In-Depth Analysis of the Cryptocurrency Market

Author: Michael Nadeau

Recently, the sharp decline of Bitcoin and various altcoins has plunged the entire market sentiment into a state of "extreme fear." In just one month, expectations for a raging bull market have turned into the acceptance of "maybe the bear market has really arrived." Investor sentiment has fluctuated like a roller coaster, with confidence ruthlessly crushed amid severe price volatility.

Is there still a bullish reason for cryptocurrencies in 2025? Has this bull market cycle really come to an end? Michael Nadeau, founder of The DeFi Report, provides his analysis and views, as follows:

01

Review of This Cycle

Before diving into on-chain data, I would like to share some qualitative analysis on how we think about cryptocurrency cycles.

1. Early Bull Market Phase

This period spans from January 2023 to October 2023.

This is the time when the market bottomed out after the FTX incident. The crypto market became very quiet (low trading volume, silence on crypto Twitter). Then we began to rise again.

Bitcoin (BTC) rose from about $16,500 to $33,000 during this time.

However, no one called this a bull market. During the "early bull market," most market participants were still on the sidelines.

2. Wealth Creation Phase

This period spans from November 2023 to March 2024.

This is when we saw some big moves and significant wealth creation. Solana (SOL) rose from $20 to $200. The airdrop of Jito (December 2023) created additional wealth effects within Solana and repriced Solana's decentralized finance (DeFi) projects (Pyth, Marinade, Raydium, Orca, etc.). The venture capital market reached a frenzied peak during this time (which is typical).

Bitcoin rose from $33,000 to $72,000. Ethereum (ETH) rose from $1,500 to $3,600.

Bonk rose from a market cap of $90 million to $2.4 billion (26 times). WIF rose from a market cap of $60 million to $4.5 billion (75 times). The seeds of a larger "meme coin season" were sown during this period.

But this period was still quite "quiet." Your "average friend" may not have started asking you about cryptocurrencies yet.

3. Wealth Distribution Phase

This period spans from March 2024 to January 2025.

The "peak of attention" period. We often see "WAGMI" (We're All Gonna Make It) type sentiments, rapid rotations, new trends (quickly fading), and blind risk-taking being rewarded. Celebrities and other "crypto brief participants" typically enter the market during this phase. Crazy headlines like "Tesla buys Bitcoin" or "Bitcoin strategic reserves" often appear during the wealth distribution phase.

Why?

New investors enter the market due to these headlines. They do not realize they have arrived late to the party.

This is the second wave of the "meme coin season," which then evolved into the "AI agent season." During this time, the market ignored many obviously problematic behaviors. No one wanted to point out any issues. Everyone was making money.

Now, this brings us to today.

4. Wealth Destruction Phase

We believe we entered this phase shortly after Trump took office.

This is the period immediately following the market peak. Bullish catalysts are now a thing of the past. Seemingly positive news is accompanied by bearish price movements.

In the current environment, administrative actions regarding "strategic Bitcoin reserves" have failed to drive the market—this is an important signal. During this period, rebounds often encounter key resistance periods and fade away (we saw this last week after Trump tweeted about crypto reserves).

Some additional signals we look for in the wealth destruction phase include:

Liquidations and "panic," events that shake the market but have not yet fully awakened it. We saw this in the DeepSeek AI panic and tariff uncertainties.

Investors holding onto "hope." We see a lot of discussions today about the dollar's decline and the rise of global M2 (more on this later in the report).

"Scammer" types entering the market. More people are DMing us to "check out their projects." Advertising capital is flowing more freely in the market. Well-funded projects are spending recklessly at conferences. More player-versus-player (PvP) competition/internal strife. The industry as a whole exudes a more "dirty" atmosphere. Bad actors are starting to be named during the "wealth destruction."

During this time, failed projects will also begin to surface—usually after liquidations. The last cycle began with Terra Luna. This led to the collapse of Three Arrows Capital. Then came the bankruptcies of BlockFi, Celsius, FTX, etc. Ultimately leading to the collapse of Genesis and the sale of CoinDesk.

