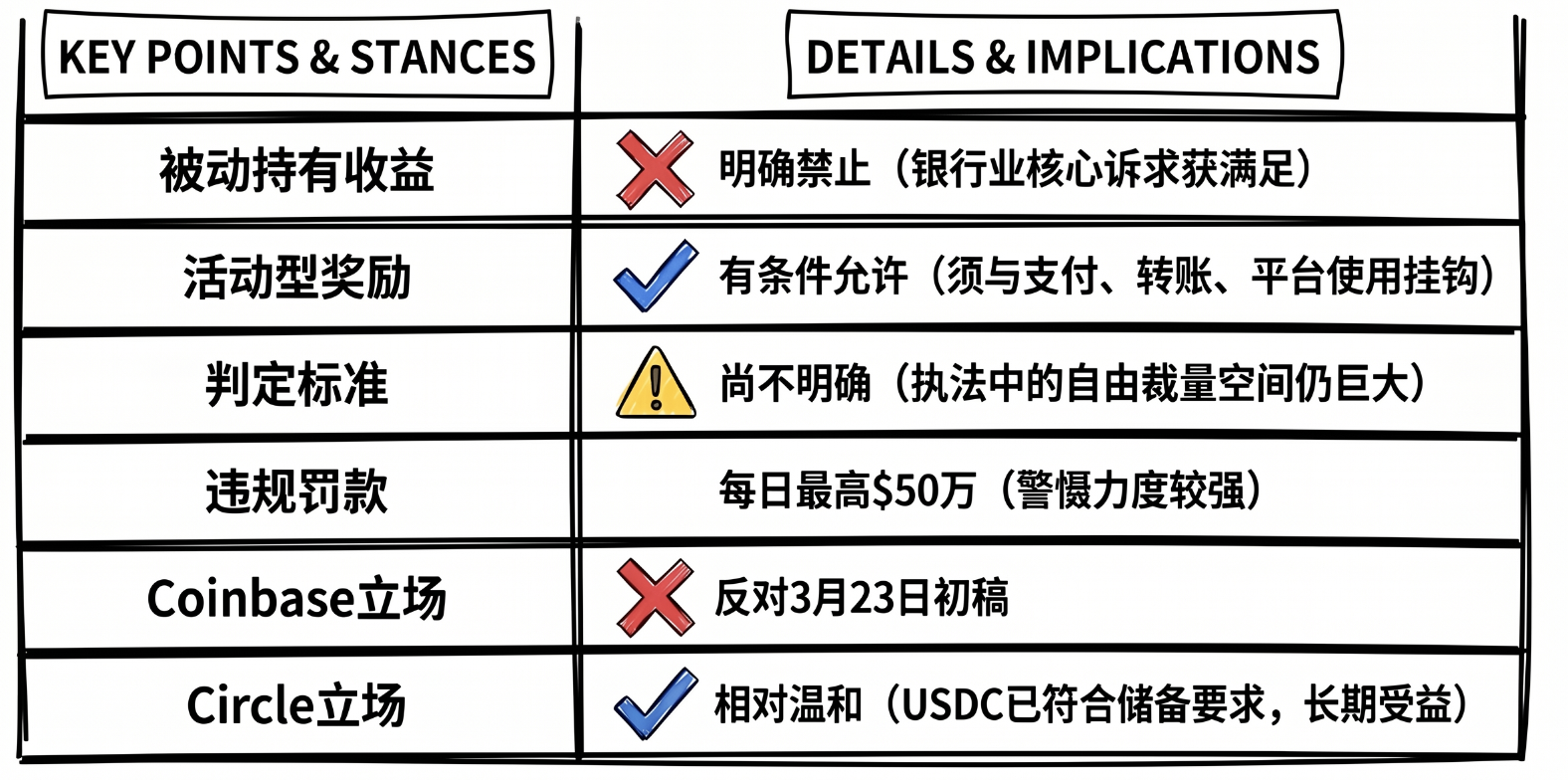

3.2 Analysis of the Tillis-Alsobrooks Compromise

On March 20, 2026, Republican Senator Thom Tillis and Democratic Senator Angela Alsobrooks reached a principled compromise, with the core framework as follows:

3.3 Four Unresolved Battlefields

- The specific distinguishing criteria for stablecoin activity reward: how law enforcement differentiates "activity-related" from "passive," with unclear technical and legal precedents.

- The Fed's veto power over state-chartered issuers: directly determining whether institutions like USDC can access the federal payment rail.

- AML compliance requirements for DeFi: some Democratic senators are concerned that non-custodial protocols become loopholes for anti-money laundering.

- Government officials' conflict of interest clauses: a rigid prerequisite for bipartisan cooperation, directly conflicting with the Trump family's business interests in crypto.

