Author: Lacie Zhang, Researcher at Bitget Wallet

Introduction: Asset Anxiety in the Era of Low Interest Rates

On September 17, Eastern Time, Federal Reserve Chairman Jerome Powell announced a 25 basis point reduction in the target range for the federal funds rate to 4.00%–4.25%. This decision not only confirmed the interest rate cut expectations that have formed since the end of last year but also reinforced the market consensus that the path for further rate cuts will remain open: the market generally predicts two more rate cuts this year, totaling 50 basis points.

Each interest rate decision by the Federal Reserve is based on a comprehensive assessment of the U.S. labor market and economic growth prospects, and its impact ripples through global capital markets. The start of this round of interest rate cuts officially signals that global investment is entering a "low interest rate era"—whether in bank savings, government bonds, or money market funds, the yield ceiling of traditional conservative investment products is being repeatedly lowered, and investors' anxiety over "asset scarcity" is growing.

Just as the yield curve of traditional finance continues to languish, stablecoin investment products in the Web3 world have entered the public eye with their "abnormal" high yields. These investment products based on dollar-pegged stablecoins offer annualized returns of 5% or even as high as 20%, whether in decentralized finance (DeFi) protocols or centralized digital asset platforms. This inevitably raises questions: as assets strictly pegged to the dollar, where do their interest rates come from? Is this astonishingly high yield a fleeting market bubble, or is it the rise of a disruptive investment model? The Bitget Wallet Research Institute will analyze layer by layer in this article, uncovering the operational logic behind these high yields and objectively assessing the opportunities and potential risks in this "new game."

I. "Demand Deposit" in the Digital World: Three Main Models of Stablecoin Investment

Before exploring the mainstream models, it is necessary to clarify the definition of "stablecoin investment." Simply put, "stablecoin investment" is the "bank deposit" of the digital world, where investors deposit stablecoins pegged 1:1 to the dollar (such as USDC, USDT) into specific platforms or protocols to earn interest. Its core goal is to provide holders with relatively considerable and predictable annual returns through on-chain or platform yield strategies while ensuring the stability of the principal's value, typically retaining high liquidity similar to demand deposits.