We have not yet seen any explosive events. We note that this cycle should have fewer explosions—simply because centralized finance (CeFi) companies have decreased. Time will tell. Fewer explosions may lead us to form higher lows when we officially bottom out.

Where might these explosions come from?

No one knows, but my guess is to keep an eye on the usual suspects.

Exchanges: Watch for hidden leverage and/or potential fraud from some "B and C level" exchanges abroad.

Stablecoins: We are watching Ethena/USDe—its circulating stablecoin value is close to $5.5 billion. It maintains its peg and generates profits through cash and arbitrage trading (holding spot assets and shorting futures)—this was a major source of leverage in the last cycle (via Greyscale). Ethena's reliance on centralized exchanges adds additional counterparty risk. Additionally, MakerDAO has also invested part of its reserves in USDe, creating additional cascading risks in DeFi.

Protocols: Watch for an increase in hacking incidents and potential liquidation cascades due to crypto collateral on platforms like Aave—Aave currently still has over $11 billion in active loans (down from a peak of $15 billion).

Microstrategy: We believe they are managing their debt well, as most is long-term unsecured debt or convertible bonds (BTC holdings have no margin calls). Additionally, they were able to withstand a 75% drop in Bitcoin during the last cycle. Nevertheless, a significant drop in Bitcoin prices could pressure Saylor, forcing him to sell a large amount of Bitcoin at the worst possible time.

The best time to re-enter the market is at the end of the wealth destruction phase. We believe that has not yet arrived. Of course, we will notify you when we think it is time to return to the "buy zone."

02

Bearish Reasons

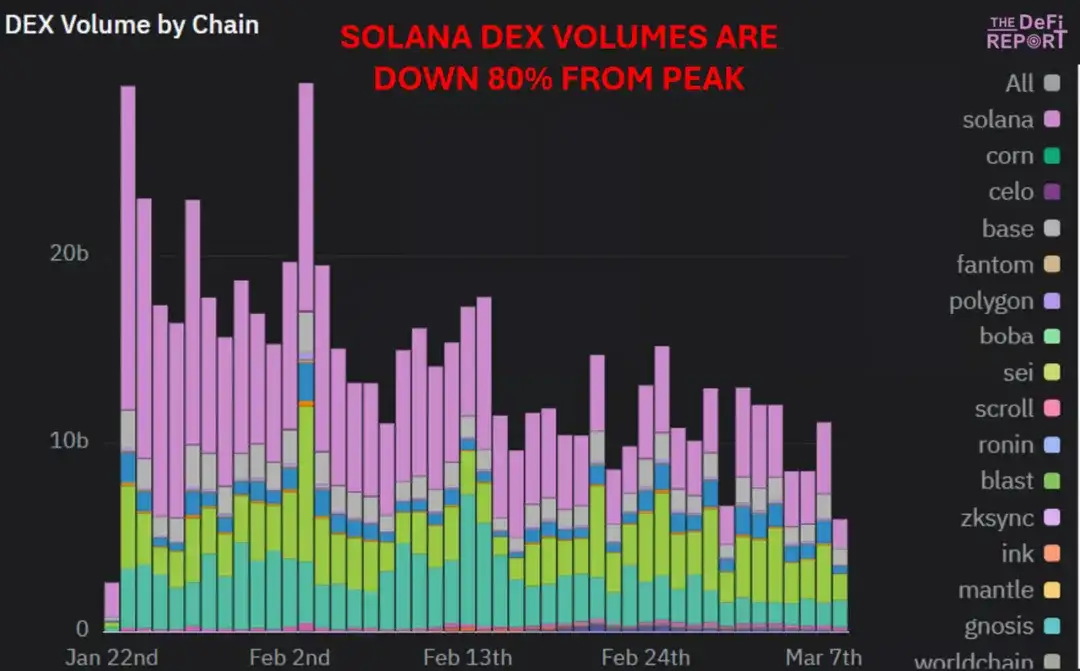

DEX Trading Volume

The trading volume on decentralized exchanges (DEX) on Solana has dropped 80% since Trump launched the meme coin. Meanwhile, the number of unique traders has decreased by over 50%. This indicates to us that animal spirits are waning.

