Author: Jae, PANews

On March 17, the cherry blossoms in Washington, D.C. had not fully bloomed yet, but the "late spring cold" in the crypto industry welcomed a glimmer of warmth during a speech.

On the stage of the DC Blockchain Summit, Paul Atkins, Chairman of the U.S. Securities and Exchange Commission (SEC), left a seemingly joking but quite significant statement: we are no longer the "Securities and Everything Commission".

This declaration marks the official end of the era where "enforcement replaced regulation," leaving countless developers sleepless in uncertainty.

68-page declaration overturns the "everything is a security" theory

In recent years, the biggest nightmare for the crypto industry has been the endless generalization of the "Howey Test".

As long as an asset involves "investment of money in a common enterprise with a reasonable expectation of profits derived from the efforts of others," it could potentially be classified as a security by the SEC. It can be said that the entire crypto industry has lived in the shadow of "possible enforcement at any time."

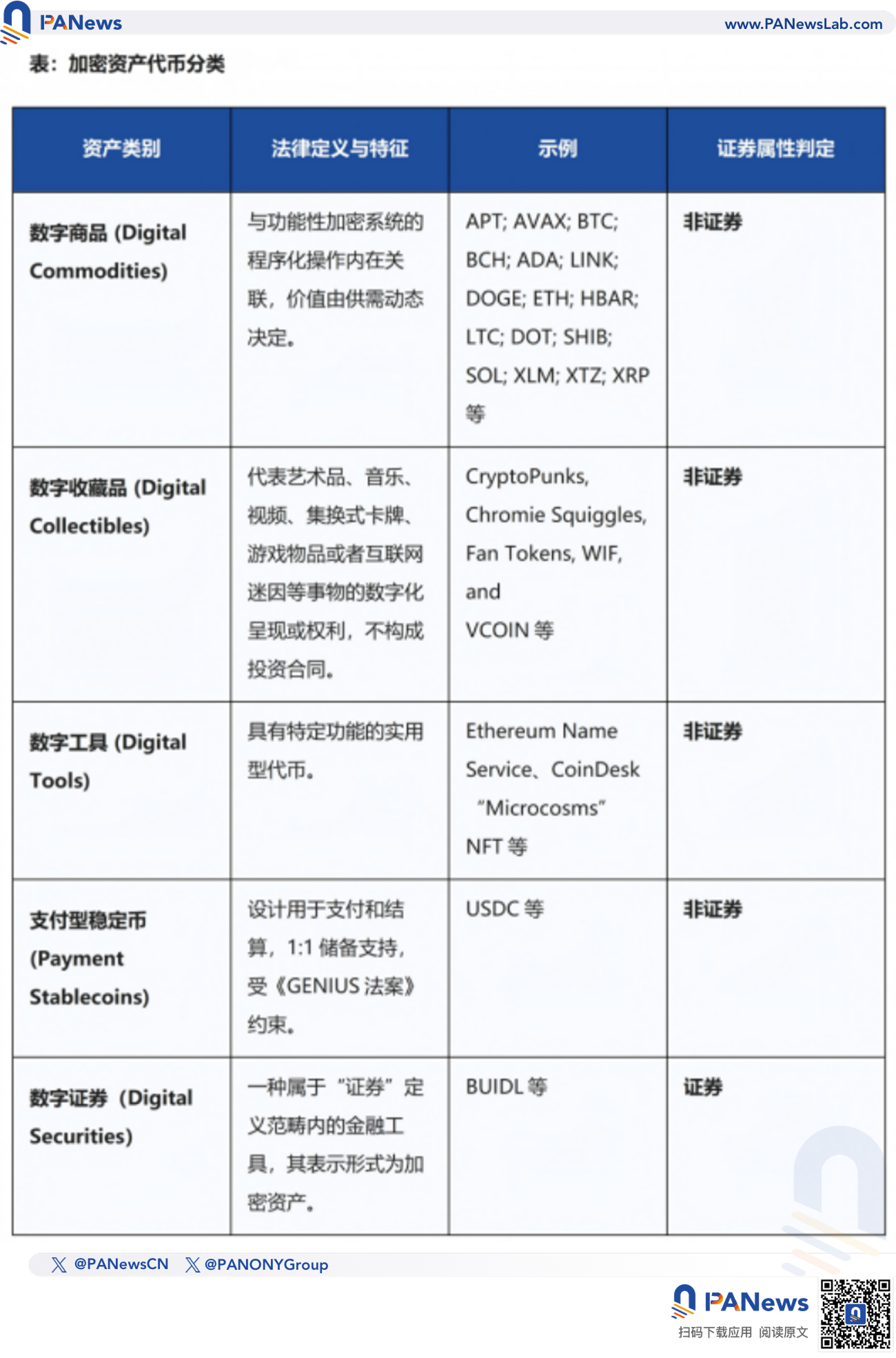

Yesterday, the SEC and the U.S. Commodity Futures Trading Commission (CFTC) jointly released a 68-page "Guidance on the Applicability of Federal Securities Laws to Certain Types of Cryptocurrency Assets and Transactions Involving Cryptocurrency Assets," which clearly defines: the majority of mainstream cryptocurrency assets do not constitute securities.