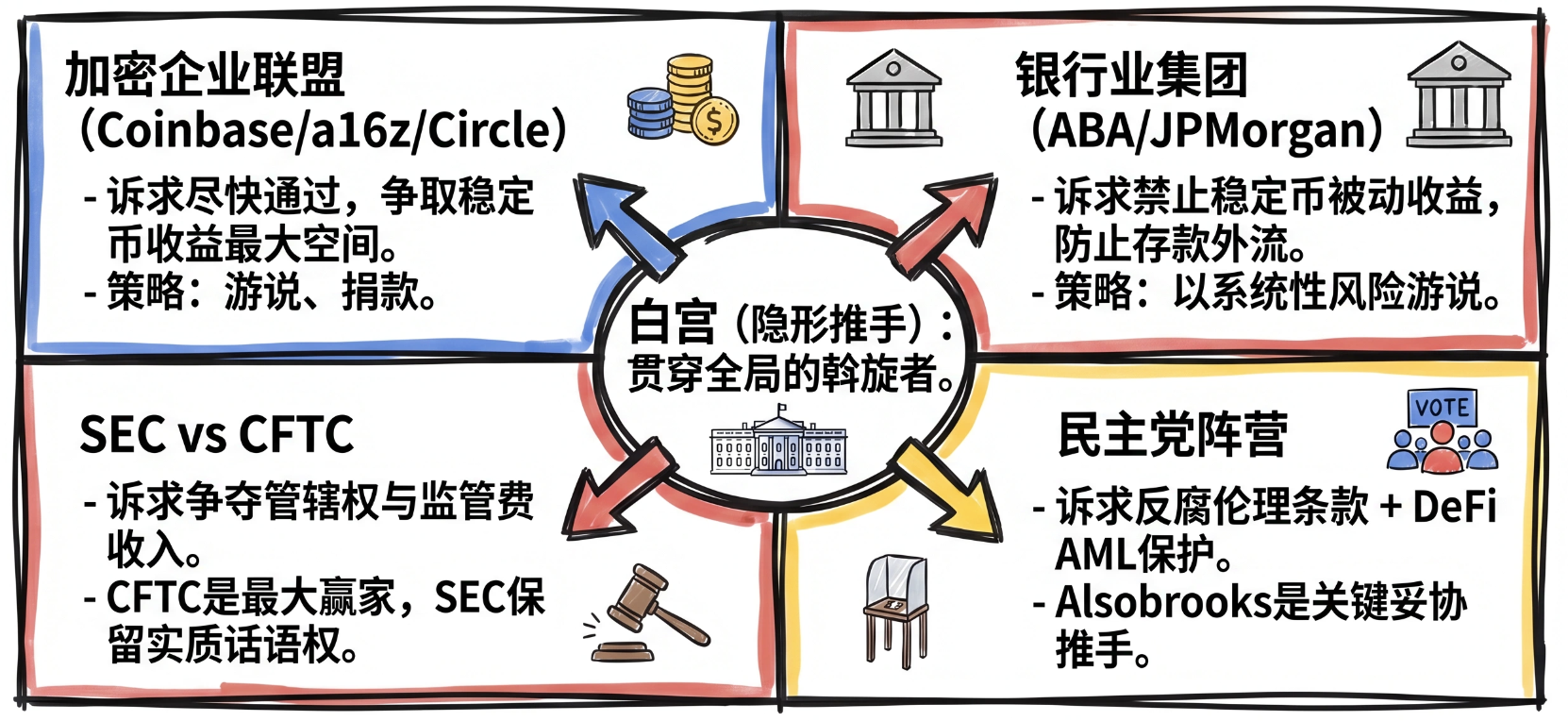

4 The Quadripartite Game Pattern

4.1 Game Map

4.2 The White House: The Strongest Hidden Force

The Trump administration positioned the Clarity Act as the core legislation of the "Make America the Global Crypto Capital" strategy, with a clear political will. Patrick Witt, executive director of the White House's Presidential Advisory Council on Digital Assets, personally leads negotiation mediation; Deputy Treasury Secretary Scott Bessent publicly urged for rapid advancement in spring 2026; and the White House's CEA report actively provides data ammunition for loosening stablecoin yields.

However, the White House faces a dilemma: accepting the Democratic president's ban on holding crypto would effectively admit compliance risks exist for Trump family business interests; if rejected, the 60-vote threshold cannot be crossed, and the bill will not advance regardless.

