The lifting of restrictions in July and the massive IPO fundraising will bring liquidity and valuation tests; the first stress test for AI assets is about to arrive.

Written by: Xiaojing

Edited by: Xu Qingyang

In the first half of 2026, global technology companies are ushering in a rare wave of IPOs.

On June 12, SpaceX is about to list on Nasdaq with a valuation of $1.77 trillion, potentially becoming the largest stock issuance case in human history; Anthropic is valued at $965 billion and has secretly submitted an IPO application; in Hong Kong stocks, the stock prices of Zhizhu AI and MiniMax have surged after going public, with Zhizhu's market value at one point exceeding twice that of JD, significantly higher than Baidu and Meituan.

Most of these companies have yet to prove traditional profitability. Zhizhu's revenue in 2025 is only 724 million yuan, remaining in the red; SpaceX's revenue in 2025 is $18.7 billion, with a net loss of $4.9 billion; Anthropic, although its ARR has surpassed $10 billion, sees its valuation nearing $1 trillion.

Why is the market willing to place such valuations?

First, AI is seen as a new technological revolution. The largest platform shift since the internet, the consensus among capital is that trillion-dollar giants will emerge from these companies, with almost no limit to the industry replacement space.

Second, the scarcity of trading. "Pure-blooded AI unicorns" are the most attractive narrative in global capital for 2026. Zhizhu has issued only over 37 million H shares, with a very small circulating supply; SpaceX's issuance accounts for only 4.2% of the total capital.

The extremely limited chip supply meets surging capital demand, pushing prices to heights that traditional valuation models cannot explain.

01 Where is the valuation anchor point?

Zhizhu AI and MiniMax are both landing on the Hong Kong Stock Exchange in January 2026. The market value gap between the two companies exceeds 400 billion Hong Kong dollars, with Zhizhu AI leading at a market value of about 500 billion Hong Kong dollars, but which market does it anchor?

If calculated based on AI Coding, the total R&D expenditure of enterprises in China is about 3.4 trillion yuan. Even assuming that 30%-40% of that is related to software development, and further assuming that 70% of it will be done by AI in the future, the corresponding substitute output limit is only about 700 billion - 1 trillion yuan. Calculating at about 460 billion yuan, Zhizhu's market value corresponds to 46%-66% of this limit under the assumption of the whole industry's AI Coding substitute output.

If calculated for SaaS replacement, the annual revenue of the US SaaS application layer is about $200 billion, equivalent to about 1.4 trillion - 1.5 trillion yuan. Zhizhu's current market value is approximately $64 billion, which is about 30% of the annual revenue of the US SaaS market. Moreover, China's SaaS market has not formed the scale and payment habits of the US.

If we add multimodal content production, AI video generation predominantly replaces production costs rather than directly creating a new content market of equivalent scale. A more reasonable metric to consider is the portion of content production costs that can be compressed by AI, which may only amount to about 200 billion - 300 billion yuan.

Combining these three most optimistic estimates, the substitute output for China's AI Coding is about 700 billion - 1 trillion yuan, the theoretical SaaS replacement limit in the US is around 1.5 trillion yuan, and the replaceable costs in the content production segment are about 200 billion - 300 billion yuan, totaling roughly 2.4 trillion - 2.8 trillion yuan.

Under this extreme assumption, Zhizhu's market cap still accounts for 16%-19% of the total pool. This does not even consider that many AI companies are competing for the same pool of budgets.

Thus, the market is pricing in the rewriting of the budget for R&D, software, and content production throughout the AI application layer in advance.

This is also where the term "AI faith" becomes intriguing. From the perspective of existing market replacement logic, this valuation is clearly very difficult to explain using just arithmetic; but valuation itself is not static arithmetic but a bet on the future. It can only indicate that the current price is expensive, but it is very hard to prove that it will be expensive in the future.

Across the ocean, SpaceX, which is rushing for its IPO, has basic data with Starlink (Starlink) having 10.3 million users, projected revenue of $11.3 billion in 2025, and a profit margin of 39%. However, the corresponding price-to-sales ratio for $1.77 trillion is nearly 100 times.

A space analyst said: "The market's expectations for SpaceX are not just about providing computing power from space to Earth. It's about providing infrastructure for the future of space. How to price this infrastructure, I think, that's a matter of imagination. The three core elements are the value of logistics, the value of the infrastructure, and the value of resources. For example, gold is $1,000 on Earth now, but if another planet is integrated into our survival map in the future, then the resources of that planet must also be valued. But this also involves complex issues like profit distribution and institutional construction. So relying solely on faith, the numbers can't be calculated."

