Original Title: Intel Should Raise Capital

Original Author: Semianalysis

Original Translator: Peggy, BlockBeats

Editor's Note: Since breaking through in early April, Intel's stock price has continued to recover, and in June, it experienced two key catalysts: first, market rumors that Google placed AI chip orders with Intel, leading to a significant one-day surge in stock price; second, Bank of America exceptionally upgraded Intel's rating from "underperform" to "buy," raising the target price from $96 to $135. Behind this rebound, the market is re-evaluating not only Intel's short-term performance but also its strategic position in AI CPUs, advanced process manufacturing, and the domestic chip supply chain in the United States.

INTC Stock Price Trend

Now, Intel's transformation narrative is shifting from "self-rescue" to "re-expansion." With Chen Lifeng taking over as CEO, a new board refresh, and strategic capital inflow from the U.S. government, SoftBank, Nvidia, etc., market expectations for Intel have clearly improved. However, this article reminds us that what ultimately determines whether Intel can return to the core table of advanced process technology is not merely customer commitments and stock price rebounds, but whether it has sufficient capital to fully build out its foundry capacity.

The author believes Intel's problems over the past decade largely stem from financial engineering: the sale of assets, introduction of joint venture partners, and alleviating cash flow pressure through Smart Capital (reducing capital expenditure pressure through joint ventures and asset disposals) have ceded long-term returns from core assets like fabs.

Currently, Intel should not focus on stock buybacks, but rather take advantage of its strong stock price to raise equity financing. The reasons are straightforward: on one hand, current valuations are high, and a 4% to 5% dilution could raise about $25 billion, significantly enhancing Intel's ability to build advanced process capacity; on the other hand, the entry prices for the U.S. government, SoftBank, and Nvidia were all below the current stock price, so a new issuance would not necessarily "punish" new shareholders but could actually increase the book value per share and provide these strategic investors with paper profits.

More importantly, alternative financing methods Intel has tried in the past have proven to be costly. Whether it's selling NAND, reducing its stake in Mobileye, transferring Altera's controlling interest, or bringing in partners like Apollo and Brookfield through SCIP (the Semiconductor Cooperative Investment Project, which exchanges long-term earnings rights of fabs for external capital), essentially they have all been ways to trade cash for assets and future earnings. Now Intel is spending $14.2 billion to repurchase Apollo's stake in Fab 34, which precisely illustrates that relinquishing the economic benefits of fabs was not cheap. Continuing to accumulate debt will elevate balance sheet pressure, and further asset sales have limited room; equity financing has instead become the cheapest and cleanest source of funds available right now.

Therefore, the core judgment of this article is: Intel currently does not lack a "revival story," but genuinely lacks the capital needed to realize that story. The demand for Agentic CPUs (new CPUs for the AI entity era), potential major customers like SpaceX and Tesla, along with orders from Nvidia and Google, provide Intel with a demand base that it can showcase to the capital markets. For Intel, issuing new shares is not merely a matter of dilution but is an opportunity to exchange cheap capital for advanced process capacity, foundry operations, and execution rights in the narrative of silicon sovereignty while the market window is open. Missing this window may be more costly than the financing itself.

The following is the original text (the content has been reorganized for easier reading):

