Key Summary

- This article comes from Tiger Research, indicating that the current status of crypto payment cards is similar to debit cards on the eve of commercialization in the 1990s: both utilize existing payment networks to bypass merchant acceptance. However, the everyday financial relationships built around bank master accounts (such as payroll deposits and regular deductions) have yet to form.

- The annual transaction volume of crypto payment cards is approximately $18 billion, with RedotPay holding more than half of the market share, and users concentrated in emerging markets. At this stage, crypto payment cards are merely a supplementary tool in regions with a scarcity of dollar acquisition channels, far from forming universal financial infrastructure.

- Relying solely on the growth of payment transaction volume cannot establish the infrastructure status of crypto payment cards. The market pattern will ultimately be determined by three types of players: platforms that control the flow of funds, service providers that seize unaddressed areas of traditional finance, and companies that build core account relationships on top of underlying payments.

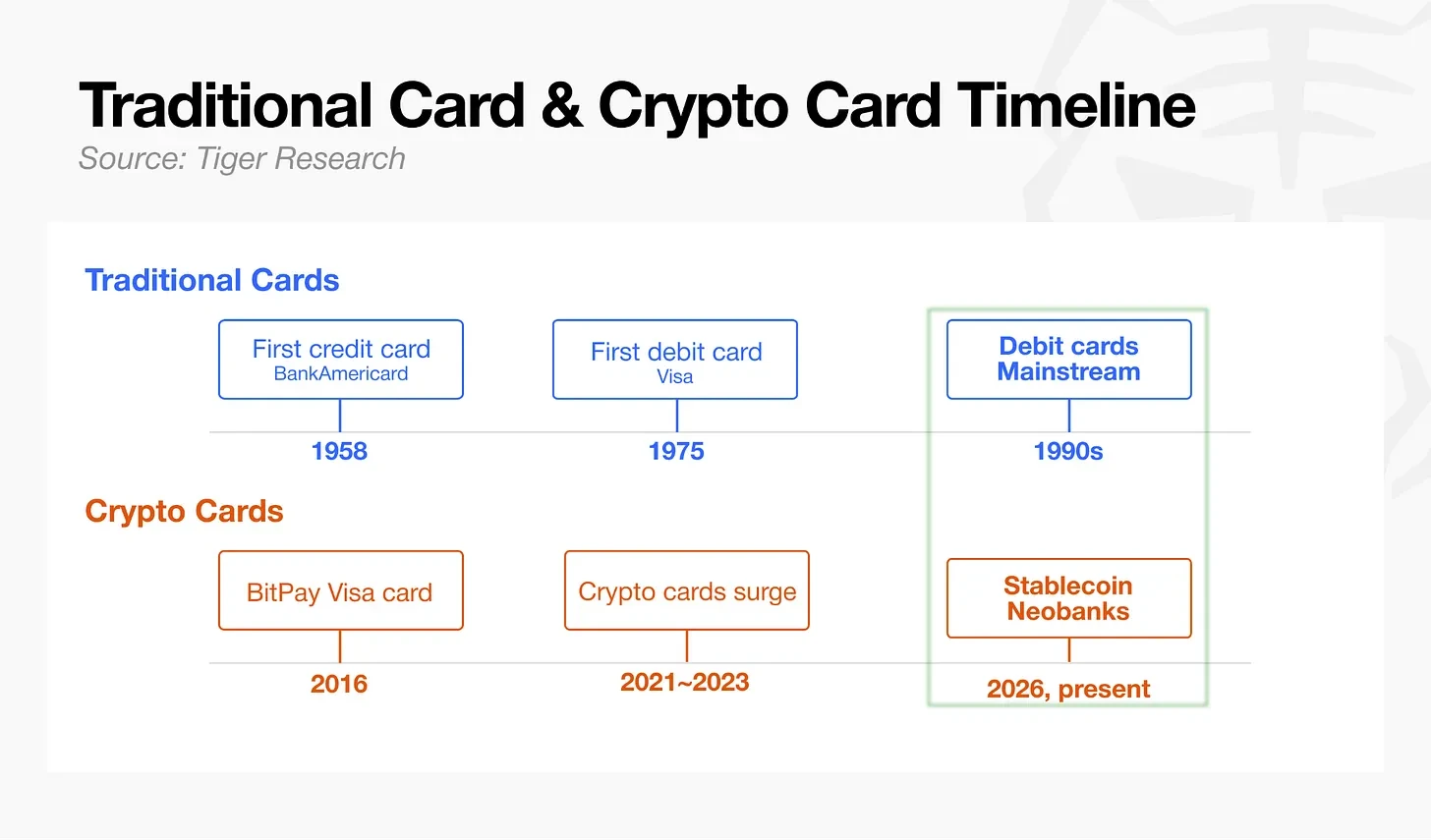

Parallel World of Debit Cards in 1990

In September 1958, Bank of America mailed credit cards to 65,000 residents in Fresno, California, which was the first payment card without supporting underlying infrastructure. After a year of operation, the business was bleak, with a default rate of 22% and losses reaching $20 million. The industry took 15 years to build an electronic settlement system, and debit cards were only officially introduced 17 years later, while Visa took a full 20 years to establish a globally accepted payment standard.

