The first wave of tokenization is paving the way for future developments: programmable compliance, autonomous collateral management, and real-time yield optimization.

Written by: Prathik Desai

Compiled and organized by: BitpushNews

Looking back to 2015, European banks had been digitalizing their operations for nearly two decades. You could check your balance, transfer funds, and pay bills via your mobile phone. Although the infrastructure was functioning well, every financial service still had to operate through the bank as the "gatekeeper." No service could access your funds without the bank's permission.

Then, PSD2 (Revised Payment Service Directive) mandated banks to open their underlying infrastructure via APIs. Stripe built its European financial operations on open banking, Plaid connected hundreds of millions of accounts, and Shopify started leveraging transaction data to underwrite loans. It is expected that by 2030, the annual revenue from embedded finance in Europe alone will exceed 100 billion euros.

However, for the industry to achieve this goal, it must first undergo a 15-year adaptation period of online banking, during which hundreds of millions of people realized that the digital financial infrastructure is reliable. The API layer did not create trust from thin air; it was built upon years of accumulated trust.

This is the story of how trust evolves around any new technology. Tokenization is currently experiencing the same moment.

Last week, Pantera Capital released a report on the state of tokenization in 2026.

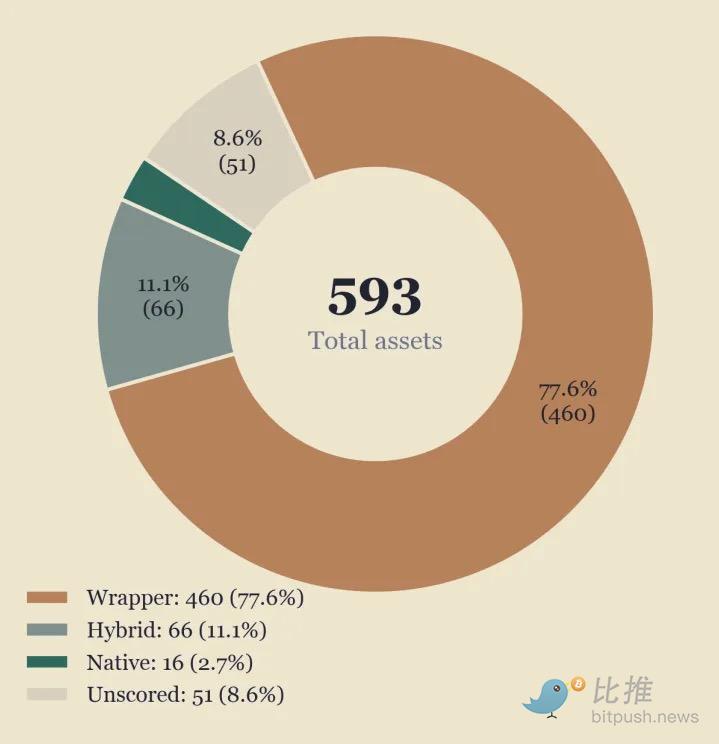

In this report, they scored 542 of the 593 real-time tokenized assets based on three dimensions of on-chain maturity—issuance and redemption, transferability and settlement, composability—resulting in an average Tokenization Progress Index (TPI) of 2.04 (out of 5). About 77% of tokenized assets are still "digital receipts" for offline original assets. In these cases, the offline ledger still holds authority, with the token merely adding a data layer on top.

It's easy for people to interpret these scores as "poor performance." Cryptocurrency natives might describe it as industry stagnation. But no technology can achieve sustained large-scale application by skipping the "trust-building phase." Here’s why:

Wrappers: The First Stop

Pantera's report found that among the 593 tracked assets, 460 (77%) fall into the category of "wrappers," whereas only 16 were launched, managed, and recorded natively on-chain. Tokenized wrappers refer to assets for which minting and redemption are still conducted off-chain through centralized issuers. About 66 are categorized as hybrid.

Pantera refers to the current stage as the "newspaper on the web stage." This stage is not a failure of the industry to mature quickly but rather the first stop in testing the proposition of whether "the on-chain representation of existing traditional assets can provide any benefits."

Let’s rewind twenty years. Imagine reading about e-commerce for the first time. You scroll through the page, click to purchase, and then a stranger sends you a box. At that time, it felt incredible. You might place an order just for the experience of it. But would you be willing to pay before the box arrived?

