Written by: Frank, MSX Maitong

What is the biggest fear of the AI bull market?

It is neither a particular company's model falling behind temporarily nor the performance of a generation of chips underperforming expectations, but rather the market starting to doubt, whether the capital expenditures of tech giants, which have been the most certain variable in the past two years, can continue to grow indefinitely.

On July 1, according to Bloomberg, Meta is preparing a new cloud computing business, planning to sell potential excess AI computing power to external customers while considering offering managed model services similar to AWS Bedrock.

After the news broke, Meta's stock price surged over 10% during the day, eventually closing up 8%, while CoreWeave and Nebius dropped 13% and 17%, respectively; on the other hand, during the Asian session, the sell-off spread to AI hardware, with the Korean KOSPI dropping about 7% at one point, and Samsung Electronics and SK Hynix both falling over 8%.

Overnight, Meta transformed from one of the most aggressive super buyers in the computing power market into a potential seller.

This sudden industry shock has revealed a significant crack in a foundational belief that has supported the entire AI bull market for the past two years: Does this mean that AI infrastructure has shifted from shortage to surplus, and that the giants' two-year arms race for computing power is about to reach a turning point?

Or is it that Meta has exposed a harsher reality: What the market is truly lacking—the GPUs or the ability to convert GPUs into models, products, and revenue?

1. If everyone lacks enough computing power, does that mean only you, Meta, have excess?

For the past two years, the underlying logic of this wave of AI markets can essentially be boiled down to two words: "shortage".

More accurately, it is a structural bull market driven by a surge in demand, supply shortages, and the frenzied capital expenditure expansion by tech giants.

For example, it was initially high-end GPUs and advanced packaging capacities that were in short supply, then bottlenecks spread outward. HBM, high-speed optical modules, and networking equipment began to be in short supply, then it extended to data center space, power capacity, gas turbines, electrical equipment, and high-density cooling. Today, the supply-demand tension has reached ordinary DRAM, NAND, enterprise-grade SSDs, and even mechanical hard drives, which were once considered "old era assets."

It can be said that the speculation across the entire AI industry chain over the past two years has resembled an ever-lengthening shortage list, clearly exhibiting the "barrel effect" and sector rotation. This also means that as long as the demand for model training and inference continues to grow, and new computing power capacity, electricity, and data centers are not released in time, every scarce link stuck in the middle will have the opportunity to gain stronger bargaining power, allowing upstream manufacturers to raise prices, lock in long-term contracts, and have the motivation to continue expanding.

Therefore, if we trace back further, we find that the true engine of this bull market is not just Nvidia, Hynix, or power equipment companies themselves, but precisely the growing AI demand expectations and capital expenditures of tech giants like Microsoft, Meta, Amazon, and Google:

The willingness of upstream giants to spend determines how many GPUs, storage, and networking equipment they will buy, how many data centers they will build, and how much third-party cloud computing power and long-term electricity resources they will secure, directly affecting the peak prosperity of the entire AI supply chain.