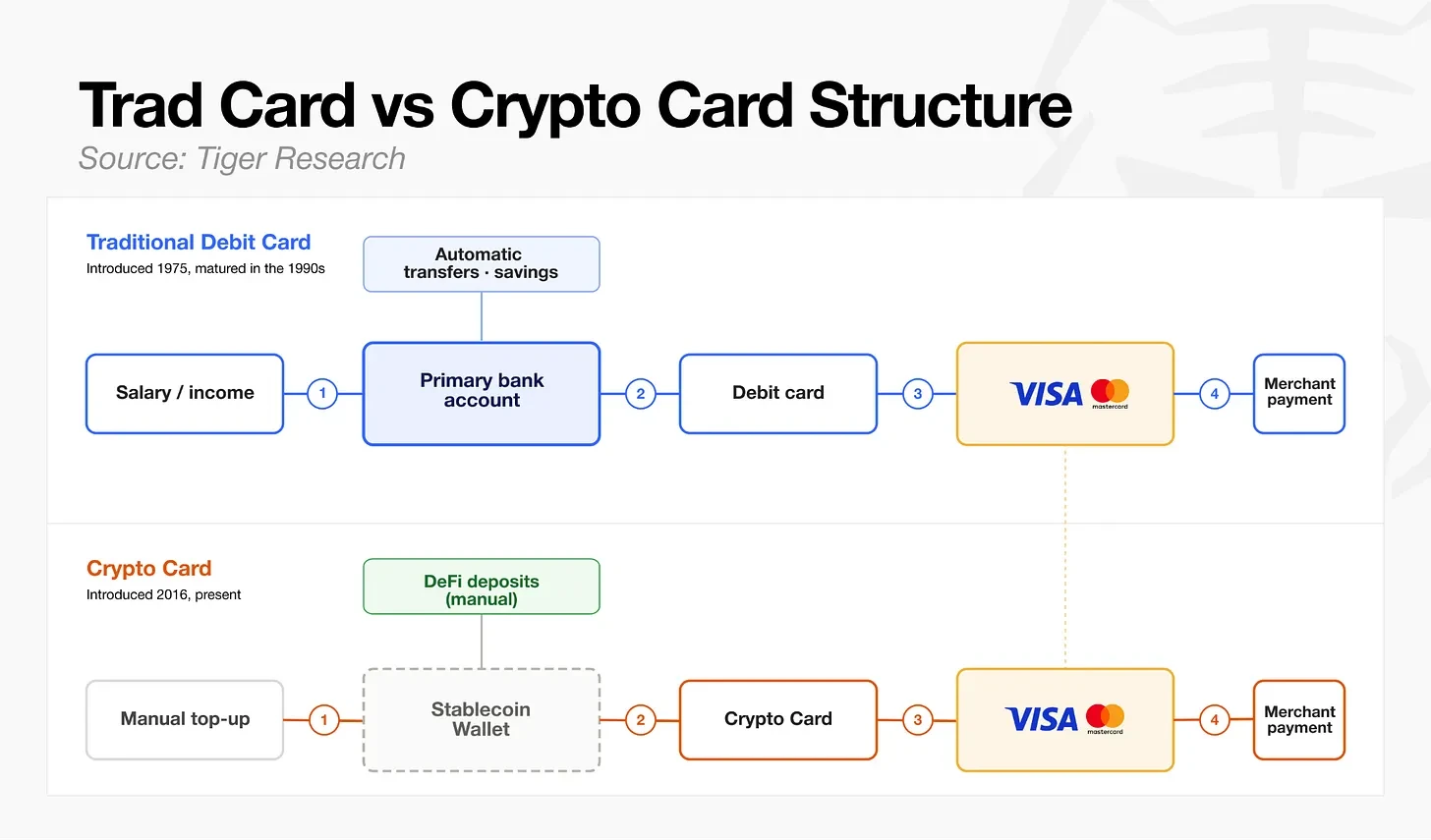

The biggest dividing line between traditional payments and crypto payments lies in whether user financial account relationships are established as a norm. Debit cards were born in 1975 and only became standard tools for personal core bank accounts after the increase in payroll remittance in the 1990s. In contrast, the current crypto payment cards have funding channels mainly reliant on users self-recharging stablecoins; the vast majority of crypto wallets cannot accommodate payroll deposits, regular deductions, and other day-to-day transactions, placing the overall development of the industry roughly on par with that of debit cards in the late 1990s.

In the future, the leaders in the crypto payment card space will not be determined by the number of cards issued, but by who first builds a core account that truly serves daily income and expenditure or finds growth points that drive user retention in the long term.

