Author: Binance Research Institute Moulik Nagesh

Key Points

In 2025, the resurgence of U.S.-led trade protectionism is strong. Since Donald Trump resumed the presidency in January 2025, the U.S. has implemented a series of large-scale new tariffs—targeting both specific countries and specific industries—raising concerns about a global trade war. Just in the past week, the U.S. launched a new round of "reciprocal" tariffs, prompting other countries to announce countermeasures.

This report will analyze how these tariffs (the most aggressive tariff measures since the 1930s) will impact the macroeconomy and the cryptocurrency market. We will examine, based on data, the levels of tariffs, macroeconomic trends (including inflation, growth, interest rates, and Federal Reserve outlook), and their effects on the performance, volatility, and correlation of crypto assets. Finally, we will explore key future observations and the market outlook for crypto assets in an environment of stagflation and protectionism.

2025 Tariff Resurgence

After several years of relative trade peace, 2025 saw a rapid reversal. In the first few days of President Trump's return to the White House, he began fulfilling his campaign promises by imposing tariffs on a wide range of imported goods—covering specific countries and industries.

Trade tensions escalated further on April 2. On that day, the U.S. announced comprehensive "reciprocal" tariffs and designated this day as "Liberation Day," marking a new turning point in this round of the global trade war. Many countries that previously viewed their trade relations with the U.S. as normalized have now undergone a fundamental shift. Key events from the past week include:

· Base Tariff: The U.S. announced a new 10% uniform tariff on all imported goods, reversing decades of trade liberalization. This base rate took effect on April 5.

· Targeted Tariffs: In addition to the base rate, higher country-specific tariffs were added. President Trump referred to these as "reciprocal" tariffs, aimed at countries that impose high barriers on U.S. products. Notably, Chinese goods will incur an additional 34% tariff—resulting in a combined tariff rate of 54% after the original 20%. Other countries' targeted tariffs include: 20% on EU goods, 24% on Japan, 46% on Vietnam, and 25% on automobile imports. Canada and Mexico were not included in the new list as they had already been subjected to a 20% tariff in February.

· Global Retaliation: U.S. trade partners quickly responded. By mid-February, several countries that had been taxed early announced countermeasures. Canada, unable to successfully negotiate a delay on U.S. tariffs, decided to impose a 25% tariff on all U.S. imports. China also responded early and escalated on April 4, announcing a 34% tariff on all U.S. imports.

With the implementation of "reciprocal" tariffs and escalating trade tensions, more countries are expected to introduce their own countermeasures. The EU has clearly stated it will respond soon, and several other major economies have also developed relevant counterattack plans. While the full extent of the global response remains unclear, all signs currently indicate that a broad trade war involving multiple fronts is forming.

Chart 1: The "Liberation Day" tariffs on April 2, 2025, cover up to 60 countries, including several of the U.S.'s major trading partners.

Source: BBC, X (@WhiteHouse), Binance Research, as of April 3, 2025

Note: This table reflects the "reciprocal" tariffs imposed by the U.S. on its top ten sources of imports as of April 2.

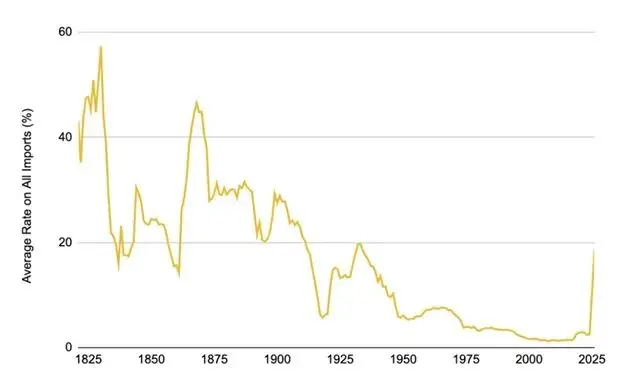

These policies have caused U.S. import tax rates to soar to their highest level since the implementation of the Smoot-Hawley Tariff Act in 1930, which imposed comprehensive tariffs on thousands of goods during the Great Depression. According to existing data, the average U.S. tariff rate has risen to about 18.8%, with some estimates even reaching 22%—a dramatic leap compared to 2.5% in 2024.

For reference, the average U.S. tariff rate has typically remained between 1-2% over the past few decades; even during the U.S.-China trade frictions from 2018 to 2019, it only rose to around 3%. Therefore, the measures in 2025 represent an unprecedented tariff shock in modern history—almost equivalent to a return to the protectionism of the 1930s.

Chart 2: The resurgence of U.S. tariffs has raised import tax rates to their highest level in nearly a century.

