Written by: Rita

Trend Guide

The Philadelphia Semiconductor Index (SOX) has increased by 85% since March, but Nomura Securities clearly believes that the peak of this cycle has not yet been reached. The most critical change is that the number of global data center construction projects increased from 240 to 280, and the number of gigawatt-level projects increased from 40 to 50. This indicates that the deployment of computing power has been pushed to after 2027, which fundamentally affects the extension of the entire cycle.

Data Center Deployment Delays Extend the Cycle

Nomura Securities' tracked deployment capacity forecasts are: 26.7GW (gigawatts) in 2026, 32.3GW in 2027, and 22.9GW in 2028. This corresponds to a demand for 4-6 million AI chips per year. 2027 is the peak of deployment, after which it begins to decline. This timeline indicates that the peak pressure on production capacity has been pushed to 2027-2028.

The growth forecast for the global server market has been raised from 43% to 74% in 2026 and 65% in 2027, and the growth rate for AI servers has been raised from 58% to 78% and 76%. This degree of upward adjustment is rare. If realized, 2026-2027 will be the two most tense years for the entire server industry chain.

CPU Demand Severely Underestimated

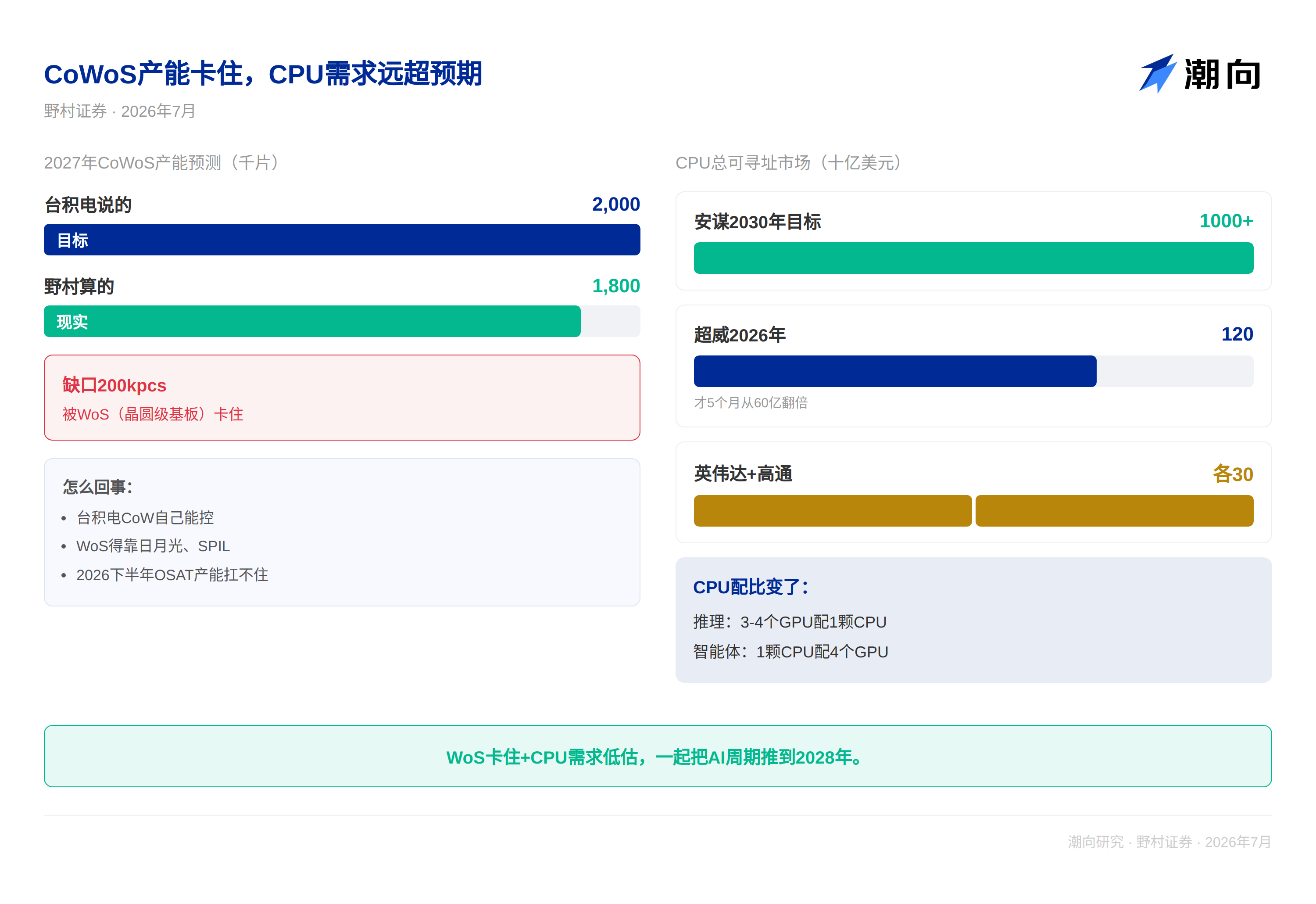

The most easily overlooked aspect of the report is the growth of CPU demand. Arm targets a total addressable market for data center CPUs exceeding $100 billion by 2030. AMD estimated that the server CPU TAM would be $60 billion in November 2024, but it had doubled to $120 billion by May 2026, merely five months later. Nvidia and Qualcomm are each targeting $20 billion.

The ratio of CPU to GPU is undergoing a fundamental change. In inference scenarios, the ratio has changed from 3:1 to 4:1. However, for agentic workloads, the ratio has reversed to 1:4 (1 CPU to 4 GPUs). This means that CPU demand far exceeds market expectations and is a key variable for the extension of the cycle.

WoS Bottleneck is a Real Constraint

The most valuable insight of the report is the micro-analysis of CoWoS capacity. TSMC has raised its CoWoS capacity target from 1,300-1,350kpcs to 2,000kpcs (by 2027), but Nomura Securities only models 1,800kpcs. This is an accurate estimate of the actual situation.

