Core Points

- This report is written by Tiger Research.The current USDC deposit rate on Aave V3 is 2.7%, lower than the 4.3% yield on the US 10-year Treasury bond. The short-term dividends brought by speculation in DeFi are fading.

- The market has not vanished. Although yields are generally declining, real-world assets (RWA) and stablecoins have grown into a multi-hundred billion dollar sector, and the industry is moving into a new development direction.

- The failures of projects like Compound, Curve, and Olympus reveal a profound lesson: models relying on tokens to support each other will collapse instantly once external incremental funds cease to flow.

- The past DeFi was like a power strip without an external power supply; RWA is now connecting this circuit to a real external value grid.

- The industry is maturing: using RWA as a value anchor while gradually establishing mechanisms for collaborative governance and responsibility constraints, initiatives like DeFi United exemplify this.

1. Yield Decline, Market Growth

Decentralized Finance (DeFi) is no longer a high-yield product.

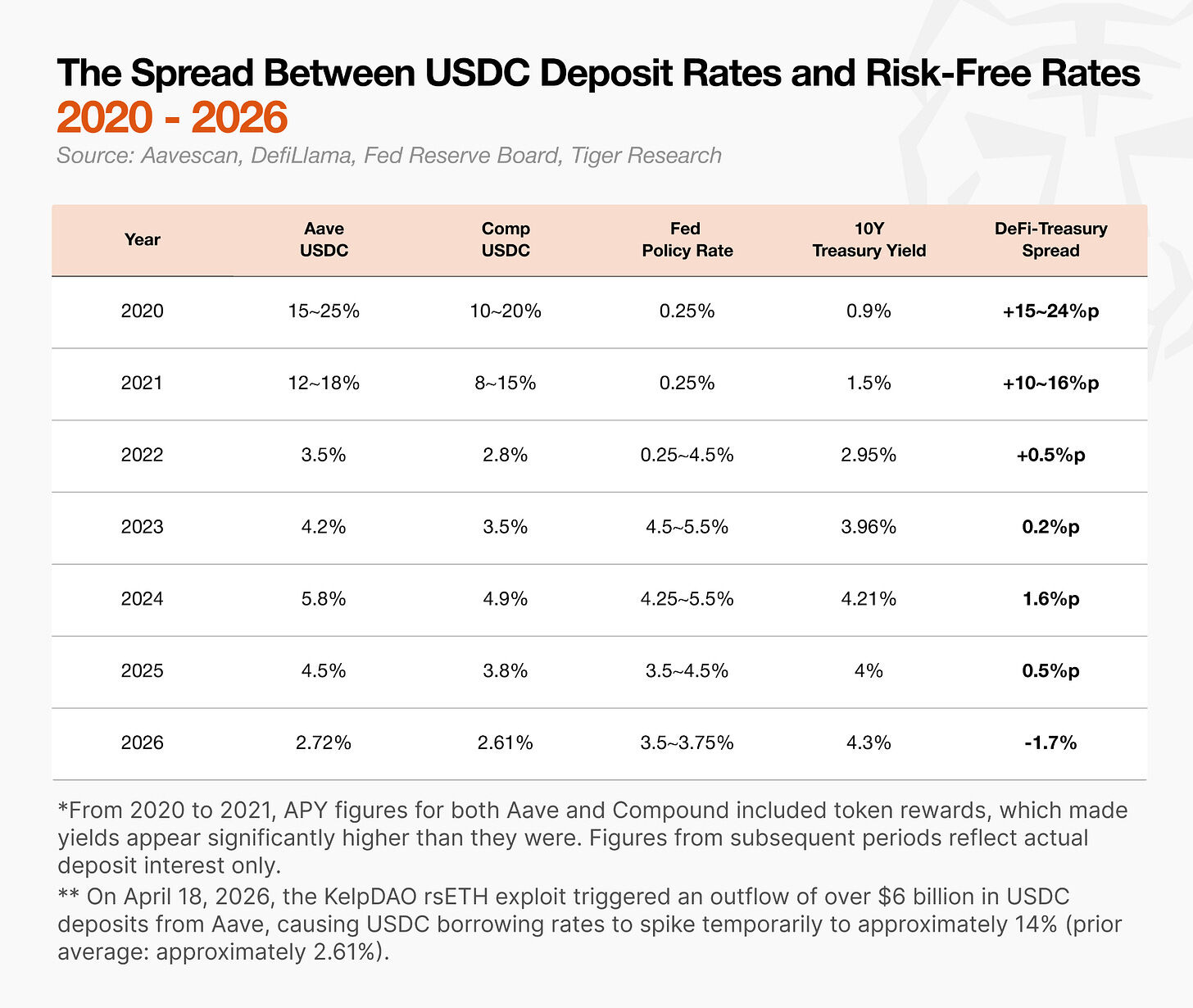

Since 2022, the spread between DeFi yields and Treasury yields has narrowed to nearly zero, with yield inversions occurring during certain periods. As of April 2026, Aave V3's USDC deposit rate is about 2.7%, lower than the US federal funds rate (3.5%) and the yield on the US 10-year Treasury bond (4.3%).

In the past, users accepted risks with clear reward logic.

At that time, on-chain yields were far higher than bank deposits, an undeniable advantage. But now the situation has reversed. If on-chain risks such as hacking attacks and stablecoin depegging are considered, the actual return on DeFi is even lower than traditional financial products, significantly weakening the incentive for ordinary retail investors to actively participate in DeFi.

However, the entire industry is continuously developing in a new direction. Native DeFi yields are declining, but ** real-world assets (RWA) ** are deeply integrating into traditional finance, with the scale reaching hundreds of billions of dollars. The entry of institutional capital is a key factor driving this shift.

However, institutions often overlook the development history and native community ecology of DeFi, blindly replicating the rules and paradigms of traditional finance. Before the large-scale entry of institutions, DeFi was a market driven by token incentives at its core. Numerous protocols relied on incentive mechanisms to gain market recognition, reshaping the operational logic of the entire industry. This model still profoundly influences DeFi today. The leading protocol Aave, born during the DeFi summer, has now become the benchmark interest rate standard for the entire DeFi industry.

For new institutional participants, deeply understanding the core players in the market that have persisted through cycles is a necessary foundational exercise before entering. This article will outline the key protocols that shape the core narrative of the industry during DeFi's complete development cycle and summarize the lessons learned from the market.

2. The History of DeFi Development: From Experimentation, Collapse to Rebuilding

DeFi was not initially built on the promise of token incentives. The starting point was quite simple: Can we autonomously complete asset lending, exchange, and collateralization on the blockchain without intermediaries?

In its early days, the industry leaned more towards a financial experiment. The core value lay in the model itself: lending without bank involvement, asset exchange without centralized exchanges, and any user holding collateral can autonomously provide liquidity. However, after 2020, the market direction changed rapidly, and token incentives began to become the core means to attract funds. A massive array of protocols and innovative ideas emerged, but ultimately only a few projects survived through the cycles. The industry learned lessons and continuously corrected its development direction through successive narrative changes.

Compound integrated its native token $COMP into a yield incentive system, successfully attracting liquidity on a large scale. But when similar projects began to replicate this strategy, the influx of new funds dried up, revealing the structural fragility of its model.