The early days of e-commerce heavily relied on cash on delivery because customers were slowly warming up to the idea of "buying things without touching and feeling the physical item." Users preferred cash on delivery because it helped them overcome the first barrier: trusting that e-commerce was a viable model. The technology facilitating online transactions was not the issue—bank transfers supporting SWIFT have existed since the early 1970s, and consumer payments via platforms like CyberCash and PayPal became possible in the late 1990s and early 2000s.

However, the shift to online payments took much longer.

Similarly, the first wave of tokenization is paving the way for future developments: programmable compliance, autonomous collateral management, and real-time yield optimization. Following this are financial building blocks that separate and recombine ownership, cash flow, and risk.

The tokenized versions of offline assets have demonstrated that new technology can achieve faster settlements, cheaper transfers, and clearer record-keeping. Every time a tokenized government bond or money market fund settles faster than its offline equivalent, it builds confidence among customers.

The data in the report also supports this view.

Among Pantera's three TPI standards, the dimension measuring transferability and settlement scores the highest, at 2.29. In fact, 205 assets scored a 3 in this dimension, indicating that the industry is leaning towards utilizing blockchain as an authoritative management and settlement layer. In contrast, the TPI for issuance and redemption lags behind at just 1.82. Over 91% of assets still rely on administrator-gated minting and custodian-mediated exits.

These scores suggest that the market is more accustomed to reliably moving assets on-chain before trusting blockchain to autonomously initiate and redeem assets.

This maturity curve is inevitable for any technology. That is because even the greatest technologies cannot create demand for the asset out of thin air.

Demand Targets Assets, Not Tracks

Introducing native on-chain assets will not automatically attract capital. The data in the report reinforces this point.