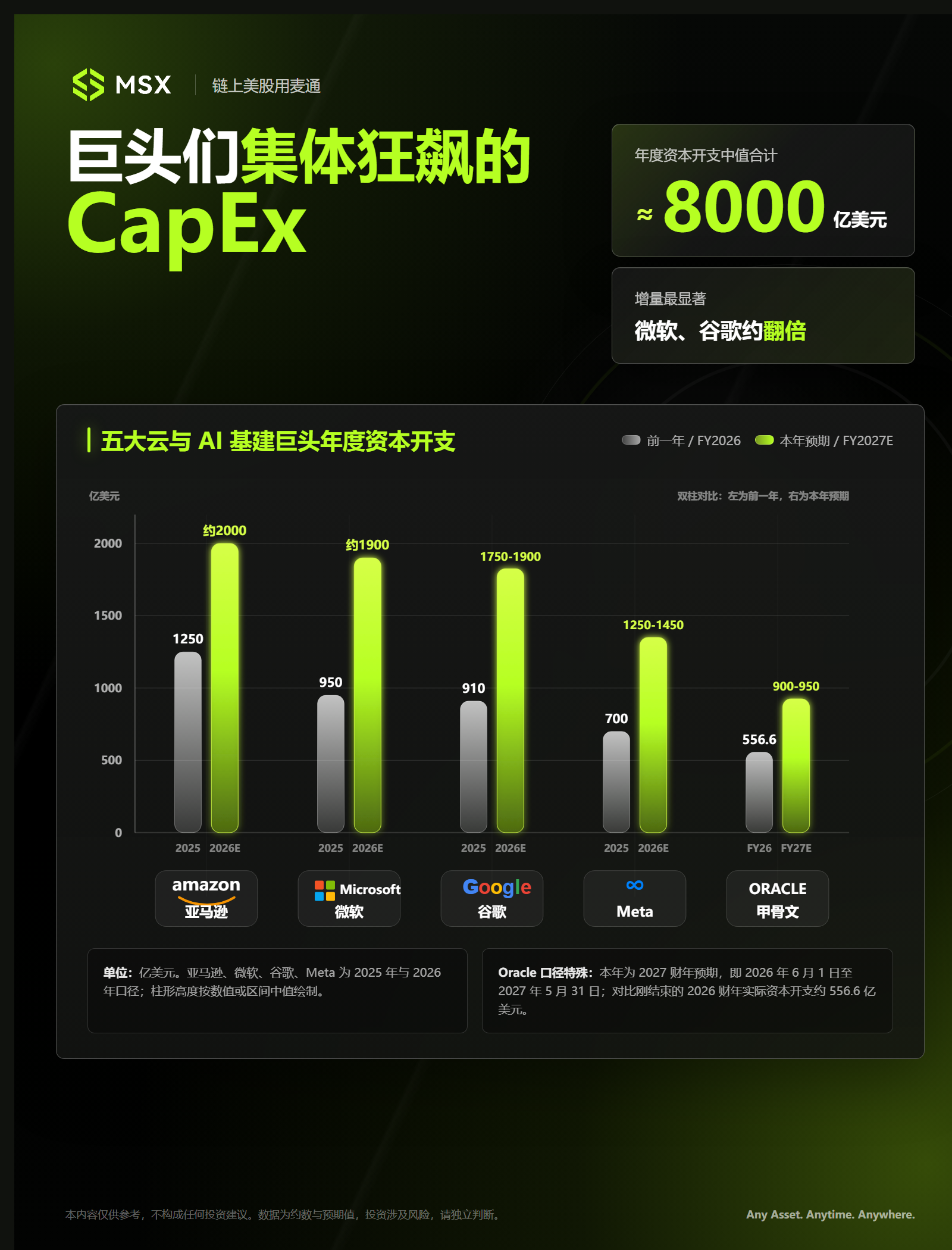

According to estimates from Bridgewater, the investments of Alphabet, Amazon, Microsoft, and Meta for expanding AI infrastructure are expected to be about $650 billion in 2026, an increase of nearly 60% compared to about $410 billion in 2025, while Reuters in May cited estimates from Goldman Sachs and Morgan Stanley showing that global AI-related capital expenditures covering data centers, power, equipment, and software may reach about $800 billion in 2026.

In a sense, this is a "delivery battle" Plus version in the AI world.

Among them, Meta has not only not contracted but has instead pressed the accelerator.

It previously raised its 2026 capital expenditure guidance from $115 billion to $135 billion, to $125 billion to $145 billion. As of the end of the first quarter of this year, Meta also had about $237.7 billion in non-cancelable contract commitments (though these are contract obligations to be fulfilled over many years), a significant portion of which relates to servers, data centers, networking infrastructure, and third-party cloud computing power.