Monthly Transactions of $1.5 Billion Do Not Represent Industry Maturity

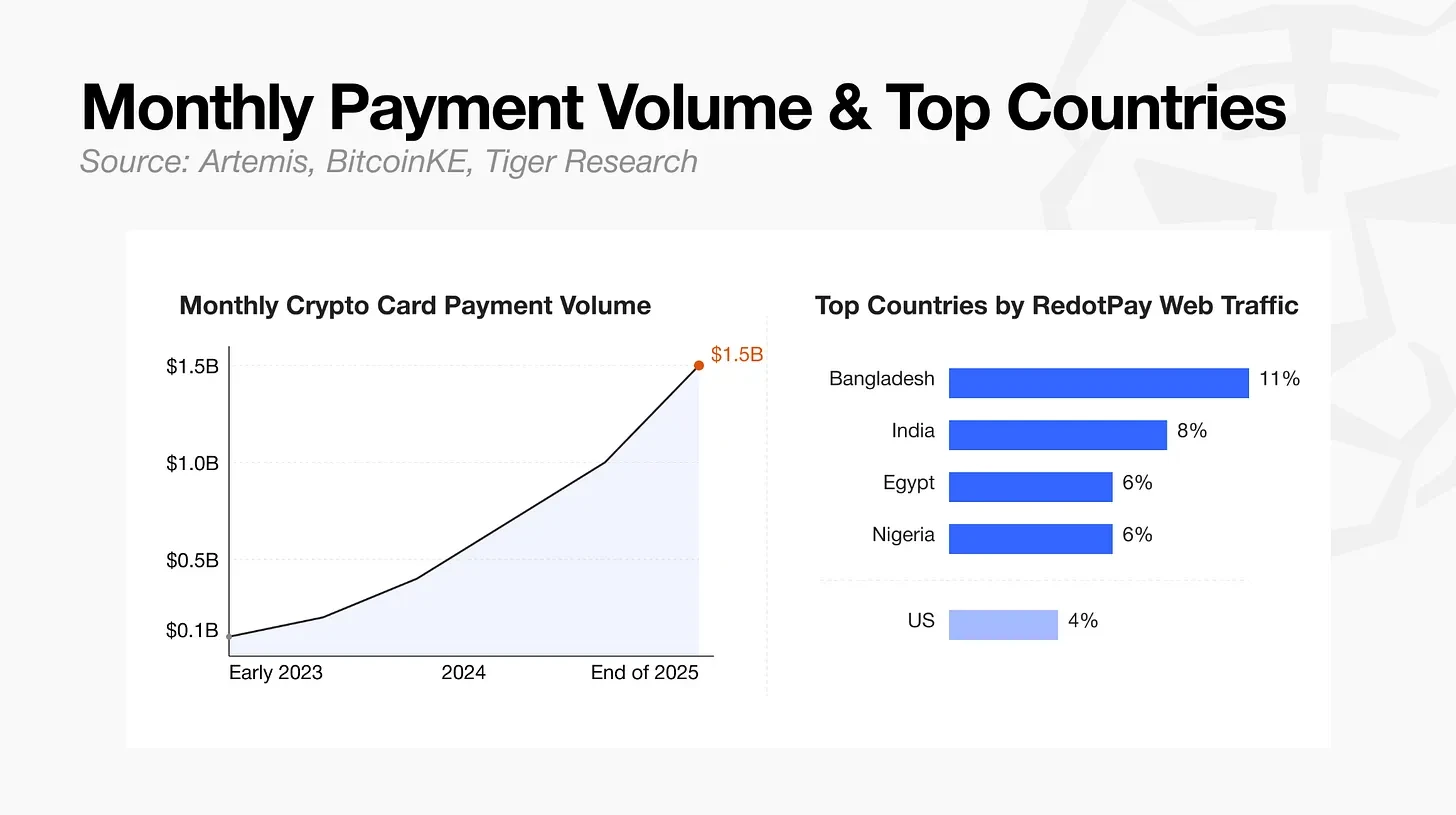

Data agency Artemis reports that the monthly transaction volume of crypto payment cards grew from $100 million at the start of 2023 to $1.5 billion by the end of 2025, with an annualized scale of approximately $18 billion. Affected by the statistical scope of on-chain data, the actual annualized values may fluctuate slightly, but the explosive growth of transaction volume is a fact.

A detailed analysis of these metrics reveals pronounced centralization in services and regions. Leading service provider RedotPay accounts for more than half of the entire industry's transaction flow; platform user visits are highly concentrated in emerging markets, with Bangladesh at 11%, India at 8%, Egypt at 6%, Nigeria at 6%, and the United States accounting for only 4%.

Thus, it is apparent that the real demand for crypto payment cards does not stem from developed mainstream markets, but from under-served areas in developing regions where financial services are lacking and channels for acquiring dollars are limited.

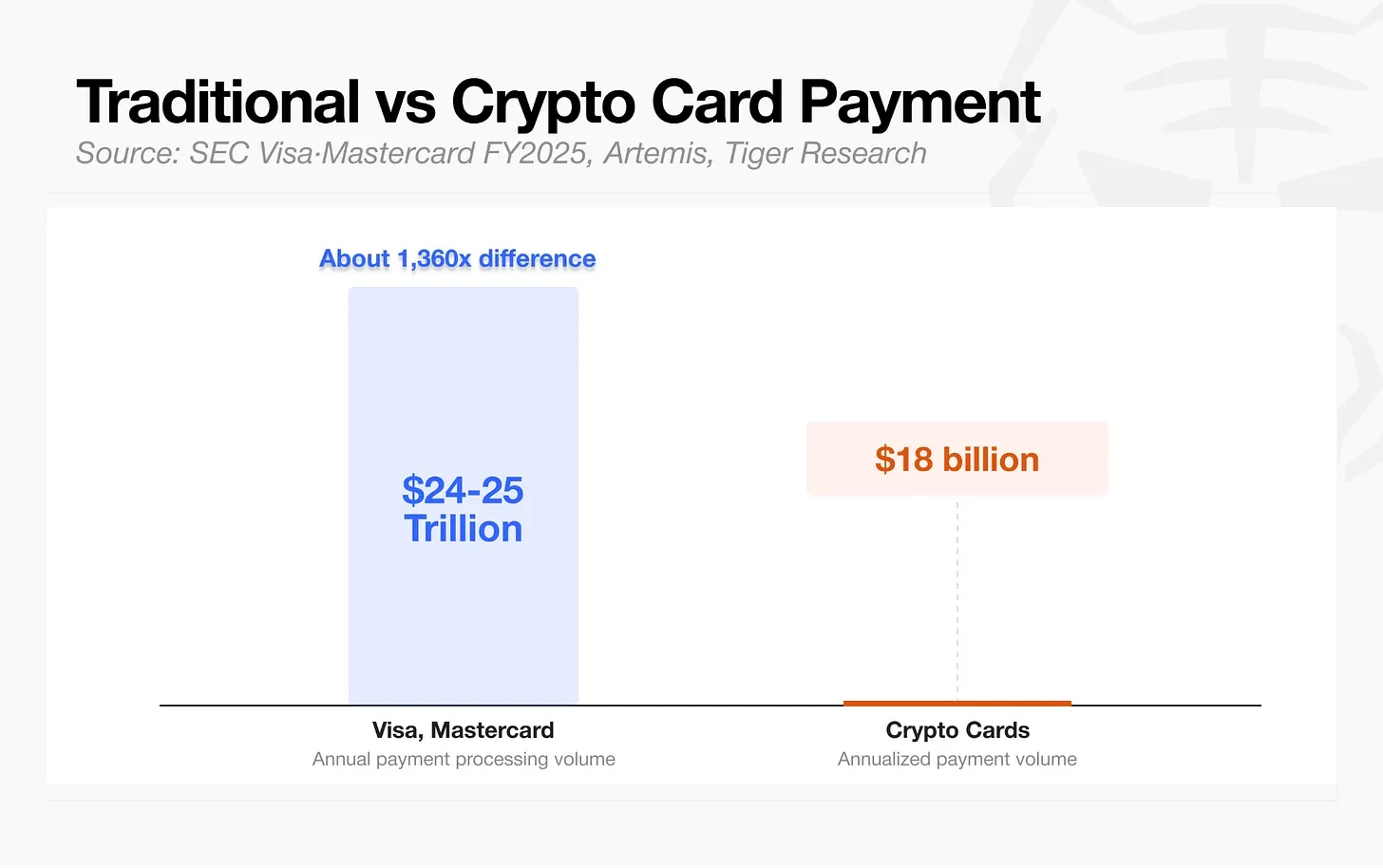

Compared to mature financial networks, the scale gap with cryptocurrencies remains enormous. The annual payment volumes of Visa and Mastercard reach $24 to $25 trillion, while crypto payment cards achieve only $18 billion in annualized transactions, with the two being completely incomparable.