Source: Tax Foundation, Binance Research, as of April 3, 2025

Market Impact: Cooling Demand, Risk Aversion, and Soaring Volatility

1. Cooling Demand and Rising Risk Aversion

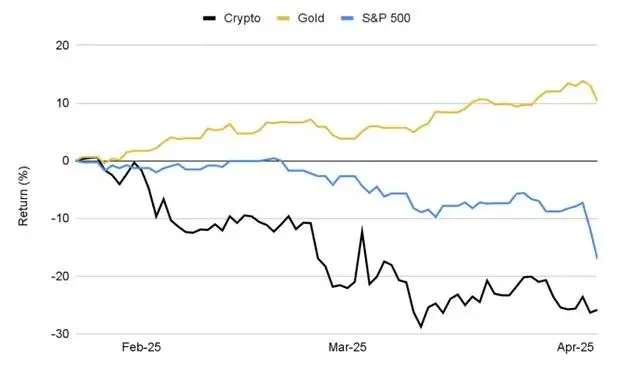

Market sentiment has clearly turned cautious, with investors exhibiting typical "risk-averse" behavior in response to the tariff announcements. The total market capitalization of the cryptocurrency market has dropped by about 25.9% from its January peak, evaporating nearly $1 trillion in market value, highlighting its high sensitivity to macroeconomic instability.

Cryptocurrency assets have moved in close alignment with the stock market, both facing cooling demand, widespread sell-offs, and entering correction territory. In contrast, traditional safe-haven assets like bonds and gold have performed well, with gold continuously reaching historical highs, becoming a refuge for investors amid rising macro uncertainty.

Chart 3: Since the initial tariff announcement, the cryptocurrency market has fallen 25.9%, the S&P 500 index has dropped 17.1%, while gold has risen 10.3%, continuously reaching historical highs.

Source: Investing.com, CoinGecko, Binance Research, as of April 4, 2025

The severe market reaction also highlights the characteristics of cryptocurrency assets during periods of intense "risk aversion": Bitcoin (BTC) fell by 19.1%, with most mainstream altcoins experiencing declines comparable to or even greater than that. Ethereum (ETH) saw a drop of over 40%, while high-beta sectors (such as meme coins and AI-related tokens) plummeted by over 50%. This round of sell-off erased most of the gains in the cryptocurrency market since the beginning of the year; as of early April, even BTC's year-to-date (YTD) returns have turned negative—despite its strong performance in 2024.

Chart 4: Under the macro panic triggered by tariffs, altcoins have seen significantly larger declines than Bitcoin, exacerbating market pessimism.

Source: CoinGecko, Binance Research, as of April 4, 2025

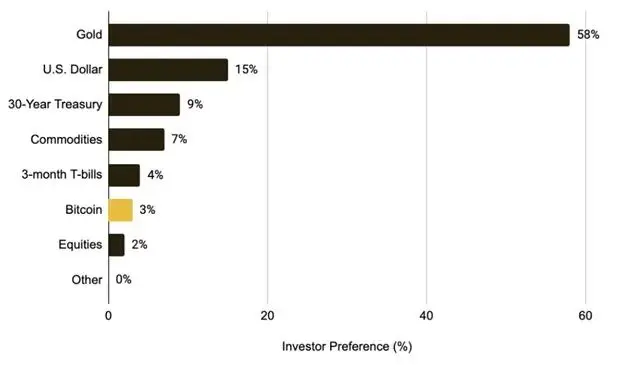

As the cryptocurrency market increasingly exhibits characteristics of a risk asset, if the trade war continues, it may further suppress capital inflows and dampen demand for digital assets in the short term. Funds may continue to remain on the sidelines or shift to gold and other assets perceived as safer. This sentiment is also reflected in a recent fund manager survey, where only 3% of respondents indicated they would allocate to Bitcoin in the current environment, while 58% preferred gold.

Chart 5: Only 3% of global fund managers view Bitcoin as the preferred asset class in the context of a trade war.

