How Whales Utilize $XPL in Hyperliquid Pre-Launch Trading: Timing, Location, and Expertise of Harvesting Masters—Early Holders Hedge by Shorting, Creating "Crowded Trades," Ultimately Triggered by "Ignition Strategies"—This is Not a Coincidental Market Fluctuation, but a Systemic Risk Arising from Structural Defects in the Pre-Launch Market.

The story begins with a tweet from AI Aunt:

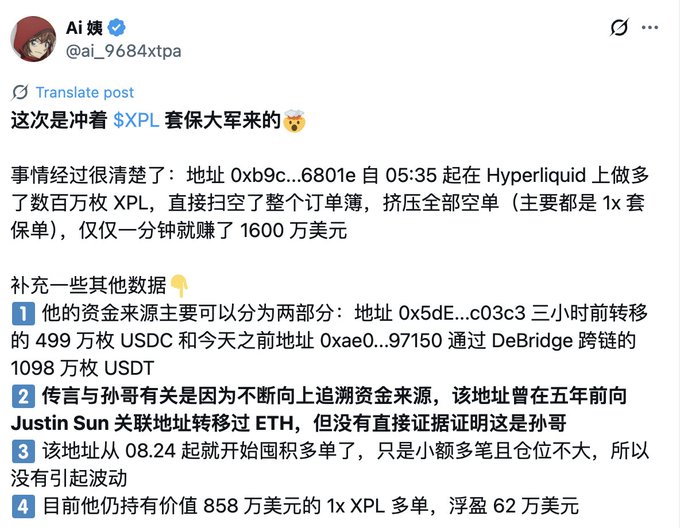

Original text:

https://x.com/ai_9684xtpa/status/1960506447965642864

This article does not evaluate the ins and outs of the XPL incident but aims to discuss some structural and systemic risk points in the "pre-launch trading market." Where there are advantages in a model, there are also disadvantages. This matter is not about right or wrong; the purpose of this article is to point out the risk points and their causes.

Section 1: A New Paradigm: Pre-Launch Trading

Pre-launch trading (more accurately, "Pre-Launch Trading") is fundamentally about creating a synthetic market for a token that has not yet been issued or publicly circulated. This is not a reflection of existing asset information but a pure price discovery process for future assets. The trading subject is not the token itself but a type of futures, with some platforms offering spot trading, others forward OTC, and others perpetual contracts.

This shift in mechanism fundamentally changes the nature of risk. The main risks of traditional pre-launch trading are insufficient liquidity and increased volatility, but the existence and fundamental value of the asset are indisputable. The cryptocurrency pre-launch market introduces new dimensions of risk: first, settlement risk or conversion risk, meaning that the project may never issue the token, leading to the market's inability to convert into a standard spot or perpetual contract market, which may ultimately be suspended or delisted.

Secondly, there is price anchoring risk. Without an external spot market as a price reference, market prices are entirely determined by internal buy and sell actions on the platform, forming a self-referential closed loop, making the market more susceptible to manipulation. Therefore, the innovation of cryptocurrency pre-launch trading lies in the creation of a market out of thin air, but at the cost of constructing a structurally weaker and more diverse risk environment.

It's not that everyone is unaware of this risk, but exchanges can gain traffic, market makers can achieve "price discovery" in advance, and project parties/early investors can "hedge risks"—under the premise of multiple parties profiting, everyone tacitly accepts this arrangement (risk).

Section 2: DEX Hedging is a Double-Edged Sword Played Blindfolded

2.1 Rational Hedgers: Why Early Holders Short Pre-Launch Futures to Lock in Value

Before the Token Generation Event (TGE) of a new token, early holders (including private investors, team members, airdrop recipients, etc.) face a common dilemma: they hold tokens or token entitlements that are not yet circulating and cannot be traded, but the value of these future assets is exposed to significant market uncertainty. Once the token is launched for trading, its price may be far below expectations, leading to a substantial reduction in paper wealth.

