Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: Long-term bonds in developed countries are collectively failing, and the market is no longer re-pricing the fiscal surprises of any single country, but rather the reality of high debt, high deficits, and even higher interest rates coexisting in the long term. As debt growth continues to outpace economic growth, energy shocks reignite inflation, and the central bank's room for interest rate cuts is constrained, the "low interest rate rolling model" that has supported financing for developed countries over the past decade is showing cracks.

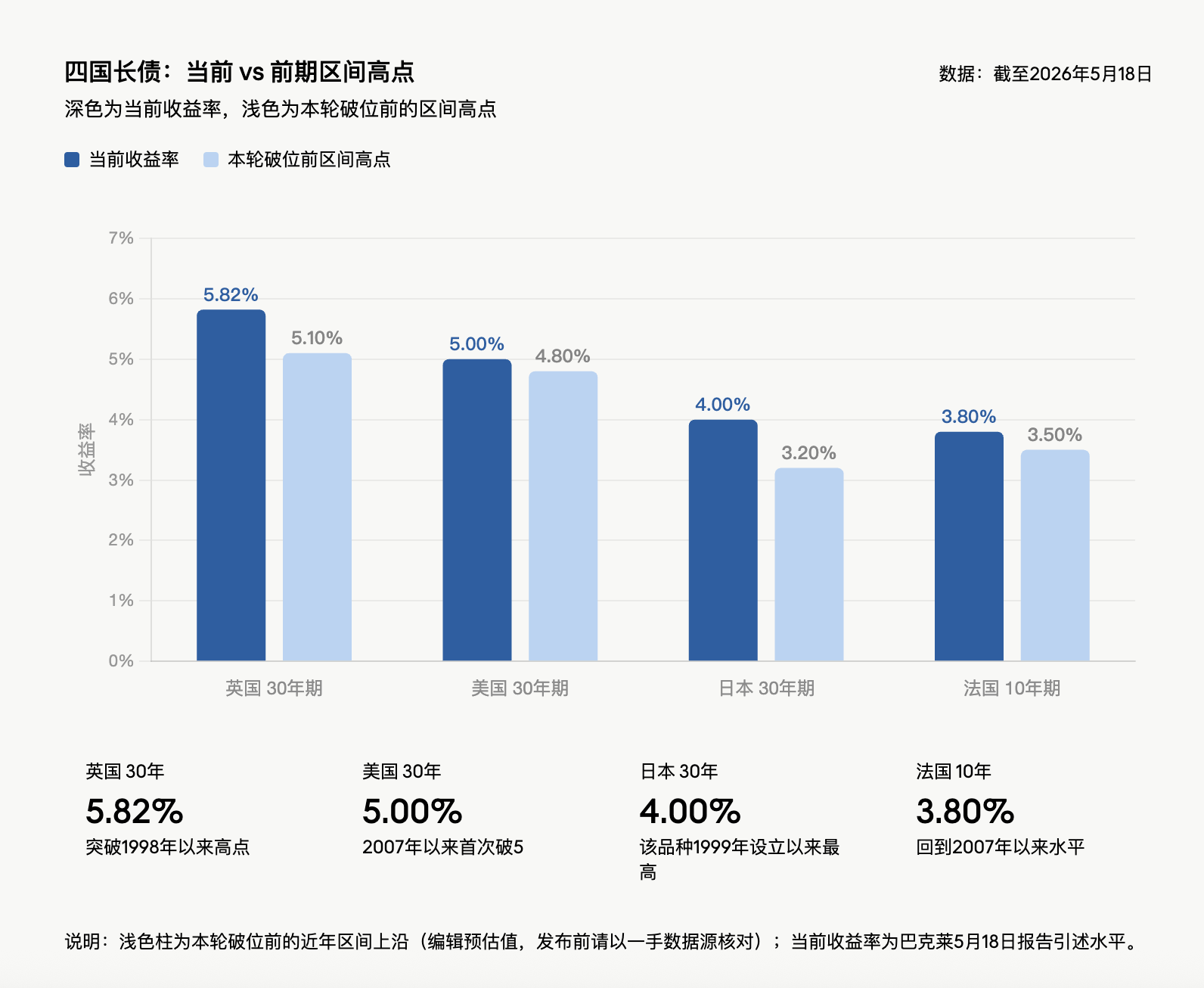

In the past week, the yield on UK 30-year government bonds rose to 5.82%, the highest since 1998; Japan's 30-year government bond yield hit 4%, the highest since the inception of this category in 1999; the US 30-year government bond yield surpassed 5% for the first time since 2007; and the yield on French 10-year government bonds reached 3.8%, also returning to high levels not seen since 2007. This sell-off has weighed down global equity markets, and G7 finance ministers will exclusively discuss this round of bond selling at their meeting this week.

According to Ajay Rajadhyaksha from Barclays Fixed Income, Currency and Commodities Research, in a report dated May 18, "Long-term bonds were not just sold off last week; they have broken through ranges everywhere." Its core judgment is that debt growth is outpacing economic growth, inflation trajectories are worsening, and there is a political lack of willingness for fiscal reform. Even if long bonds have declined, there is not enough reason to extend duration.

