Original author: @Chandler_btc | Arkstream Capital

TL;DR

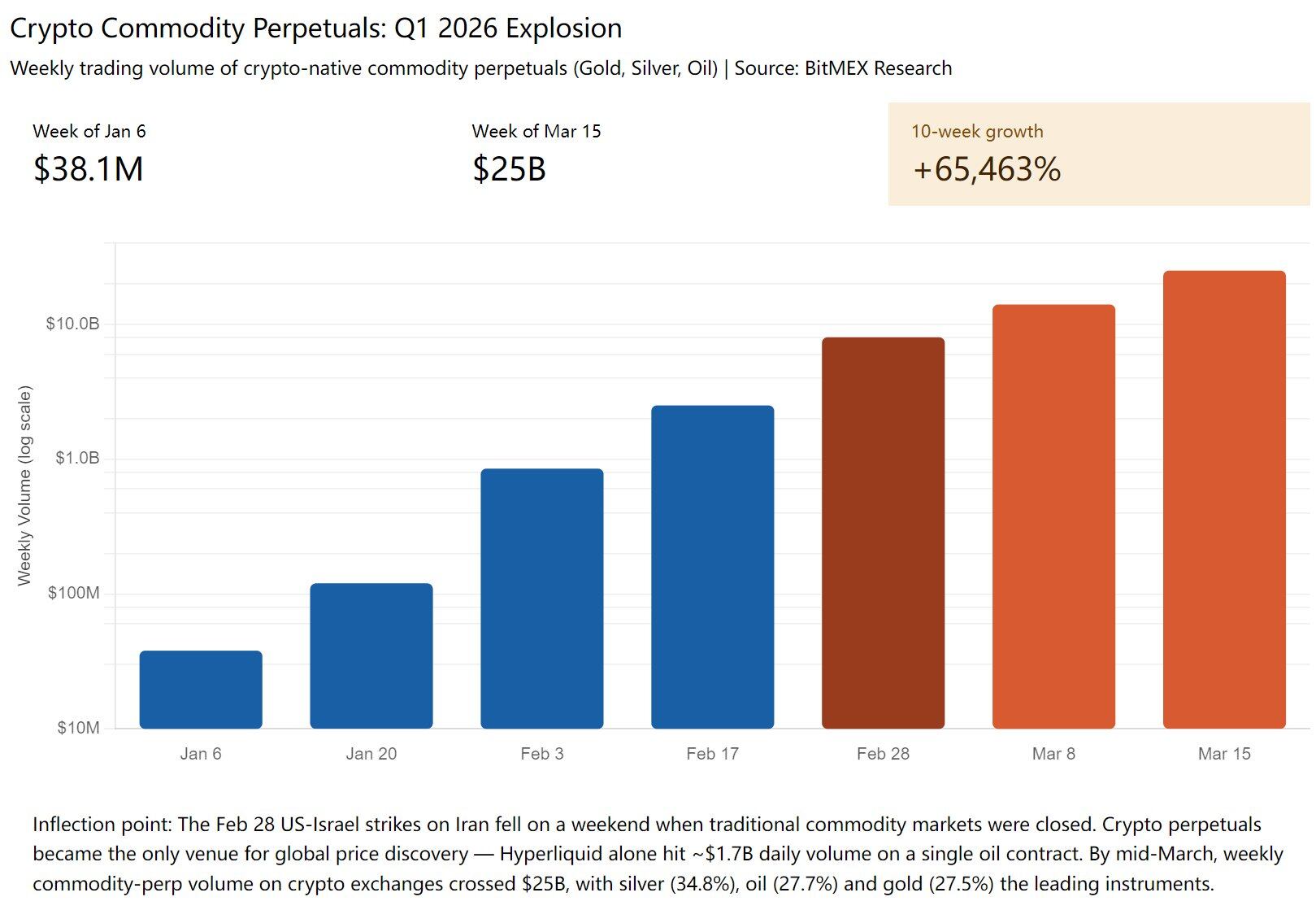

- In Q1 2026, the weekly trading volume of commodity perpetual contracts (gold, silver, crude oil) on cryptocurrency exchanges skyrocketed from $38.1M to $25B, an increase of 65,463%. The tokenization of traditional assets will be the main theme for Crypto in the next 5-10 years, and Pre-IPO tokenization is merely the latest entry in this trend.