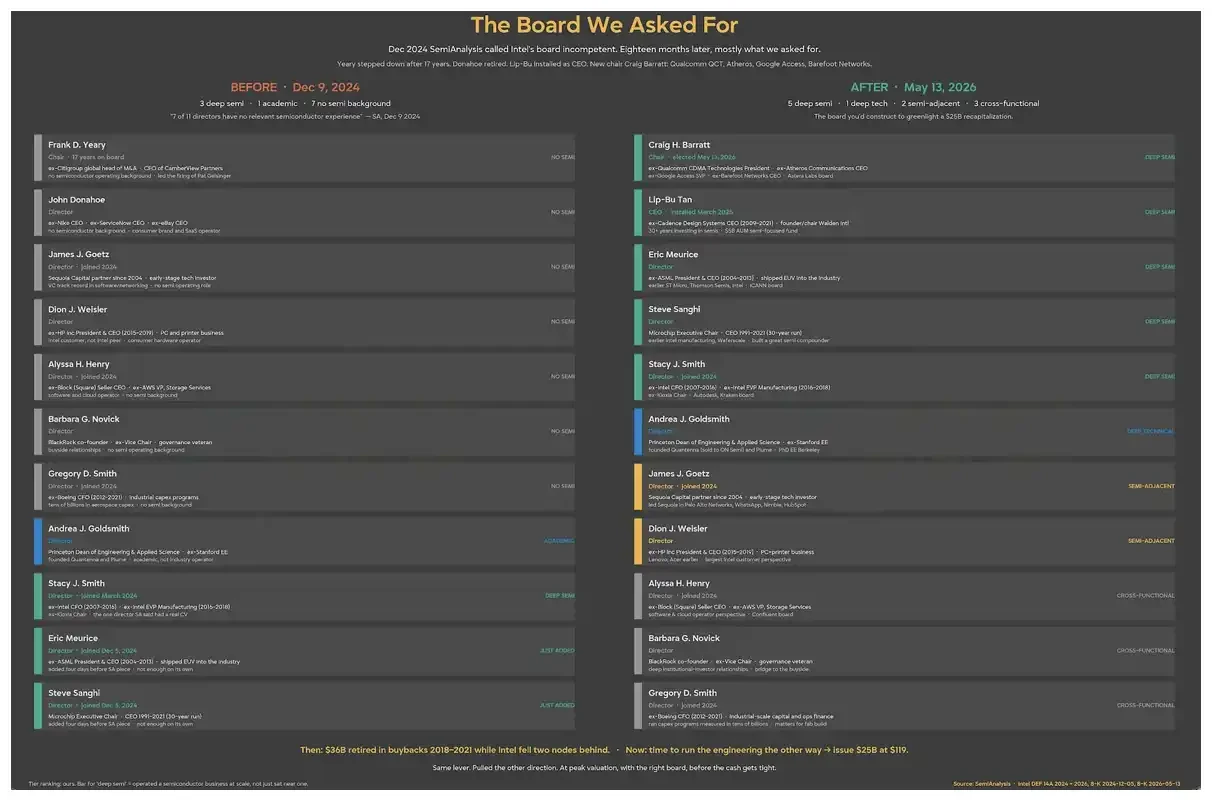

We have written many articles about Intel. This company holds special significance for us; it can almost be said to be the starting point of the semiconductor industry. Merely saying that we love Intel and acknowledge its role in the world is still far from enough. In the past, when early Intel products made mistakes, we pointed out the problems very frankly; but for its transformation, we have always held support and expectations. One of our firm judgments is that the Intel board is one of the biggest culprits causing Intel's decline, and recently, we have finally seen the changes we have long wanted to see.

Franky Yeary just stepped down after 17 years on the board, and the new board is now composed of people who truly understand this industry, not just financial engineers. The new chairman previously worked at Qualcomm, and Chen Lifeng (Lip-Bu Tan) serves as CEO, joined by Steve Sanghi and Stacey Smith from Microchip, as well as Eric Meurice from ASML on the board. In other words, this board finally truly understands technology.

However, even though Intel's transformation has partially started, the road to revitalizing the company remains long. Today we believe Intel should take another significant strategic bet under this new board: not to buy back stock, but to issue enough shares to completely repair Intel's financial situation at once.

Chen Lifeng has pulled Intel back from the brink and raised approximately $20 billion through investments from the U.S. government, SoftBank, Altera, and Nvidia. Intel should not stop halfway but should continue to capitalize on the current strong stock price. In the years of poor performance in the past, the company was a major net buyer of stocks; now, it is time to issue equity while the stock price is strong. If done properly, this will make Intel's transformation more likely to succeed.

Note: Chen Lifeng is the CEO of Intel, appointed in March 2025, and also joined the Intel board.

Current Equity Dilution Actually Rewards Already-Bet Investors

Look at what price these funds initially entered at. The U.S. government subscribed for up to 433 million shares at a price of $20.47 per share, corresponding to a 9.9% ownership stake; as of the end of the first quarter, 149 million shares are still in custody. SoftBank's entry price was $23.00, and Nvidia's entry price was $23.28. Now, all these holders are already in a profit position.

Therefore, the intuition that financing will punish recently-entering investors is actually misguided. Issuing shares at today's prices, which are substantially higher than these entry points, will increase the book value per share and also allow the U.S. government, SoftBank, and Nvidia to attain paper profits. That nearly 10% sovereign capital anchoring is also a significant reason Intel can carry out massive stock issuances at a lower cost during a hot market sentiment, supported by the U.S. government. As long as this leverage exists, it is worth utilizing.