Curve transformed the governance voting mechanism into a battleground for yield distribution among liquidity pools, turning yield competition into a struggle for protocol control. The market thus realized: DeFi governance could also become a tool for power and incentive monopolization.

OlympusDAO was one of the most extreme cases. The project attempted to validate the feasibility of DeFi operating without external capital and autonomously controlling liquidity with extremely high annualized yields. However, most of its rewards did not come from real cash flows but were maintained through token issuance and new deposits. Once the flow of funds slowed, the price of the governance token OHM collapsed, and market confidence in the protocol completely disintegrated.

These three projects collectively sounded the alarm for the industry: If the core source of yield is the protocol's native token, this business model will ultimately be unsustainable. This past experience fundamentally reshaped the perceptions of ordinary users, development teams, and institutional capital toward DeFi.

It is precisely after this bubble burst that a new track arose: EigenLayer, Pendle, YBS, and RWA.

2.1. Compound: A Bubble Built on Token Distribution

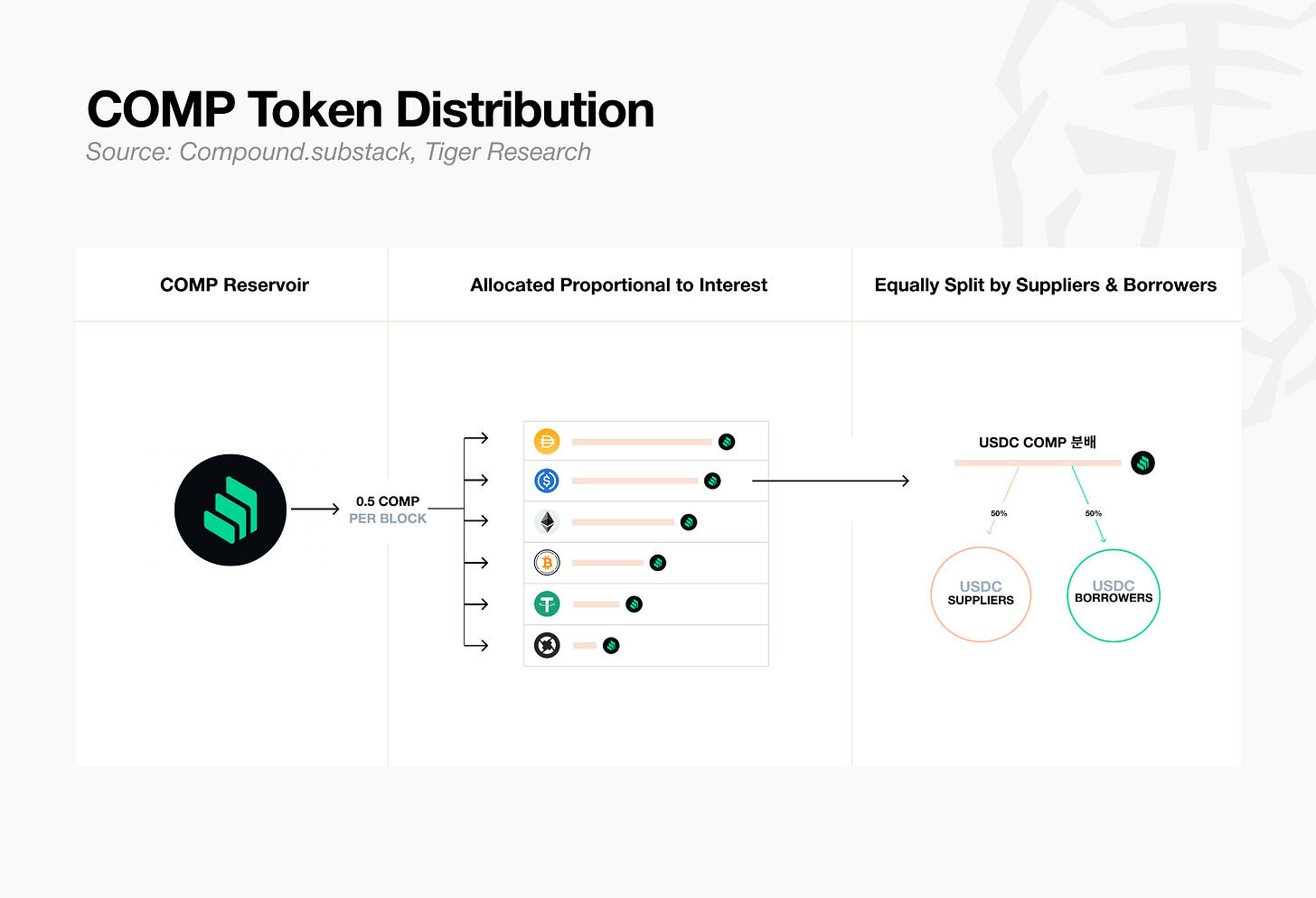

In June 2020, Compound began distributing governance tokens to users, incentivizing both depositors and borrowers with token rewards. At certain stages, COMP rewards even exceeded borrowing costs, creating a peculiar phenomenon where borrowing money became profitable.

This established a new industry paradigm. As users flooded in, Ethereum transaction fees soared, with single transfers costing dozens of dollars becoming normal. Depositing and borrowing transformed from mere financial operations into tools for mining rewards, with capital chasing high yields rapidly circulating between major protocols.

This period is what the industry refers to as the "DeFi Summer." Projects like Uniswap, Aave, and Yearn Finance rose one after another, establishing on-chain finance firmly and transforming it into an independent sector. However, the model ultimately built by Compound fundamentally relied on attracting funding through token incentives, subsequently increasing token prices due to the influx of funds, creating a positive feedback loop. The current behavior habits of DeFi users, highly sensitive to yield, liquidity, and reward mechanisms, gradually solidified during this phase.