Data Source: The DeFi Report, Dune

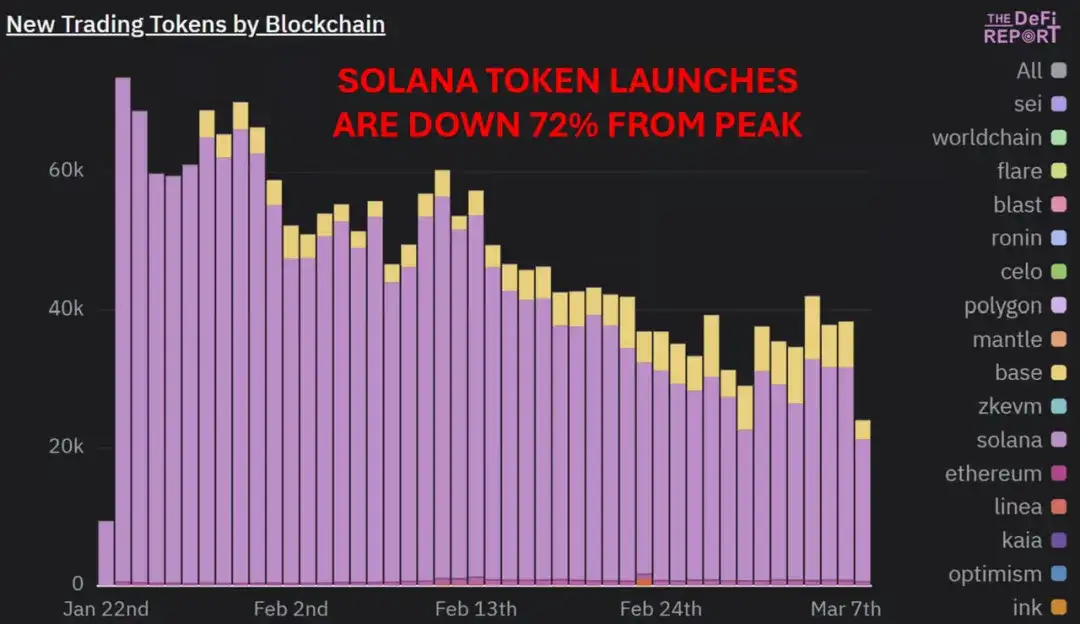

Token Issuance

The token issuance on Solana has decreased by 72% from its peak. Nevertheless, the chain still sees over 20,000 tokens created daily.

Data Source: The DeFi Report, Dune

Bitcoin Long-Term Holder MVRV Ratio

Data Source: Glassnode

The MVRV (Market Value to Realized Value) of long-term holders (the "smart money" of Bitcoin) peaked at 4.4 in December. This is 35% of the peak of 12.5 in the 2021 cycle, which was also 35% of the peak of the 2017 cycle.

Bitcoin rose about 80 times from the bottom to the peak in the 2017 cycle. It rose about 20 times in the 2021 cycle. It has risen about 6.6 times in the current cycle.

The realized price of Bitcoin (the average cost basis of all circulating Bitcoin) peaked at $5,403 in the 2017 cycle, which was 15.1 times higher than the peak of the 2013 cycle. It reached $24,530 in the 2021 cycle, which was 4.5 times higher than the peak of the 2017 cycle. Today, the realized price is $43,240, which is 1.7 times higher than the peak of the 2021 cycle.

Key Points:

Through each of the data points above, we can observe a symmetry in the reduction of peaks from one cycle to the next. We believe this data clearly tells us that the law of diminishing returns is very real.