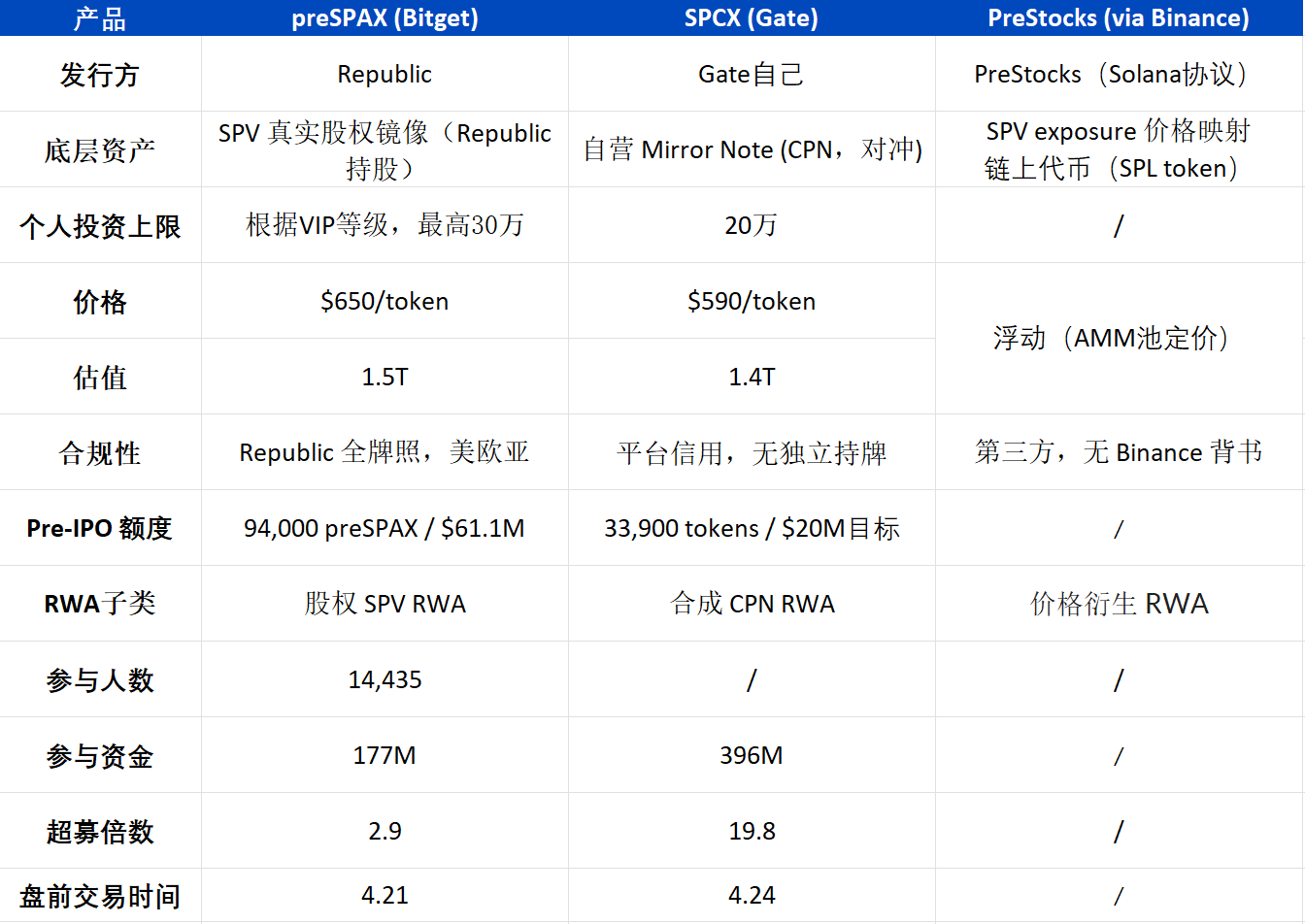

- In April, three leading exchanges, Bitget, Gate, and Binance (PreStocks), simultaneously launched tokenized products related to SpaceX. Although their compliance methods differ, the essence is the same: fragmenting the pre-IPO market share that previously catered only to ultra-high-net-worth clients and selling it to retail investors.