2.2. Curve and veCRV: The Start of the Curve War

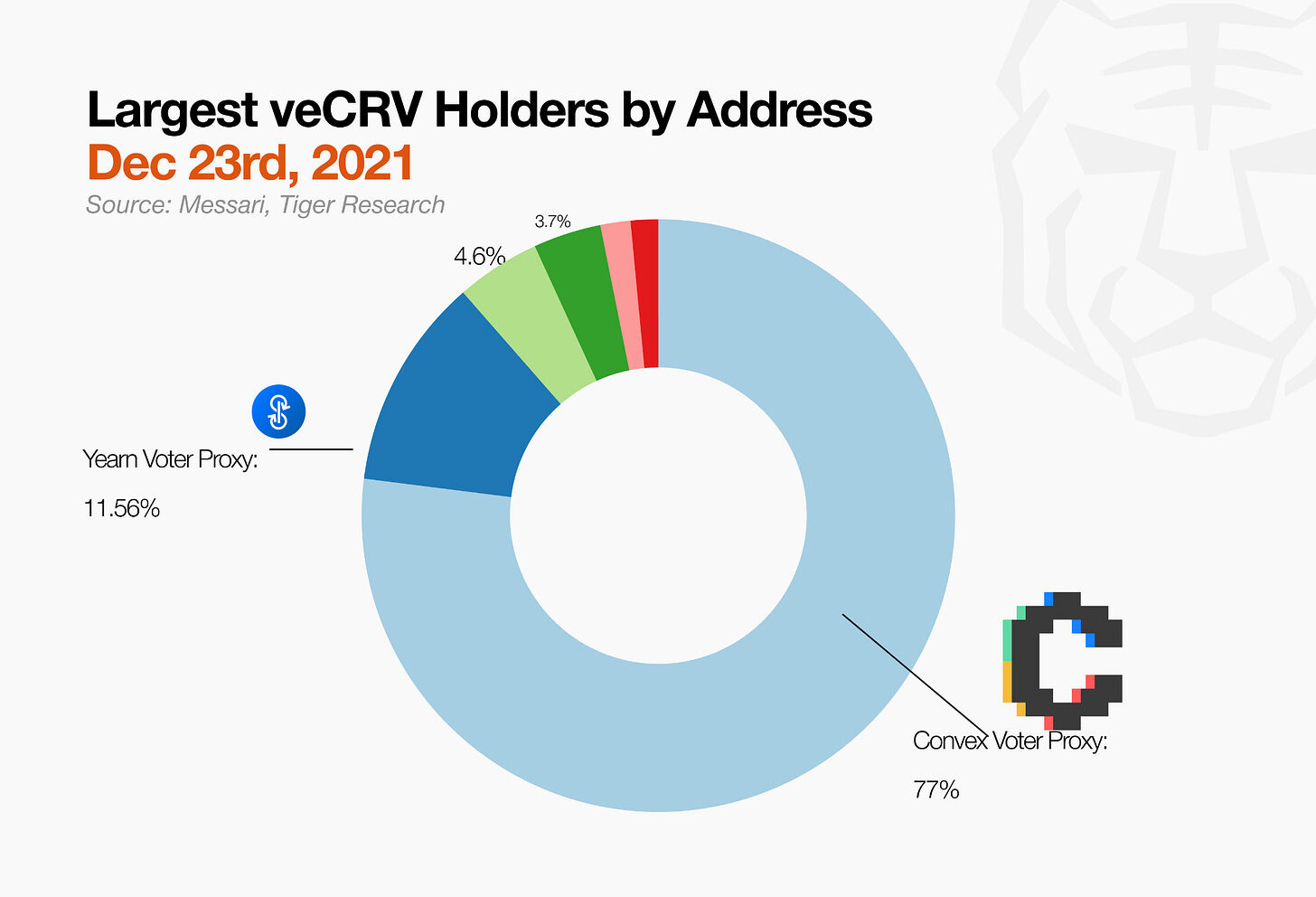

Curve initially was just a trading platform focused on stablecoin exchanges, but the introduction of veCRV completely rewrote its underlying logic. The longer users lock their CRV, the more veCRV they receive; veCRV represents weighted voting rights that can determine the distribution ratio of CRV rewards among various liquidity pools.

From then on, the core of industry competition was no longer the level of yield but the power to control yield distribution. Entities holding large amounts of veCRV could skew more token rewards toward their own pools. Major protocols began stockpiling veCRV, leading to fierce competition, thus initiating the Curve War.

Initially, this mechanism was attractive to both retail and project parties: the longer retail users locked up their assets, the higher their yields; project parties could reduce token circulation and direct liquidity to targeted pools. Because of this, similar locking governance models quickly became popular within the ecosystem, such as Balancer's veBAL and Frax's veFXS.

However, over time, governance power was no longer in the hands of ordinary users. Meta-protocols like Convex began to aggregate and lock CRV on behalf of users, concentrating veCRV voting rights in exchange for higher yield incentives. The Curve War escalated further, with the main battleground shifting to Convex.

Ultimately, veCRV validated a core conclusion: the power to control yield is much more attractive than yield itself. Users no longer held governance power directly but delegated it to more efficient intermediaries like Convex. Curve also made the market realize that DeFi governance rights themselves could become income-generating assets, and such power is prone to centralized monopolization.

2.3. OlympusDAO: The Golden Age Built on Game Theory

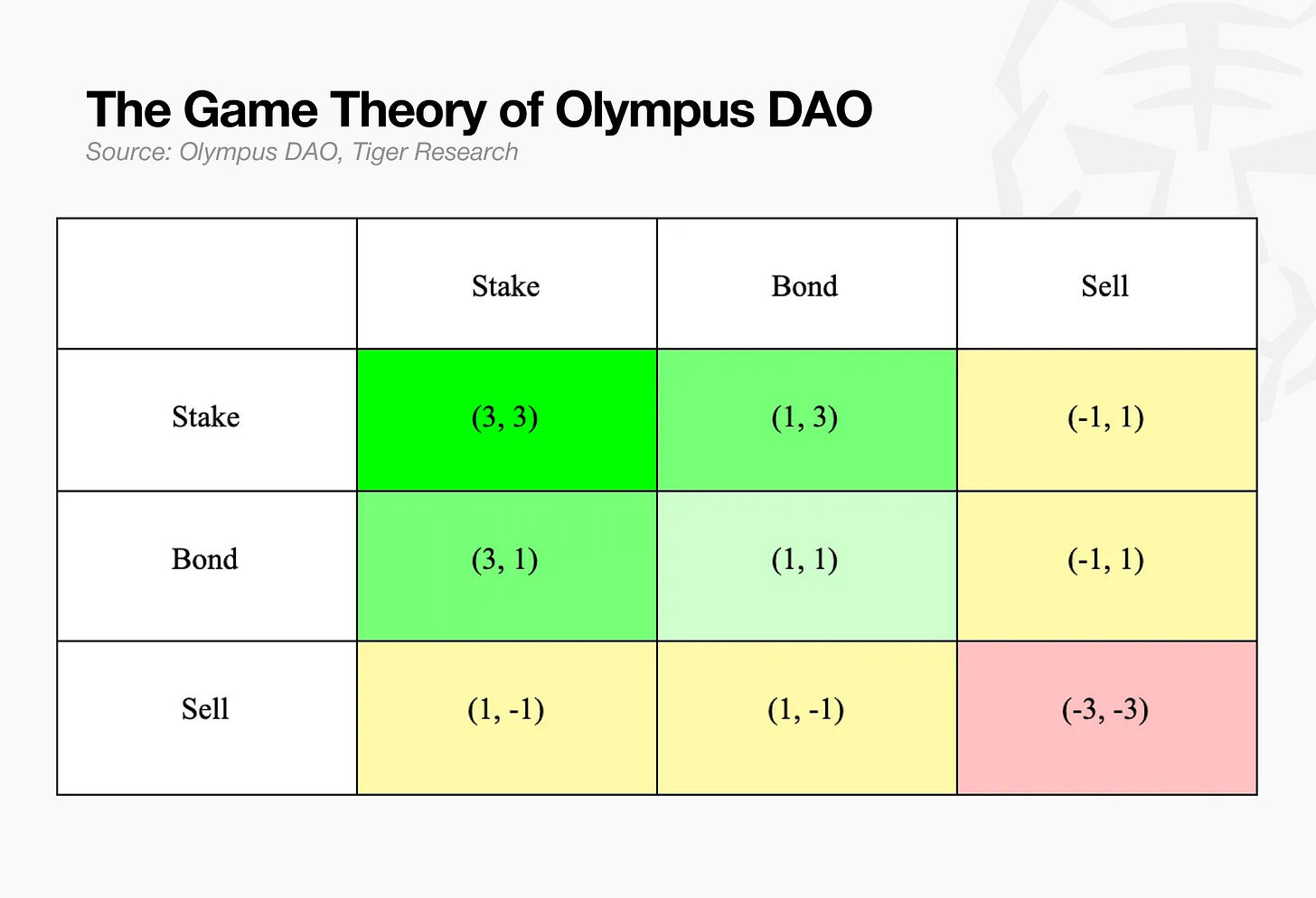

Even after the introduction of Curve's veToken mechanism, liquidity remained the biggest long-term challenge for DeFi. Injected liquidity would immediately withdraw if better incentives appeared elsewhere; this kind of capital essentially belongs to speculative capital.