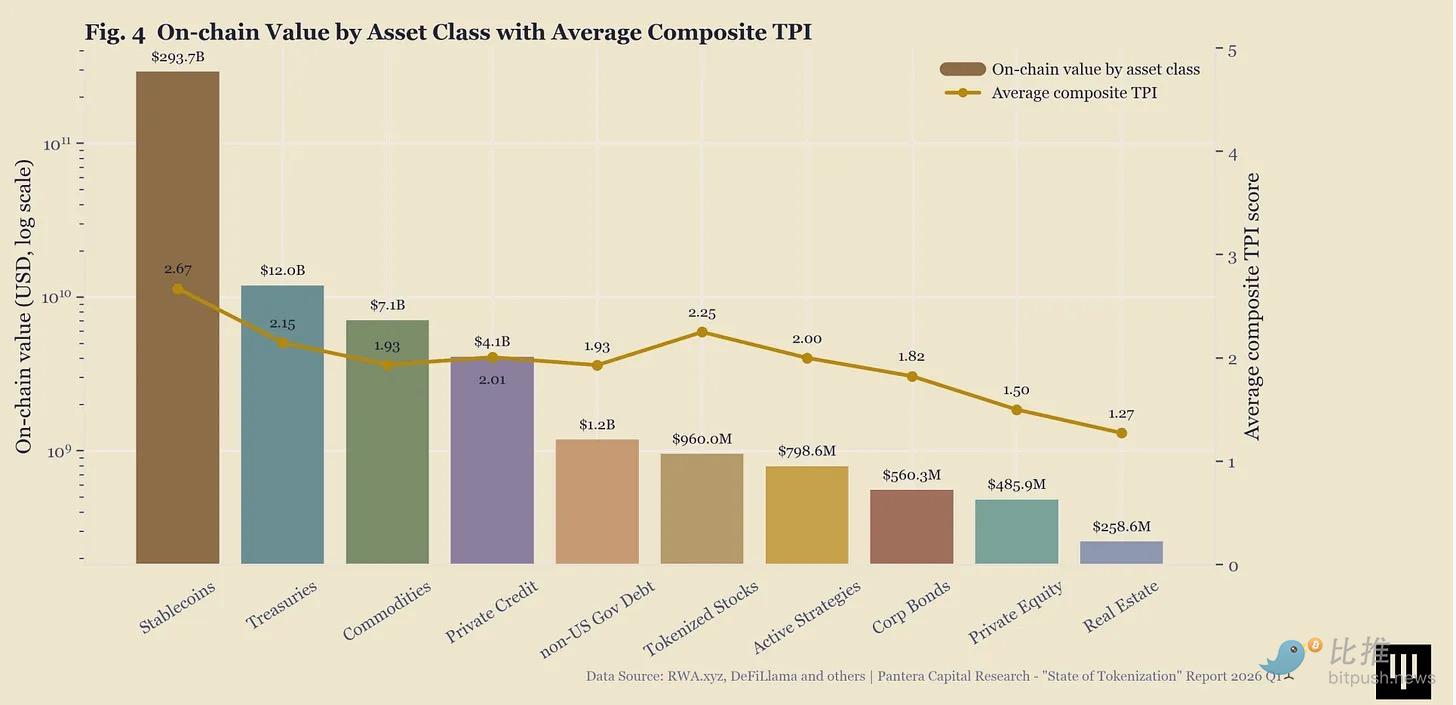

Stablecoins account for 91.6% of the $320 billion tokenization market. U.S. government bonds contribute an additional $12 billion. Together, they account for approximately 95% of the total. All other assets, including private equity, real estate, and corporate bonds, currently only represent a negligible 5%.

This indicates that the market is not blindly following the most intriguing "native tokenized assets." Demand is following the assets that people have always wanted to invest in. People do not care whether something appears in the form of a wrapper or as a native on-chain government bond fund. As long as the new infrastructure can provide them with a progressively better experience in holding, transferring, and recording assets, they are more inclined to choose it over the old infrastructure.

We see this dynamic across multiple primitives in the crypto ecosystem.

Hyperliquid's HIP-3, launched at the end of 2025, has created a permissionless perpetual futures market for real-world assets, including stocks, commodities, indices, and forex. Since its launch, these markets have seen trading volumes exceeding $240 billion. In January 2026, Hyperliquid's silver HIP-3 perpetual contract market gained a 2% share of the metal's global trading volume within just a month of its launch.

The surge in demand is not because Hyperliquid invented a new format. The traders choosing Hyperliquid were already looking to gain exposure to Tesla, silver, gold, and the S&P 500 index. The format provided by Hyperliquid—a permissionless, non-custodial venue available 24/7—merely minimized the friction and time between the occurrence of events and the traders expressing their opinions. These underlying assets were already popular outside of Hyperliquid. The success of this technology stems from the platform amplifying access opportunities.

A similar dynamic is playing out in the field of tokenization.