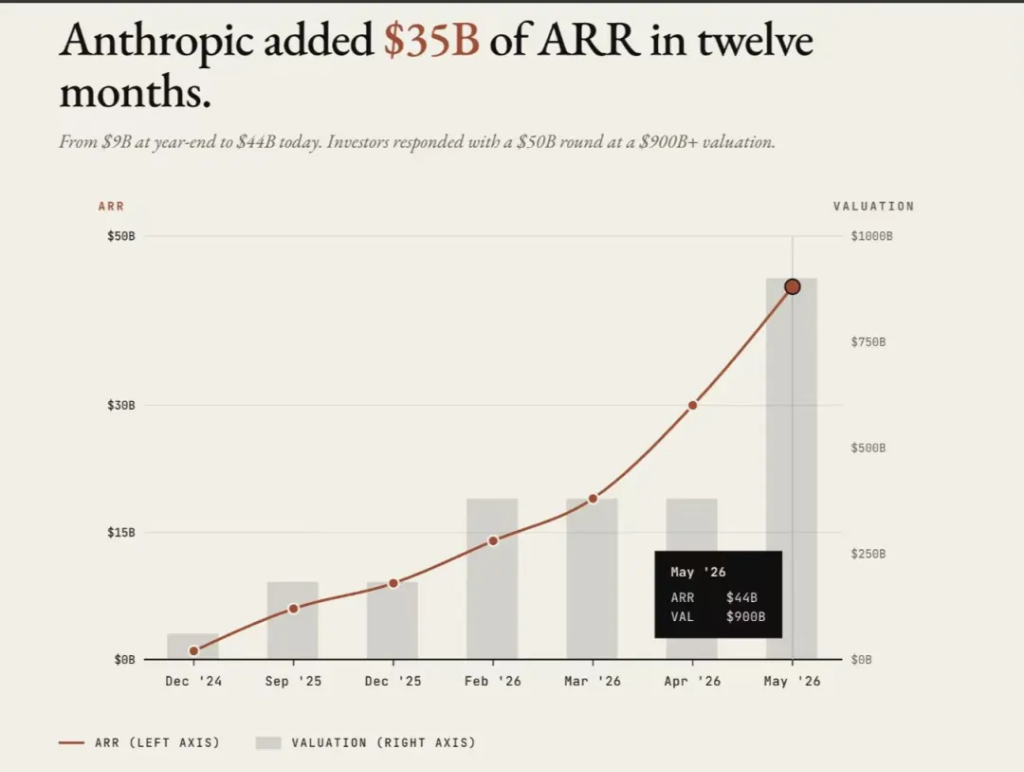

An example of Anthropic's faith is its rapidly growing ARR, surging from $9 billion at the beginning of the year to $44 billion in May, doubling in two months. What is behind this is that it has hit the right track for AI coding, with capital viewing it as a company occupying the development access and capturing the future stronghold of safe AI, thus deserving more than just platform-level valuation multiples.

OpenAI is the giant unicorn at the center of this wave of generative AI, with a valuation of $852 billion, ChatGPT achieving 900 million weekly active users, and having the most complete product matrix, but it currently lacks more imagination, making it difficult for capital markets to assign a higher level of faith.

Image: Anthropic's ARR surged from approximately $9 billion to $44 billion within a year.

02 The "formula" of AI faith

The word "faith" sounds like a mockery, but the faith in capital markets has never been blind.

It has a formula, a transmission path, and an inherent logic.

Just two days before SpaceX launched its roadshow, on June 2, Forbes' real-time billionaire list showed that SoftBank founder Masayoshi Son's net worth climbed to $100.7 billion, reclaiming the title of Asia's richest man after more than twenty years. On the same day, SoftBank's market value skyrocketed to 49.3 trillion yen, officially surpassing Toyota, ending Toyota's two-decade reign as Japan's top market cap.

Masayoshi Son's "revenge" path is the best slice for understanding the pricing of this AI faith.

At the end of 2022, he was seen as a "loser". The Vision Fund's losses in WeWork, Uber, and various sharing economy companies were still bleeding, and SoftBank's market value shrunk to over $60 billion. But during the subsequent two years of silence, he completed a total change of direction.

