Author: Alice

The global financial system is undergoing a profound wave of transformation. Traditional payment networks are facing comprehensive challenges from emerging alternatives—stablecoins—due to outdated infrastructure, lengthy settlement cycles, and high costs. These digital assets are rapidly innovating the patterns of cross-border value flow, the paradigms of corporate transactions, and the ways individuals access financial services.

In recent years, stablecoins have continued to develop and have become an important underlying infrastructure for global payments. Large fintech companies, payment processors, and sovereign entities are gradually integrating stablecoins into consumer-facing applications and corporate cash flows. Meanwhile, a range of emerging financial tools, from payment gateways to deposit and withdrawal channels, to programmable yield products, has greatly enhanced the convenience of using stablecoins.

This report deeply analyzes the stablecoin ecosystem from both technical and business perspectives. It studies the key participants shaping this field, the core infrastructure supporting stablecoin transactions, and the dynamic demand driving their applications. Additionally, it explores how stablecoins are giving rise to new financial application scenarios and the challenges they face in being widely integrated into the global economic process.

I. Why Choose Stablecoin Payments?

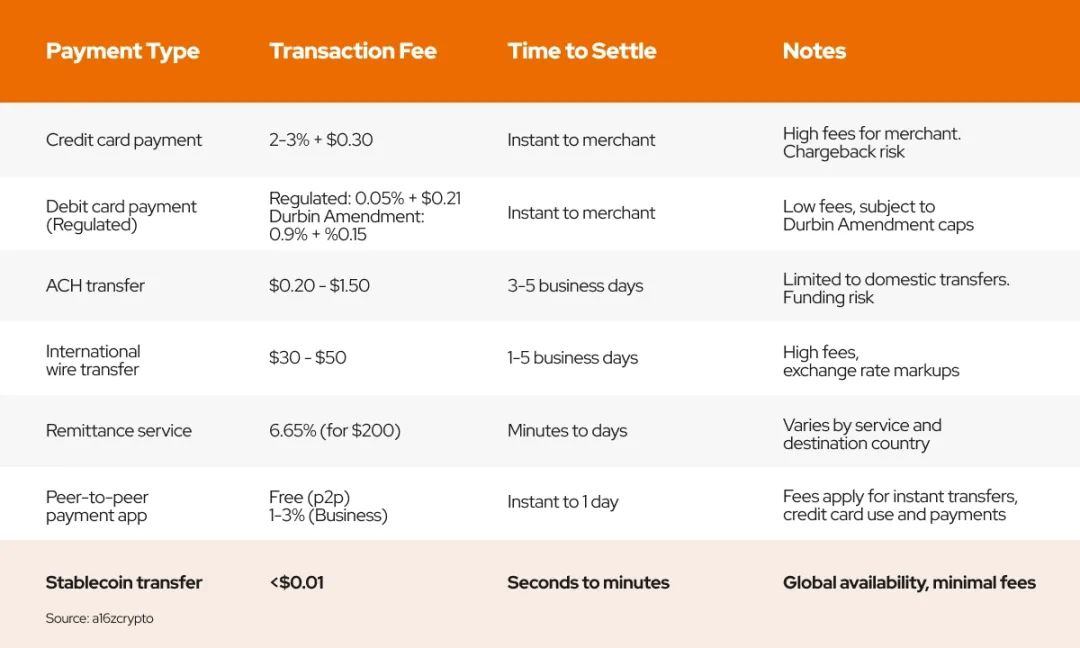

To explore the impact of stablecoins, it is essential to examine traditional payment solutions. These traditional systems include cash, checks, debit cards, credit cards, international wire transfers (SWIFT), automated clearing houses (ACH), and peer-to-peer payments. Although they have become part of daily life, many payment channels, such as ACH and SWIFT, have existed since the 1970s. While groundbreaking at the time, most of these global payment infrastructures are now outdated and highly fragmented. Overall, these payment methods are plagued by high fees, high friction, long processing times, inability to achieve round-the-clock settlement, and complex backend processes. Additionally, they often bundle unnecessary extra services such as identity verification, lending, compliance, fraud protection, and bank integration, which come at a cost.