The velocity metrics for assessing the prevalence of everyday payments are also low. Visa reports that the retail circulation velocity of on-chain stablecoins is just 0.08, only one-twentieth that of the narrow definition of M1 money supply velocity (1.65). The use of stablecoins is not a normalized flow of payroll deposits, everyday consumption, and recurrent recharges, but rather more like one-time recharges followed by intermittent card usage.

Growth in transaction volume does not equate to a mature universal clearing system in the market. Currently, a significant amount of transactions from crypto payment cards comes from emerging market users who cannot conveniently open dollar accounts, making these crypto cards indeed hold practical financial value for such users.

However, in developed markets, crypto payment cards have yet to find a stable product-market fit and have not established deep account binding relationships that payroll remittance and automatic deductions create.

Considering both the channels for capital inflow and consumption scenarios, current crypto payment cards are more suited to specific segmented needs of certain countries, serving as supplementary tools rather than universal financial infrastructure. Nevertheless, under the backdrop of high-speed industry growth, leading players across the four major business models are simultaneously enhancing various segments of the industrial chain.

Four Major Business Models of Crypto Payment Cards

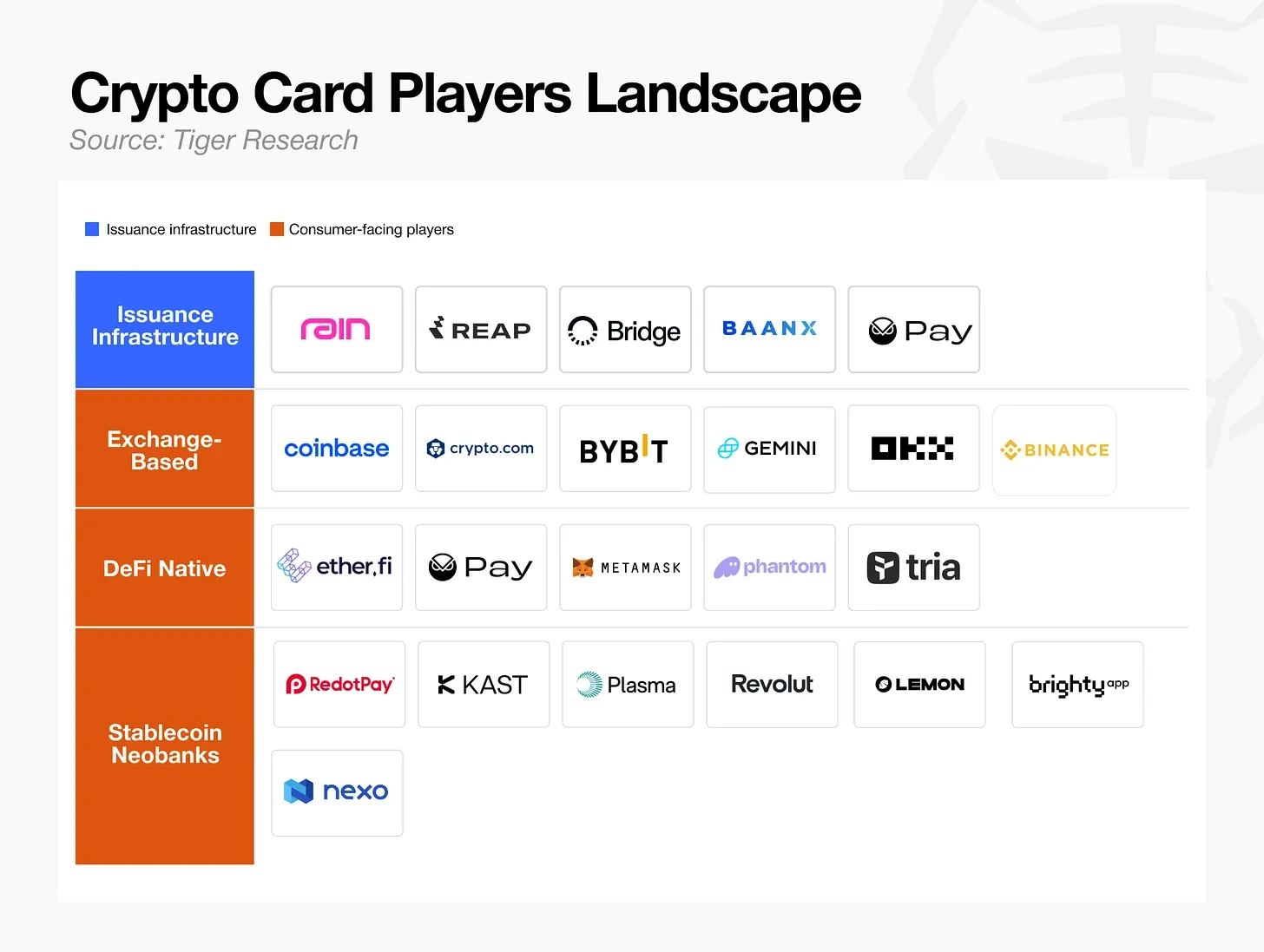

The crypto card industry can be roughly divided into four business models, with various participants competing to seize opportunities at different levels. These models vary, ranging from companies focused on providing backend infrastructure to those merely borrowing the card form but with entirely different underlying structures.

