NVIDIA has fallen into a strange cycle where small beats expectations are seen as not meeting expectations.

Written by: Li Yuan

Source: Geek Park

On August 28, China time, NVIDIA released its Q2 fiscal report for 2026.

From a performance perspective, NVIDIA once again delivered an excellent report card:

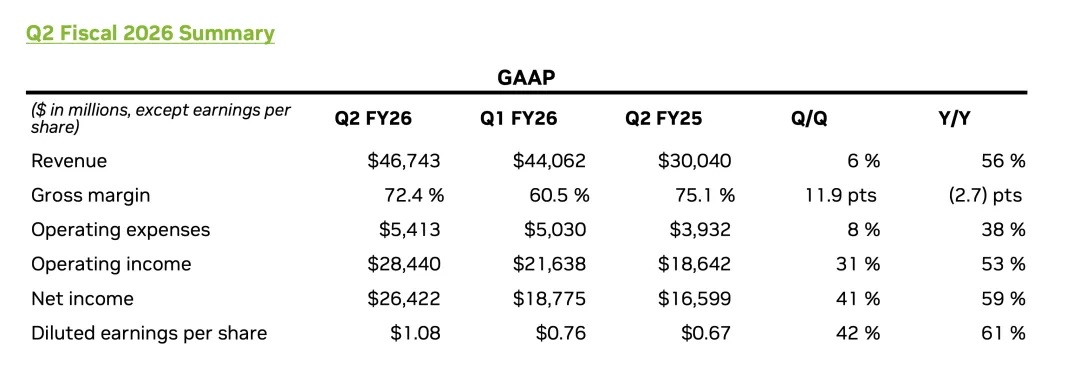

Q2 revenue reached $46.743 billion, a year-on-year increase of 56%, slightly higher than the market's previous expectation of $46.23 billion;

The data center business, as the core engine, set a new record with revenue of $41.1 billion, also a 56% year-on-year increase;

Adjusted earnings per share were $1.05, a 54% year-on-year increase, also exceeding expectations.

However, this seemingly perfect performance did not fully reassure Wall Street.

The market's reaction was direct and severe: NVIDIA's stock price fell more than 5% in after-hours trading, and by the end of the day, the decline narrowed to 3%, but the volatility itself indicated several issues.

NVIDIA is an extremely unique company in the current market: its core business revenue is heavily reliant on AI data center operations, and this massive and rapidly growing data center revenue is also highly concentrated among a few "whale" clients, such as large cloud service providers and top AI model research institutions represented by OpenAI.

This revenue structure means that NVIDIA's growth is deeply "bound" to the capital expenditures and AI strategies of these leading players. Any minor fluctuations from them will directly impact NVIDIA's performance and market expectations. NVIDIA's stock price is no longer a simple reflection of its own performance but rather a barometer of confidence in the entire AI market.

Moreover, its extremely high valuation has already overdrawn the dream of "AI soaring to new heights," and the market has fallen into a strange cycle where "small beats expectations are seen as not meeting expectations," with only crushing "big beats" able to drive an increase.

A deeper anxiety lies in the fact that the capital market's fundamental questioning of AI has never ceased: Is this revolution driven by computing power still in the stage of needing high investment for early layout, or has it nearly reached the "cost reduction and efficiency increase" accounting logic? No one knows the answer, but everyone fears the party could end at any moment.

At the same time, the uncertainties in the Chinese market have intensified this uncertainty. The financial report shows that NVIDIA did not sell H20 chips to China in Q2, and the revenue outlook for Q3 does not include related income. Although Jensen Huang expressed long-term optimism about the Chinese market during the earnings call, believing that "the possibility of introducing Blackwell to the Chinese market is real," and estimating that the opportunity size in the Chinese market this year could reach $50 billion, the short-term revenue gap is very real.

As the manager of this world-leading company, Jensen Huang is confident: he has painted an extremely grand vision for the future of NVIDIA and the entire AI industry. During the earnings call, he clearly predicted that by the end of this decade, global annual spending on AI infrastructure will reach $3 trillion to $4 trillion. He sees not just a quarter's worth of orders but a decade-long new industrial revolution driven by AI.

His confidence is also reflected in the fact that NVIDIA has returned $10 billion to shareholders this quarter and announced a new stock buyback authorization of up to $60 billion.

The expected growth for the next quarter is also substantial: the revenue guidance of $54 billion for Q3 means the company will create an astonishing incremental revenue of over $9.3 billion in just three months.

This guidance, while slightly above Wall Street's consensus expectations, is far below some optimistic analysts' expectations of up to $60 billion. This market's perpetual expectation for "soaring" greed, intertwined with fears of slowing growth and external risks, is the most significant challenge NVIDIA faces going forward.