Source: BofA Global Fund Manager Survey, Binance Research, as of February 2025

2. Soaring Volatility

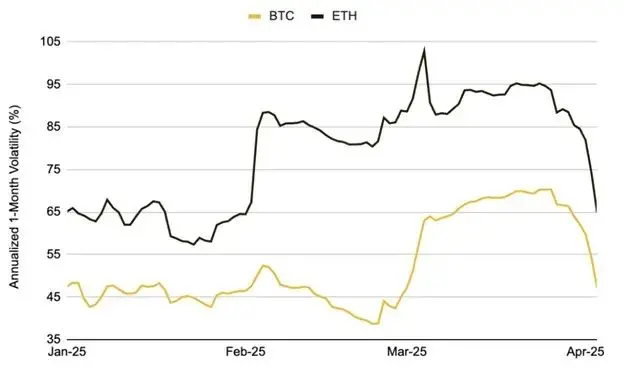

The market's sensitivity to tariff policies is evident, with each major announcement triggering significant price fluctuations. Over the past few months, BTC has experienced multiple large price swings—one of which was among the largest single-day declines since the COVID-19 crash in 2020. At the end of February 2025, when Trump suddenly announced plans to impose tariffs on Canada and the EU, BTC dropped by about 15% in the following days, while its actual volatility surged significantly. ETH exhibited a similar trend, with its one-month volatility soaring from around 50% to over 100%.

These market behaviors underscore the cryptocurrency market's extreme sensitivity to sudden policy changes in the current high-uncertainty macro environment. In the near term, if policy directions remain unclear or the trade war escalates further, the market will likely maintain high volatility. Historical experience also indicates that volatility may only gradually decrease once the market fully digests and prices in the new tariff policies.

Chart 6: During this phase, BTC's one-month actual volatility rose above 70%, while ETH exceeded 100%, reflecting the severe market fluctuations following the tariff announcements.

Source: Glassnode, Binance Research, as of April 4, 2025

Macroeconomic Impact: Inflation, Stagflation Concerns, Interest Rates, and Federal Reserve Outlook

1. Inflation and Stagflation Concerns

The new tariffs effectively impose a large amount of additional taxes on imported goods, exacerbating inflationary pressures at a time when the Federal Reserve is trying to suppress price growth. Concerns have emerged in the market that these measures could disrupt the process of inflation decline. Market indicators such as one-year inflation swaps have surged above 3%, while expectations in consumer surveys have risen to around 5%, indicating a widespread belief that prices will continue to rise over the next 12 months.

Meanwhile, economists warn that if the trade war escalates fully and triggers a global retaliatory response, the loss of global economic output could reach $1.4 trillion. U.S. per capita real GDP is expected to decline by nearly 1% initially. Fitch Ratings noted that if a comprehensive tariff regime persists, most economies may enter recession, stating that "the current high level of U.S. tariffs has rendered most economic forecasting models ineffective."

Amid rising inflation expectations and growth concerns, the risk of the global economy slipping into stagflation (a combination of economic stagnation and rising prices) is increasingly prominent.

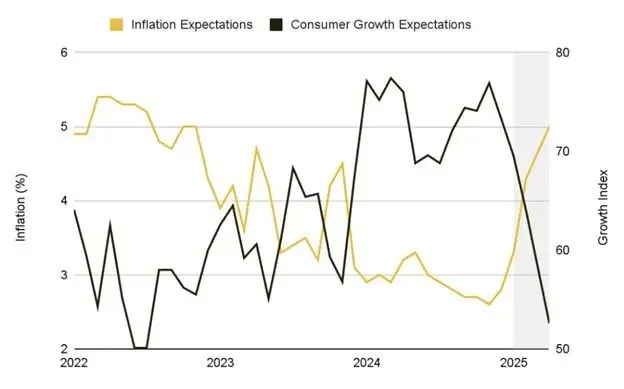

Chart 7: Changes in macro conditions in 2025 drive one-year expected inflation upward while growth expectations decline.

Source: University of Michigan, Binance Research, as of April 5, 2025

2. Interest Rate Outlook and Federal Reserve Stance

Federal funds futures data indicate that market expectations for interest rate cuts in the coming months have risen significantly. This marks a clear shift in attitude—just a few weeks ago, the Federal Reserve was firmly committed to curbing inflation, but now, due to growing concerns about economic growth prospects, the market has begun to anticipate a potential shift towards easing monetary policy to support the economy.

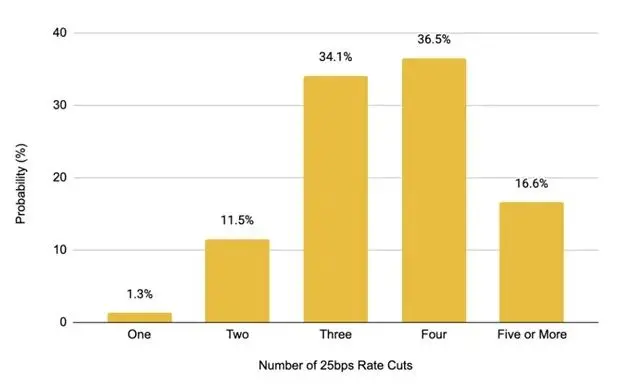

Chart 8: Market expectations for interest rate cuts in 2025 continue to rise, with current expectations of four 25 basis point cuts—far higher than the previous expectation of just one cut.