OlympusDAO, born in the second half of 2021, gained significant attention as a potential solution to this problem. Its core design includes three main elements: protocol-owned liquidity (POL), where the protocol directly holds its own liquidity; a (3,3) game theory model advocating that all users choose to stake and lock tokens to achieve an optimal global result; and an initial extremely high annualized yield exceeding 200,000%.

However, this model ultimately proved unsustainable. OHM's yield heavily relied on the issuance of new tokens rather than real business cash flows. Its bond mechanism spawned many imitation forks, and OHM's price eventually plummeted over 90%. Following this event, the mindset of developers and users completely transformed: before pursuing "how high yields can be," people began to first scrutinize the real sources of those yields.

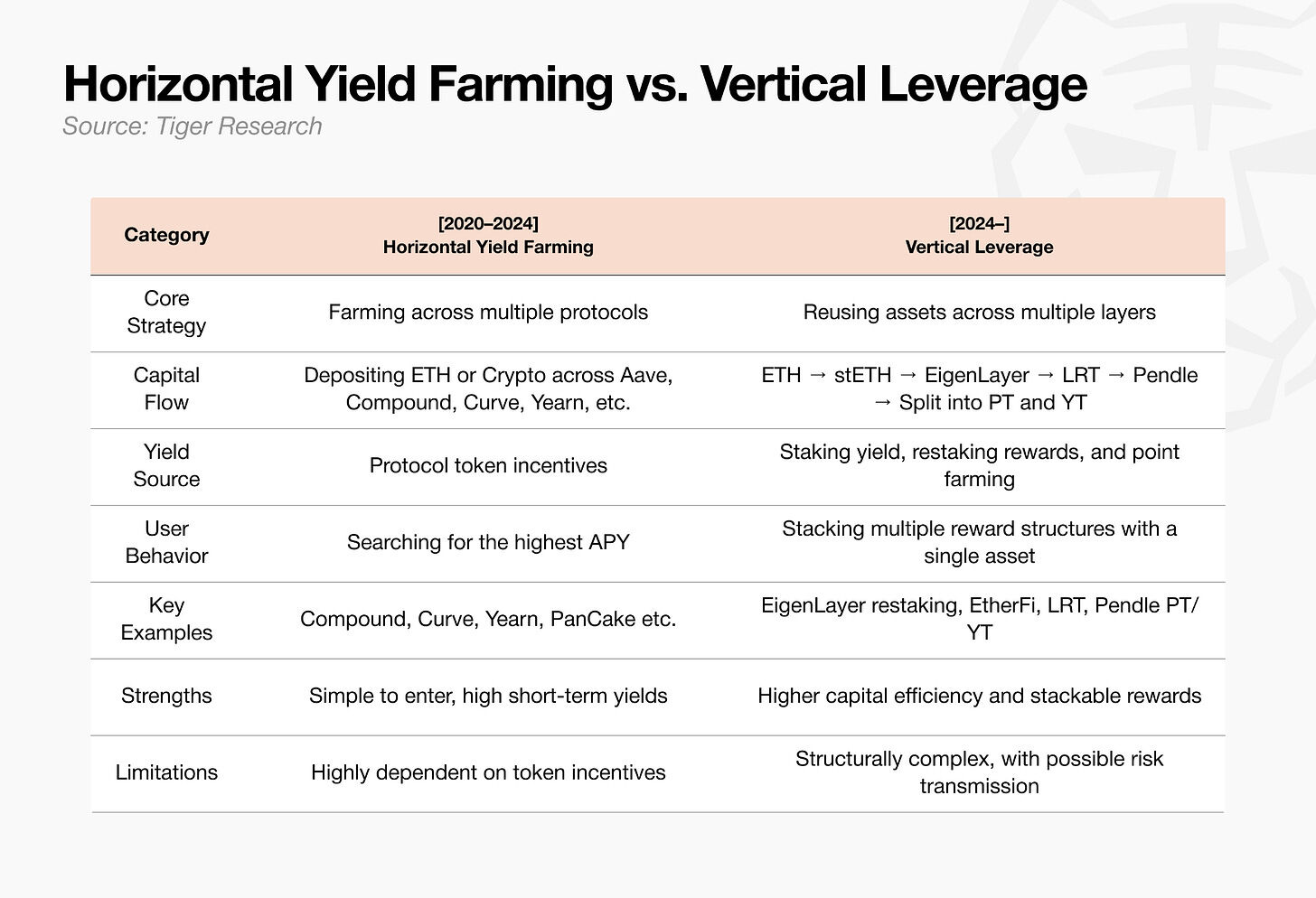

2.4. EigenLayer and Pendle: From Horizontal Yield Mining to Vertical Leverage

This collapse completely altered the behavior patterns of retail investors. From 2020 to 2022, the gameplay was simple and brutal: First mine incentives, then cash out. It became commonplace for the same user to spread funds across multiple protocols. Mining during that period was horizontal arbitrage: capital rapidly flowed between different protocols chasing higher annualized yields.

After 2022, this model's efficiency plummeted. Token incentive models were proven unsustainable, and airdrop competition became increasingly fierce. Simply diversifying deposits across multiple platforms resulted in diminishing marginal returns. The market direction shifted, and capital began seeking multi-layer yield stacking from single assets: re-staking Ethereum (stETH), reinvesting liquid staking derivatives (LRT) into DeFi, and splitting yield ownership to capture points and future potential returns.

EigenLayer and Pendle became the core representatives of this round of transformation. Starting in 2024, EigenLayer launched a re-staking framework that allows staked ETH and liquid staking assets (LST) to earn additional rewards. Within just about six months, its total value locked (TVL) surged from less than $400 million to $18.8 billion, clearly demonstrating: capital is transitioning massively from simple deposits to the re-staking track.

Pendle divides income-generating assets into Principal Tokens (PT) and Yield Tokens (YT). PT corresponds to principal equity that is almost capital-protected; YT encompasses all interest, mining rewards, and point entitlements during its term. Although yield tokens value to zero at maturity, they can maximize the capture of points and yields during the holding period. Even without understanding the underlying complex mechanisms, purchasing YT has evolved into a mainstream mining strategy that simultaneously utilizes time and capital leverage.

The industry strategy has thus been rewritten: from scattering capital everywhere and diversifying across multiple protocols, it has upgraded to focus on single targets with multi-layer yield stacking and compound interest.

3. Profit Model Restructuring: RWA and YBS

In the past, projects heavily relied on token incentives to increase total value locked (TVL). As the locking scale increased, the protocol appeared to expand, and the token price also rose. However, a core flaw remained: external liquidity comes and goes quickly, making it difficult to solidify.

Today, while TVL remains an important industry metric, the industry focus has completely shifted: fee revenues, backing by real assets, and compliance capabilities are now the key variables. The entry of institutional capital is crucial to this shift. Institutions will rigorously scrutinize the source of yields and the real quality of underlying collateral assets. A new generation of products is iterating and upgrading, aligning both retail needs and institutional compliance requirements.