Therefore, strictly speaking, Meta's current consideration of selling part of its computing power does not mean that it suddenly judges that the entire industry no longer lacks computing power, nor does it equal that it is ready to exit the AI arms race. On the contrary, precisely because the construction cycle of data centers often lasts for several years, Meta must prepare capacity in accordance with more aggressive demand scenarios in advance, but once the infrastructure is built ahead of time, the internal needs for models, products, and traffic may not be able to perfectly keep up at the same time, which may lead to occasional mismatches in supply and demand.

To put it plainly, Meta is preparing for a large-scale construction of computing power in the next few years, but currently, as its self-developed models are temporarily not as capable and internal products have not fully operationalized, part of the already available capacity may not be immediately absorbed. Rather than letting these expensive GPUs sit idle in the data center and continue to depreciate, it is better to push them to the external market, maximizing utilization and recouping some costs.

Theoretically, Meta is not the first AI company to sell off its self-built computing power. In May of this year, xAI had already partnered with Anthropic to open access to its Colossus 1 supercomputing cluster, which has over 220,000 Nvidia GPUs, at a price of $1.25 billion per month.

The economic logic behind this is straightforward: resources will ultimately flow to the enterprises that can maximize their value. When a company temporarily cannot fully utilize its computing power, as long as another company is willing to pay a sufficiently high price, the most rational choice is not to let the GPUs gather dust in the data center but to rent them out for monetization.

However, Meta's representative significance far exceeds that of xAI.

Because Meta does not lack user entry points. Facebook, Instagram, WhatsApp, Messenger, and Threads together form one of the world's largest consumer internet product matrices. Theoretically, it should be one of the easiest companies to embed AI models into existing products, forming a user flywheel and absorbing computing power.

However, at least at this stage, Meta has not yet smoothly linked its models, products, cloud services, and user entry points like Google has. This has created a rather ironic contradictory image—Meta is simultaneously constructing its own AI infrastructure on a large scale while still needing to procure external models and computing power services like Gemini. Just days ago, there were reports that Meta's demand for the Gemini model and computing resources was so great that Google could not fully satisfy it, and some internal AI projects were even affected as a result.

At first glance, this seems contradictory, but fundamentally, it reflects a mismatch between long-cycle supply and short-cycle demand, primarily due to its current large model application and immediate inference needs, as self-developed models cannot yet fully replace external solutions and still rely on suppliers like Google.

Therefore, the simultaneous occurrence of "procuring external computing power" and "selling part of its own computing power" by Meta is not contradictory. The real question is whether the computing power it possesses can match the truly competitive models and products at the right time and in the right form, meaning Meta was overly optimistic about its capabilities, built too much computing power, leading to its own models/products being surplus, and could only sell them.

2. Is it really a lack of computing power or a lack of models and products that can effectively utilize that computing power?

After Meta announced its plan to sell computing power, the market's reaction was very interesting.

Meta's stock price surged over 10% during the day, eventually closing up 8%; on the other side, CoreWeave and Nebius plummeted 13% and 17%, respectively; by the next day during the Asian trading session, the sell-off continued to spread to AI hardware, with the Korean KOSPI dropping about 7% at one point, and Samsung Electronics and SK Hynix both falling over 8%.

The phrases "cloud down, hardware down, software up" became the most intuitive market expression at that moment.

This reaction seems to be logically consistent at first glance:

- For Meta, this is definitely a short-term positive: If its self-developed models and internal products cannot temporarily absorb all the computing power, then leasing part of the resources externally or providing managed model services similar to AWS Bedrock would allow the infrastructure, which would otherwise only depreciate, to recover some costs through cloud services, essentially adding a layer of safety to its hundreds of billions in capital expenditures. At worst, it can learn from Apple, hold onto traffic, and collaborate directly with the top external model products, after all, Zuckerberg is not new to the "tail cut for survival" scenario;

- However, for CoreWeave and Nebius, this is like a thunderclap on a clear day: Meta was originally a major client. Just in April, CoreWeave had just added about $21 billion to its long-term computing power agreement with Meta, extending the contract until 2032; the related agreement between Nebius and Meta reached up to $27 billion. In the blink of an eye, the super big spender that was sitting across the table signing contracts moved their chair to the same side and began competing with them for subletting business, which obviously isn't good;

The sense of urgency in the hardware industry chain comes from a deeper market logic: If even a giant like Meta is starting to sell computing power, doesn't that imply that computing power is on the verge of oversupply? Are the giants about to lower their capital expenditures?