Source: CME Group, Binance Research, as of April 4, 2025

This shift in sentiment is reflected in the public statements of Federal Reserve officials. They have expressed concerns, emphasizing that the new round of tariffs is contrary to previous economic policy guidelines. The Federal Reserve now faces a difficult choice: to tolerate the additional inflation brought on by tariffs or to maintain a hawkish stance, risking further suppression of growth?

"The scale of tariffs announced in recent weeks has exceeded expectations, and their impact on inflation and growth—especially the cumulative effect—needs to be closely monitored."

— Jerome Powell, April 4, 2025

In the short term, the Federal Reserve seems committed to maintaining stable long-term inflation expectations. However, monetary policy decisions will continue to rely on data, depending on which signal—inflation or growth—appears weaker. If inflation significantly exceeds targets, the stagflation environment may limit the Federal Reserve's ability to respond. This uncertain policy outlook also exacerbates market volatility.

Outlook

1. Correlation and Diversification Allocation

The evolving relationship between cryptocurrency assets and traditional markets is becoming a focal point—Bitcoin, as the dominant asset in the market, serves as the best window to observe this change. The "risk aversion" event triggered by the trade war has significantly affected the correlation structure between BTC and the stock market as well as traditional safe-haven assets.

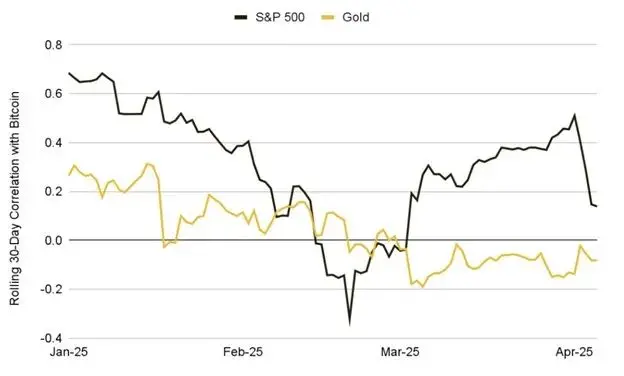

Since the first mention of tariffs on January 23, the initial market response was inconsistent—Bitcoin's movements were somewhat independent of stocks, causing their 30-day correlation to drop to –0.32 on February 20. However, as trade war rhetoric escalated and risk aversion sentiment spread, this value rose to 0.47 in March, indicating an increased short-term linkage between Bitcoin and overall risk assets.

In contrast, the correlation between Bitcoin and traditional safe-haven assets like gold has significantly weakened—what was previously a neutral to positive relationship turned into a negative correlation of –0.22 by early April.

These changes indicate that macroeconomic factors, particularly trade policy and interest rate expectations, are increasingly dominating cryptocurrency market behavior, temporarily suppressing the market structure that was originally driven by supply and demand logic. Observing whether this correlation structure persists will help understand Bitcoin's long-term positioning and its diversification value.

Chart 9: Initial responses were mixed; as the trade war escalated, BTC's linkage with the S&P 500 strengthened, while its correlation with gold continued to weaken.

Source: Investing.com, Binance Research, as of April 5, 2025

2. Reestablishing the Safe-Haven Asset Narrative

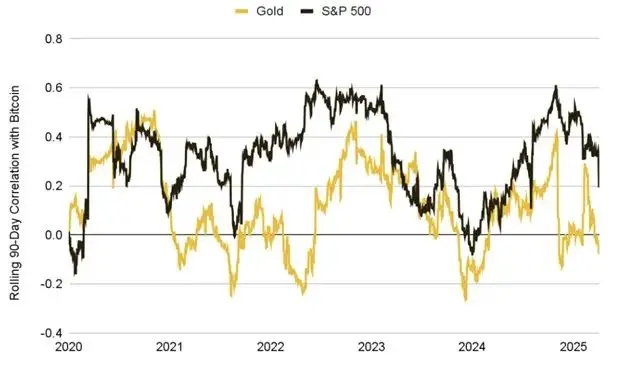

Despite recent macro and liquidity shocks highlighting the "risk attributes" of cryptocurrency assets, the long-term trend remains unchanged: Bitcoin's correlation with traditional markets typically rises under extreme stress but gradually declines as the market stabilizes. Since 2020, the 90-day average correlation between BTC and the stock market has been about 0.32, while with gold it has only been 0.12, indicating that it has maintained a certain separation from traditional asset classes.