JPMorgan Asset Management portfolio manager Priya Misra issued a similar warning: "Long-end interest rates are rising in sync worldwide, often reinforcing one another, as expectations for rate hikes by the Federal Reserve are entering market narratives."

Multiple national bond markets breaking down simultaneously, revealing a collective "Fiscal Ponzi scheme"

The decline in a single country's bond market is typically attributed to domestic inflation, fiscal, political, or central bank communication, but this time, the simultaneous breakdown of markets in the UK, Japan, the US, and France indicates that the risks being traded are not just local.

The commonality is clear: major developed economies have debt levels generally exceeding 100% of GDP, and fiscal deficits are not covered by nominal growth. The US deficit is about $2 trillion, equivalent to 6.5% of GDP, with nominal growth around 4.5% to 5%; France's nominal GDP growth for the quarter ending in March 2026 is 2.2%, with a deficit of about 5%; and the UK's deficit exceeds 4%.

This highlights the core contradiction pointed to by a "Fiscal Ponzi scheme": the government continues to rely on new debt and rolling financing to maintain spending, but the speed of debt expansion exceeds economic growth, while interest costs have become more expensive again. As long as this combination doesn’t change, long-term bonds will require higher yields to attract buyers.

New expenditures are also increasing pressure. NATO agreed in The Hague last year to raise defense spending goals to 5% of GDP by 2035; European defense spending achieved double-digit growth last year as a percentage, and may continue for a decade; the US government is requesting Congress for a $1.5 trillion defense budget for the next fiscal year. These expenditures do not have corresponding cuts to offset them.

Blocking of the Strait of Hormuz, oil price shocks ignite inflation

Debt and deficits are already fragile, and energy price shocks further tighten policy space. The blockade of the Strait of Hormuz is a direct trigger for this round of turmoil in the bond market, as this most important global oil transportation route is obstructed, continuously pushing up oil prices and reigniting inflation expectations.

Barclays' basic assumption is that the average price of Brent crude oil will reach $100 in 2026, a 50% increase over the average price in 2025. This will directly worsen the inflation outlook, compress central bank room for rate cuts, and may even force the central bank to raise rates. Higher interest rates mean existing debt interest expenses continue to rise, and rising interest expenses make it harder for deficits to decrease. This resembles a fiscal ratchet, where each step forward leaves the government with less maneuvering space, and the compensation demanded by bond investors becomes higher.

JPMorgan managing director Priya Misra stated bluntly, "Unless the Strait reopens, the interest rate range has overall shifted upward."

From the short-end data, the yield on US 2-year bonds once rose to 4.09%, the highest since February 2025; the 10-year yield reported at 4.58%, a near one-year high; the overall US treasury bonds have recorded negative returns so far this year, while at the end of February, the annual increase was close to 2%.

Inflation narrative dominates the market, term premium is being repriced

Karen Manna, fixed income strategist and portfolio manager at Federated Hermes, believes: "We are seeing a world that is truly confronting a new round of inflation."

Kevin Flanagan, director of investment strategy at WisdomTree, expects the next consumer price index report to show annual inflation reaching 4%, which would be the highest level since 2023. He directly pointed out the market logic: "The inflation narrative is dominating the market, and the bond market is demanding higher premium compensation to hold new government bonds."

Last week’s treasury auctions confirmed this pricing: the yield on the 30-year auction hit 5%, the first time since 2007, but demand was tepid; investor demand for the 3-year and 10-year auctions was also lukewarm. Even though long bond yields have increased to year-high levels, this alone is not a sufficient reason to buy duration.

Federal Reserve path is completely reversed, bets shift from two rate cuts to a March rate hike

The inflation storm is reshaping expectations for Federal Reserve policy paths. The incoming Federal Reserve chairman Kevin Warsh now faces an environment that is far from the "easing path" drawn by the market at the beginning of the year.

Traders currently view a March rate hike next year as a high probability event, with the probability of a rate hike in December about three-quarters; however, at the end of February this year, the market still expected two rate cuts in 2026. US treasury yields are now roughly 50 basis points or more higher than the levels at the end of February.

Officials' statements further solidify hawkish pricing. Chicago Fed President Austan Goolsbee stated last week that widespread price pressures may even indicate an overheated economy; Federal Reserve Governor Michael Barr called inflation the "overwhelming" risk the economy faces. The minutes from the Federal Reserve's April meeting will be released this Wednesday, and the market will closely monitor how much support dissenting members have received among officials.

The latest JPMorgan US treasury investor survey shows that treasury short positions have risen to the highest level in 13 weeks, with market bets on further declines in the bond market significantly heating up.

Japan's low interest rate system is being repriced

The yield on Japan's 30-year government bond reached 4%, which is not extreme when considered in the context of the US or UK, but carries a different significance for the Japanese market. For the past 20 years, Japan's long-term interest rates have been near zero, with the asset-liability structures of pensions, insurance companies, and local banks built around this environment.