Bitcoin is currently a $1.7 trillion asset. No matter how bullish the headlines are, investors should not expect to see the same sustainable parabolic trends as in the past. It now takes too much capital to drive this asset. When Bitcoin loses momentum, the rest of the market suffers greatly.

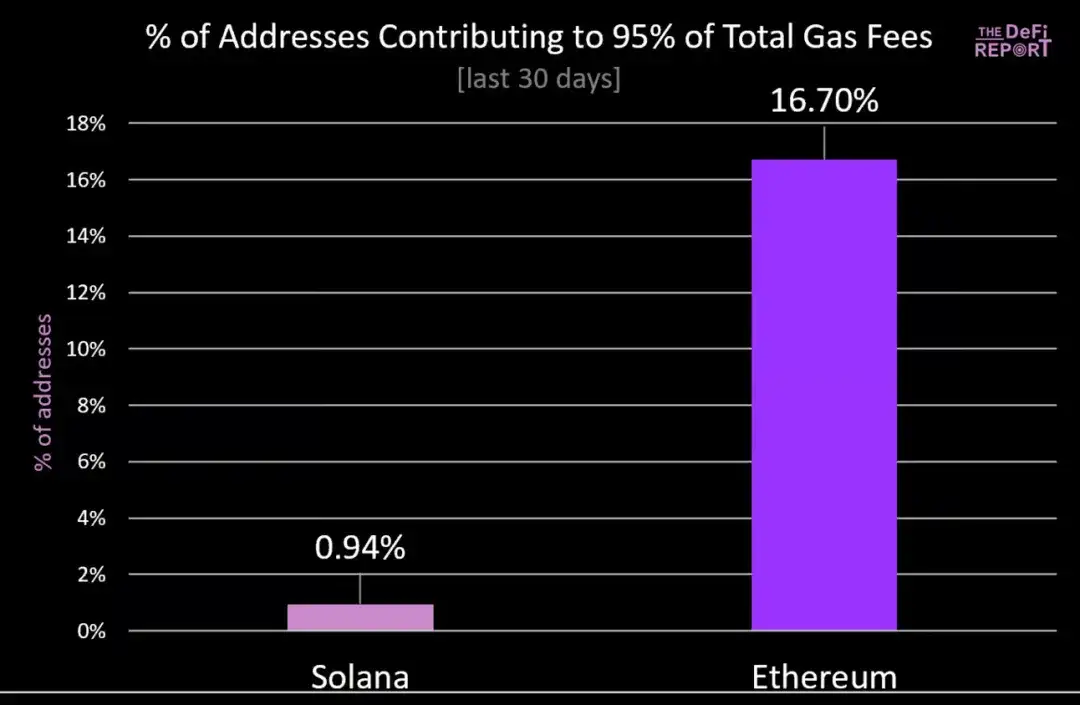

Animal spirits on Solana are waning. We are keeping an eye on this because we are concerned that Solana's "recovery story" seems to be built on a "house of cards"—considering that 61% of DEX trading volume this year has involved meme coins. Additionally, in the past 30 days, less than 1% of Solana users contributed over 95% of the GAS fees. This is concerning as it highlights that a small portion of Solana users ("big fish") are preying on everyone else (trading meme coins as "small fish"). Therefore, if the "small fish" get tired of losing money and take a break (we believe they are doing so), we may see Solana's fundamentals decline rapidly.

Data Source: The DeFi Report, Dune (Base fees + priority fees + Jito tips on Solana)

Long-term Bitcoin holders have taken profits twice in the past year. Their realized price (cost basis proxy) is currently around $25,000. Meanwhile, short-term holders who bought at the top are currently at a loss (average cost basis of $92,000). We believe this group may continue to sell at lower highs as they realize the reality that Bitcoin peaked at $109,000.

Data Source: Glassnode

Data Source: Glassnode

When you lay all this out, it is undeniable that the "typical" cycle has ended. To deny this is to deny reality.

Of course, there are no "laws" at play here.

In our view, the best way to handle this information is to accept reality + set a probability for the cycle peak. We believe this probability is clearly above 50%.