3.1. Real-World Assets (RWA): Institutional Entry on a Large Scale

Since 2024, traditional financial institutions like BlackRock, Franklin Templeton, and JPMorgan have entered the on-chain market with real-world assets (RWA) as a starting point. Their operational models involve tokenizing off-chain tangible assets such as US Treasuries, money market funds, private credits, gold, and real estate, and issuing them on the blockchain.

The on-chain RWA market size has grown from several billion dollars in 2022 to several hundred billion dollars by April 2026. The tokenization of government bonds and private debts is the core driving force behind this recent growth.

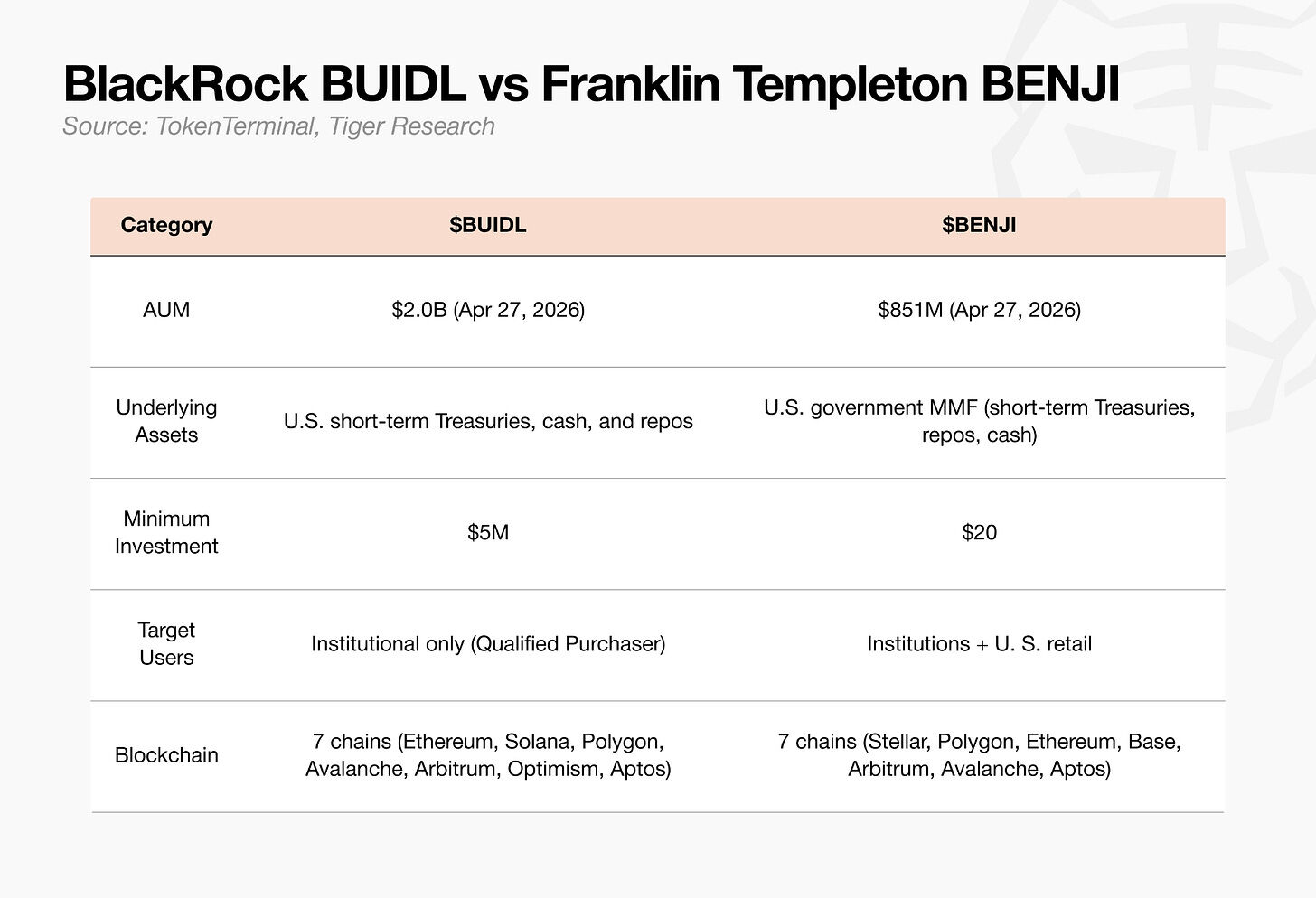

Currently, leading institutional products include BlackRock’s BUIDL and Franklin Templeton’s BENJI. Both product types have similar underlying asset categories but differ in operational models: BUIDL is strictly aimed at institutional investors, while BENJI has a minimum entry threshold of only $20, making it accessible to ordinary retail investors in the US.

In addition, asset management giants like Apollo, Hamilton Lane, and KKR are teaming up with on-chain issuance platforms like Securitize to accelerate the tokenization of private equity funds and private credit.

For traditional institutions, the on-chain market is not a completely unknown field but a new asset distribution channel. Therefore, various protocols serving institutional clients are working to improve supporting systems: building compliant customer identity verification (KYC) and anti-money laundering (AML) mechanisms, custody infrastructure, legal jurisdiction adaptability, and specialized risk management frameworks.

3.2. Yield-Generating Stablecoins (YBS): Dollar Assets with Built-In Yield Properties

The most noteworthy segment right now is yield-generating stablecoins (YBS). Yield-generating stablecoins are stablecoin products that directly embed a yield mechanism into the token itself. Ondo USDY, Sky sUSDS, Ethena sUSDe, and the previously mentioned BlackRock BUIDL and Franklin BENJI all belong to this category.

Users only need to hold these assets to automatically accumulate the income generated from the underlying asset. The underlying assets include US Treasuries, funding rate revenue, staking interest, and money market funds. The entire structure essentially equals a migration of traditional money market funds (MMF) to blockchain.