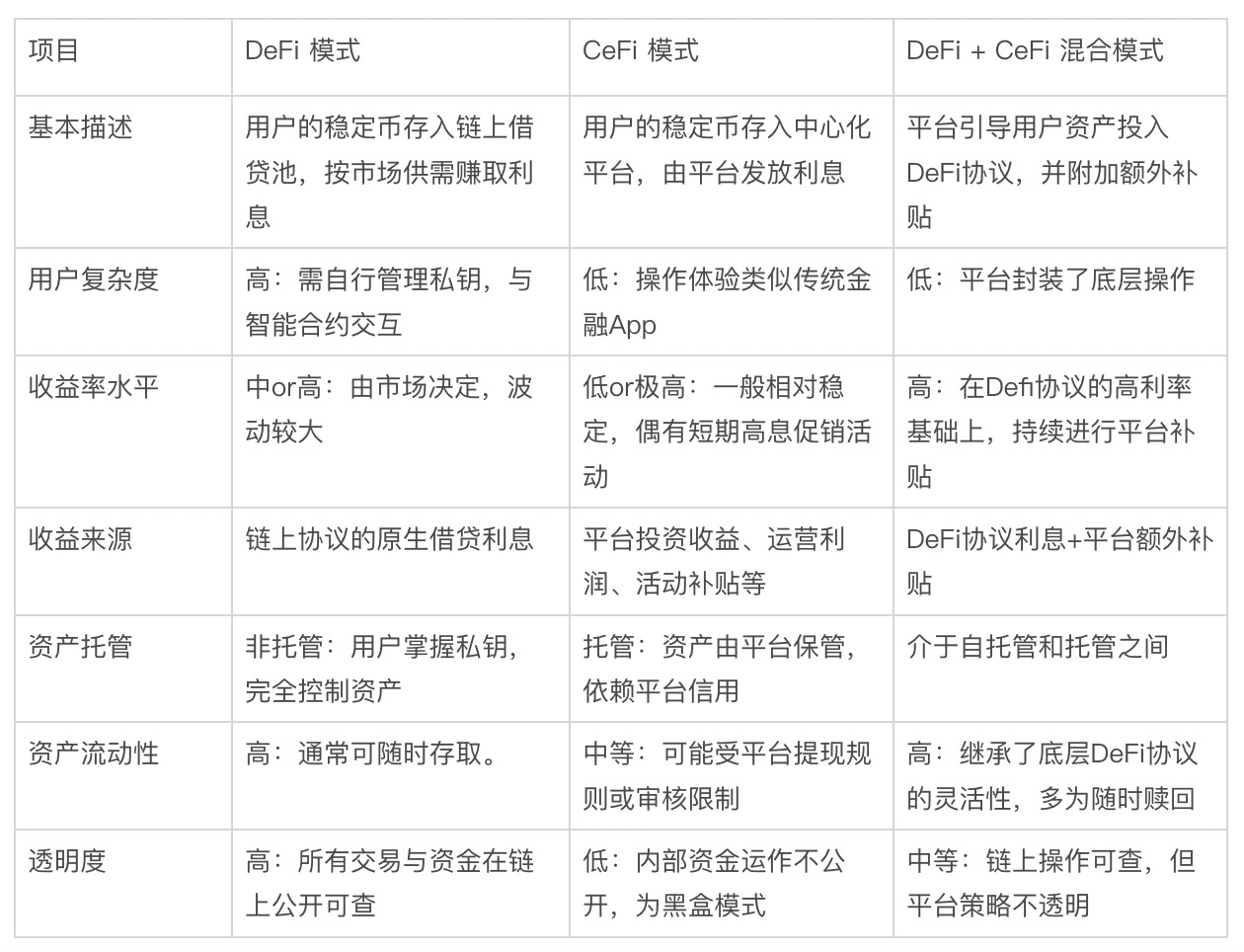

Currently, stablecoin investment products in the market can be mainly divided into three models based on their underlying operational logic and asset custody methods: DeFi Native Model, CeFi Custodial Model, and Hybrid Model Combining DeFi and CeFi.

Comparison Table of Mainstream Stablecoin Investment Models

- DeFi Native Model: Creating a completely transparent "on-chain bank." Users must manage their wallet private keys and interact directly with decentralized lending protocols like Aave and Compound, depositing stablecoins into on-chain liquidity pools to earn floating interest based on real-time market borrowing demand. The advantage of this model is that users have complete control over their assets, and all fund flows are public and transparent, but it requires a higher level of user operation and some blockchain knowledge.

- CeFi Custodial Model: More similar to traditional financial investment products. Users deposit stablecoins into centralized platforms (such as Coinbase, Binance, etc.), where the platform manages the assets and distributes interest, providing an experience similar to mobile banking apps. Its advantage lies in convenience and ease of use, but the cost is that users give up direct control over their assets, and the operation of funds is a "black box," relying on the platform's credit endorsement.

- Ce-DeFi Hybrid Model: Attempts to combine the advantages of the above two models. The platform uses technology to guide users' assets directly into selected underlying DeFi protocols for earning interest, while the platform itself may provide additional yield subsidies. Users enjoy the convenience of CeFi-like operations while keeping their assets in their own wallets (non-custodial), balancing high yields with asset ownership. However, this also adds risks from the underlying DeFi protocols and platform risks.

II. Exploring the Source of Yields: How DeFi Lending Protocols Support the Interest Rate Foundation of Stablecoin Investments?

After sorting through the three mainstream models, a clear conclusion emerges: If we set aside the temporary marketing activities of centralized platforms, stablecoin investments can provide a sustainable and high-return interest rate foundation, entirely based on on-chain DeFi protocols.