Atkins emphasized that the role of regulatory agencies is to "define clear boundaries with precise language." Regulation needs to provide the market with a "compliance uphill" rather than "enforcement traps," and this guidance is the SEC's systematic reckoning of the regulatory chaos over the past decade.

This guidance establishes a refined "Token Taxonomy" that liberates cryptocurrency assets from the singular securities label.

Among them, the guidance focuses on the concept of "Functional" cryptocurrency systems. When an asset's value primarily derives from the systematic programming and market supply and demand, rather than the management efforts of a single issuer, this asset exhibits the properties of a "commodity." This explanation may provide a significant legal moat for public chain protocols.

More importantly, the guidance also provides a positive response to the industry's long-standing concerns about mining, protocol staking, and airdrops: in the absence of a clearly defined issuer as a counterparty or manager, these algorithm and code-based activities are generally not regarded as securities issuance.

This marks a logical shift from "the asset itself is a security" to "the method of sale determines the security attributes." It effectively adopts the judicial logic from the previous Ripple case, namely: XRP itself is not a security; only specific institutional sales contracts may constitute securities issuance.

If the joint guidance serves as macro-level regulatory correction, then the CFTC's recent issuance of a "No Action Letter" (NFA) to the wallet application Phantom represents a micro-level practical implementation.

Phantom plans to provide regulated derivatives and event contract access services, which could have easily been deemed unauthorized "introducing brokers" in the past.

However, the CFTC's Market Participants Division determined that Phantom's role is limited to providing a "passive software interface" that allows users to interact directly with registered designated contract markets (DCM) or futures commission merchants (FCM) without handling user assets or facilitating trades.

Regulators have explicitly acknowledged for the first time: a pure software interface does not need to bear the legal responsibilities of its broker-dealer. This distinction between "code" and "intermediary" will greatly unleash the potential of wallets as Web3 business portals.

The regulatory clearance obtained by Phantom may provide a replicable compliance model for non-custodial wallets, Layer 2 interfaces, and even DeFi protocol frontends.

Regulatory reshaping will trigger "triple ripples" in the crypto ecosystem

When "the majority of cryptocurrency assets are not securities" becomes the official benchmark, the market pricing logic will fundamentally change.

Previously, due to the expectation of securitization, the liquidity of many tokens was restricted to non-U.S. platforms, and U.S. users were turned away, leading to a significant "compliance discount".

The release of the new guidance is expected to trigger a large-scale asset re-evaluation, especially for projects with functional utility (Digital Tools) and effective market adjustment mechanisms (Digital Commodities).

With the unified guidance from the SEC and CFTC implemented, the integration and access paths for cryptocurrency assets and traditional finance will become smoother. National pensions, traditional hedge funds, mutual funds, and even corporate treasuries will be able to allocate assets based on clear classifications, significantly reducing the subsequent regulatory traceability risks. Additionally, applications for various token ETFs will proceed more smoothly.

It's worth mentioning that CFTC Chairman Michael Selig has expressed positive support for "tokenized collateral". The CFTC is formulating new rules, attempting to treat qualified tokenized assets as collateral, promoting 24/7 real-time risk management in financial markets, and further optimizing capital efficiency.

The NFA obtained by Phantom marks the beginning of regulators accepting the non-intermediated characteristics of blockchain. This distinction between "interface" and "intermediary" may encourage more developers to adopt decentralized architecture, stimulating more innovative activities in the crypto space.

Although not holding private keys or facilitating trades, this "regulation-driven technological evolution" may guide more protocols to choose a more decentralized operational model, freeing on-chain activities from shackles, allowing decentralized platforms to openly welcome users.

After the spring thunder in Washington, the crypto industry finally welcomes a long-awaited shower of blessings.

With the joint efforts of the two chairmen, the once-divided regulatory system is healing, and the blurred legal boundaries are gradually becoming clearer.

Of course, the game continues. The full implementation of the guidance will still take time, but the general direction is already clear. As PANews has emphasized before: compliance is not the enemy of innovation, but its ticket to mainstream market entry.

As the majority of cryptocurrency assets are classified as non-securities and non-custodial interfaces gain regulatory recognition, the crypto industry is slowly shedding the label of "illegal experimentation" and adorning itself as the "cornerstone of digital finance."

The implementation of this series of regulatory actions signifies that the era of profiting from gray areas is entering a countdown, and a new era of crypto priced by certainty, transparency, and technical hard power is about to begin.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。