However, we must clarify a core fact: Meta's internal excess computing power does not equate to the entire tech industry's peak in computing power, and actually, it is a huge misunderstanding.

If we broaden our perspective to the super long cycle of 3 to 5 years, we will find that the expansion plans of large-scale cloud providers are still advancing along an almost crazy compounding curve. To get a clearer view of the endgame of this arms race, MSX Maitong has also conducted a quantitative comparison of the computing power capacities of the core players worldwide for the next few years.

First, let's look at Meta itself. By the end of 2025, external estimates suggest that Meta will have roughly equivalent AI computing power to 2 million to 2.5 million H100s (corresponding to about 2GW). Following its 2026 capital expenditure guidance, it plans to add 2-3 GW of computing power in a year. Thus, by the end of 2026, Meta's total computing power should be around 5GW.

5GW sounds substantial, but when placed before the industry's demand, it becomes insignificant, as the real demand anchors are planned in completely different magnitudes:

- Google: In May, The Information revealed stunning news that Anthropic pledged to invest $200 billion in Google Cloud for TPU computing power over the next five years; this part of computing power alone is at the 5GW level. If we conservatively speculate Anthropic accounts for 25% of Google Cloud demand, then Google Cloud alone will need to reach around 20GW in total computing power by 2028, and the overall figure for Google could reach 25GW;

- Amazon: Similarly, relying on 5GW from Anthropic and 2GW from OpenAI, combined with its internal plan to double its computing power capacity in 2027 compared to 2025 (which stands at 6.5GW), the overall demand is also at the 20GW level;

- Microsoft: Tied to a $250 billion Azure contract with OpenAI, estimated similarly, corresponds to a demand exposure of about 20GW. Not to mention OpenAI itself has independent deployment plans for Stargate, 10GW with Nvidia, and 10GW with Broadcom (though these have yet to be fulfilled), none of which have been fully included in the cloud providers' computing pools;

Putting these groups of data together, the conclusion is clear and even somewhat cruel—if Meta opens up all its 5GW computing power by the end of 2026, compared to the new computing power plans in the next three years, often exceeding 10GW or even 20GW, it is merely a drop in the bucket.

Meta surely knows this conclusion as well, the driving force behind the industry's computing power construction is already the demands of large-scale models from Google, Anthropic, and OpenAI. Whether Meta's models stay on the table does not affect the direction of this train's advance at all.

Since the industry does not lack demand, why does Meta still have excess computing power? This exposes an incredibly painful question: how can one hold the world's top traffic users and still not use up its own 5GW of computing power? What the market truly lacks is not computing power, but the models and products that are capable of effectively utilizing that computing power?

From this perspective, we can even think that Meta's rental of computing power does not necessarily serve as a leading indicator of overcapacity, but rather may reveal the current state of extreme thirst for computing power in the market:

Just look at the pricing for xAI renting computing power to Anthropic—$1.25 billion/month for 500MW capacity. Calculated, that means $30 billion/GW/year, indicating that even if a player temporarily "leaves the table" for various reasons, the bit of idle computing power they free up will be instantly gobbled up by those front players who have stronger model capabilities and shorter monetization paths.

Thus MSX Maitong believes that Meta's action is not definitively the first warning of loosened computing power supply. We shouldn't jump to conclusions too quickly; what we really need to observe is whether this released computing power will be instantly snatched up, and whether the transaction prices remain sufficiently high. If everything goes as anticipated, it may actually prove that AI computing is still extremely tight.

At this point, the deeper logic behind "cloud down, hardware down, software up" begins to truly emerge, which means that the market is not trading "excess computing power," but rather trading the reconstruction and migration of the value of computing power within the industry chain.