This article mainly clarifies two things: first, what traditional Pre-IPO really is, and second, how retail investors can participate.

The tokenization of traditional assets will be the main theme for Crypto in the next 5-10 years

According to statistics, in Q1 2026, the weekly trading volume of commodity perpetual contracts (gold, silver, crude oil) on cryptocurrency exchanges surged from $38.1M to $25B, an increase of 65,463%. After Binance launched its TradFi Perpetual segment in January, its cumulative trading volume exceeded $153B with over 114 million transactions in three months; its XAG (silver) contracts had an average daily trading volume of $1.31B, and its global market share skyrocketed from 0.2% to 4.9% (a 23.5-fold increase).

The most striking event was the war in Iran at the end of February, when the U.S. and Israel struck Iran over the weekend, and traditional futures, stocks, and forex markets were all closed, leaving only the crypto market open for trading. During that time, Hyperliquid's crude oil perpetual contracts skyrocketed by 5%, daily trading volume of Tether gold XAUT exceeded $300 million, and the CIO of Bitwise referred to it as "the weekend that changed finance."

U.S. stocks, precious metals, crude oil, and forex—assets that previously could only be traded from 9 to 4 on weekdays—are being tokenized and moved on-chain, providing 24/7 global liquidity. Pre-IPO tokenization is just the latest category to join this wave.

Source: BitMEX Research

What is Pre-IPO?