Card Issuance Infrastructure

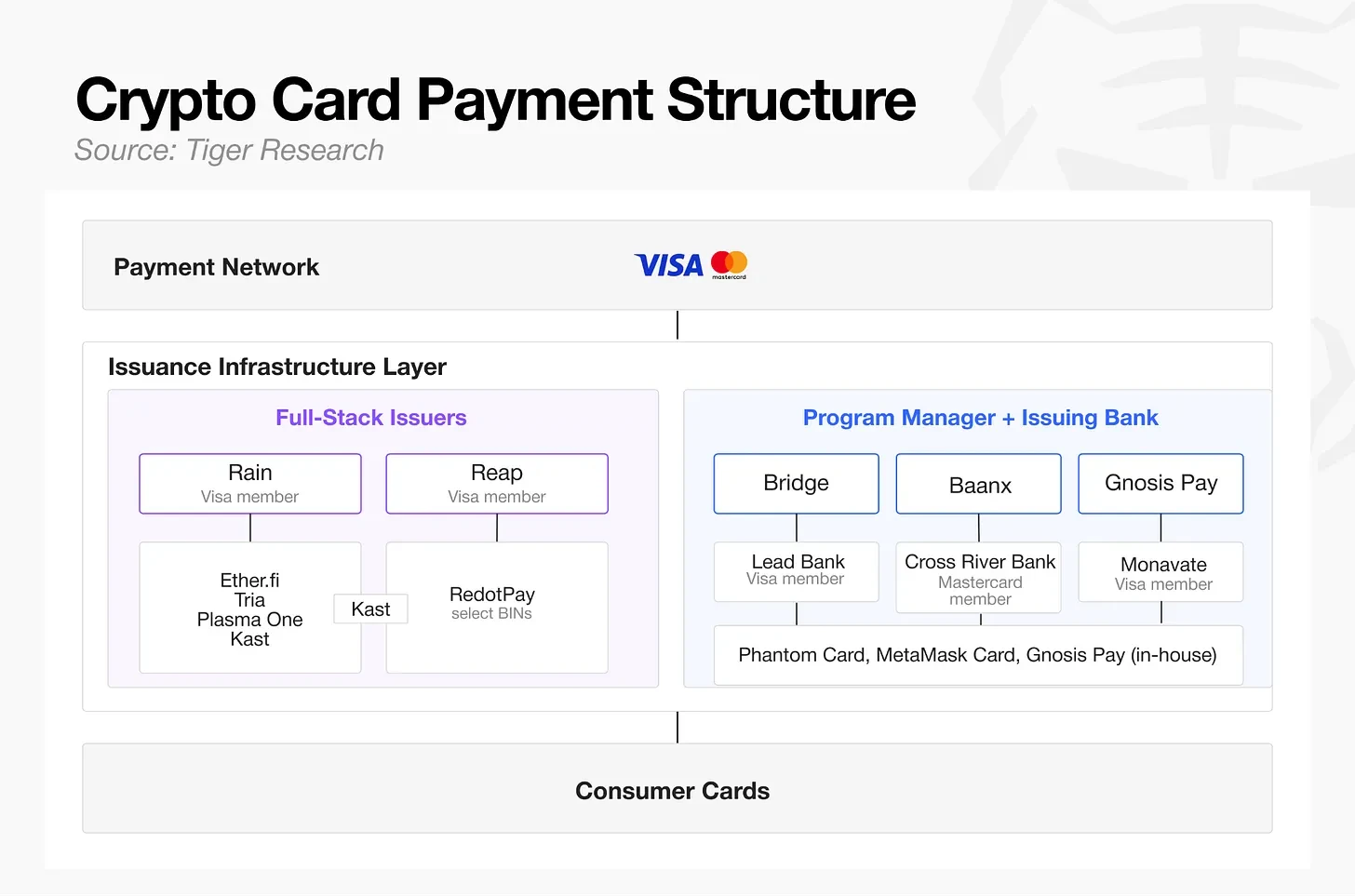

Visa and Mastercard, the two well-known payment networks, also apply to the cryptocurrency card ecosystem. Beneath them is the card issuance infrastructure layer, ultimately extending to consumer cards. As illustrated above, two structures exist within the card issuance infrastructure layer. The first is a traditional two-tier structure, where the project management entity responsible for operations is separate from the issuing bank that manages membership and settlements. The second is a full-stack issuer, such as Rain and Reap, which combines both roles.

Many seemingly independent payment card brands share the same few project service providers at their core, with Phantom Card, MetaMask Card, and Gnosis Pay being typical examples.

Seemingly independent payment card products like Kast, Ether.fi, Tria, and Plasma One also share a small number of underlying infrastructure service providers, with Rain handling the vast majority of consumer card business.