Once the groundwork is laid, we will attempt to challenge our arguments and stress-test our views.

03

Bullish Reasons

I still see many people countering bearish views. Bulls are not easily laying down their arms.

This raises the question: Is the bullish view more evidence that we have entered the "wealth destruction" phase, i.e., the "denial" phase? Or are we perhaps being too bearish at a local low, and the market will rise again afterward?

In this section, we will discuss some of the main "bullish points" I see.

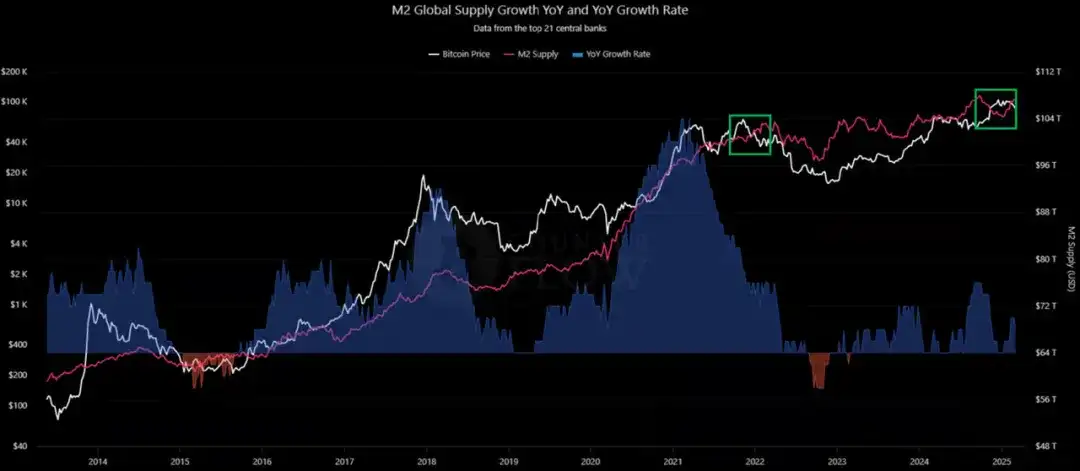

Global M2/Liquidity

Data Source: Bitcoin Counter Flow

Data Source: Bitcoin Counter Flow

The green box on the right shows that as global M2 begins to rise, Bitcoin is falling. Some point this out, mentioning the correlation between Bitcoin and M2, and that Bitcoin typically has a 2 to 3-month lag response.

However, the green box on the left shows that the same dynamic occurred at the end of the last cycle: M2 was rising while Bitcoin was falling. In fact, M2 did not peak until early April 2022—5 months after Bitcoin peaked.

Since mid-January, global M2 has risen by 1.87% as central banks have shifted from tightening to easing.

This is positive for liquidity conditions.

However, we should also raise the following questions:

What is driving the increase in M2? We believe this primarily comes from the decline of the dollar (down 4% since February 28!)—foreign currencies are increasing when measured in dollars. This is a driving factor for global M2. Additionally, the reverse repo facility has recently been exhausted + China is easing to stimulate its economy.

Will it continue? We believe the dollar will continue to decline as investors shift funds overseas, but it will not continue at the pace of the past few weeks. We believe China will continue to ease in response to the dollar's decline. However, we do not think the Federal Reserve will ease in the short term, as they have stated that reserves remain "ample." We believe they are still concerned about inflation.