3. What is the real "ghost story" that the market should be afraid of?

There is one thing that is easily misunderstood, which is that Meta selling computing power does not mean Zuckerberg is giving up on the AI arms race completely.

On the contrary, the more Meta relies on external models like Google and Anthropic, the more its product ecosystem and advertising profit margins become susceptible to limitations. The struggle between AWS and Anthropic has already illustrated this problem—once model companies truly master user relationships and core demands, even cloud vendors with large infrastructures may be forced to compromise on profit distribution.

Zuckerberg cannot be blind to this; otherwise, he wouldn't be reorganizing the new management team while also hard-launching the closed-source MuseSpark model to build barriers, while simultaneously revising capital expenditures upward, continuing large-scale acquisition and layout.

Since Meta hasn't thrown in the towel, why has the market reacted so violently? Because this has opened the curtains on the migration of the underlying pricing logic within the industry, which is the real "ghost story" that the market should be concerned about.

As mentioned earlier, for the past two years, the estimation logic driving the entire AI bull market is: the ROI of AI is uncertain, but the CapEx of AI is absolutely certain. So long as the giants continue to madly purchase chips and build facilities, the upstream businesses—Nvidia, optical modules, and the semiconductor industry chain—can lie back and enjoy a risk premium with certainty.

"As long as AI giants expand CapEx, everything will be fine."

However, now, this ghost story is undergoing two layers of terrifying qualitative change.

The first qualitative change is that while the ROI of AI remains uncertain, the CapEx of the giants is starting to become a bit uncertain. Since Meta's stock surge, the capital markets have begun to reward those giants who sell surplus computing power and understand how to control depreciation costs, with the implication being clear—everyone is now reckoning "who is wasting money ineffectively."

Once this aesthetics of "computing return" becomes mainstream, the lists of giants voluntarily conceding or temporarily slowing down the arms race will lengthen, leading to a direct collapse of the high growth certainty bubble in the upstream hardware sector.

The second qualitative change is that this risk has not yet been fully reflected in the valuation premium of semiconductor hardware manufacturers. The anxiety regarding return rates has successfully suppressed the valuations of cloud vendors like Mag7, but the chip and hardware segments responsible for manufacturing "shovels" have still maintained highly optimistic perpetual growth expectations.

As long as the market begins to shift towards the belief that "unlimited competitive races for computing power are unnecessary," the supply-demand balance of computing power resources will undergo dramatic structural loosening in certain areas.

In summary, Meta's issue isn't that its computing power lacks value, but rather that its models and products have not yet fully utilized all that value. When the scarcity premium of computing power begins to be reevaluated, the market will naturally reduce its blind chase for "how many GPUs one owns," turning instead to those who can genuinely transform computing power into products and revenue.

After all, for software and application companies, increased computing power supply and reduced inference costs could lower the thresholds for developing and deploying AI, thus, funds may not necessarily leave AI; they are simply shifting from "who hoards the most computing power" to "who best utilizes computing power."

From this angle, the Meta incident is temporarily not evidence of the end of the AI bull market, but it does serve as a wake-up call for the market: previously, capital markets were only concerned with whether there was enough computing power, and moving forward, they will also have to care about where that computing power ultimately flows and who can make the most money from it.

This also implies that when resources begin to concentrate towards a few leading model companies, the all-out competition in the AI industry may just be getting started.

Final Thoughts

From Claude's breakout to the impressive catch-up of domestic models like GLM, the capital markets have never scrimped on offering high premiums for top-performing large models.

Thus, as giants push idle computing power to the external market, this indirectly lowers the entire industry's thresholds for inference and development, potentially being a long-awaited boon for software and application companies.

Therefore, the Meta incident is by no means the death knell for the AI bull market. However, it indeed serves as a reminder for everyone: the phase of barbarically piling up hardware in the AI industry has peaked, and resources are accelerating towards a select few top players capable of achieving an efficient loop of "computing power-model-product-revenue" in an irreversible momentum.

This winner-takes-all elimination race in the era of large models has only just begun.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。