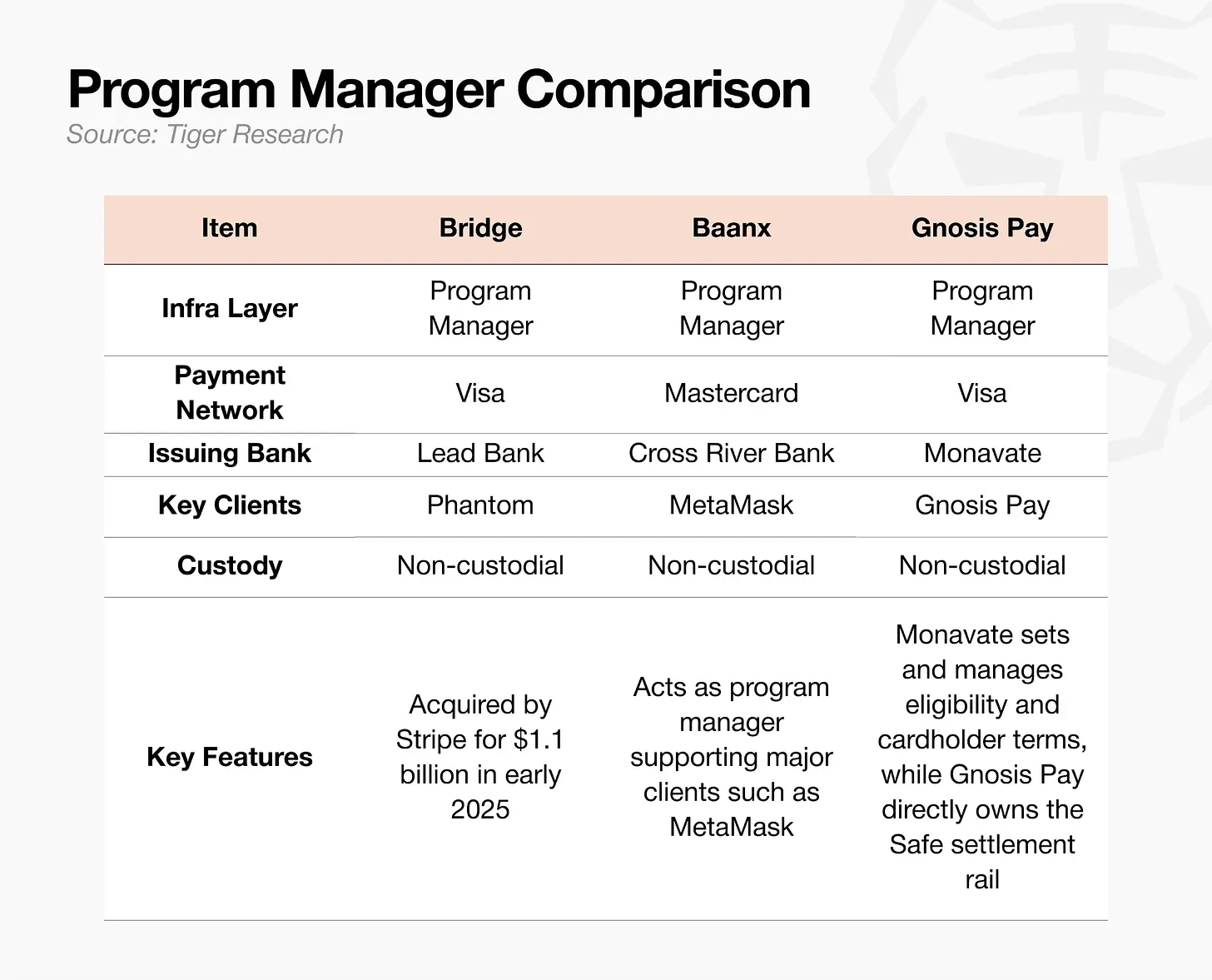

The high concentration of card issuance infrastructure also attracts traditional digital banks with mature experience to enter the fray. In March 2026, Nium launched a stablecoin issuance platform supporting both Visa and Mastercard networks; other traditional financial infrastructure vendors include Bridge, acquired by Stripe for $1.1 billion in early 2025, and BVNK, which Mastercard acquired for up to $1.8 billion in March 2026.

With increased competition in the card issuance track, full-stack issuers, well-established project service providers, and emerging fintech firms are competing on the same stage, making it difficult for pure card issuance businesses to build high barriers to entry.

Rain has differentiated itself by achieving T+0 settlement for stablecoins through Visa, drastically improving the capital turnover efficiency for partner platforms like Ether.fi, overcoming the long traditional card settlement cycle of several days. Recently, the platform introduced AI-powered layers for automatic generation of disposable virtual cards, extending capabilities beyond basic card issuance infrastructure.

Card issuance service providers wanting to break through must not only provide foundational payment channels but also quickly implement differentiated value-added functions that traditional infrastructure cannot achieve.

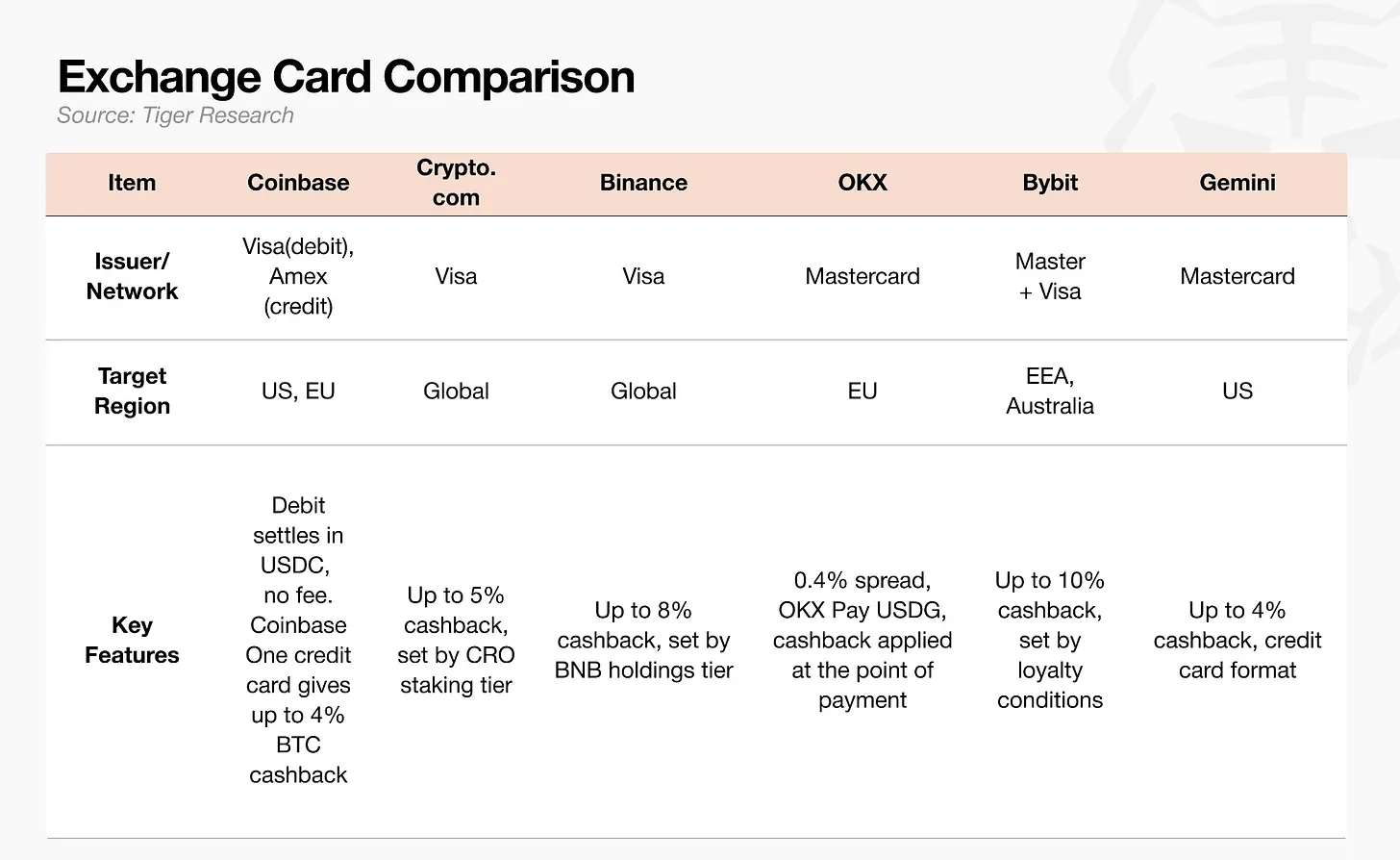

Exchange-Supported Payment Cards

For exchanges, payment cards are not a core source of income; their primary role is user retention. By leveraging existing users, assets, and trading data, they add card functionality to prevent user attrition. Platforms' real revenue comes from trading fees, lending businesses, and asset custody, rather than from card consumption itself.