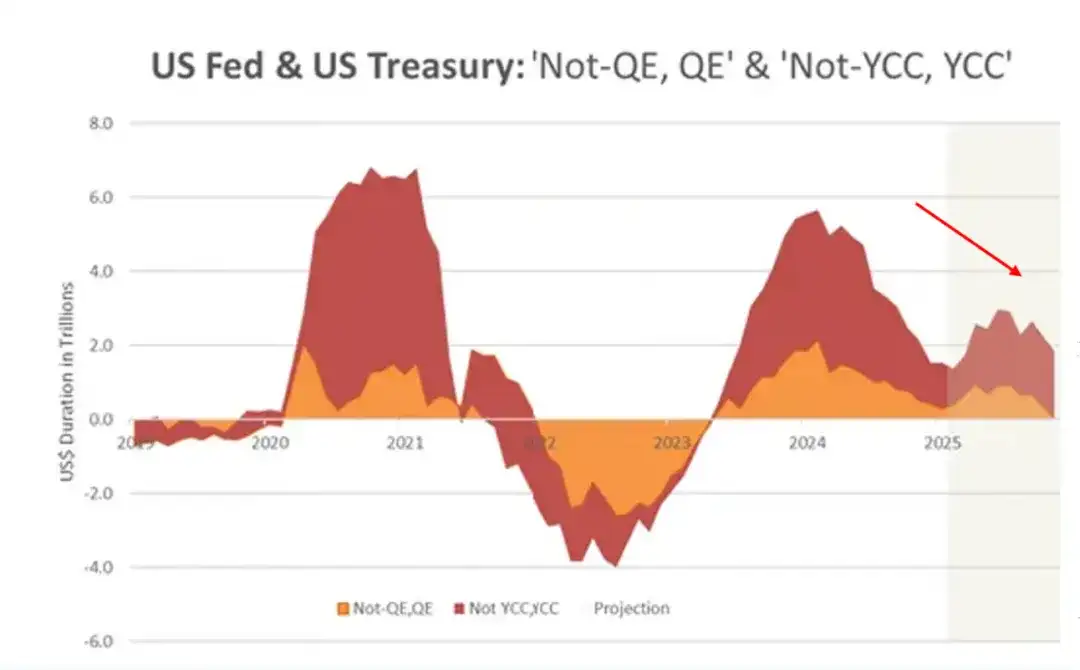

How does this compare to last year's liquidity conditions? We believe the current liquidity conditions should be viewed as a headwind compared to last year. Remember, this is more about the rate of change rather than nominal increases. We strongly believe that the Fed and Treasury injected vitality into the market last year through "shadow liquidity"—or in the words of Cross Border Capital's Michael Howell, "not QE's QE" and "not yield curve control's yield curve control." The chart below shows the rate of change impact of removing these policies under Trump's new administration.

Data Source: Cross Border Capital

Data Source: Cross Border Capital

The "secret stimulus" in the above chart is estimated to have injected $5.7 trillion into the U.S. market at the beginning of 2024. This was accomplished by exhausting reverse repos + issuing new debt notes in advance.

Finally, we believe investors should closely monitor what Treasury Secretary Yellen said last week in an interview with CNBC:

"The market and the economy have become addicted. We have become addicted to this government spending. There will be a detox period. There will be a detox period."

Business Cycle/ISM

We previously pointed out that ISM data indicates a new business cycle is beginning. We also recorded strong data on capital expenditure purchases and small business confidence. We believe this is real, but growth is clearly slowing. The data we saw last month may have been skewed due to some manufacturers "front-loading" purchases in anticipation of tariffs. We have seen softening in services and new orders data. The manufacturing PMI reading for February was 50.3, down from 50.9 in January.

Strategic Bitcoin Reserves

Until last Friday, native cryptocurrency individuals were still hopeful about discussions of strategic cryptocurrency/Bitcoin reserves—despite the market repeatedly ignoring this news over the past 6 weeks.

I think we can all agree now that this is a "buy the rumor, sell the news" event. Is "cycle thinking" flawed?

We should also acknowledge that this "cycle" is different from the past.

For example:

Bitcoin reached a historical high for the first time before the halving.

This cycle is much shorter, with only two years of a bull market.

The "altcoin season" has behaved quite differently, as Bitcoin's dominance has been gradually rising since early 2023.

Bitcoin is now fully integrated into the financial system and supported by the U.S. government.