Intel Needs Capital to Execute Its Transformation

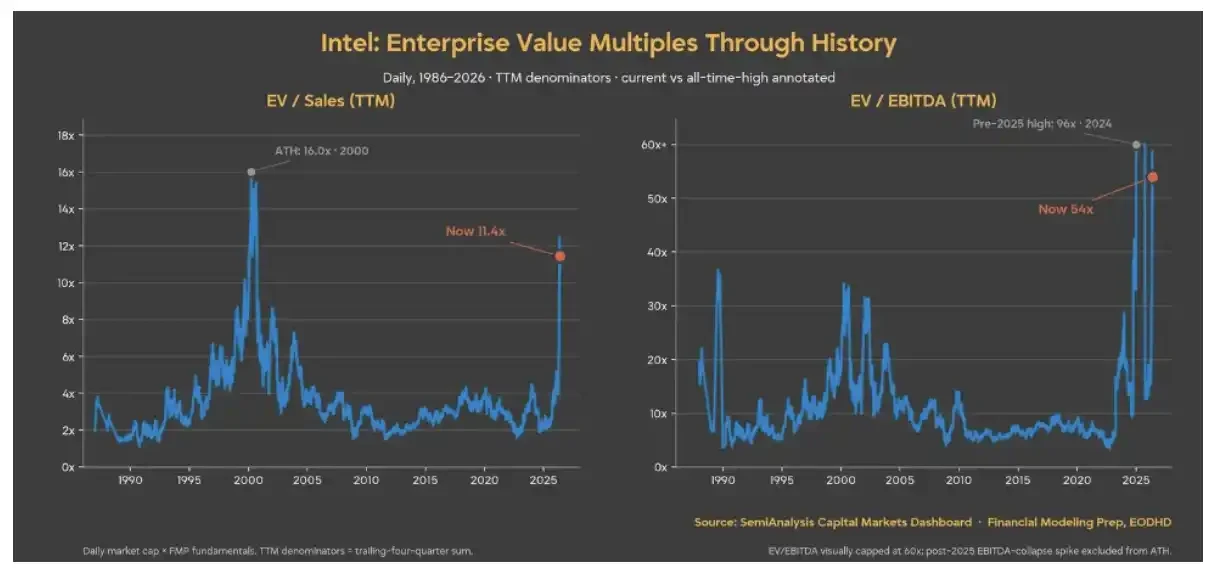

Based on performance over the past 12 months, Intel has rarely been as expensive as it is now since the 2000 bubble. We believe the company's prospects are bright, but one of the crucial factors to realize this prospect is capital; and the current stock price does not sufficiently reflect the actual execution risks.

More importantly, even in the most optimistic scenarios where demand for Agentic CPUs (new CPUs for the AI entity era) rebounds, Intel cannot shoulder all the investments required on its own. We believe now is the time for Intel to conduct a "reverse buyback": take advantage of the current market demand for stock issuance and raise equity financing.

Equity is Now the Cheapest Capital Intel Can Obtain

Opponents might argue that Intel has other ways to finance fabs. However, it has tried all of these methods and has just shown the market through its actions that these methods are not effective.

Apollo previously invested $11.2 billion for a 49% stake in the Fab 34 joint venture; Brookfield designed a financing structure for the Arizona fab project; and Silver Lake acquired 51% of Altera for an enterprise value of $8.75 billion, bringing Intel around $4.3 billion in net cash. Intel also phased out its NAND business with SK Hynix and continued selling shares of Mobileye. "Smart Capital" (through joint ventures and asset sales to reduce capital expenditure pressure) was once Intel's core narrative.

Then, on March 31, 2026, Intel agreed to buy back the 49% stake in Fab 34 held by Apollo and completed the transaction on April 8, totaling $14.2 billion, of which about $7.7 billion was cash and another $6.5 billion was in bridge loans. Management claims this buyback will increase earnings, and they are correct; this is the crux. If buying back fab shares enhances earnings, then selling the economic benefits of the fabs to partners has always been an expensive form of financing. SCIP (the Semiconductor Cooperative Investment Project) essentially transfers part of the long-term earnings rights of the company’s most valuable assets to external financiers in exchange for what appears to be a lower-cost capital but is actually more expensive. Intel has now shown with its checkbook: compared to continuing to relinquish the earnings of fabs, it prefers to hold onto the fabs itself and bear the corresponding debt.

So, let's eliminate other options. Continuing to conduct more SCIP is exactly the type of choice that management just spent $14.2 billion to reverse. Continuing to increase debt would compound on the existing $45 billion debt on the balance sheet; if the Apollo bridge loans are included, the debt scale would reach about $51.5 billion. Major asset sales have basically been completed; either Mobileye and Altera have already been sold, or the control of them has been sold. What remains is equity financing. At the current valuation level, equity is Intel's cheapest form of capital.

With the announcement of large Terafab projects and the overflow demand caused by the serious shortage of N3, Intel's foundry business has just begun. To truly seize this special window, Intel must become a key supplier for the industry at a time when advanced process wafer supply is tight. The funding required for this huge bet far exceeds what Intel can afford through its current operating cash flow.

A simple 4% to 5% equity dilution could raise about $25 billion, which is sufficient to turn the most optimistic supply capacity narrative into reality at this critical moment.

Agentic CPU Demand is Not Enough to Pay the Terafab Bills

Commitments from major customers like SpaceX, Tesla, and those represented by Terafab are key to solving the 14A capacity issues. The initial goal is to reach a wafer capacity of 100,000 pieces/month (WSPM), and then further expand to 1 million pieces—this will be very difficult and will bring extremely heavy capital pressure. But this step must happen because Chen Lifeng has publicly told the market that he would shut down the foundry business without customers. Now that the customers have arrived, it is time to build.

