This article is from:Bankless

Translated by|Odaily Planet Daily(@OdailyChina);Translator|Azuma(@azuma_eth)

Strategy disclosed on July 7 that the company sold 3,588 BTC worth about $216 million between June 29 and July 5.

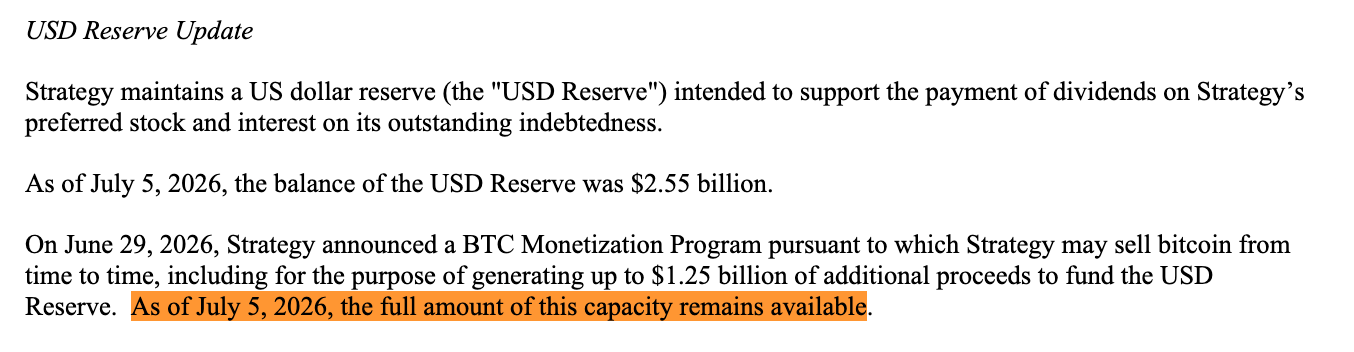

The funds were used to pay the dividends of STRC and to replenish the previously used dollar reserve (USD Reserve) for paying dividends. Despite completing this sale, Strategy stated that its full reserve-building capacity of $1.25 billion remains intact.

- Odaily Note: In the self-rescue plan announced last week, Strategy indicated that it was authorized to sell BTC and build up to $1.25 billion in dollar reserves.

In other words, the $216 million BTC sold by Strategy to replenish reserves was not included in the previously disclosed reserve-building capacity.

Strictly speaking, there is a technical difference between the two: one is "replenishing reserves," and the other is "building reserves." But in reality, both types of sales ultimately flow into the same reserve pool for the same purpose, only classified for different uses.

From another perspective, the previously disclosed "Bitcoin Monetization Program" (selling BTC) does not limit Strategy to only selling $1.25 billion worth of Bitcoin; it only restricts one funding pool - that is, using the sale of BTC to "build" dollar reserves.

The program also allows Strategy to sell BTC for other purposes, which is exactly what we see happening now.

Three Funding Pools

On June 29, after weeks of pressure on MSTR and STRC, Strategy launched the aforementioned BTC "Monetization Program" as part of its larger "Digital Credit Capital Framework."

The program allows Strategy to sell Bitcoin, and indeed mentions three main uses:

- The first is to build reserves, allowing for the sale of up to $1.25 billion in BTC for building dollar reserves (USD Reserve);

- The second is to cover the preferreds, which means selling BTC to pay for the fixed dividends and interest obligations that Strategy has on its preferred shares and debt. If management believes "selling BTC is more beneficial than issuing common stock," it can also sell BTC to replenish the previously used reserve fund for these obligations.