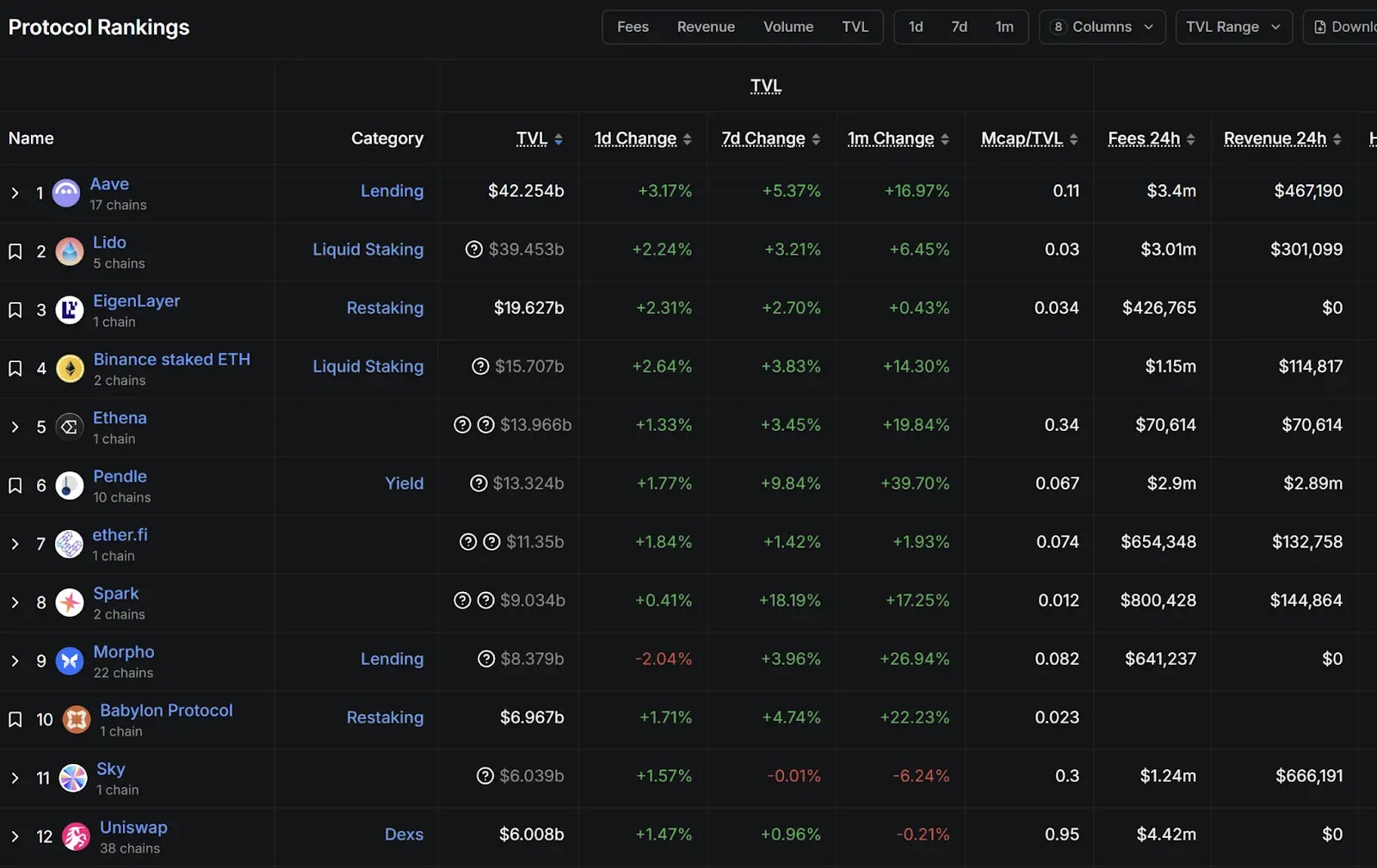

Data Source: DefiLlama, as of September 17, 2025

According to data from DefiLlama (as of September 17, 2025), the on-chain protocol ecosystem is quite diverse, including staking, lending, re-staking, and decentralized exchanges. Although the mechanisms vary, the mainstream protocols relied upon by stablecoin investment products generally adopt the most basic financial logic—"earning the borrowing spread," which is very similar to the core of traditional commercial banks. Therefore, this section will analyze this typical earning model using Aave, the leading protocol in the current DeFi lending space, as a template.