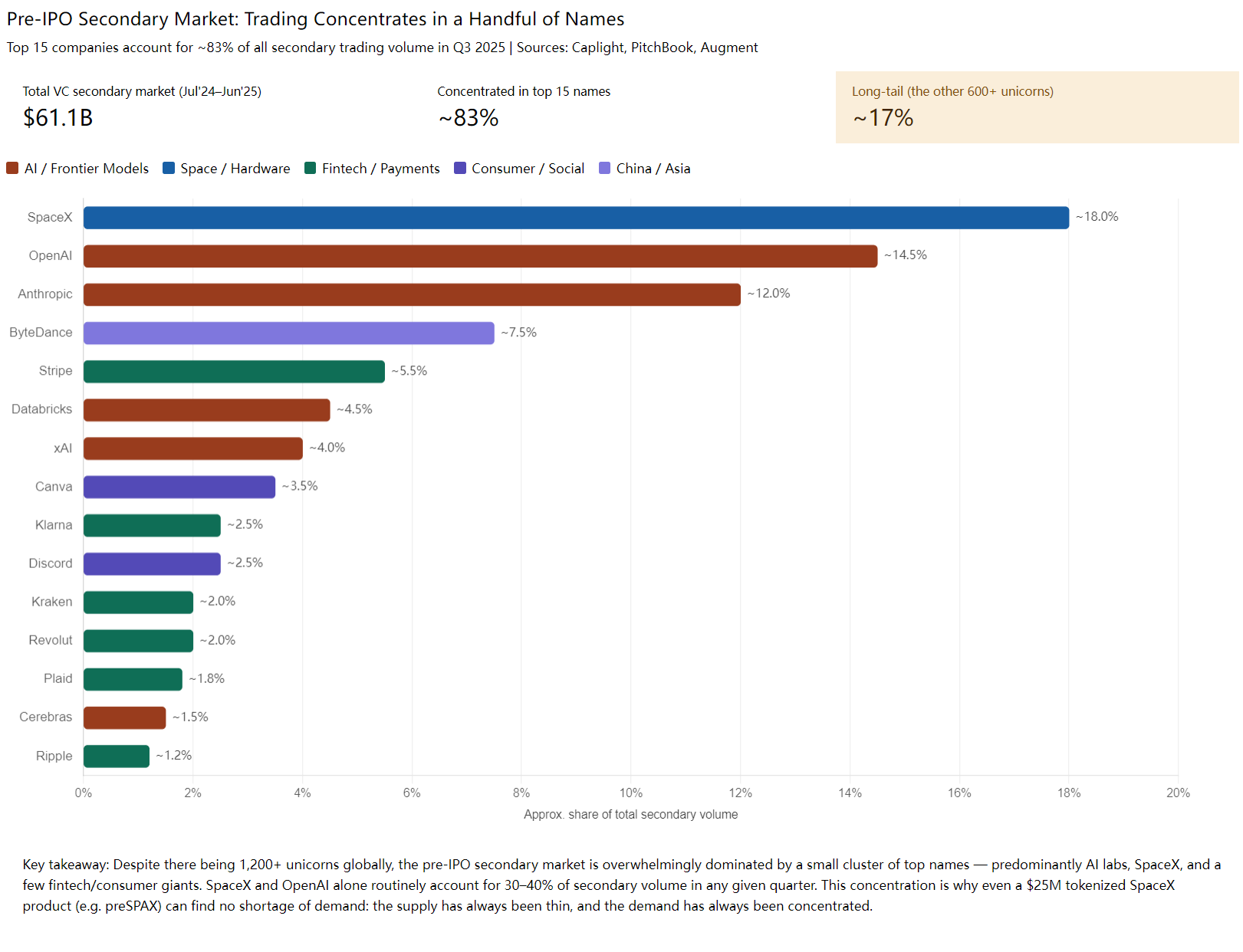

The Pre-IPO secondary market (old stock trading) has existed for over a decade, and in 2024, the global trading volume reached $160B, with the direct secondary market in the U.S. accounting for $61.1B. Buyers primarily include family offices, sovereign funds, institutional investors, and high-net-worth individuals, with single transactions usually starting at $10M, effectively keeping retail investors out.

The vast majority of transactions are conducted through SPV (Special Purpose Vehicle): original shareholders place their shares into a specially formed shell company, which then sells its shares to new buyers. Buyers receive shares of the SPV, holding an indirect interest in the underlying company shares. The reason is that old stock trades rarely allow strangers to directly join the cap table (company shareholder register), as this would trigger other shareholders' ROFR (Right of First Refusal), a complicated process that may be intercepted by original shareholders. Thus, buyers ultimately purchase the SPV's LP interest or Unit, which corresponds to holding indirect rights in the old stock.

Due to the high concentration of trading in a few top targets, giants like SpaceX, OpenAI, and Anthropic have long accounted for 30-40% of trading volume, while leading unicorns like ByteDance, Stripe, Databricks, and xAI make up 83% of transaction volume among the top 15 companies. (This concentration is also why even if Bitget/Gate only issued SpaceX tokens this time, they could easily raise over a hundred million, since the supply of leading Pre-IPOs has always been scarce, while demand is highly concentrated.)

Most of these targets are American, and the biggest regulatory obstacle is CFIUS (Committee on Foreign Investment in the United States). It restricts foreign investment in sensitive industries (AI, semiconductors, defense), and funds from certain countries buying SpaceX/Anthropic will face strict scrutiny. Therefore, before transactions, sellers usually stipulate that certain countries' UBOs are not allowed to purchase—GPs will penetrate the SPV to determine whether the ultimate controllers of the buyer are from restricted nationalities like China/Russia/Iran. The deeper the layers, the harder it is to verify, but it is not absolutely safe; we previously encountered a case where a Chinese UBO in a two-layer SPV was discovered, causing the entire deal to fall through.

Sources: Caplight PitchBook, Augment

After a U.S. company goes public, there is also a standard Lock-up Period: SEC Rule 144, in conjunction with underwriting agreements, stipulates that early shareholders and employees can only sell their shares on the public market six months after the company's IPO. This rule applies to almost all U.S. companies (Facebook, Coinbase, Reddit, Cerebras had a 6-month lock-up period). This is why Bitget/Gate’s Pre-IPO "tokens will not settle for 6 months," but it does not affect pre-market trading.

Sharing real trading details of Pre-IPO

The ticket size is extremely high

The traditional Pre-IPO ticket size typically starts at $10M, and transactions below $1M are rarely accepted—not because of lack of interest, but due to fixed costs (legal fees, KYC, SPV establishment, channel fees) that cannot be reduced. Therefore, the operations of exchanges in this round are a disruptive attempt that breaks down class barriers. In the past, retail investors (and they had to be sophisticated players, with conditions such as a U.S. stock account) could only participate after an IPO; now the exchanges, although a bit more expensive, at least provide ordinary people with the opportunity to participate.