Even in the wake of the recent tariff announcements, BTC has shown some resilience on days when certain traditional risk assets weakened. At the same time, the supply held by long-term holders continues to rise—indicating that core holders have not significantly reduced their positions amid recent volatility, but rather show strong confidence.

This behavior suggests that despite increased short-term price volatility, Bitcoin may reestablish a more independent macro identity.

Chart 10: Since 2020, the long-term correlation between Bitcoin and traditional assets has remained moderate: 0.32 with the S&P 500 and 0.12 with gold.

Source: Investing.com, Binance Research, as of April 5, 2025

The key question is whether BTC can return to a long-term structure of low correlation with the stock market. A similar trend was observed during the banking turmoil in March 2023, when BTC successfully decoupled and strengthened amid a stock market downturn.

Now, as the trade war intensifies and global markets begin to adapt to a long-term fragmented trade landscape, whether Bitcoin can once again be viewed as a "sovereign-free, permissionless" safe-haven asset will determine its future macro role. Market participants will closely monitor whether BTC can retain this independent value proposition.

One potential path is to regain its appeal during periods of currency inflation and fiat currency depreciation, especially as the Federal Reserve shifts towards easing. If the Federal Reserve begins to cut rates while inflation remains high, Bitcoin may regain favor as a "hard asset" or inflation hedge.

Ultimately, this process will determine BTC's long-term positioning as an asset class—and its diversification utility within investment portfolios. This also applies to other mainstream altcoins, which exhibit stronger risk attributes in the current environment and may continue to rely on BTC-driven market sentiment.

3. The Cryptocurrency Market in a Stagflation and Protectionist World

Looking ahead, the cryptocurrency market will face a complex macro environment dominated by trade policy risks, stagflation pressures, and a breakdown of global coordination. If global growth continues to weaken and the cryptocurrency market fails to establish a clear narrative, investor sentiment may further decline.

A prolonged trade war will test the resilience of the entire industry—potentially leading to a depletion of retail capital, a slowdown in institutional allocations, and reduced venture capital financing. Key macro variables to closely monitor in the coming months include:

· Trade Dynamics: Any new tariff lists, unexpected easing measures, or significant bilateral changes (such as U.S.-China negotiations or further escalations) will directly impact market sentiment and inflation expectations.

· Core Inflation Data: Upcoming CPI and PCE data are crucial. If they unexpectedly rise due to import cost pressures, stagflation concerns will intensify; if the data is weak, it may alleviate central bank pressure and enhance the appeal of risk assets (including cryptocurrencies).

· Global Growth Indicators: Declining consumer confidence, slowing business activity (PMI), a weak labor market (rising unemployment claims, slowing non-farm employment), corporate earnings warnings, and an inverted yield curve (a common recession signal) may further trigger risk aversion in the short term. However, if macro weakness accelerates expectations for monetary easing, it could also provide support for the cryptocurrency market.

· Central Bank Policy Path: How the Federal Reserve and other major central banks seek to balance inflation and recession will determine liquidity across various assets. If they refuse to cut rates against a backdrop of slowing growth, risk assets will continue to be pressured; if they shift towards easing, it could lead to a broad uplift. If real interest rates decline (whether due to policy or persistent inflation), long-duration assets like Bitcoin may benefit. Divergence in central bank policies (e.g., the Federal Reserve turning dovish while the European Central Bank remains hawkish) could also trigger cross-border capital flows, further exacerbating volatility in the cryptocurrency market.

· Cryptocurrency-Specific Policy Events: Approvals for ETFs, strategic BTC reserves, and key legislative advancements may become independent catalysts in the current macro context, potentially breaking the "macro binding" state of cryptocurrency assets and re-emphasizing their uniqueness. However, one should also be wary of reverse risks, such as regulatory delays or unfavorable litigation developments, which could produce negative feedback.

Conclusion

The most aggressive round of tariff policies since the 1930s is having a profound impact on the macro economy and the cryptocurrency market. In the short term, the cryptocurrency market may continue to exhibit high volatility, with investor sentiment swinging in response to trade war news.

If inflation remains high while growth slows, the Federal Reserve's response will become a critical turning point: if it shifts towards easing, the cryptocurrency market may rebound due to rising liquidity; if it maintains a hawkish stance, pressure on risk assets will persist.

If the macro environment stabilizes and a new narrative emerges, or if cryptocurrency assets regain their long-term safe-haven status, the market may be poised for recovery. Until then, the market is likely to maintain a volatile pattern and remain highly sensitive to macro news. Investors need to closely monitor global dynamics, maintain diversified asset allocations, and seek opportunities amid potential market dislocations brought about by the trade war.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。