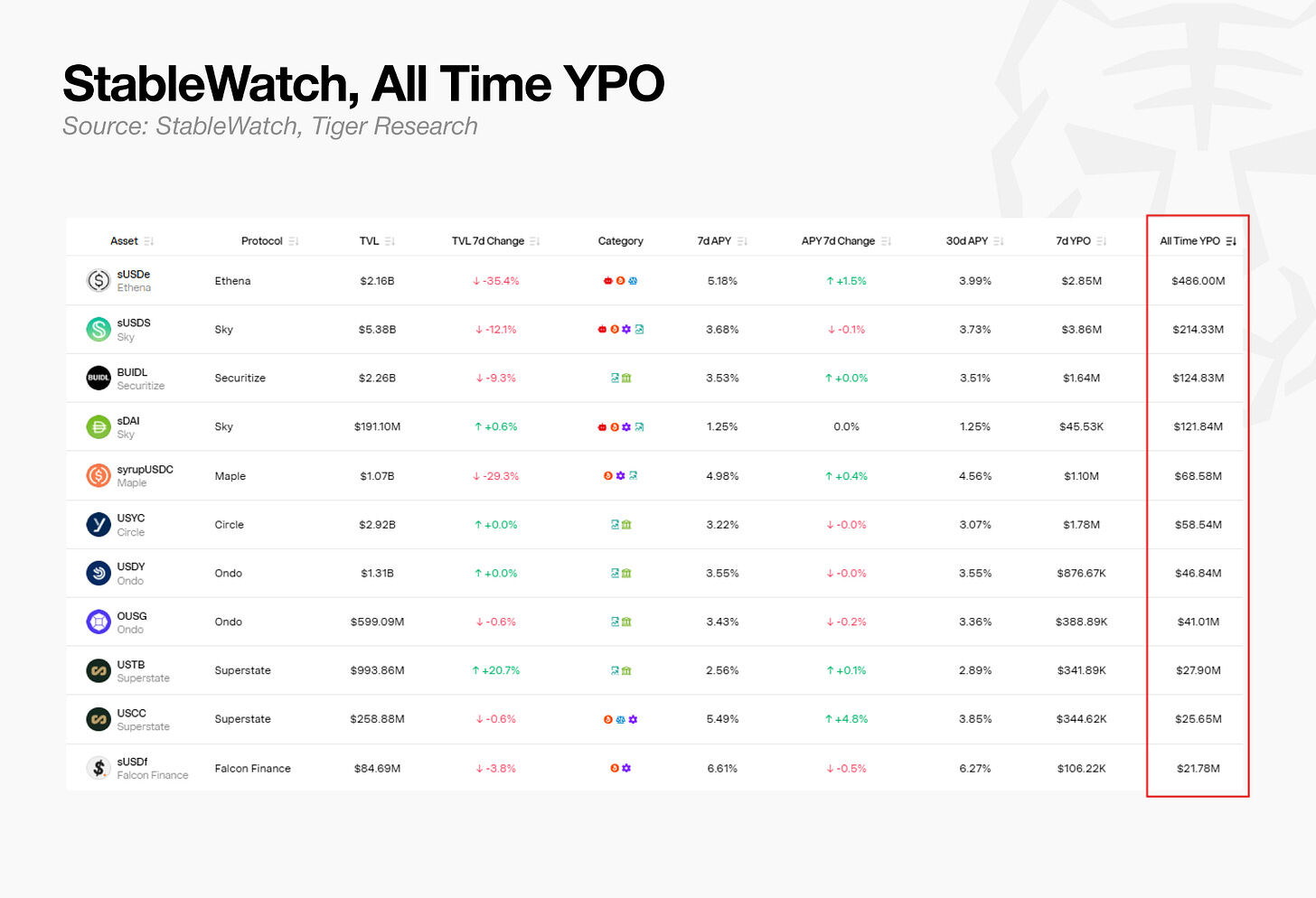

According to StableWatch's accumulated yield production (YPO) data, Ethena sUSDe, Sky sUSDS, BlackRock BUIDL, and Sky sDAI are the top products in terms of accumulated interest payment scale across the market. Although data may vary slightly under different statistical methodologies, it is undeniable: yield-generating stablecoins have already moved beyond niche experimental stages to grow into a mature sector capable of consistently distributing real interest.

Even so, merely moving money market funds to the blockchain does not constitute a core differentiation advantage. The real barrier lies in composability. BlackRock's BUIDL accounts for 90% of Ethena's dollar reserve asset USDtb margin, while USDtb can also be used as collateral in the Aave lending ecosystem.

In other words, foundational financial products, originally intended as RWA tools, have now transformed into stable underlying components of on-chain finance. DeFi no longer relies on limited "built-in batteries" to struggle for operation but has begun connecting to the external real value energy.

4. Building the RWA Value Grid: Learning from Historical Failures

Previously, DeFi was always doing one thing: sequentially linking and nesting power strip circuits, claiming them as growth flywheels.

Layer after layer of leverage and derivatives stacked up, creating a closed-loop. The fatal flaw is that the energy originates externally from the future, and most revenues are artificially created from protocol-native token incentives. Compound relied on its native tokens to back loans, while Curve used its tokens to retain liquidity providers.

On the surface, all parties provided mutual support, circulating continuously, but in reality, the entire system shared a limited shared battery. Once the market faced shocks, the underlying value collapsed first, transmitting up through the layers, causing the derivative products at the end to halt and fail first. This self-closed, self-backed model has a natural ceiling on carrying capacity.

RWA integrates real external value grids into this system for the first time. Bond interests, rent from properties, receivables from trade, and other cash flows from the real economy become stable power sources supporting on-chain finance. Interest rates are no longer artificially manipulated by internal token incentives but are determined collectively by external market supply and demand, macro interest rates, and credit risks.

As stable cash flows continue to circulate, various financial modules such as issuance, custody, collateralization, lending, and settlement can layer upon this grid. Many complex financial products that were challenging to implement in traditional DeFi are now feasible solutions relying on RWA's underlying architecture. The core proposition of the industry is no longer to endlessly stack power strips and pile on layers but to find ways to acquire long-term stable value currents.

This is precisely the core essence of on-chain RWA: bringing assets with real underlying value onto the blockchain and layering various financial business modules on top of the continuous cash flow they generate. If traditional DeFi relied on token incentives as a temporary battery to borrow liquidity for survival, then today’s RWA track is achieving long-term liquidity sedimentation through the inherent cash flows of the assets themselves.

Today, leading players in the track are starting from their respective fields to collaboratively build this new financial grid:

- Theo is responsible for filtering which underlying assets can be put on-chain and determining which tangible assets to connect, acting as the energy source for the entire grid.

- Plume builds the foundational infrastructure for asset issuance and circulation, laying power transmission lines and scheduling hubs to ensure smooth value transfer.

- Morpho builds the lending and collateral markets using circulated tangible assets as collateral, becoming one of the first real financial terminals to consume and utilize value on this new grid.

No single institution can monopolize the entire grid. This new financial loop called on-chain RWA is only complete when the energy source, transmission network, and application terminals are interconnected.