4.3 Five-Step Legislative Process: Each Step is a Veto Point

5 The Global Impact of Passing or Not Passing

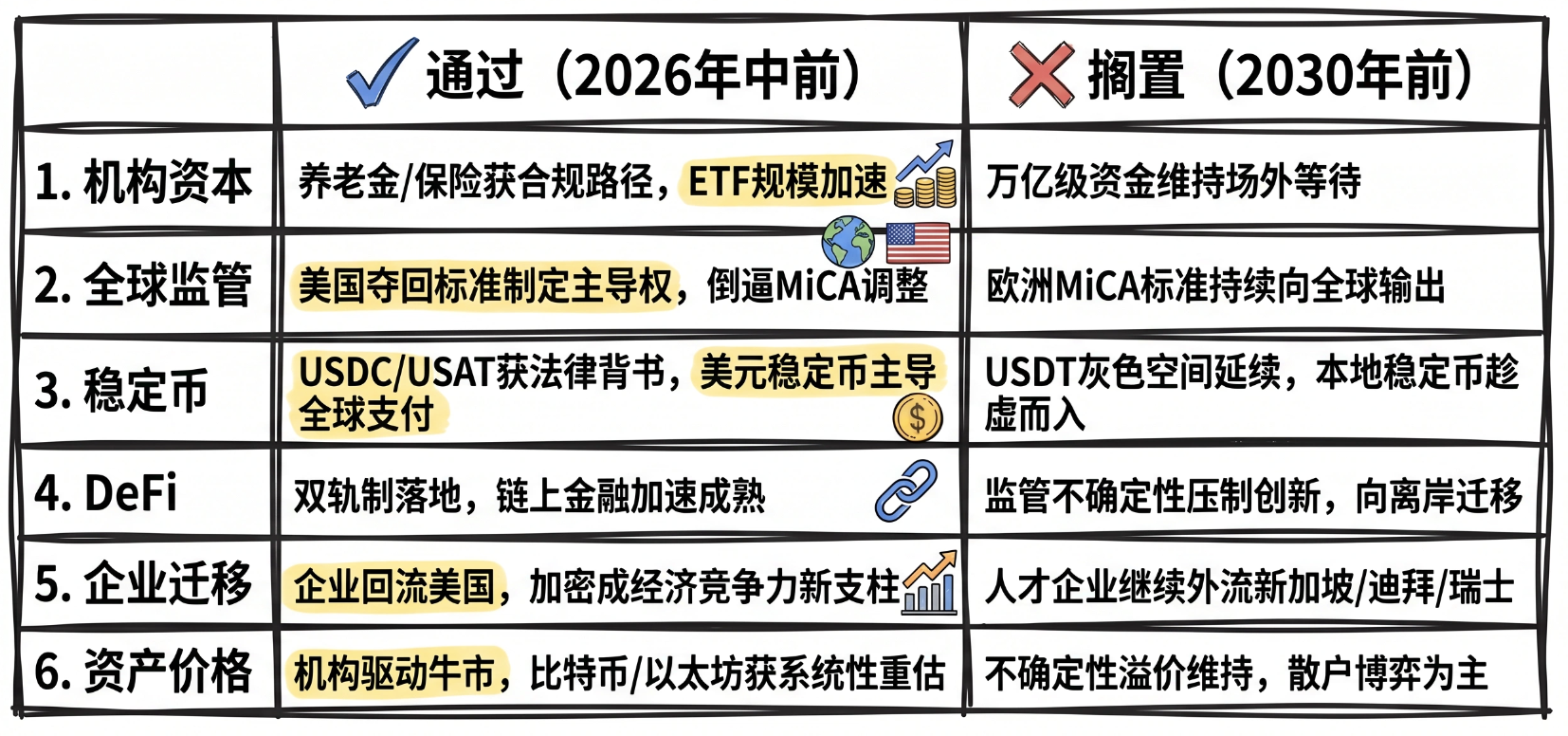

5.1 Passing vs. Shelving: Six-Dimensional Comparison Matrix

5.2 Competitive Landscape with Europe's MiCA

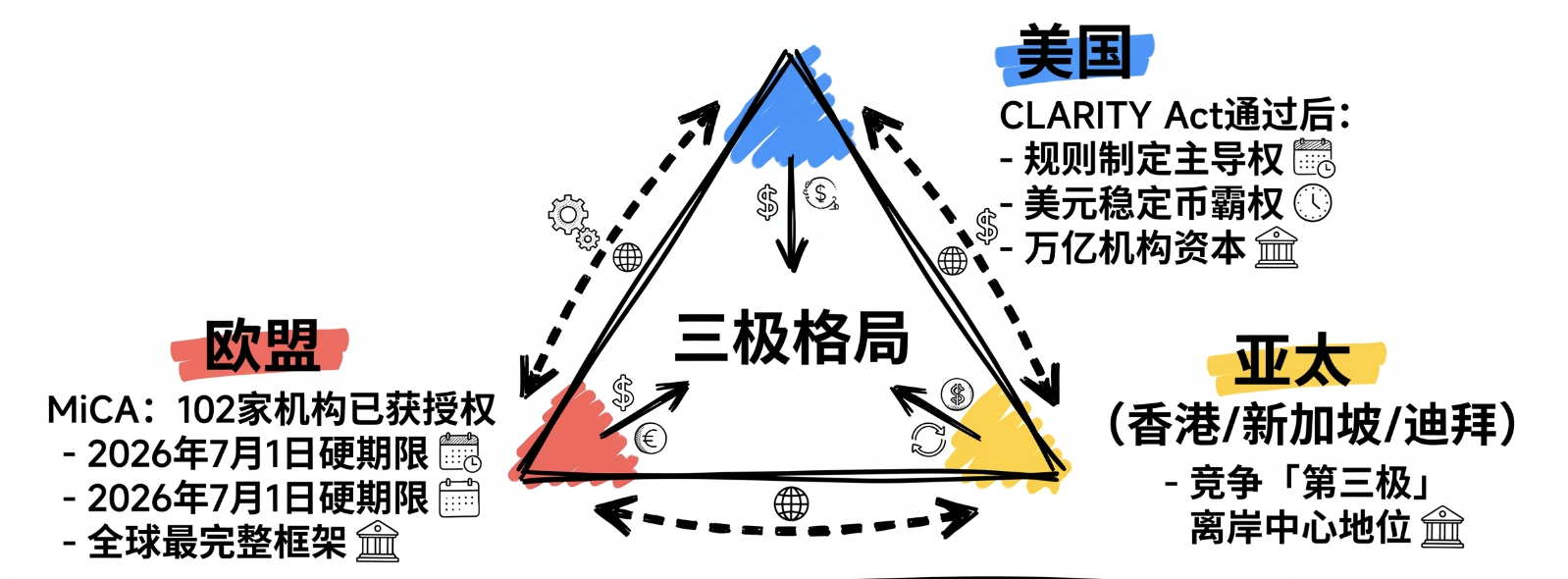

MiCA (EU Regulation on Markets in Crypto-Assets) fully came into effect in early 2025, with around 102 institutions authorized under MiCA, making it the most complete regulatory framework for cryptocurrencies globally. If the Clarity Act passes, pressure for regulatory alignment between the U.S. and Europe will increase, and bilateral regulatory recognition negotiations may commence, directly competing with the Euro stablecoin alliance (ING/UniCredit/BNP Paribas, expected to launch in the second half of 2026). If shelved, European MiCA standards will continue to be exported globally without the pressure of U.S. competition.

5.3 The Triangular Structure of Global Regulatory Competition

Global regulatory competition is forming a triad: the U.S. (post-passage of the Clarity Act), the EU (MiCA), and the Hong Kong/Singapore/Dubai competing as the "third pole" offshore center. Pakistan officially abolished an 8-year crypto banking ban on April 14, 2026; the UK's FCA simultaneously released a consultation document on crypto regulation, with the authorization window opening on September 30. In the absence of the U.S., the Asia-Pacific regulatory gap will continue to attract the outflow of businesses and talent.

5.4 The Direct Quantitative Impact of Institutional Capital Deployment

