The helplessness of the Korean exchange after the SpaceX IPO: Listing "Spacecoin" and SPX6900, is it just to borrow momentum to increase volume?

Written by: Four Pillars (@FourPillarsFP)

Translated by: AididiaoJP, Foresight News

Key Points

On June 16, 2026, Bithumb listed Spacecoin, and Upbit listed SPX6900, after which Bithumb also listed SPX6900. The Korean community linked these listings to SpaceX's NASDAQ IPO four days earlier (on June 12). A low-profile token and an old meme coin were listed at this time with names easily associated with SpaceX, and many interpreted it as the exchanges promoting trading volume by leveraging the buzz around SpaceX.

This interpretation is more convincing against the backdrop of poor performance by Korean exchanges. Dunamu's revenue in the first quarter of 2026 fell by about 55% year-on-year, and Bithumb reported a net loss. Both exchanges rely almost entirely on trading fees for income; when volume drops, earnings collapse.

Korea classifies tokenized stocks as securities, prohibiting cryptocurrency exchanges from handling them and not allowing cryptocurrency futures, derivatives, or spot ETFs. Meanwhile, Binance, Kraken, and Bybit are expanding into tokenized stocks and direct trading of overseas stocks, generating billions of dollars in related trades on the day of SpaceX's listing. The Korean exchanges can only participate in the global narrative through "similarly named spot tokens," a situation that is quite lamentable.

Regulations aimed at protecting investors have pushed exchanges into the most speculative corners of the market. With revenue sources and product lines like derivatives, tokenized stocks, and ETFs all shut down, the only lever exchanges can use to pull volume is through spot listings, and as the volume dries up, they tend to list high-profile and more speculative assets.

Background: Upbit and Bithumb List SPACE and SPX, the Shock in the Korean Community

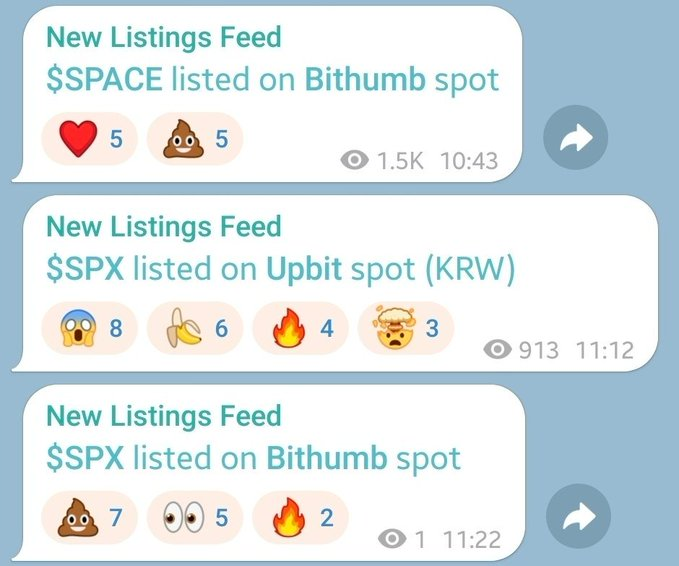

On the morning of June 16, 2026, the biggest topic in the Korean community was Bithumb listing Spacecoin (SPACE) and Upbit listing SPX6900 in the Korean won market. One might ask if this isn't just a normal token listing announcement? But the reason for the attention is not the listing itself.

What truly stirred the community was the combination and timing.

Four days earlier (on June 12), SpaceX went public on NASDAQ under the ticker SPCX. As is well-known, this is the largest IPO in history, and topics related to the stock have dominated the Korean crypto community, being a hot name since the weekend.

After Upbit and Bithumb issued their listing announcements, the community quickly suspected that the two exchanges were listing tokens with names and tickers similar to SPCX to leverage the momentum for increased volume. This association was based solely on context, but it was quickly accepted, which itself indicates the position of Korean exchanges.

The reaction quickly turned to self-deprecation: overseas platforms like Coinbase, Binance, and Bybit allow users to trade overseas stocks like SpaceX directly on their exchanges, while Korean exchanges, constrained by regulations, can only list at least a similarly named coin.