In 2016, Son invested $31 billion to acquire ARM, and in 2023, he repurchased 25% of the shares from the Vision Fund for $16.1 billion, totaling an investment of $47.1 billion. Entering 2026, the explosion in demand for AI agents from servers' CPUs, combined with the energy efficiency advantages of the Arm architecture, saw Arm's stock price surge by 268% within the year. Based on SoftBank holding nearly 90% of the shares, as of early June, the paper gains exceeded $32 billion.

At the bottom layer is the application layer. SoftBank has invested over $64 billion in OpenAI, acquiring about 13% equity and becoming the second-largest external investor after Microsoft. As of March 31, 2026, this investment has confirmed a return of approximately $45 billion.

Above that is computing power infrastructure. The US Stargate project, a collaboration of SoftBank with OpenAI and Oracle, has a total investment of $500 billion; the French data center plan, €75 billion, with the first phase at €45 billion, aiming for 3.1 gigawatts of computing power by 2031. In between, SoftBank also plans to acquire Ampere Computing for $6.5 billion in 2025, completing the last piece of the puzzle for Arm architecture data center CPUs.

Chip design (Arm) → General computing power chips (Ampere) → Data center infrastructure (Stargate + France) → Model layer applications (OpenAI 13% equity).

From bottom silicon to top intelligence, Masayoshi Son has drawn a vertical integration causal chain for AI infrastructure.

The market has given him the corresponding valuation. SoftBank's stock price rose over 140% from its low in 2026, while annual net profit of 550.8 billion yen hit a historical high.

Son's own words at the shareholder meeting were: "The scale of this wave of AI will be at least 10 times that of the internet, and may even reach 50 times." He likened it to the Great Depression of 1929, when industries related to electronic and industrial mechanization suffered a severe setback, yet continued to grow steadily for nearly a century afterwards.

But the issue lies in the fact that not every investor is making a systematic bet like Son; many just see his results and attempt to replicate his confidence using a far more rudimentary logic.

03 July letters, the first test of faith

In July 2026, a liquidity shock that has been scheduled for half a year will arrive on time.

About 25.86 million shares (accounting for 5.76% of the total capital) held by cornerstone investors of Zhizhu will end their lock-up period. This number seems small, but when divided by the current circulating capital: Zhizhu's actual circulation rate is only about 2.67%, with total tradable shares just above 12 million. The unlocking of cornerstone shares will expand the tradable capital by more than twice overnight.

The impact on MiniMax is even more severe. On July 8, about 44.29% of old shareholders (with a six-month lock-up) and 5.34% of cornerstone investors will unlock nearly 50% of their shares simultaneously. Previously, MiniMax's circulation rate was about 5.44%, meaning that after the unlocking, the tradable capital in the market will suddenly expand from less than 6% of the total capital to close to 56%. The circulation will increase tenfold overnight.

Historical references do not provide comfort. In August 2021, Kuaishou faced a large-scale unlocking six months after its IPO, with its stock price plummeting 15.3% on the same day. Xiaomi’s shares dropped 7.5% on the first day after unlocking in January 2019, and then continued to decline to a record low since its IPO.

However, the situation Zhizhu and MiniMax face is more complex than what Kuaishou encountered back then. By the time Kuaishou had its unlocking, its stock price had already fallen by more than half from its peak, significantly reducing the incentive for liquidation; while Zhizhu remains at around 10 times its issue price, MiniMax has surged over three times its issue price. Cornerstone investors and Pre-IPO shareholders are looking at multiples, even tenfold returns on their paper gains.

More crucially is the arrangement of the timeline. On June 8, both Zhizhu and MiniMax were included in the Hang Seng Tech Index, with a combined weight of about 5%-7%. Passive tracking funds amounting to approximately $25 billion correlate with a mandatory purchase of around $1.25 billion to $1.75 billion. Zhizhu was simultaneously included in the Hong Kong stock connect, and under baseline scenarios, southbound funds are expected to contribute around HK$18.6 billion in net inflow. Since MiniMax has a dual-class share structure, its Hong Kong stock connect will not open until August 6.

The bearers of liquidity might ease price pressure. However, when the circulating capital expands from 3% to over 50%, the magic of the "scarcity premium" in this pricing factor will diminish.

Of course, unlocking does not equate to selling. Not all shareholders who gain trading rights will sell on the first day. For instance, industrial capital has limited motives for large-scale sales in the short term.

But great fluctuations are inevitable.