01 Future of Data Center Business: Chip Transition Relay + Agent AI

As the absolute core of NVIDIA's empire, the performance of the data center business this quarter perfectly illustrates the subtle gap between "excellence" and "market expectations."

From the data, the growth story continues.

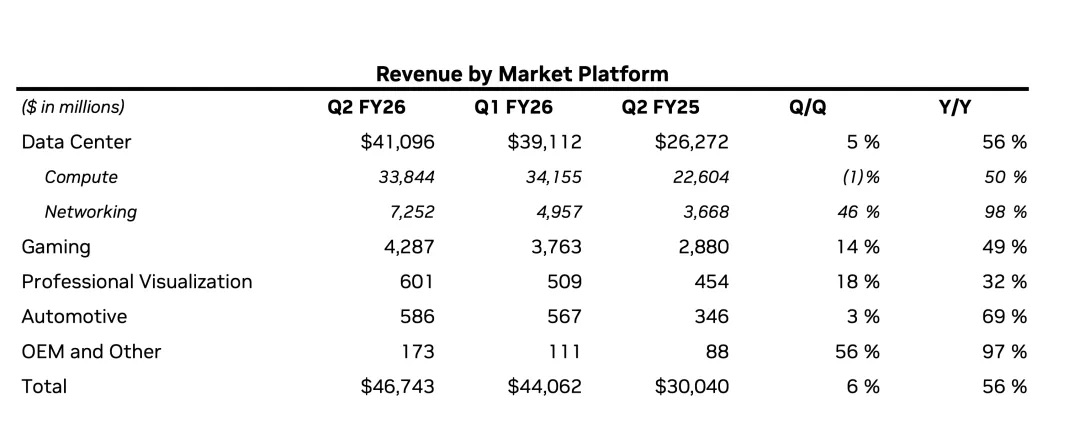

Overall revenue reached a new high: total revenue from the data center business was $41.1 billion, a year-on-year increase of 56% and a quarter-on-quarter increase of 5%.

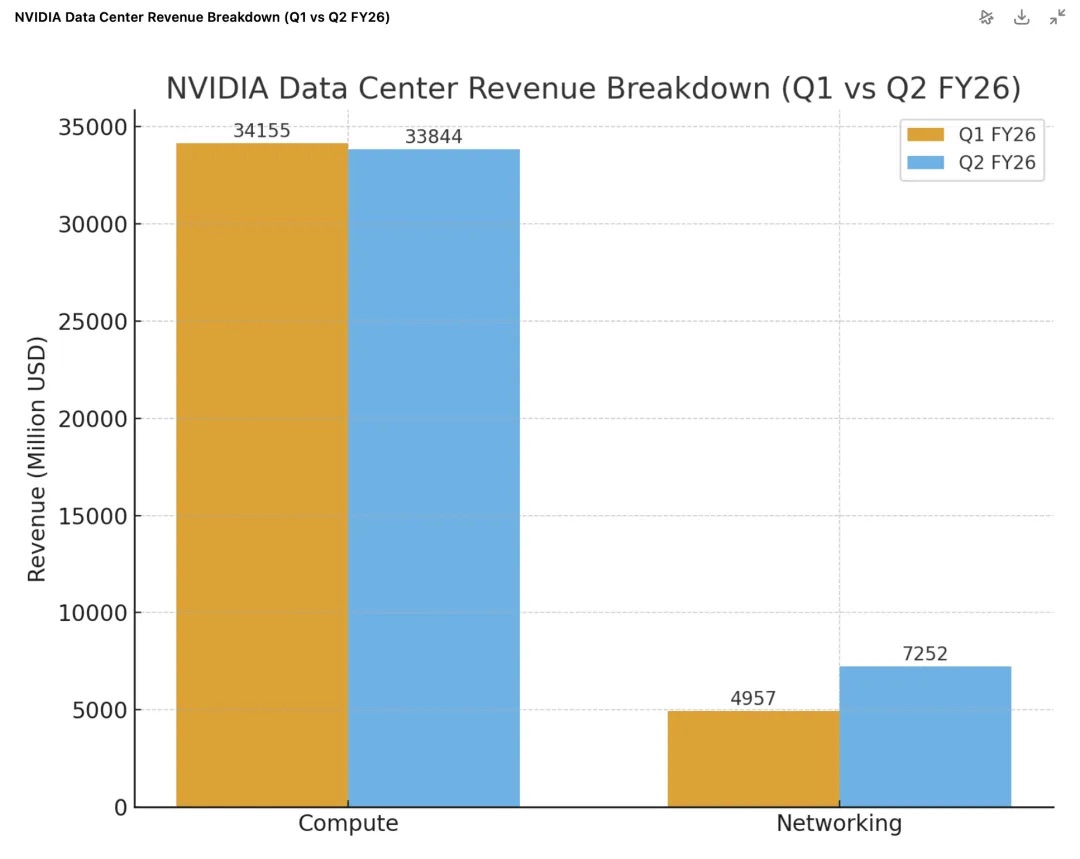

Blackwell engine fully launched: The new generation of Blackwell architecture products began to ramp up strongly, with data center-related revenue soaring 17% quarter-on-quarter. The flagship product GB300 has entered full production, reaching a production rate of about 1,000 racks per week. The Blackwell Ultra platform has already become a "multi-billion dollar" product line this quarter, showing extreme market demand for the new architecture.