I believe this event should not be taken lightly. It clearly demonstrates how harsh the competitive environment is for Korean crypto exchanges relative to their overseas counterparts. This article will examine the current market and regulatory environment surrounding Korean crypto exchanges, as well as how these conditions differ from global standards.

The Current Situation of Korean Exchanges

High Dependence on Fee-Based Revenue Structure

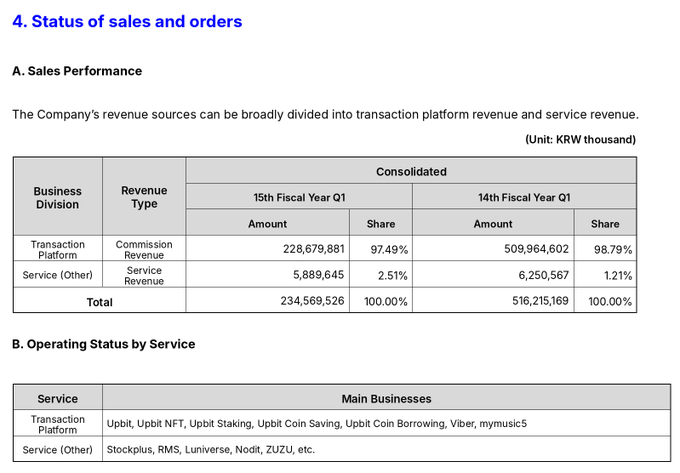

The first quarter of 2026's earnings report showed poor performance across major Korean exchanges. According to the quarterly report released via the Financial Supervisory Service's electronic disclosure system on May 15, Dunamu, operating Upbit, reported consolidated revenues of 234.6 billion won, a year-on-year decline of 54.6%. Operating profit dropped 77.8% to 88 billion won, and net profit fell 78.3% to 69.5 billion won. Upbit's fee revenue fell by 55.2%, tumbling into the 200 billion won range, while operating costs rose by 22% during the same period, severely squeezing profit margins.

Bithumb’s situation is even more severe. The first quarter revenue fell 57.6% to 82.5 billion won, with operating profit plummeting 95.8% to 2.9 billion won. Net profit turned negative, showing a net loss of 86.9 billion won, marking the second consecutive quarter of net loss after the previous quarter. The direct cause was a drop in trading volume leading to an 87% decrease in fee income. Additionally, the Korean Financial Intelligence Unit imposed a 6-month partial suspension of business and a fine of 36.9 billion won for violating the Specific Financial Transaction Information Act, which also reflected in the first quarter results.

The biggest problem is that the revenue structure of Korean exchanges relies almost entirely on trading fees. Fees account for approximately 97.5% of Dunamu's revenue, while Bithumb is as high as 99.99%. This structure is more a result of the regulatory environment discussed below rather than operational negligence.

Regulatory Landscape

Korean crypto exchanges can primarily handle crypto spot tokens, while other areas are mostly explicitly regulated or tacitly avoided.

- Tokenized Stocks: In June 2026, the Financial Services Commission and Financial Supervisory Service leaned towards classifying tokenized stocks as securities rather than virtual assets. Securities, regardless of how they are issued, are governed by the Capital Markets Act; under the Electronic Securities Act, only licensed electronic registration organizations can perform electronic registration of rights. If a crypto exchange issues or circulates securities tokens without being one of these organizations, it constitutes unlicensed operation. In other words, the rapidly growing tokenized stocks overseas are structurally assets that Korean crypto exchanges cannot handle, and this is unlikely to change in the short term.

- Futures and Derivatives: Korean crypto exchanges only provide spot trading and cannot offer perpetual futures or derivatives like options to domestic users. This is not explicitly prohibited by law but stems from obstacles left by a previous attempt. Coinone, one of the top five exchanges in Korea, provided margin trading with up to 4x leverage for about a year starting in December 2016. After the government's regulatory actions and police investigations began at the end of 2017, this service was completely shut down. In 2018, the police treated it as gambling for operating without approval from financial authorities, charging CEO Cha Myung-hoon and others with running a casino, and registering 20 users who traded more than 3 billion won as gamblers. The case was ultimately not prosecuted about three years later (in 2021) due to insufficient evidence. Since then, no crypto exchange has considered incorporating margin or futures trading.