Looking across the ocean, Anthropic, OpenAI, and SpaceX will collectively raise over $200 billion from the public markets through their IPOs, a number equivalent to the total of the US IPO market over the past three to four years, potentially concentrated in the upcoming 4-5 months.

Specifically, SpaceX has a planned fundraising of $75 billion for its June 12 IPO, and OpenAI and Anthropic submitted their S-1s covertly on June 8 and June 1 respectively, but have yet to finalize their listing dates. Market expectations are that they may land as early as this autumn, with each planning to raise between $60 billion to $90 billion.

However, the real pain points have already begun in the roadshow phase. Large asset managers need to reduce holdings in other tech stocks to make room for new IPO positions starting from SpaceX's roadshow in June.

Historically, the panic caused by every massive IPO has proven to be short-term digestion issues rather than structural disasters. What should truly be concerned is whether these trillion-dollar valuations can really hold. If any one of them falls below the issue price, the impact on the valuation anchor of the AI sector would be far more lethal than a liquidity loss of $200 billion.

However, multiple secondary market investors have stated: "Even if the primary market pricing is high, there is still ample space in the secondary market. This round of cash burning is far less brutal than the previous internet wave, but the potential for growth is much larger."

During the peak of the 2000 internet bubble, annual venture capital investment in internet companies was about $105 billion (according to historical data from NVCA/PitchBook, roughly $190 billion adjusted for inflation today).

However, the cash burning scale of single companies was limited, with Amazon recognized as the largest "cash-burning machine" of that era, generating $1.64 billion in annual revenue and a net loss of $720 million throughout 1999 (Amazon's 1999 10-K annual report). Pets.com burned less than $300 million from its establishment to its closure, while Webvan cumulatively consumed about $800 million. Throughout the dot-com era, no single company recorded a loss exceeding $1.5 billion in a single year.

However, during the dot-com period, many companies had almost no revenue and were purely cash-burning, leading to their direct demise, creating a horrific scene as the Nasdaq plummeted from 5,048 points to 1,114 points, a drop of 78%, with hundreds of listed companies becoming worthless.

In contrast, the current AI companies at least have real and rapidly growing revenue, backed by powerful giants like Microsoft, Google, and Amazon, which will not lead to a batch of sudden deaths in the style of dot-com in the short term.

At the same time, however, analysts at Morgan Stanley have clearly pointed out that Meta, Microsoft, and Alphabet's respective CapEx-to-revenue ratios (21%-35%) have exceeded the levels of AT&T during the peak of the telecom bubble.

There are optimistic expectations, but risks are also accumulating.

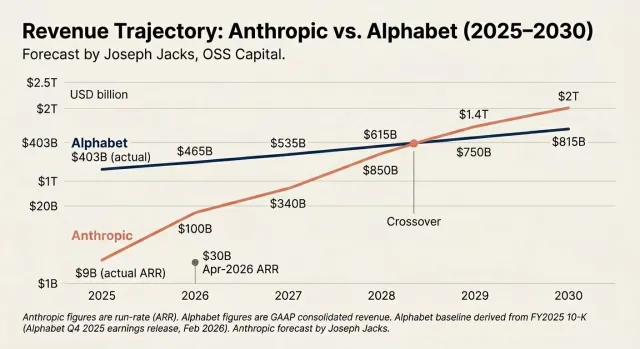

Image: Some investors predict that Anthropic's revenue growth will accelerate to the point of overtaking Google’s parent company Alphabet around 2028.

This is a race against time.

Domestically, DeepSeek's valuation, rumored in May to be in the range of $10 billion - $20 billion, was quickly raised to $45 billion - $50 billion and is now approaching $60 billion; reports indicate that Jieyue Star submitted applications to the Hong Kong stock exchange on June 8, having just completed nearly $2.5 billion in pre-IPO funding; the Dark Side of the Moon was reported to be seeking a new round of $2 billion financing on June 8, with a valuation target of $30 billion and is simultaneously preparing for a Hong Kong IPO; Zero One Everything has transitioned to corporate AI applications, with founder Kai-Fu Lee clearly aiming for a Hong Kong listing in 2027.

"No one knows how long the window period will last, but seizing the window period is too important," said an investor.

During the window period, understanding the pricing logic of AI faith will allow one to seize the opportunity of this golden era; otherwise, it will just be a mirage of bubbles.

This is the best of times, and it is the worst of times.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。