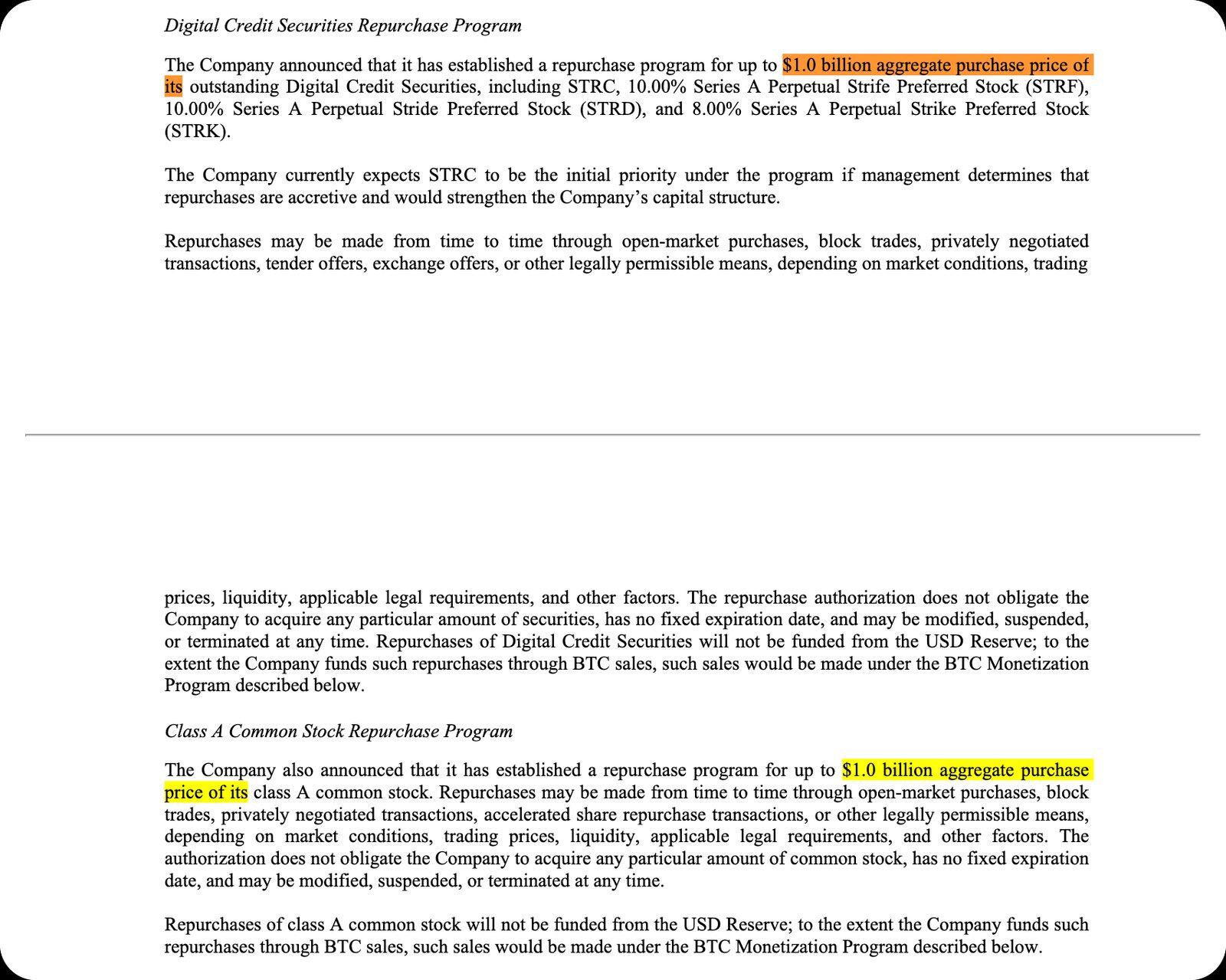

- The third is to fund buybacks, which means selling BTC to repurchase up to $1 billion of preferred shares and up to $1 billion of MSTR common stock. Additionally, the proceeds from BTC sales may also be used to cover related taxes, fees, and other costs.

At that time, the entire market's discussion focused on the $1.25 billion limit of the first funding pool, but the reality is far from that.

Just looking at the third funding pool alone, it actually adds an extra $2 billion in sales capacity; therefore, when only considering the parts with clear upper limits, the BTC selling scale currently designed by Strategy has already exceeded $3 billion, and this does not include the funding pools for paying dividends, interest, and replenishing reserves — this part currently has no disclosed upper limit.