Broker/FA Chaos

A cross-border Pre-IPO deal typically goes through multiple layers:

Bottom-layer GP - Rep (seller representative) - primary broker - secondary broker - … - FA - client

Each layer adds a 1-5% fee. A bottom-layer deal valued at $500B could end up costing over $600B by the time it reaches the real buyer.

Take SpaceX, for example, the real market price is about $1.25T plus a 3-11% access fee (varying across channels and levels), meaning the final price is nearly $1.375T, not including the compliance costs of Tokenization. Overall, the price given by the exchanges is fairly reasonable, likely designed to attract new users.

Furthermore, most block offers in the market are fictitious—shares from the same batch are listed multiple times by various brokers, and less than 10% are actually executable. For instance, SpaceX had a platform listing at a $1.2T valuation, but after deeper discussions, all were found to be fictitious listings. This situation is common even among large platforms and intermediaries.

Sources: An old stock trading platform

Sources: An old stock trading platform

If the transaction involves an LP Interest Swap, you also need to obtain GP Consent, which is the GP's approval for the transfer of LP shares in the underlying SPV. GPs have the right to refuse. The reality in the industry is that GPs are generally not welcoming of such transfers—because verifying new LPs, ensuring compliance, and introducing strangers are all troublesome, so in many cases, you need to bribe the GP to get things done, adding another layer of cost.

Poor liquidity is the biggest pain point for Pre-IPO old stocks

It's very difficult to exit midway; either you have to wait for the company's IPO (usually 3-7 years), and even after that, you must wait for an additional 6-month lock-up period, or search for new takers and go through the structured process again—two to three weeks (at the earliest) plus FA fees.

Every transfer is an independent OTC transaction, requiring the redoing of legal documents, KYC/AML/UBO penetration, GP approval. This is why Pre-IPO has always been priced as a "non-liquid asset."

How ordinary people can participate in this round of Pre-IPO

It can be predicted that a series of old stock tokenization products will emerge in the market, essentially all the same: platforms purchase real old stocks in the traditional Pre-IPO market, then fragment them into tokens to sell to retail investors.

For ordinary people, this provides an opportunity to enter before the company's IPO rounds, benefiting naturally from the rising valuations.