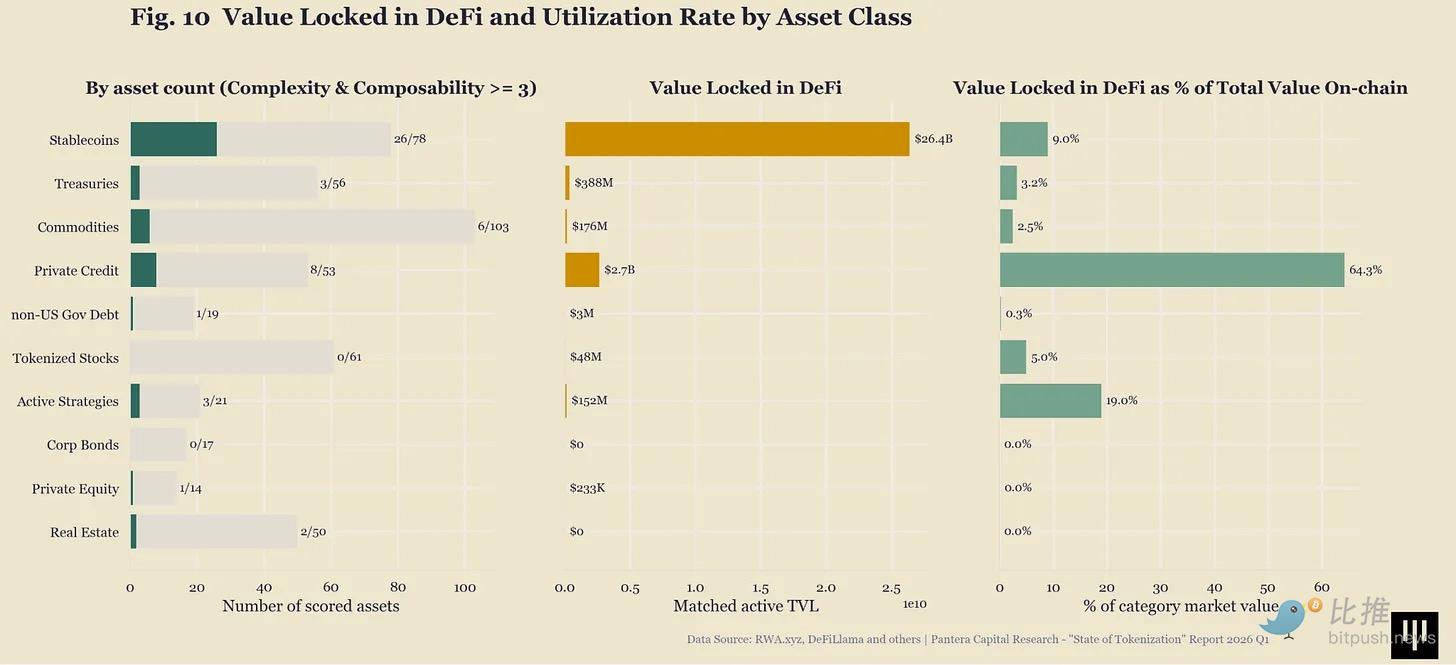

Private credit has captured 64% of the highest share of its supply actively deployed in DeFi protocols. This is significantly higher than the 9% for stablecoins and 3.2% for government bonds. The demand is not specifically targeting "tokenized" private credit.

Those deploying funds through tokenized private credit into DeFi protocols are doing so because these wrappers provide them with returns denominated in stablecoins. The underlying demand remains the thirst for non-crypto yields. They do not care whether the underlying track is merely a wrapper for existing private credit products or a native on-chain product.

Even the surge in commodities confirms this.

Native on-chain products around tokenized commodity systems grew from $1 billion in January 2025 to $5 billion today, a fivefold increase. This was not because these tracks offered something different. This leap followed gold's 65% increase in 2025—its strongest annual increase since 1979. The appreciation in tokenized gold products is largely due to the appreciation of gold itself. The blockchain merely facilitated better settlement, transfer, and ownership management of the asset.

If the underlying asset is attractive, tokenization can make it more accessible, settlement cheaper, and movement easier. If the underlying asset is itself mundane, no amount of on-chain composability can compensate for that.

Where is the industry headed?

The Pre-API Era

I find the PSD2 moment astonishingly similar to the journey of tokenization.

The regulatory breakthrough in Europe occurred in 2015, took effect in 2018, and led to scaled native products like Stripe Financial Connections and embedded loans between 2020 and 2023. It took about five to eight years for the underlying open infrastructure to nurture mature native products.

The regulatory breakthrough moment for tokenization began to take shape in 2024, gradually rolling out across various jurisdictions. MiCA (Markets in Crypto-Assets Regulation) will fully come into effect in December 2024, and by the end of 2025, 102 crypto asset service providers will be authorized across Europe. The GENIUS Act was signed in July 2025, becoming the first federal legislation in the U.S. targeting digital assets. A few weeks later, the SEC launched Project Crypto, with Chairperson Atkins acknowledging that companies from Wall Street to Silicon Valley are queuing for tokenization.

If the timeline for embedded finance is a reference, we should expect the emergence of native on-chain products within the next 3-4 years. They may not be ubiquitous or cover all asset classes. However, in those segments where enough trust has already been established during the wrapper phase, and where underlying demand exists, we will see transformation sooner.

Private credit is the clearest candidate. For every three dollars of on-chain private credit, two dollars are already actively involved in DeFi. The composability of private credit products like Maple's syrupUSDC, which perform prominently in DeFi, is built on a foundation that has first proven it can reliably underwrite, issue, and recall loans on-chain. Native functionality will come as an extension of the trust that has already been earned.

The $320 billion tokenization market scores only 2.04 (out of 5). This still reads as a failing grade. But this is a starting point for a new industry beginning to build trust, positioning itself through faster settlements, cheaper bookkeeping, and more transparent ledgers until the market's demand for native on-chain assets truly explodes.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。