Exchanges view payment cards as a traffic entry point to create financial super applications. However, the platform's own token cashback model carries risks; price volatility of tokens directly leads to unstable actual cashback percentages.

Alternative industry solutions include stablecoin cashbacks and interest on balances, but the U.S. "GENIUS Stablecoin Act" prohibits interest-based services, posing an obstacle to market expansion.

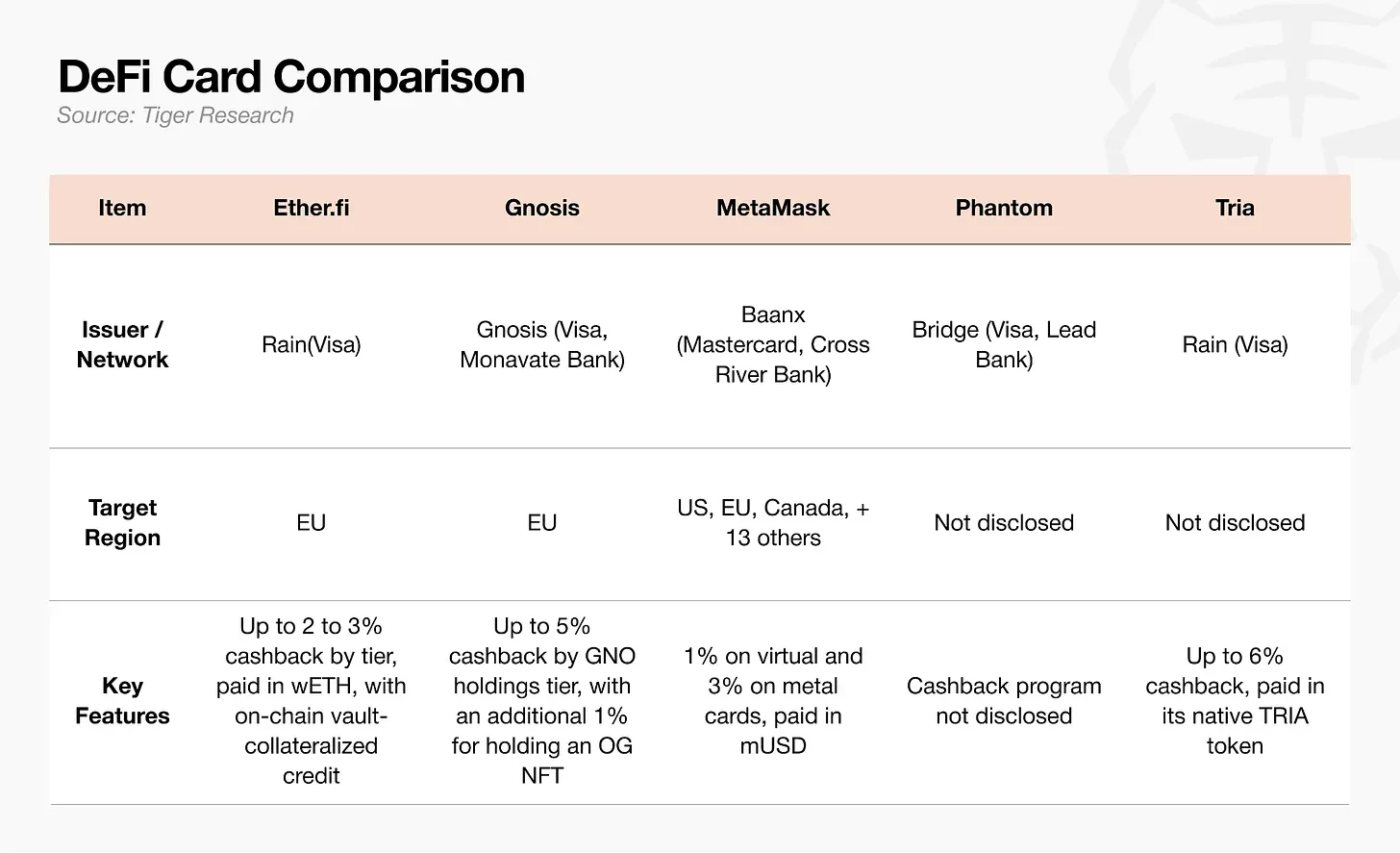

Decentralized Wallets DeFi

The core logic of this model is that the wallet itself acts as the user account, with assets self-custodied on-chain, eliminating the need for centralized exchanges, and card consumption settling directly from on-chain assets. At the same time, it offers credit limits, with assets potentially serving as collateral.

However, users need to build vaults, manage collateral, and monitor settlement risks, resulting in a high operational threshold that limits the scale of the user base for this model.

When making payments, the system real-time converts on-chain assets to fiat currency for settlement, with each transaction incurring on-chain gas fees; during periods of insufficient throughput on public chains or network congestion, fees may exceed the consumption amount, causing frequent delays in transaction authorization.

Therefore, MetaMask Card has chosen to use its self-developed second-layer network, Linea, reducing single transaction gas fees to about $0.01, alleviating pain points of fees and delays for small payments. Tria employs a gas-free recharge solution, with the platform absorbing the transaction fees incurred during recharges, eliminating the operational costs for users to select public chains and calculate fees.

However, until the model's interaction experience balances self-custody of assets with the convenience of card use to the level of traditional debit cards, users will be limited to native crypto users only.