Networking business becomes the "second engine": This quarter, the networking business performed exceptionally well, with revenue reaching $7.3 billion, a year-on-year increase of 98% and a quarter-on-quarter increase of 46%. Among them, the AI-optimized Spectrum-X Ethernet business has annualized revenue exceeding $10 billion.

Emerging markets are rapidly rising: "Sovereign AI" is becoming a significant growth point, with NVIDIA expecting revenue in this area to exceed $2 billion this year, more than double last year's figure.

However, under the market's magnifying glass, this report card also shows "flaws" that make investors uneasy. First, the $41.1 billion revenue was slightly below the market's previous expectation of $41.3 billion. However, this decline was mainly due to a $4 billion reduction in revenue from H20 chip sales to China, consistent with the situation that emerged in Q1.

Fortunately, the explosive growth of the networking business has become a key highlight to offset GPU pressure. This quarter, networking business revenue reached $7.3 billion, a year-on-year increase of 98% and a quarter-on-quarter increase of 46%. This was mainly due to the hot sales of high-performance networking products such as NVLink and InfiniBand, which are tied to the Blackwell platform. This data clearly indicates that NVIDIA's success is no longer about selling standalone GPUs but rather selling a complete set of high-profit "AI factory solutions" that include high-speed interconnect networks.

The core question behind the data is what the market is most concerned about: Can NVIDIA maintain high-speed growth on such a large scale?

In the current market landscape, this is hardly a question of "competition." Jensen Huang clearly stated during the earnings call that due to the rapid iteration of AI models and the extreme complexity of the technology stack, the general-purpose, full-stack NVIDIA platform has a significant advantage over dedicated ASIC chips, so external competitive pressure is not fatal.

Jensen Huang also emphasized the current core bottleneck in data center construction—power. When power becomes the core constraint on data center revenue, "performance per watt" directly determines the profitability of the data center. This explains why customers are willing and must continuously purchase NVIDIA's latest and most expensive chips at an annual pace. Each new architecture generation (from Hopper to Blackwell to Rubin) has made significant leaps in "performance per watt," making the purchase of new chips essentially a direct investment in the "revenue ceiling" under their limited power resources.

The real pressure comes from the natural law of AI development—can AI development be sustained?

In response, Jensen Huang provided his answer: reasoning agent AI.

He stated during the earnings call:

"In the past, the interaction model of chatbots was 'single-trigger'—you give a command, and it generates an answer; now, AI can autonomously conduct research, think, and formulate plans, even calling tools. This process is called 'deep thinking'… Compared to the 'single-trigger' model, the computing power required for reasoning agent AI models may reach 100 times or 1,000 times."

The core logic of this statement is: As AI evolves from a simple "question-and-answer tool" to an "agent" capable of independently completing complex tasks, the computing power required behind it will explode exponentially.

For investors, NVIDIA's data center business story is already very clear and layered: current growth is firmly passed on by the Blackwell platform; the next generation of growth is already on the way—Jensen Huang clearly announced during the earnings call that the six new chips of the next-generation platform Rubin have all completed tape-out at TSMC and have entered the wafer manufacturing stage, preparing for mass production next year as planned.

The ultimate fuel driving all this sustainable growth rests entirely on whether the market believes that the "Agent AI" era will indeed arrive as predicted and create endless demand for computing power.

02 Regarding China: Geopolitical Influences Continue

During the earnings call, Jensen Huang reiterated his long-term confidence in the Chinese market, estimating that "China could bring the company $50 billion in opportunities this year, with a market growth rate of about 50%," and clearly expressed his desire to "sell updated chips to the Chinese market."

The blueprint is optimistic, but the reality on the financial report is stark.

As the core engine contributing over 88% of revenue, NVIDIA's data center business grew 56% year-on-year this quarter, but its $41.1 billion revenue was slightly below analysts' expectations of $41.29 billion. This marks the second consecutive quarter that this business has failed to meet Wall Street expectations.