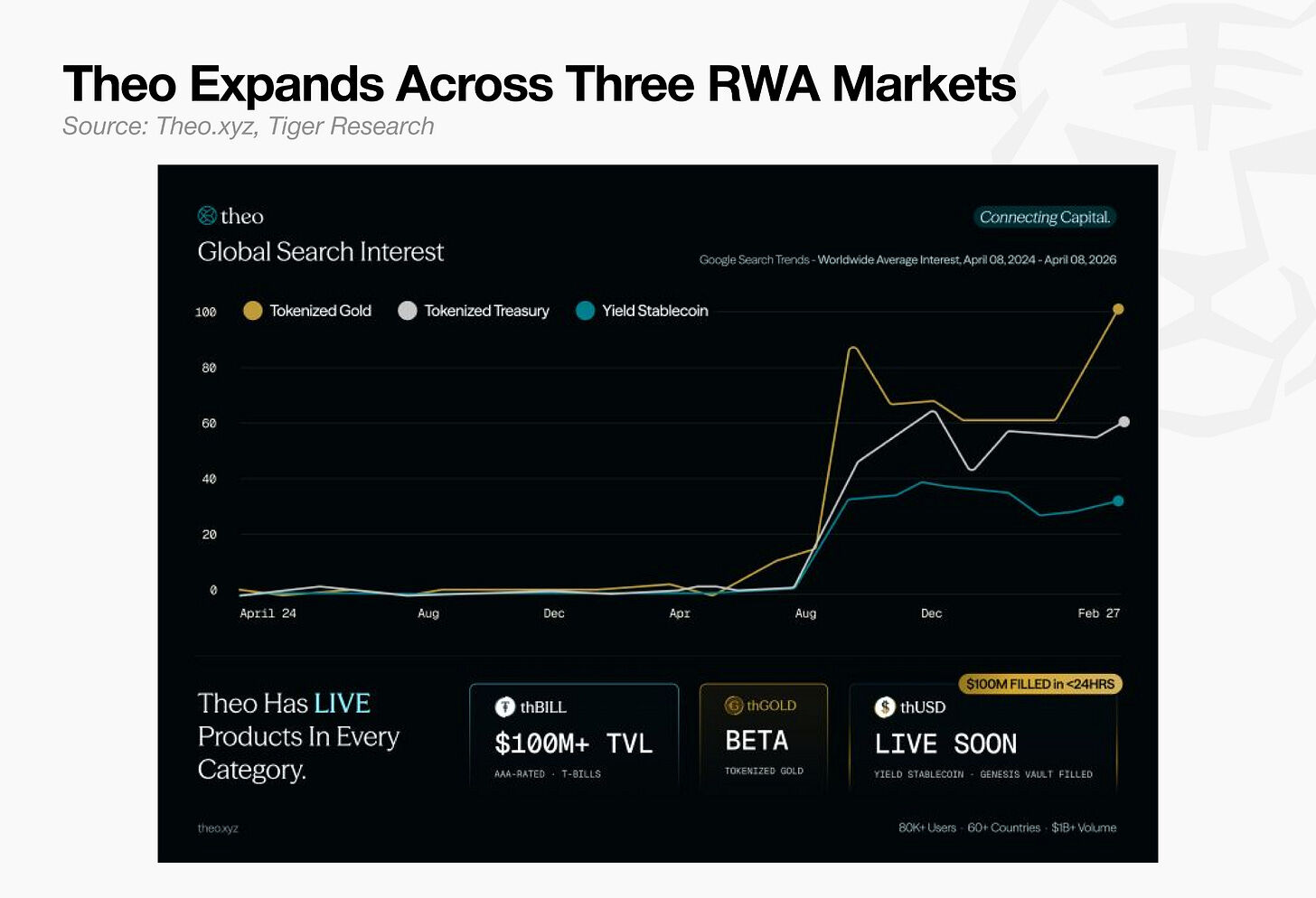

4.1. Theo: A Case of User Group Strategic Restructuring

Theo is a typical example: starting from filtering underlying assets, it has completely reshaped its customer base and undergone a full transformation.

Theo’s flagship product was initially a strategy vault. However, as the market landscape changed, the needs of retail and institutional investors began to diverge significantly. Theo proactively adapted to industry trends, repositions its target customer groups comprehensively.

The current core product is thBILL. This product consists of a tokenized portfolio of US short-term government bonds provided by a compliant issuer, serving as the core underlying asset of the Theo ecosystem, continuously generating stable returns. The project roadmap has added thGOLD (tokenized gold), and the yield-generating stablecoin thUSD, issued against thGOLD as collateral, is about to go live.

This transformation is not just an iteration of products but also confirms one point: projects originating from retail incentive tracks can completely reconstruct their underlying architecture to fit and connect with institutional compliance and business requirements.

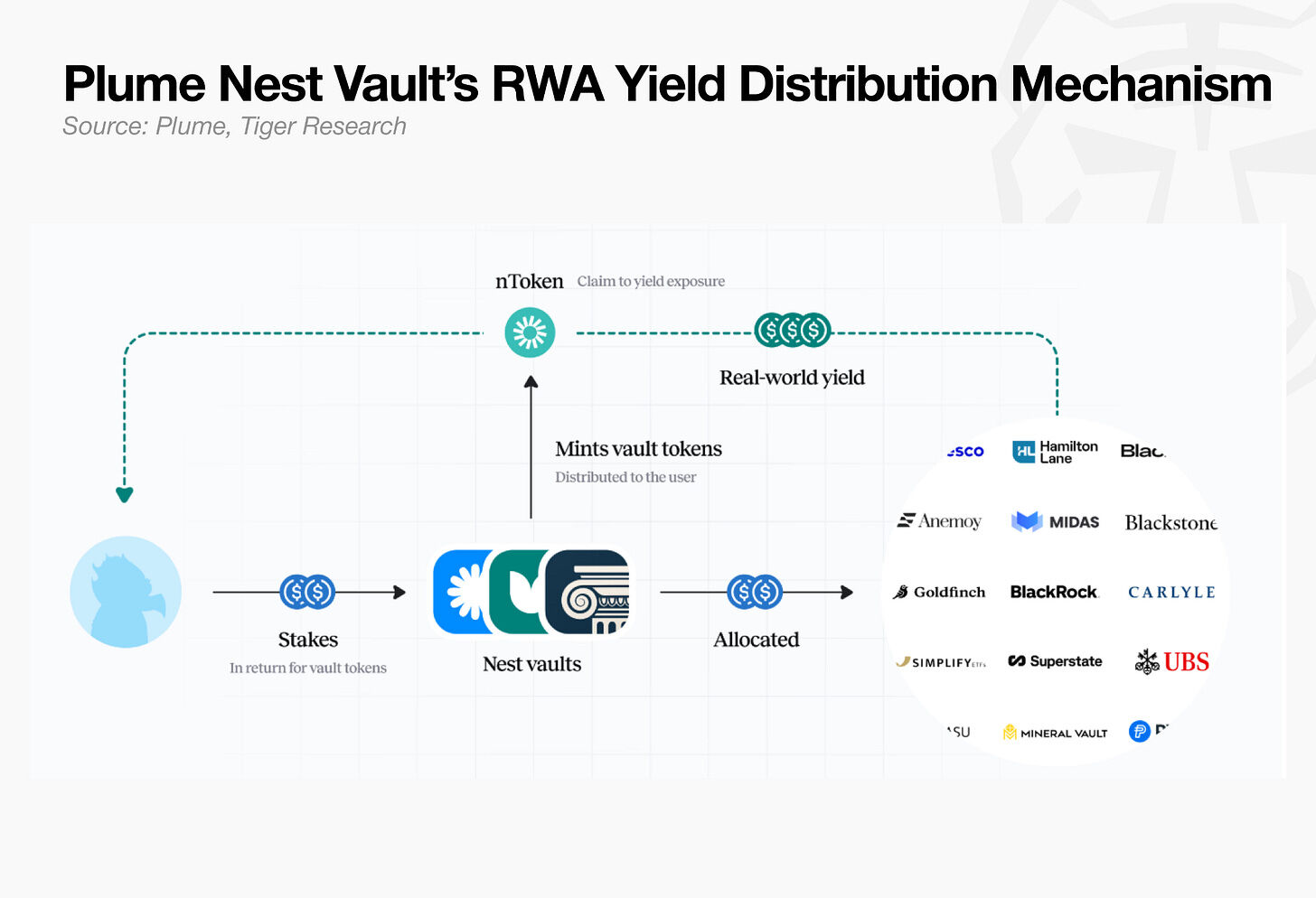

4.2. Plume: Building the Underlying Ecology for RWA Implementation

Plume is another typical example, integrating essential infrastructure for asset circulation with upper-level market demand in a deep and unified construction.