- Tacit avoidance under self-regulation: Korean crypto exchanges are self-regulated by the Digital Asset eXchange Alliance (DAXA), which consists of five major won market exchanges. Their listing review standards include transparency issues arising from de-identification, the possibility of becoming securities, and money laundering risks. These standards effectively exclude privacy coins that emphasize anonymity, leading exchanges to avoid tokens that could be interpreted as securities. Assets that could raise questions of securities or gambling (like exchange tokens or prediction market tokens) are similarly infrequently seen on Korean exchanges.

Overall, almost all new areas that overseas exchanges are expanding into—derivatives, tokenized stocks, certain privacy coins, and prediction market tokens—are essentially blocked on Korean exchanges.

Comparison with Overseas Exchanges

Have Korean Exchanges Lowered Listing Standards?

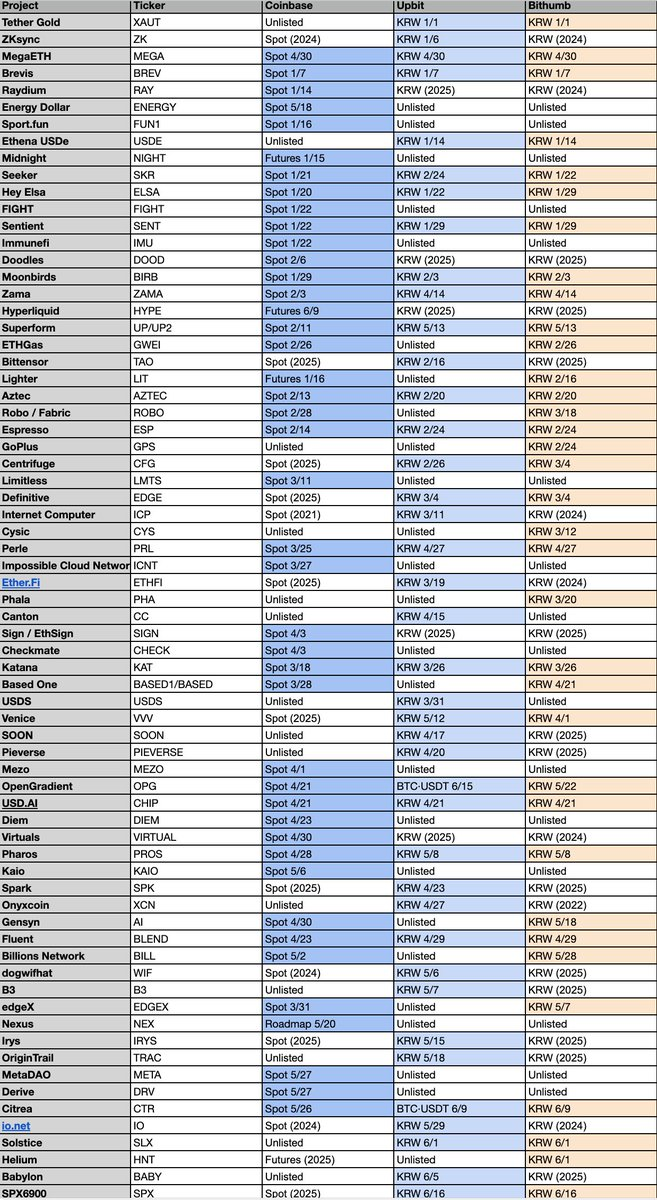

These listings have sparked accusations that Upbit and Bithumb have relaxed their review standards. The following table is my complete investigation of token listings by Coinbase, Upbit, and Bithumb in 2026; I hope to examine this accusation through data.

In terms of original listing quantities, Coinbase leads. Coinbase has listed many assets not listed by Korean exchanges, and a large proportion of them not only provide spot but also futures, offering exposure earlier. Looking only at frequency and timing, Coinbase is actually more aggressive.