In addition to Terafab partners, Intel's order book is also being filled. Nvidia's DGX Rubin NVL8 configuration lists dual Intel Xeon 6 host CPUs; Google has signed a multi-year agreement covering Xeon and custom IPUs; and SambaNova is also joining in on inference business. The wafer quantities behind these orders have not all been disclosed, but the capital markets are funding a visible order book at a cost far lower than providing funds for a transformation story. And Intel finally has orders it can show the market. Raising equity financing based on signed demand is fundamentally different in pricing logic from raising equity financing based on a promise.

Due to lower-than-expected CPU demand, Intel has been doing everything it can to delay capital expenditures. But now, it is time to bet all the chips again, like in the Gelsinger era. This is a key moment for silicon sovereignty, and Intel must continue to double down.

The complete multi-phase project for Intel may cost up to $119 billion. While SpaceX will provide initial capital, Intel must also make a meaningful contribution. Even marginal capital matching means a need for new funds in the hundreds of billions, and this funding was not even in Intel's capital expenditure decision matrix a month ago.

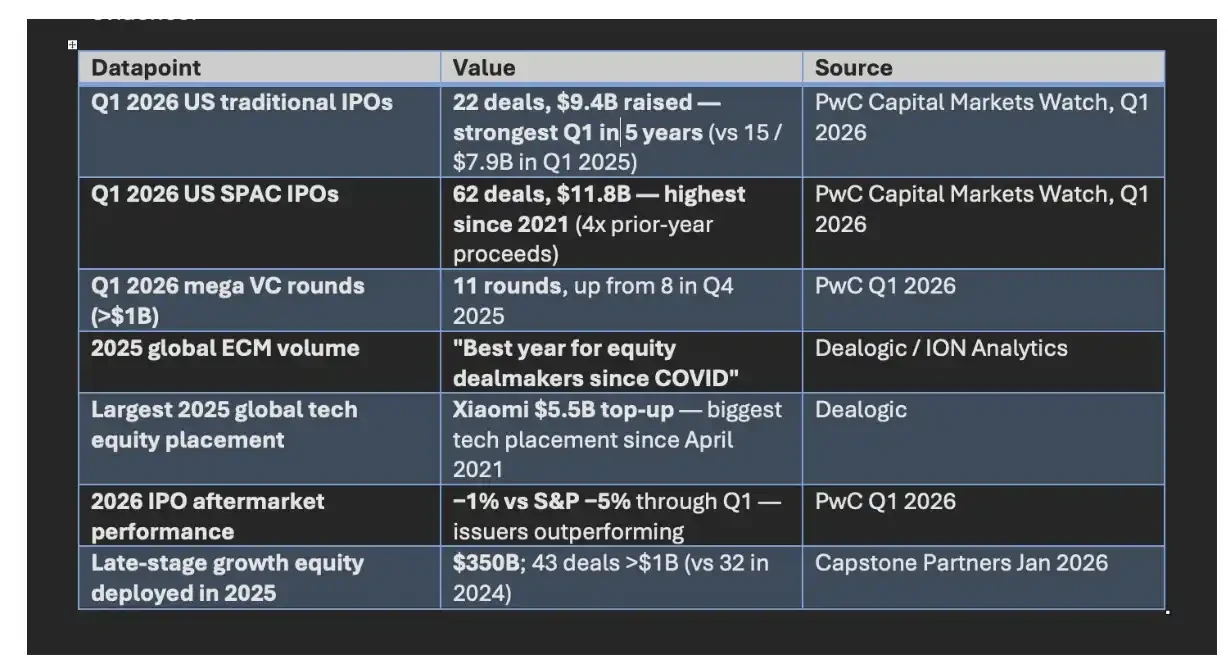

Now is the time to end the financial engineering of the past decade and issue shares immediately. Because although ramping up capacity is exciting, it will be very expensive. The current equity issuance window is the broadest it has been in a while; if Cerebras can raise $5.55 billion, Intel can raise $25 billion. This argument will only become stronger as Intel’s approx. $498 billion market cap can fully support a much larger follow-on issuance. From our observation, this window seems to have fully opened. Below are some data from other recent issuance cases.

The Trading Window Has Opened

In other words, the real problem for Intel now is no longer "Is there a story?" but "Is there enough capital to turn the story into capacity?" With strategic capital from the U.S. government, SoftBank, Nvidia, and others already in place and the supply of advanced processes in a tight window, equity financing is no longer just a defensive move to dilute shareholders but could become an offensive choice for Intel to rekindle its foundry ambitions and bet on silicon sovereignty. For Intel, missing this financing window may be even more expensive than the issuance itself.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。