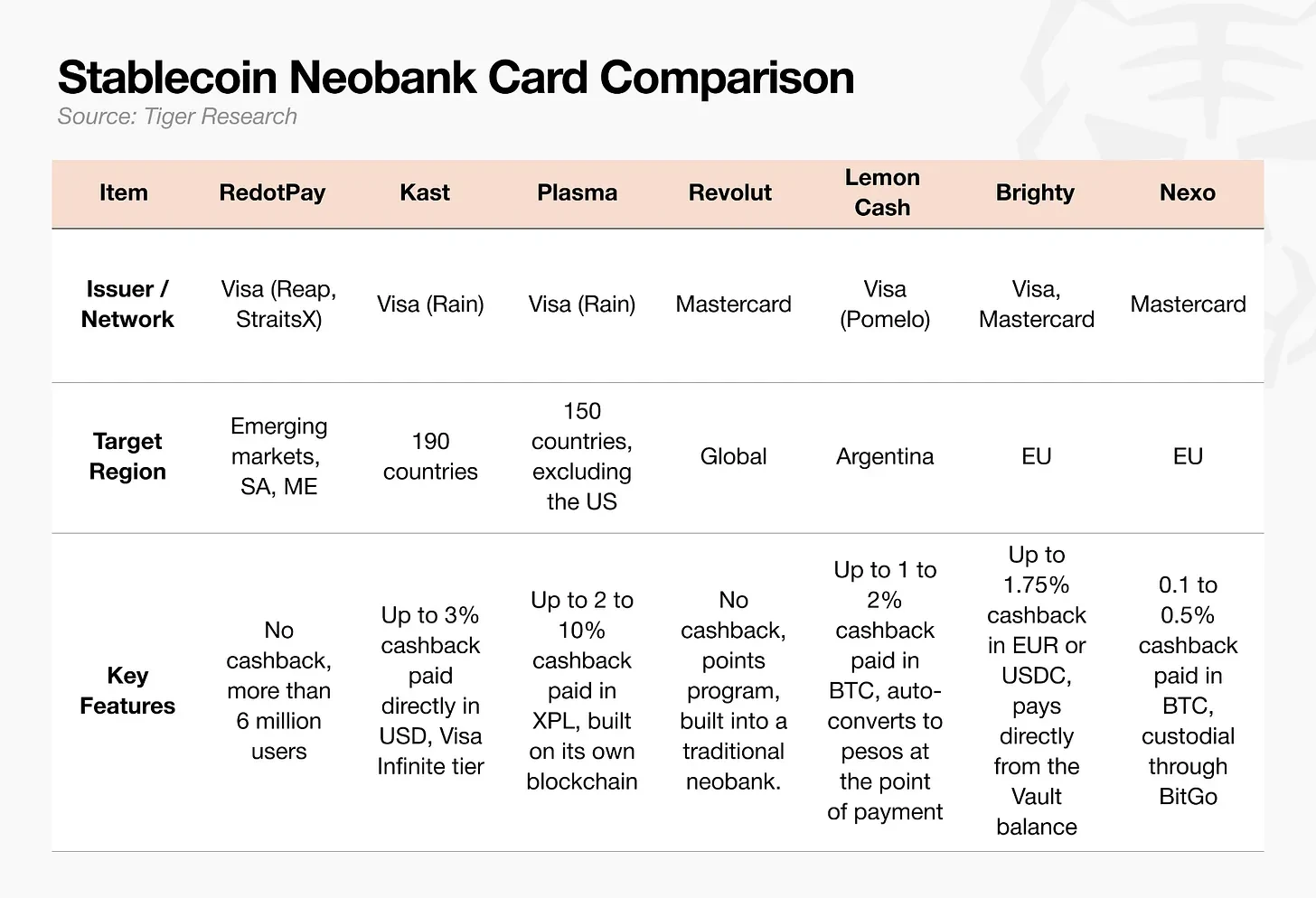

Stablecoin Digital Banks

This is currently the track with the highest market share, focusing on account functionality rather than the card itself. Stablecoin balances integrate foreign exchange, cross-border remittance, and wealth management functions, with payment cards merely serving as consumption carriers. In emerging markets where the value of local currencies fluctuates widely, cross-border remittance costs are high, and acquiring dollars is challenging, this model holds significant competitiveness.

To sustain growth, this track must move away from the "preloaded card" single form, i.e., the model where users autonomously purchase stablecoins to transfer into their balances.

Cashback strategies among platforms are differentiated by market positioning. Industry leader RedotPay and traditional fintech veteran Revolut do not offer cashback promotions at all, while later entrants like Kast and Plasma One vigorously implement cashback in dollars or platform tokens to drive traffic.

However, relying solely on welfare subsidies cannot truly integrate crypto payment cards into users' everyday consumption.

Single Payment Functionality Cannot Support Long-Term Development

The development history of traditional bank cards and digital banks proves that the profitability ceiling for pure payment services is extremely low. These enterprises can only achieve profitability by integrating concepts of main accounts and profits from deposits and loans into their business models. The crypto payment card industry is now at the same critical development juncture, but global regulatory rules like the U.S. "GENIUS Act" and the EU MiCA restrict the development of stablecoin interest and asset management businesses, making breakthroughs exceedingly difficult.

Under macro regulatory constraints, industry players seeking long-term survival must seize three core strategies:

- Directly control the flow of funds;

- Secure unique application scenarios in emerging markets;

- Build proprietary user account systems that cannot be substituted by underlying infrastructure providers.

As industry standards form, firms that cannot achieve the above three points will gradually fall behind.

Looking back at the history of debit card development, the firm that ultimately dominated the market was not the one issuing the most cards, but the one that first controlled users' primary bank accounts. The crypto payment card industry is now facing exactly the same proposition.

Crypto card operators need to directly control the flow of funds upstream of the Visa payment process, seizing opportunities in segmented markets, and, like the rise of bank accounts in traditional finance, control consumer infrastructure. This means establishing a global standard without any precedent to follow.

If the above points are not achieved, crypto payment cards will never become essential tools integrated into everyday life, but will instead remain prepaid cards used by niche groups for small rebates.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。