In 2026, a considerable portion of the new won market tokens listed by Upbit had already been listed on Bithumb. For example, Bittensor (TAO), Internet Computer (ICP), Ether.fi (ETHFI), io.net, dogwifhat, Spark (SPK), and Babylon, most of which are names that do not trade actively on Bithumb. Rather than being newly discovered assets, they are tokens that already exist in the market and were listed afterward, likely exacerbating the feeling that "the listings aren't fresh enough."

This perceived decline in quality does not stem from a decrease in standards per se, but rather from the diminishing volume that can be pulled from single listings. In an environment where the volume driven by a single listing quickly dries up and fresh assets worth listing become increasingly scarce, exchanges maintain their listing pace by following up on tokens already listed by Bithumb. Ultimately, complaints from Korean users are not directed at any specific name but rather arise from the perceived convenience gap compared to other markets offering new products like tokenized stocks.

As overseas exchanges target becoming the "Everything Exchange," Korean exchanges...

Meanwhile, the path taken by large overseas exchanges is quite the opposite. They are surpassing the fences of virtual assets, moving towards the so-called "Everything Exchange"—a single app where all assets can be traded.

The most obvious example is Coinbase. In the fourth quarter of 2025, Coinbase stated in its shareholder letter that it had started trading stocks and ETFs (besides crypto and derivatives) within the app, opening up about 3,000 assets to early users, aiming to bind traditional and digital assets into a single investment experience. The letter also emphasized that it has become the first platform in the industry to launch 24-hour U.S. perpetual products, enhancing its market share in derivatives.

Binance is even more direct. As of June 1, 2026, it opened up U.S. stock trading to eligible users, allowing direct access to over 7,000 U.S.-listed stocks and ETFs. Additionally, it launched bStocks, which tokenizes U.S. stocks 1:1, settles in stablecoins, can be withdrawn to self-custody wallets, and trades around the clock.

Bybit has joined the xStocks Alliance (a tokenized stock alliance), handling tokenized stocks created by regulated Swiss issuers. These price-tracking tokens are backed by real stocks and can be traded using stablecoins around the clock.

Some platforms place tokenized stocks at their core. Kraken's tokenized stock product xStocks holds over 100 U.S. stocks and ETFs, with cumulative trading volume reaching hundreds of billions of dollars, aiming to grow to over 500 by the end of 2026. Gemini offers zero-fee 24-hour tokenized stocks in some European countries, while Robinhood provides stock tokens tracking underlying stocks in Europe.

The most dramatic stage for showcasing the gap between domestic and foreign trading environments is the SpaceX listing itself. For overseas exchanges, this listing is a test in the race for tokenized stocks.

Even before SpaceX started trading on NASDAQ, four tokenized products were already in operation. Ondo Finance, Kraken, and the Solana-based Backpack each launched tokenized SpaceX, and Hyperliquid opened pre-listing perpetual futures. Bybit also selected SpaceX as the first product for its tokenized IPO access service, opening spot trading on the day of the listing. Within 24 hours post-listing, the entire crypto market saw around $9 billion in SpaceX-related trading, with Binance alone processing $5.6 billion.

In contrast, Korean crypto exchanges have no place on this stage. Tokenized stocks, perpetual futures, or any products tracking SpaceX are not permitted domestically. While major global exchanges transact billions of dollars around the same narrative, Korean crypto exchanges effectively have no channels to join this flow of funds.

Impact and Insights

For exchanges that cannot compete in product scope, the remaining battlefield is listings. The revenue of Korean exchanges actually relies on spot trading fees. In a structure where they cannot handle derivatives, stocks, or tokenized securities, the only sure way to increase volume is to list names that can catch investors' attention at the right time.