The pre-launch futures market provides an almost perfect solution to this dilemma. By shorting an equivalent amount of perpetual contracts in the pre-launch market, holders can lock in their future token selling price in advance. For example, an airdrop user expected to receive 10,000 tokens, if the futures price of the token in the pre-launch market is $3, can hedge the risk by shorting 10,000 contracts. Regardless of the spot price at TGE, their total profit will be locked in at about $30,000 (ignoring transaction costs and basis). The essence of this operation is to construct a delta-neutral position: the risk of their spot long (the airdrop they hold) is offset by their futures short (the short perpetual contracts). For any rational risk-averse individual, this is a standard and wise financial operation.

2.2 Formation of Crowded Trades: When Collective Hedging Creates Concentrated Vulnerability

When a large number of market participants trade based on similar logic, at the same time, and using the same strategy, "crowded trades" emerge. This risk does not stem from the asset's fundamentals (exogenous risk) but from the high correlation of market participants' behaviors, representing an endogenous risk.

If you have seen the ALPACA episode before, you know this operation is a "market consensus"—where there is market consensus, there is direction; where there is direction, there is opportunity; where there is opportunity, there is speculation.

In the pre-launch market, this crowding phenomenon is structural and predictable. The nature of airdrops and early token distributions determines that there will be a large, homogeneous group (i.e., token recipients) facing identical risk exposures at the same time (before TGE) and having the same hedging motivation (shorting). Meanwhile, the group of speculators willing to take risks and buy these futures contracts is relatively small and dispersed. This natural long-short imbalance inevitably leads to extreme crowding in the short direction, forming a typical crowded short.

The greatest danger of crowded trades lies in their vulnerability. Since the vast majority of participants are on the same side of the boat, once a catalyst emerges that forces them to close their positions (e.g., a reverse price movement), there will be insufficient counterparties in the market to absorb these liquidation orders. This will trigger a "stampede" to "exit," leading to extreme and violent one-way price movements. For crowded short positions, this stampede manifests as a devastating short squeeze. This originally risk management tool, due to its collective use, instead creates a new, larger systemic risk point.

2.3 Identifying Imbalance: Detecting Crowded Conditions Through Data Analysis

While individual traders cannot know exactly how many others hold the same position, analyzing public market data can effectively identify signs of crowded trading.

Open Interest (OI) Analysis: OI is a key indicator measuring the total number of outstanding derivative contracts in the market, reflecting the total amount of funds flowing into the market and market participation. In the pre-launch market, if OI continues to rise rapidly while prices stagnate or even slightly decline, this is a strong signal indicating that a large amount of capital is flowing into short positions, forming a bearish consensus, i.e., a crowded short is forming.

On-Chain Data Analysis: Although the tokens are not yet circulating, analysts can track activities related to airdrops through blockchain explorers. By analyzing the number of wallets eligible for airdrops, the concentration of token distribution, and the historical behavior of these wallets, one can roughly estimate the total amount of "spot" positions that may need to be hedged. A large-scale and dispersed airdrop often indicates stronger hedging demand and higher crowding risk.

Funding Rates and Spreads: On platforms like Hyperliquid that have funding rates, a continuously negative and deepening funding rate is direct evidence of short dominance. On platforms like Aevo, although there are no funding rates, a continuously widening bid-ask spread and a sell-side order book depth far exceeding the buy-side can also reflect unilateral selling pressure.

This series of analyses reveals a profound phenomenon: the "crowded hedging" in the pre-launch market is not an accident of market failure but an inevitable product of systemic design. The airdrop mechanism creates a large and uniformly motivated group, while the pre-launch market provides them with the perfect hedging tool. Individual rational behavior (hedging risk) aggregates into a collective irrational state (an extremely vulnerable crowded position). This vulnerability is predictable, systematically concentrating a large number of risk-averse traders, creating a perfect prey pool for those who understand and can exploit this structural defect.

Short squeezes do not require reasons, narratives, or uses; rather, when capital reaches a certain level, it attracts whales and speculation—contract versions of "having a gem brings trouble."