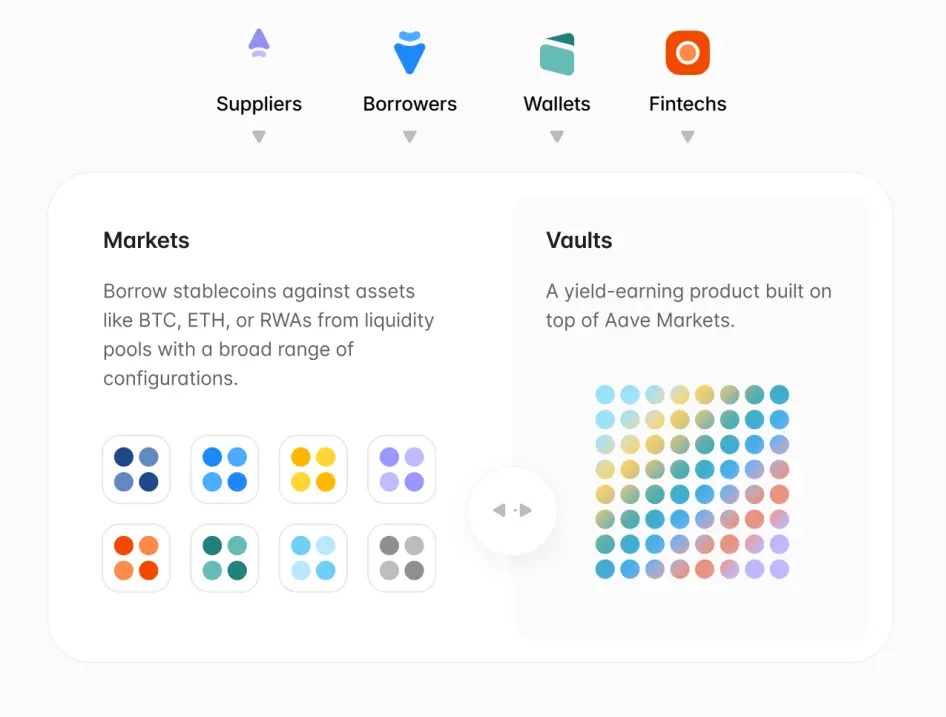

Aave was founded in 2017 by Finnish entrepreneur Stani Kulechov, originally as ETHLend, and later transformed and renamed Aave (which means "ghost" in Finnish). According to DefiLlama, Aave's total value locked (TVL) has exceeded $40 billion, ranking first among all DeFi protocols. Its official website also states that Aave operates across 14 mainstream networks, with net deposits exceeding $70 billion and a 30-day trading volume reaching as high as $270 billion, making it a giant in the "on-chain banking" space.

Data Source: Aave Official Website

Aave's core business model is an efficient and transparent "peer-to-peer" lending market, which can continuously provide high interest rates mainly relies on three core mechanisms:

- Over-Collateralization: This is the foundation and safety net of all on-chain lending. Anyone wishing to borrow must first deposit a cryptocurrency asset worth significantly more than the amount they wish to borrow as collateral (for example, to borrow $100 in stablecoins, one must deposit Ethereum worth $150). This barrier greatly ensures the safety of depositors' funds and prevents bad debts due to borrower defaults.

- Pool-to-Peer Model: Unlike the traditional model of matching individual borrowers with depositors, Aave pools all depositors' stablecoins into a massive liquidity pool. Borrowers borrow directly from this pool, and interest is paid to the entire liquidity pool. This design greatly enhances the efficiency of fund matching and liquidity, allowing users to deposit and withdraw funds instantly without waiting for a counterparty.