The strict regulation of Korean crypto exchanges aims to protect investors. It excludes leveraged margin trading, which amplifies losses, from being viewed as substantive gambling; filters out securities tokens with opaque rights structures; and excludes assets prone to money laundering or price manipulation from listing review. However, when this protective framework sequentially strips exchanges of their revenue sources and product lines, the only remaining lever becomes spot listings. And as the volume dries up, this lever is increasingly shifted towards high-profile and more speculative names. Protection at the product phase ultimately encourages a tilt towards speculative assets at the listing phase. What we witnessed this time is just one scenario where this tilt comes to light.

A deeper issue is that even such protection cannot work entirely. Domestic investors wishing to trade perpetual futures or tokenized stocks will not simply abandon their demand. They turn to overseas platforms like Binance, Bybit, and Hyperliquid. In fact, all platforms operating tokenized products and pre-listing perpetual futures during the SpaceX listing were overseas. In other words, regulations did not eliminate high-risk trading itself but pushed it into markets that Korean authorities cannot regulate. When the 2027 tax and cross-border information exchange (CARF) fully comes into effect, the scale of this offshore trading will be revealed in the data, but that will be more of an after-the-fact confirmation of what has already happened. Ultimately, investors still bear speculative exposure but lose domestic protections, and Korean exchanges miss out on the revenue these trades could have generated.

This structure also leaves exchanges themselves vulnerable. With almost all revenue coming from a single engine of trading fees, they are completely exposed to volume cycles. While Coinbase diversifies its revenue into custody, stablecoins, tokenized stocks, and derivatives to buffer against downturns, Korean exchanges must face the same cycle head-on with a single product. As this gap compounds quarter after quarter, it translates into disparities in investment capability and product competitiveness, ultimately returning in the form of a convenience gap perceived by domestic users.

Of course, the Korean government is also making efforts to construct crypto regulations. The second phase of the Digital Asset Basic Act, institutionalization of security token offerings (STOs), allowing corporate trading, won stablecoins, and spot ETFs have all been brought to the agenda in 2026, clearly demonstrating the government's efforts. However, even if these new products are opened up, they are likely to be allocated to existing licensed institutions, such as securities firms and electronic registration organizations, rather than today's crypto exchanges.

Stock brokerage (i.e., investment brokerage under the Capital Markets Act) is an inherently licensed operation that can only be conducted with a financial investment business license issued by the Financial Services Commission. Upbit and Bithumb are registered only as "virtual asset service providers" under the Specific Financial Transaction Information Act and the Virtual Asset User Protection Act and do not hold this license. Exchanges seeking to broker stocks independently must navigate separate thresholds, including capital requirements and major shareholder qualification checks, and the longstanding stance of "separation of finance and crypto" (opposing the mixing of traditional finance and virtual assets within one company) has long blocked this entry.

Therefore, the merging that is actually happening is not exchanges becoming securities firms but securities firms and banks acquiring shares in exchanges and bringing them under the same umbrella. In 2026, Hanwha Investment & Securities increased its stake in Dunamu to 9.84%, becoming the third-largest shareholder; Hana Financial Group held 6.55%; and Samsung Securities, Samsung Card, and Samsung SDS held a combined 4%. Korbit was acquired by Mirae Asset Group; Korea Investment & Securities signed a strategic equity investment, holding 20% of Coinone’s shares, becoming its third-largest shareholder. As the financial authorities' attitude toward the separation of finance and crypto becomes more cautious and leans towards easing, such alliances are rapidly increasing.

Will Korea, like overseas, retain the possibility of crypto exchanges growing into "Everything Exchanges"? I think the possibility is very slim. Stock and securities functions will flow to licensed securities-affiliated companies, while exchanges themselves are likely to remain within the fence of spot trading. This is also why I believe that even if new products are opened, their channels are more likely to be allocated to existing licensed institutions, such as securities firms and electronic registration organizations, rather than crypto exchanges.

What I want to argue is not that regulation should be loosened immediately. The issue is that a protective framework designed for an era is now creating increasing intangible costs as the market rapidly moves towards asset integration. Crypto exchanges operating in such a harsh environment will pass these costs onto users during the current bear market, ultimately leading to listings of short-lived tokens that cater to one-off trading demands and create more victims. I hope everyone can recognize this.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。