If "cycle thinking" is flawed, is it possible that we have not yet reached the peak? Instead, we may be experiencing a pause/correction/consolidation phase, followed by the next round of increases, rather than a year-long bear market with prices dropping 75-80% as in the past?

Our view is that the cycle is indeed evolving. Nevertheless, we still expect a bear market that could last 9-12 months.

04

Summary

To summarize our views:

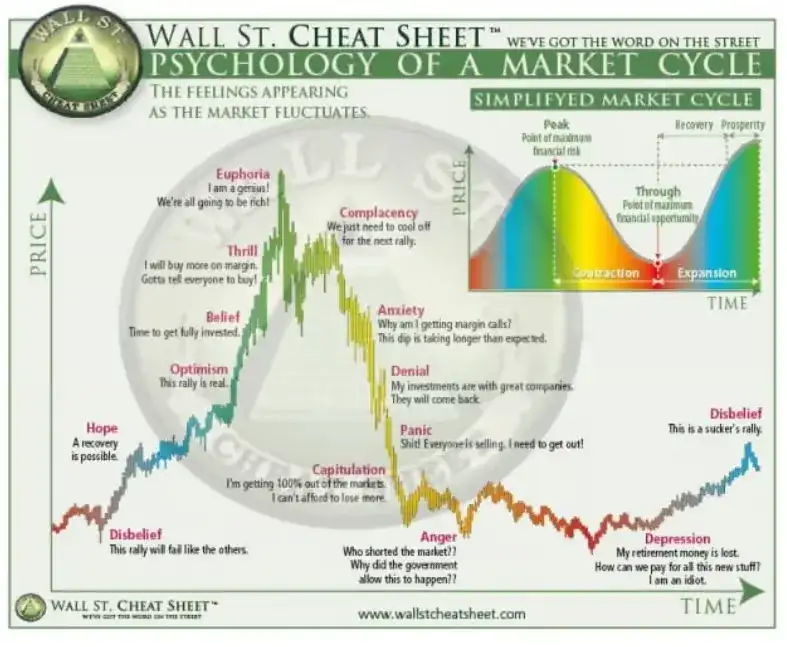

We believe we are currently in the "Complacency" stage shown in the above chart.

All the bullish catalysts that could be identified a few years ago have already played out.

The economy may be heading toward recession. We believe the messages from the Trump administration have been very clear. They are essentially telling us that the economy needs detoxification. We should take them at their word. This is very similar to when Powell came out in early 2022 and said, "Pain is coming." We currently believe that cryptocurrencies are the canary in the coal mine. Traditional financial markets will follow with slow bleeding/volatility.

Given the extreme bearish sentiment, we may see a short-term market rebound to the low of $90,000 for Bitcoin. However, we believe this will be met with aggressive selling—which could stifle any hope of restoring the bull market structure.

As always, we remain open to being wrong. Our analysis is based on the information available today. As new information comes in, we will update our views.

What do we need to see to become bullish again?

We will look for the following:

Fiscal constraints/reversal of DOGE efforts.

Significant rate cuts/QE from the Fed.

Major inflows of global liquidity driven by the Fed (not just China).

Significant corrections/surrender in the S&P 500/Nasdaq.

One concern we have is that bearish scenarios are starting to become consensus. This makes us a bit hesitant. But we still need to stick to all other factors—because the probabilities indicate that the cycle peak has been reached and a bear market is imminent.

Of course, there are many bullish things to look forward to in the long run.

Cryptocurrencies have truly entered their "turning point" period. It is finally time to rebuild the financial system on public blockchains.

Not to mention, we love bear markets. As the tide goes out, it becomes easier to separate the noise from the signals of past cycles—which will prepare us for the next bull market.

Original Title: Still bullish?

Original Link: https://thedefireport.io/research/bulls-valid-case#the-bear-case

Original Author: Michael Nadeau

Translation: Baihua Blockchain

Article Link: https://www.hellobtc.com/kp/du/03/5709.html

Source: https://mp.weixin.qq.com/s/1LKGB9fL72UEJV5JDohAqA

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。