TSMC's chip-level packaging (CoW) capacity expansion is under its own control, but the WoS expansion relies on open foundry testing (OSAT) manufacturers such as ASE and SPIL, and the speed of capacity adjustment is significantly lagging. Starting in the second half of 2026, WoS capacity will become a constraint on the overall CoWoS output. TSMC's capacity targets have historically not been met, with actual capacity closer to 1,800kpcs.

Intel's EMIB-T (Embedded Multi-die Interconnect Bridge) technology poses a challenge to TSMC. Google's v9 Tensor Processing Unit may adopt a Through-Silicon Via (TSV) solution in 2028, threatening TSMC's pricing power in advanced packaging.

Target Prices of Nine Companies Raised by 15-50%

Nomura Securities has raised the target prices of nine AI semiconductor companies. Among them, MediaTek was raised by 49.5% to NT$5,800, TSMC by 46.4% to NT$3,425, Realtek by 33.9% to NT$2,115, NXP by 30.9% to NT$6,880, GlobalWafers by 28.2% to NT$1,200, Jingyuan Electronic by 26.6% to NT$390, Bihai Technology by 24.1% to NT$720, Kingstone Integrated by 22.3% to NT$19,100, and ASE by 15.5% to NT$730.

Trend Perspective

Nomura Securities' micro-insight about the WoS bottleneck is the core value of this report. However, investors need to be vigilant: TSMC's capacity targets have historically not been met, and if OSAT expansion is slower than expected, the actual output of CoWoS in 2027 may fall below 1,800kpcs.

Nomura Securities adjusted TSMC's rating in its May AI report, and just three months later raised the target price again, such frequency of changes warrants caution. However, Nomura Securities' tracking accuracy has consistently been high.

Attention should be paid to the progress of Intel EMIB-T, Google's TPU, and Amazon's Trainium, which are "non-Nvidia" routes. These alternatives could shift the entire supply chain landscape.

From an investment perspective, the top of the AI cycle is at least delayed until 2028, and any pullback during this period is worth buying. However, it should also be recognized that capacity constraints are evolving from the supply side to the pricing side, which may affect chip manufacturers' profit margins less than expected.

Disclaimer

This article is an整理与解读 of third-party brokerage research reports by Trend Research. The ratings, target prices, earnings forecasts, and related judgments quoted in this document are the views of the analysts of that brokerage and only represent the positions of their respective organizations, not the views of Trend Research and do not constitute any investment advice.

The market has risks, and decisions need to be independent. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。