Galaxy Research estimates: if the bill does not complete committee review by April, the probability of passing in 2026 will plummet to a very low level. TradingKey analysis states: "The passage of the bill will unleash trillions in institutional capital"—conservative institutional investors like pensions and insurance companies will gain a clear compliance pathway. In 2025, Bitcoin ETFs had already accumulated over $115 billion in assets, signaling a potential for larger institutional allocations following the passage of the Clarity Act.

Conclusion: A New Order for Crypto After Regulatory Conclusion

2026 is a historic turning point for U.S. crypto regulation. Three main lines—the legislative conclusion of the Clarity Act, the restructuring of the stablecoin market by the Genius Act, and the generational leap in regulatory cognition represented by Warsh—point in the same direction: cryptocurrencies are being drawn from the gray area of regulation into the institutional core of the mainstream financial system.

The scarcity of the legislative window determines that this game has no second chance. Every participant in the quadripartite game—the crypto enterprises, the banking sector, regulatory agencies, and the Democratic camp—is searching for their path to maximize interests in this time-limited game, and the final compromise text will inevitably be a gray area that "none are completely satisfied with, but all can accept."

For market participants, there is only one core strategic judgment: regardless of the form in which the bill ultimately passes, compliance capability will become the most important competitive moat for the next five years. In a new crypto market dominated by institutional capital, those who complete the construction of compliance infrastructure in advance amid institutional uncertainty will inevitably be the pioneers able to cross regulatory cycles.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。