The Bank of Japan's policy interest rate is currently 0.75%. At the April meeting, three of the nine members opposed the existing stance; market pricing shows a 77% probability of a rate hike in June. Even if the Bank of Japan raises rates to 1%, real rates will still be significantly negative.

The upward movement in Japan's long-end yields can be interpreted as monetary policy normalization: the end of deflation, real wage growth, and the economy returning to a more normal state. But the problem is that for an economy whose debt exceeds twice GDP, interest rate normalization may not be mild. A 4% yield on 30-year Japanese bonds is not just a change in yield numbers but means that the entire low-interest financial system needs to be repriced.

UK and France: Political structures make it nearly impossible to reduce deficits

The Labour government in the UK holds a working majority of over 150 seats in a 650-seat parliament, theoretically having the capacity for fiscal adjustments. However, last summer, a savings of £1.4 billion concerning winter fuel subsidies sparked a backlash from Labour's parliamentary caucus.

Political pressure is also increasing. 97 Labour MPs demanded the prime minister's resignation or a departure timeline; leading challenger Andy Burnham once argued that fiscal policy should not bow to the bond market, later clarifying that he would not completely ignore investors. The UK has changed four prime ministers and five chancellors in the past four years. Bond market pricing indicates that the Bank of England still has over 60 basis points of potential rate hike space by the end of the year, even though Governor Bailey may prefer to take a wait-and-see approach.

France's problem may not be as glaring as UK debt, but its fiscal structure is similarly tricky. France has changed five prime ministers in less than three years. The current government, aiming for a budget with a target deficit rate of 5% of GDP, has survived two votes of no confidence. The reform to raise the retirement age to 64, happening in 2023, is under attack, even as 64 remains lower than most Western economies. France's deficit is already significantly higher than the nominal GDP growth rate, and voters would strongly punish attempts at austerity; constitutional arrangements also make it easier for parliament to block spending cuts. Everyone knows that deficits must decline, but no one is willing to bear the political costs to make it happen.

US buyer structure has changed: foreign central banks turn to gold, private investors demand higher prices

The yield on US 30-year government bonds has surpassed 5% for the first time since 2007. The direct cause is rising inflation, fiscal expansion, and high deficits, but this is not new; a deeper change is the marginal buyers are changing.

The US federal deficit is about $2 trillion. The Congressional Budget Office estimates that the proportion of publicly held federal debt to GDP will rise from the current level of over 100% to 120% by 2036. However, this forecast may still be overly optimistic. One crucial variable is tariff revenue: The effective US tariff rate has fallen from a high of 12% to 7% to 8%, below the 15% assumed by the Congressional Budget Office. Even if it rises to 10%, tariff revenue over the next ten years would only be about 60% of the assumed $3 trillion deficit reduction scale. Assumptions regarding defense spending and interest costs may also be too low.

The dollar's status as a reserve currency remains a structural advantage for the United States, allowing it to finance at rates difficult to obtain by similar indebted countries. However, this does not mean that a 6.5% deficit rate is sustainable. Foreign central banks were stable buyers of long-duration assets in the past, but after the freeze of Russia's foreign reserves, their allocation has shifted to gold. Last year, the share of gold in central bank reserves exceeded that of US treasuries. Japan, as the largest holder of US debt, also has more attractive domestic market rates. The Federal Reserve is still in a balance sheet contraction phase. The buyer of long bonds is now private investors, who are more sensitive to price and demand higher term premiums.

The Federal Reserve is not a "fuse" for long bonds

Debt management agencies have relatively reduced long-term bond issuance over the past few years, and may continue to adjust their issuance structure in the future, but this can only alleviate supply pressure and cannot change the direction of fiscal and inflation.

There has been discussion in the market about whether the Federal Reserve will be forced to restart large-scale asset purchases to prevent long-end rates from continuing to rise. However, Warsh’s previous statements regarding the Federal Reserve's balance sheet indicated that "a bloated balance sheet can be significantly reduced," which does not suggest readiness to implement a US-style yield curve control.

In the face of ongoing sell-offs, some investors choose to remain on the sidelines. WisdomTree analyst Kevin Flanagan stated that they currently insist on holding floating rate notes and maintaining a low interest rate exposure, "better to buy late than to buy early." He believes that the 4.5% yield level on 10-year bonds is "more of a psychological barrier," and if the situation in the Middle East escalates again and pushes oil prices higher, yields may retest last year’s high of 4.62%. Hank Smith, director of investment strategy at Haverford Trust, takes a more cautious stance, stating that whether the rise in consumer and producer prices is temporary, "or will last until 2027" remains an open question.

The driving forces behind the sell-off include fiscal deterioration, rising defense spending, sticky inflation, and constrained central banks, all of which are unlikely to disappear in a week or two. Unless economic data weakens significantly or fiscal paths undergo credible changes, developed countries’ long bonds are still trading the same issue: the low interest rate financing model of the high debt era is being repriced by the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。