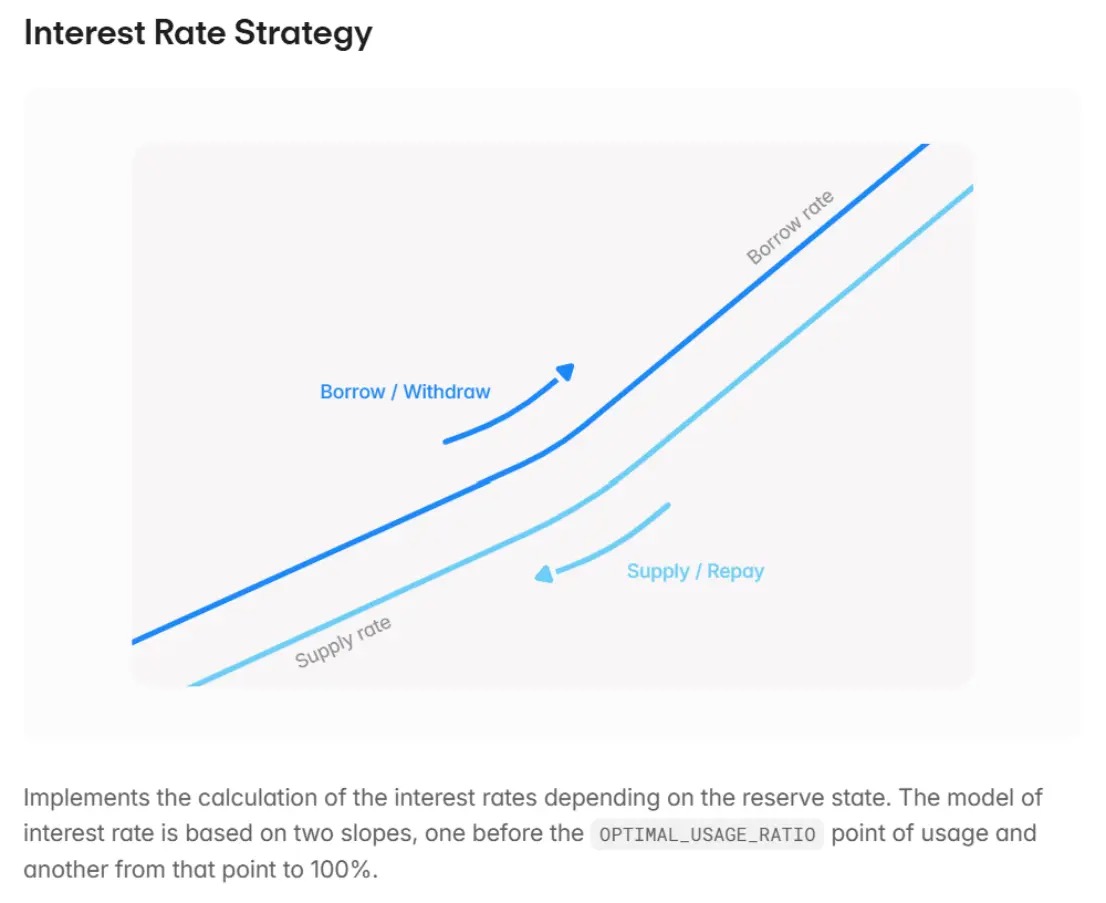

- Dynamic Interest Rates: This is the direct source of high yields. The interest rates of the liquidity pool are not fixed but are adjusted in real-time by an algorithm based on the "utilization rate" (the proportion of funds borrowed from the pool). When market demand for borrowing crypto assets (such as BTC, ETH) is high (for example, during a bull market when traders want to leverage long), a large amount of funds is borrowed, increasing the utilization rate, and the algorithm automatically raises deposit interest rates to attract more stablecoins while also increasing borrowing rates. Therefore, the high interest earned by stablecoin depositors essentially comes from the strong demand of crypto asset borrowers. For instance, on the actively traded Base chain, Aave's stablecoin deposit interest rate has long maintained around 5%, reflecting the true supply and demand of the market.

Data Source: Aave Official Documentation

Thus, it is evident that the high yields of stablecoin investments are not fictitious; they are rooted in the unique lending activities of "non-stablecoins" driven by high volatility and high trading demand in the crypto market. Protocols like Aave essentially act as decentralized financial intermediaries driven by code and algorithms.

III. Balancing Opportunities and Realities: The Opportunities and Considerations of Stablecoin Investments

After clarifying its underlying logic, the market positioning of stablecoin investments becomes increasingly clear. It precisely addresses the core pain points of investors in the current low-interest-rate environment, allowing holders to effectively avoid the price volatility of mainstream assets like Bitcoin and Ethereum while obtaining stable returns far exceeding traditional channels.