Building vs. Replenishing

The subtlety lies here.

The purpose of the dollar reserve (USD Reserve) is to pay these preferred share dividends and debt interest obligations. Under the current policy framework, it cannot be used for stock buybacks.

As of June 28, Strategy's dollar reserve size was $2.55 billion, enough to cover the company's annual debt and preferred stock payment obligations of about $1.76 billion, roughly equivalent to a coverage period of 17 months. The minimum requirement set by the Strategy Board is to maintain a 12-month coverage level unless the Board approves a reduction of this standard.

This is also why the boundary between "building reserves" and "replenishing reserves" is worth noting.

- Selling BTC before paying dividends adds cash to reserves: this is defined as "building."

- Using reserves to pay dividends, then selling BTC to replenish reserves: this is defined as "replenishing."

The program treats the two as different categories, but they essentially do the same thing — convert BTC into cash to cover preferred share dividends and interest expenses.

These details have actually been disclosed in the documents, but the recent sale made the differences in this classification more apparent. Strategy sold $216 million worth of BTC, used the funds to pay dividends and replenish reserves, while still announcing that its $1.25 billion reserve building capacity remains intact.

Now, the market needs to begin to understand Strategy's "special language": "building" and "replenishing" are essentially just accounting classifications, but they determine whether Strategy's BTC sales will occupy that "public capacity" seen in the market.

From Hoarding Coins to Active Capital Management

In the announcement on June 29, Michael Saylor stated that the framework reflects Strategy's needs for "liquidity, discipline, and active capital management."

Strategy CEO Phong Le stated more directly: “Strategy is transitioning from a one-way capital issuance model to an active capital management model.”

As Matt Walsh and Jeff Dorman from Castle Island explained last week in a podcast, Strategy is gradually transforming into an actively managed hedge fund.

The past narrative of Strategy was very straightforward: sell MSTR stock → buy Bitcoin → provide investors with leveraged BTC exposure, but now the logic has changed.

Now, Strategy is buying and selling different components of its capital structure to manage the pressures between common stock (MSTR), preferred shares, dollar reserves, and Bitcoin assets (BTC).

This dynamic also brings new conflicts of interest, Walsh and Dorman point out:

- Selling common stock can support preferred share dividends but will depress MSTR's premium relative to its BTC value;

- Selling Bitcoin can extend cash flow duration but will further weaken the core narrative of "never selling";

- Supporting the preferred share system can maintain market confidence but will consume cash reserves;

- Cutting preferred share dividends can protect liquidity but may lead to a collapse in preferred share prices.

The so-called "reserve loophole" is a manifestation of this transformation. Bitcoin is no longer merely an asset that Strategy continuously accumulates; it is becoming a balance-sheet lever used to maintain the operation of the preferred share system.

What Will We Ultimately See

Now, investors must assess whether Saylor has the capability to operate such a "machine" — every adjustment of a lever in the capital structure helps one part while potentially threatening another part.

This is precisely the most noteworthy conclusion after the document disclosure on July 6. Strategy does not lack options. It may have more operational space than what the market perceives on the surface.

Please do not mistakenly think that the $1.25 billion limit represents the total cap for Strategy's Bitcoin sales.

Now, Strategy has become an institution that requires the market to redefine its understanding. Now, every specialized term has become more important:

- Build;

- Replenish;

- Issue;

- Repurchase;

- Defend;

Just as Federal Reserve observers meticulously analyze every punctuation mark in each policy statement, the market must also dissect each term used by Strategy to assess what it means for future BTC sales.

By launching this plan, Strategy has secured greater flexibility, but the underlying contradictions still exist. This is no longer a simple “leveraged Bitcoin transaction”; it has now turned into a bet on its ability to manage active capital.

Can Strategy continuously excel at "selling BTC," "replenishing reserves," "issuing securities," "repurchasing stock," and "maintaining capital structure," while ensuring that none of these links disrupt the others?

I personally would not want to bet on that.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。