For institutions, simply chaining assets is far from enough; they also need comprehensive infrastructure covering issuance, compliance, distribution, and yield productization. On the other hand, for on-chain users, wanting to invest in government bonds, funds, and other institutional-grade assets also requires a well-developed product system to support it.

Nest is a yield protocol built on Plume's underlying infrastructure. Users can easily earn yields generated by institutional-level real-world assets (RWA) by depositing stablecoins. The various vault products it offers, including nBASIS, nTBILL, and nWisdom, each rely on different tangible assets as their yield foundations; vault tokens can be freely transferred and circulated within the DeFi ecosystem.

WisdomTree has issued 14 tokenized funds on Plume, and Apollo Global Management has launched a $50 million credit strategy, while Invesco has migrated a $6.3 billion senior loan strategy to Plume’s on-chain environment. Nest has become the central entry point for ordinary users to connect with such institutional assets.

In addition to its ecosystem links, Plume is also a set of comprehensive integrated infrastructure, building a standardized distribution channel between institutional assets and on-chain capital needs.

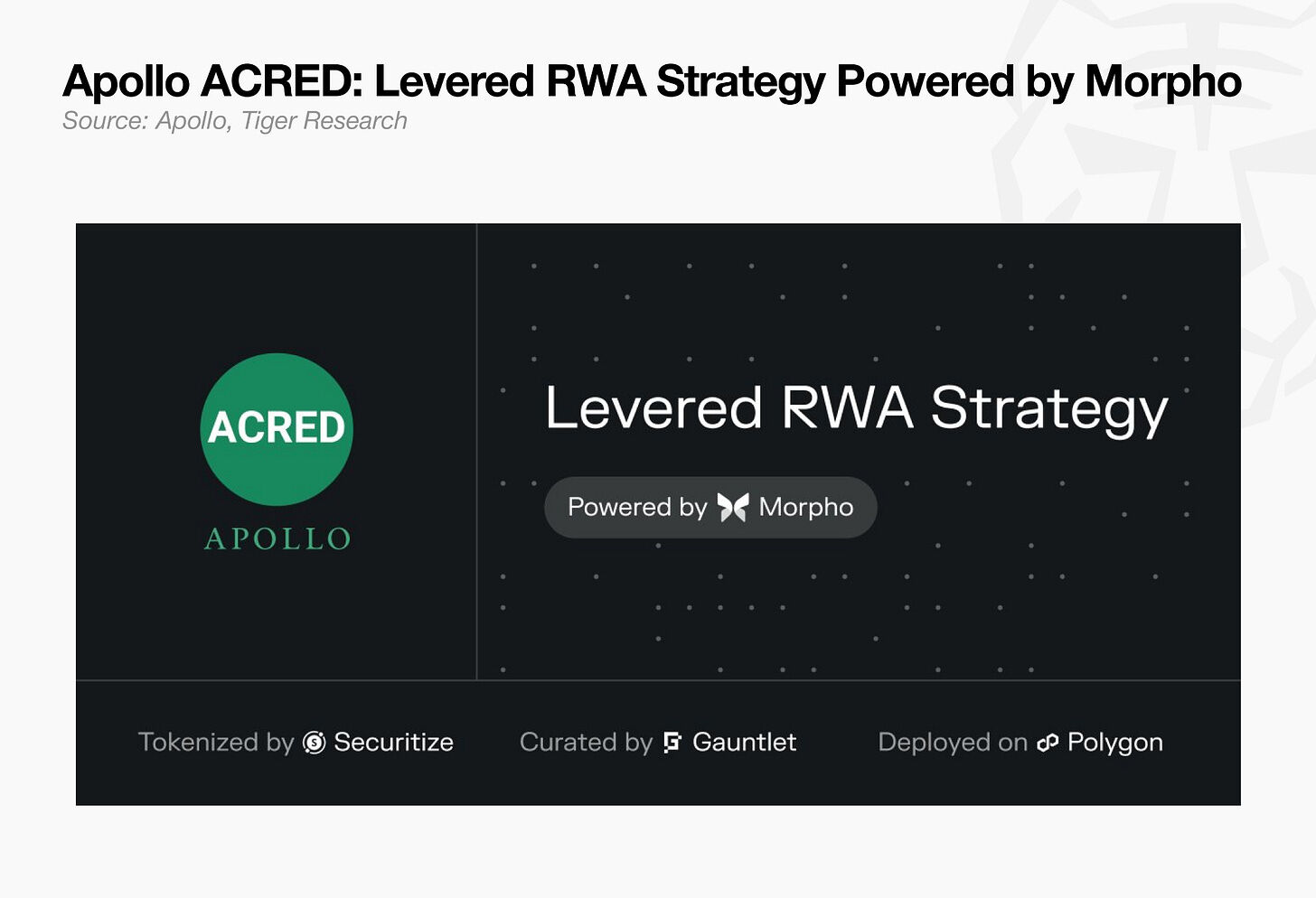

4.3. Morpho: Adding Complete Financial Functions to Institutional Assets

Morpho serves as the third typical case, illustrating how to transform assets into collateral, borrowing tools, and liquidity sources.

For institutions, registering assets on-chain is only the starting point; the crucial question is: can these assets serve as collateral and release liquidity accordingly? Loan terms and risk parameters must be clearly defined, and all business operations must be legally conducted within custody and compliance frameworks.

A typical example is Apollo's ACRED product. Apollo deploys its credit strategy on Plume and allows ACRED to be used as collateral in Morpho, enabling holders to borrow stablecoins while retaining their fund holdings. ACRED is a tokenized private credit fund structured around Apollo's diversified securitized credit fund, issued on-chain by Securitize.

Only when institutional assets can serve as collateral, support lending, and release liquidity, can they genuinely become usable raw materials for on-chain finance.

5. What Remains After the Dopamine Rush Fades

Looking back, the golden age of DeFi resembles a mirage built upon token incentives and leverage stacking.

Although some voices in the industry continue to predict a bleak recovery for DeFi, citing frequent hacking incidents.

However, the recent handling of the Kelp DAO rsETH incident and the establishment of the DeFi United alliance present a starkly contrasting trend in the industry. As of April 28, 2026, Aave and DeFi United have successfully raised over $300 million, far exceeding the $190 million in losses from this hacking.

This strongly indicates that the industry is gradually building trust infrastructures, and a more mature collective accountability mechanism has already begun to germinate.

Throughout the history of DeFi development, it can be seen that the early industry was in a state of complete disorder with no accountability. Users' sole objective was to rapidly seize high-yield tokens; project teams often designed various high-yield mechanisms that would see them withdraw after achieving their fundraising targets.

Now the industry is undergoing a complete turn: institutional accountability is being proactively written into system designs. A complete and mature financial system has yet to take shape, but it is certain that a consensus has been reached within the industry: confronting common risks, fairly sharing losses, and clarifying responsibilities.

Many skeptics point to market vulnerabilities, not only due to frequent security breaches but also due to the complete disappearance of short-term high yields and the lack of new narratives or growth catalysts.

The influence of the vague concept of “DeFi” is continuing to weaken. The market has segmented into more precise vertical tracks: lending, stablecoins, real-world assets (RWA), re-staking, and on-chain credit, etc.

The names of concepts are no longer significant. Early innovations and experiments originating from DeFi are steadily maturing and evolving into sustainable foundational architectures, enabling more assets to authentically enter the real economy and generate actual value.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。