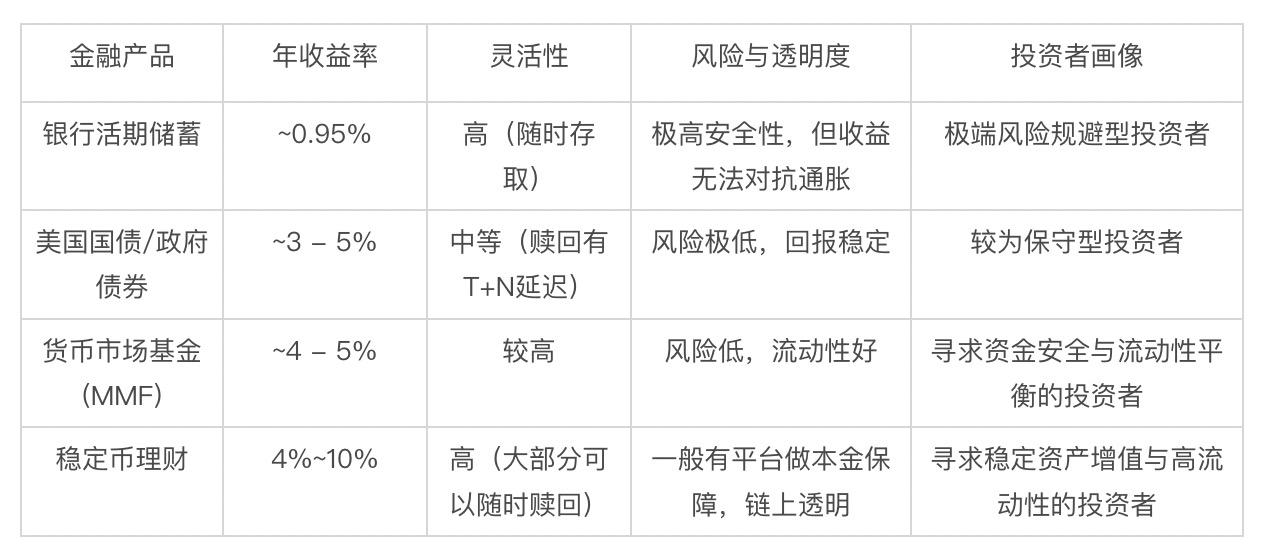

As shown in the table below, compared to mainstream conservative dollar investment products, stablecoin investments exhibit unique appeal. They align in risk attributes with government bonds and money market funds, pursuing principal stability, but their yield potential is more than double that of the latter. Additionally, they offer liquidity at the level of demand deposits, extremely low participation thresholds, and high transparency brought by the on-chain model. This combination of "high yield, high flexibility, and high transparency" constitutes its core competitiveness in the current market environment.

Comparison of Mainstream Conservative Dollar Investment Products

Data Source: Public Information Compilation

However, the other side of opportunity is always risk. As stated in Aave's official documentation, "Accessing decentralized liquidity is not without risks, but risks can be mitigated and managed." While investors are attracted by high yields, they must have a clear understanding of the following potential risks:

First is Protocol Security Risk. This is an inherent technical risk in the blockchain world. Potential code vulnerabilities in smart contracts, oracle attacks, and the security of cross-chain bridges can all become entry points for hacker attacks. Although methods like multiple code audits and community oversight can reduce risks, they cannot eliminate them.

Second is Extreme Market Conditions Risk. Although stablecoin investment products themselves invest in stablecoins, their yield sources come from the borrowing demand for mainstream crypto assets (such as Bitcoin and Ethereum). If the crypto market experiences a systemic collapse, it could trigger large-scale chain liquidations, putting immense liquidity pressure on the underlying protocol's liquidity pool. Such "black swan" events will severely test the risk control mechanisms of the protocols.

Finally, there is the De-pegging Risk of Stablecoins. History has shown that stablecoins are not absolutely stable; even mainstream stablecoins can temporarily deviate from their pegged price due to market panic or issuer credit crises. If a systemic credit collapse similar to the "Lehman Brothers" incident in traditional finance occurs, the chain reaction could have immeasurable impacts on the entire ecosystem.

IV. Conclusion: Embracing Rational Attitudes Towards DeFi Innovation in the New Normal of Rate Cuts

Returning to the initial question posed in this article: as the Federal Reserve's door to rate cuts slowly opens and global investors are forced to seek new sources of yield growth, DeFi innovations represented by stablecoin investments undoubtedly provide an attractive option. It is no longer an experimental product for a few geeks but is gradually evolving into a financial ecosystem capable of accommodating large-scale funds, logically coherent, and operating efficiently. It cleverly transforms the strong capital demand within the Web3 world into products that external investors can understand and participate in, resembling "high-yield dollar savings," bridging traditional investors with decentralized finance.

Of course, a reality that must be acknowledged is that this "new land" is still under construction, with opportunities and risks coexisting. For ordinary investors, the correct approach is not to blindly rush in or to avoid it altogether, but to adopt a rational attitude based on a full understanding of its sources of yield and potential risks, treating it as a new option worth considering in a diversified asset allocation. Only by acknowledging and learning to manage these risks deeply rooted in technology and the market can this emerging investment track truly achieve stability and longevity, allowing the innovative light of DeFi to "fly into the homes of ordinary people."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。