The problem lies in the Chinese business. Further breaking down the data center business reveals that its core GPU computing chips generated $33.8 billion in revenue, a quarter-on-quarter decline of 1%. The direct reason for this decline is that the H20 "special edition" chips for the Chinese market did not achieve any sales to China this quarter, resulting in a revenue gap of about $4 billion.

To understand this gap, one must review the policy changes over the past two quarters:

Q1: Policy "Emergency Brake"

In April this year, the U.S. government mandated that H20 chip exports to China require prior licensing, which almost instantly "stopped" NVIDIA's H20 in the Chinese market.

Faced with a large backlog of inventory and related contracts prepared for the Chinese market, the company had to write down a loss of $4.5 billion. At the same time, $2.5 billion in signed orders could not be fulfilled due to the new regulations.

Nevertheless, NVIDIA successfully shipped $4.6 billion worth of H20 chips to the Chinese market before the restrictions took full effect. This "last-minute" sale, although one-time, significantly boosted the revenue base for the computing business in Q1.

Q2: Revenue "Vacuum Period"

By the second quarter, sales of H20 to China had completely dropped to zero.

However, NVIDIA found some new customers outside of China and successfully sold $650 million worth of H20 inventory. With this batch sold, the company was able to reverse a previously set aside risk reserve of $180 million back into profits.

Overall, revenue related to H20 chips still sharply decreased by about $4 billion compared to the first quarter. This explains why the computing business saw a slight quarter-on-quarter decline of 1% in Q2—because it was being compared to a first quarter that included a "one-time" high revenue.

Currently, the U.S. government's export restrictions on AI chips remain unclear. The previous Trump administration had proposed requiring companies like NVIDIA and AMD to remit 15% of their chip sales revenue to China, but this policy has not yet been formalized into regulations.

Based on this uncertainty, NVIDIA adopted the most conservative stance in its official guidance—its revenue estimate of $54 billion for Q3 explicitly counts H20 revenue from China as zero. However, CFO Colette Kress also provided a statement with potential upside. She revealed that the company "is waiting for formal regulations from the White House," while also stating, "If the geopolitical environment allows, revenue from H20 chip shipments to China in Q3 could reach $2 billion to $5 billion."

Whether it can sell to the Chinese market, when it can sell, and what it can sell, completely does not depend on NVIDIA itself, but rather hangs in the balance of geopolitical factors.

03 Growth of Supporting Roles: Fast, but Hard to Support a Trillion-Dollar Valuation

When all the spotlight is on the data center business, it is easy to overlook the growth of NVIDIA's other business segments. In fact, if viewed separately, each of them has quite impressive report cards.

The gaming business is the most eye-catching supporting role this quarter.

This business achieved revenue of $4.3 billion, a year-on-year increase of 49% and a quarter-on-quarter growth of 14%, demonstrating strong recovery momentum.

The core driver of growth comes from new products: the GeForce RTX 5060, based on the Blackwell architecture, quickly became NVIDIA's fastest-selling x60 level GPU ever, proving its strong appeal in the consumer market.

The professional visualization and automotive robotics businesses are sowing seeds for the future.

The professional visualization business generated $601 million in revenue, a year-on-year increase of 32%, with high-end RTX workstation GPUs increasingly being used in AI-driven workflows such as design, simulation, and industrial digital twins.

The automotive and robotics business generated $586 million in revenue, a year-on-year increase of 69%, with the most critical advancement being the official shipment of the DRIVE AGX Thor system-on-chip, regarded as the next-generation "supercomputer on wheels," marking the beginning of its commercial harvest in the automotive sector.

Additionally, this quarter, its next-generation robotic computing platform THOR was officially launched, achieving an "order of magnitude" improvement in AI performance and energy efficiency compared to previous products. Jensen Huang's logic here is that the demand for computing power in robotic applications for both the device and infrastructure (used for training and simulation in the Omniverse digital twin platform) will grow exponentially, becoming a significant driver of long-term demand for future data center platforms.

However, despite the impressive growth rates of these businesses, their scale is not even in the same order of magnitude compared to the data center business.

The gaming business's revenue of $4.3 billion is only one-tenth of the data center business. The combined revenue of the professional visualization and automotive robotics businesses is only about $1.2 billion, which, in the face of the $41.1 billion data center giant, can almost be considered "other income."

This leads to a clear conclusion: in the foreseeable future, NVIDIA does not have any "side business" that can grow into a "second growth curve" to rival the data center. They are healthy and important businesses that build a richer ecosystem for the company and explore the possibilities of AI in the terminal and physical world.

But for a giant that needs hundreds of billions in revenue to support its multi-trillion-dollar valuation, the current contributions of these businesses are far from sufficient to alleviate the market's "growth anxiety."

NVIDIA's stock price fate remains firmly tied to the "war chariot" of the data center.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。