Section 3: Ignition Moment: Utilizing Crowded Trades to Trigger Chain Liquidations

3.1 Momentum Ignition: A Mechanism of a Predatory Trading Strategy

Momentum Ignition is a complex market manipulation strategy typically executed by high-frequency traders or large trading funds. Its core objective is not based on fundamental analysis but rather to artificially create one-way price momentum through a series of rapid, aggressive trades, aiming to trigger preset stop-loss or forced liquidation lines in the market, and then profit from the resulting chain reaction.

The execution of this strategy usually follows a precise "attack sequence":

Detection and Preparation: The attacker first submits a series of small, rapid orders to test the market's liquidity depth and create the illusion of increasing demand.

Aggressive Ordering: Upon confirming insufficient market depth, the attacker will rapidly impact the sell side of the order book with a large number of market buy orders. The goal at this stage is to quickly and violently push up the price.

Triggering Chain Reactions: The sharp price increase will hit the forced liquidation prices of many crowded short positions. Once the first liquidation is triggered, the exchange's risk engine will automatically execute market buy orders to close that short position, further pushing up the price.

Harvesting Profits: The initial attacker, having established a large number of long positions in the first two stages, will begin to reverse their operations as the chain liquidations start, selling their long positions to these forced liquidation buyers, thus realizing profits at the artificially inflated prices they created.

3.2 Perfect Prey: How Illiquidity and Crowded Shorts Create an Ideal Attack Environment

The pre-launch market provides an almost perfect breeding ground for the implementation of momentum ignition strategies.

Extremely Low Liquidity: As mentioned earlier, the liquidity in the pre-launch market is extremely scarce. This means that attackers can exert a significant impact on prices with relatively little capital. Manipulative actions that may be costly in mature markets with ample liquidity become inexpensive and efficient in the pre-launch market.

Predictable Liquidation Clusters: Due to a large number of hedgers adopting similar entry prices and leverage ratios, their forced liquidation prices are densely distributed within a narrow range above the market price. This creates a clear, predictable "liquidation cluster." Attackers are well aware that they only need to push the price into this area to trigger the entire chain reaction. This aligns with the logic of "hunting stop losses" in traditional markets, where attackers specifically target known clusters of stop-loss orders (via liquidation maps).

Unilateral Market Structure: Crowded shorts mean that during price increases, there is almost no natural buying power to absorb the selling pressure from attackers. Prices can effortlessly rise until they hit the "wall" of the liquidation cluster. Once they hit it, the passive liquidation buying pressure becomes the "fuel" driving prices further up.

3.3 Collapse: From Targeted Liquidations to Widespread Chain Liquidations

The entire process is a meticulously planned, phased collapse.

Short Squeeze: The initial price surge triggered by the momentum ignition strategy first forces the liquidation of the most leveraged and vulnerable short positions. The buying pressure generated by these forced liquidations further drives up the price, creating a typical short squeeze market.

Chain Liquidations: The price, elevated by the first round of short squeezes, now reaches the liquidation lines of the second and third batches of short positions. This creates a vicious positive feedback loop: liquidations lead to price increases, and rising prices trigger more liquidations. The market spirals out of control, with prices soaring vertically in a very short time, forming long upper shadows on charts, known as "liar candles."

Final Outcome: For early holders seeking to hedge, their outcome is "liquidation"—their margin is exhausted, and their hedging positions are forcibly closed, resulting in significant financial losses. They not only lose the "insurance" set up to protect the spot value but also pay a heavy price for it. Once the chain liquidations have exhausted all available short positions for liquidation, and the attackers have completed their profit harvesting, prices often quickly revert to their initial levels, leaving chaos in their wake.

From a deeper analysis, the momentum ignition strategy in the pre-launch market has transcended simple market manipulation; it is not market manipulation but rather a game between capital.

It is a structural arbitrage based on the microstructural flaws of the market. The attackers leverage publicly available information (the scale of airdrops), the platform's design (leverage mechanisms), and predictable group behavior (collective hedging) to execute a nearly deterministic game by calculating the attack costs (the capital required to push prices up in a low liquidity market) and potential profits (profits after triggering liquidation clusters). Their profits do not stem from accurate judgments of asset value but from the precise exploitation and amplification of market failures.

Understanding the phenomenon and the reasons behind it.

May we always maintain a sense of reverence for the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。