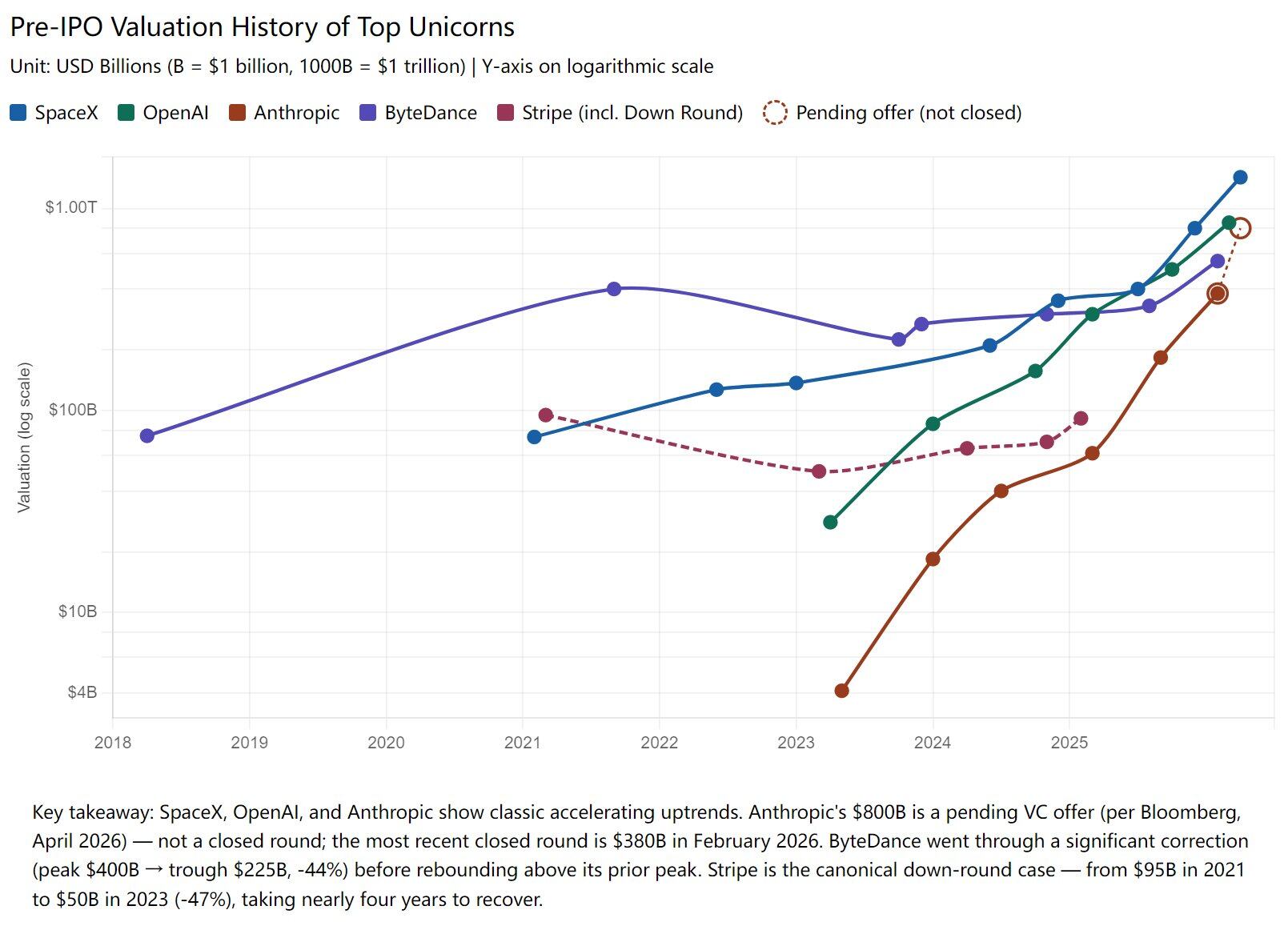

Top-quality targets typically see monotonous upward financing valuations. SpaceX has risen from $74B in 2021 to over $1.4T now, OpenAI from $29B to over $852B, Anthropic from $4B to over $800B, and Byte from $75B to over $600B. Every new financing round elevates valuations, and old shareholders rise accordingly.

But one must be clear: this is not a guaranteed win. Historically, Stripe experienced a valuation halving from $95B to $50B in a down round, TrueLayer dropped by 30%, Cybereason fell by 90%, and WeWork went bankrupt from a $49B valuation. In 2023, there were 128 unicorns globally that saw a decrease in valuation, with 42 dropping out of the unicorn category altogether.

Therefore, the key to participating in Pre-IPO is not to speculate on trends, but to select targets, following the natural appreciation of a company's valuation for long-term gains—not to rush and chase emotional trades for short-term fluctuations. Many Crypto users treat Pre-IPO like an IDO in the coin circle, which operates on entirely different logic.

To summarize the participation logic:

1. Do you have a long-term outlook on this target? Is SpaceX/OpenAI/Anthropic worth the post-IPO valuation level? Are you willing to hold until the next funding round or after the IPO?

2. Is this product safe? Who is the issuer? Where is the safety net? Who to pursue in case of issues?

Future forms of RWA in the next three years

The RWA of Pre-IPO is still in the very early stages, with supply of top targets being scarce, demand highly concentrated, and valuations on a long-term upward trend. In the coming months, tokenized products for leading targets such as OpenAI, Anthropic, xAI, Stripe, ByteDance, and Kimi will gradually emerge.

And this is just a small branch of the overall Tokenization; the main four-layer structure can be clearly anticipated:

- Stablecoin issuers: providing on-chain dollars and settlement gateways

- Public chain networks: carrying asset issuance and circulation

- Trading and distribution platforms: CEX, DEX. Additionally, we believe there is a potential player, LaunchPad / IDO platforms (such as Buidlpad, etc.), who already possess the full set of capabilities for new asset KYC, issuance, subscription, and distribution, which used to issue crypto tokens but can now fully issue Pre-IPO tokens

- Asset issuance service providers: companies that offer services for bringing various assets on-chain

It can be foreseen that this main line of Tokenization will not only give birth to a batch of unicorns, but also has the potential to nurture new trillion-dollar infrastructures, as well as a batch of billion-dollar platform players.

Everything has just begun.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。