Stablecoin payments effectively address these pain points. Compared to traditional payment methods, using blockchain for payment settlement greatly simplifies the payment process, reduces intermediaries, and achieves real-time visibility of fund flows, not only shortening settlement times but also lowering costs.

The main advantages of stablecoin payments can be summarized as follows:

- Real-time settlement: Transactions are completed almost instantaneously, eliminating delays in traditional banking systems.

- Security and reliability: The immutable ledger of blockchain ensures the security and transparency of transactions, providing protection for users.

- Cost reduction: The removal of intermediaries significantly lowers transaction fees, saving costs for users.

- Global coverage: Decentralized platforms can reach markets underserved by traditional financial services (including unbanked populations), achieving financial inclusion.

II. The Landscape of the Stablecoin Payment Industry

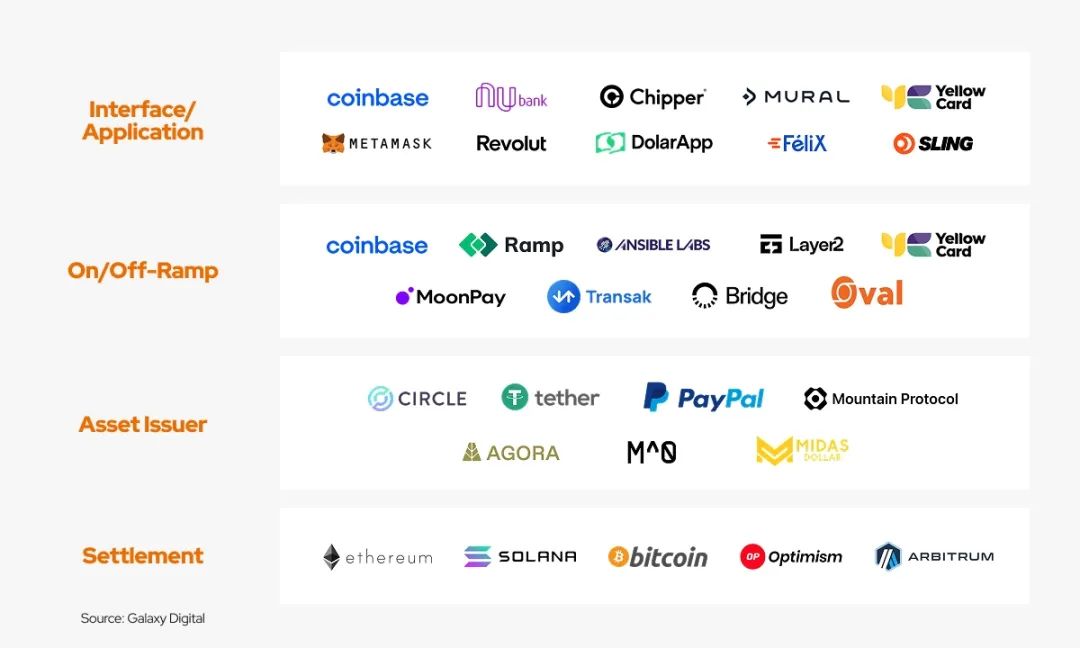

The stablecoin payment industry can be segmented into four layers of technology stack:

1. First Layer: Application Layer

The application layer is primarily composed of various payment service providers (PSPs) that integrate multiple independent deposit and withdrawal payment institutions into a unified aggregation platform. These platforms provide users with convenient access to stablecoins, offer tools for developers building on the application layer, and provide credit card services for Web3 users.

a. Payment Gateways

Payment gateways are services that facilitate transactions between buyers and sellers by securely processing payments.

Notable companies innovating in this field include:

- Stripe: A traditional payment provider that integrates stablecoins like USDC for global payments.

- MetaMask: Does not provide direct fiat currency exchange functionality, but users can perform deposit and withdrawal operations through integration with third-party services.

- Helio: With 450,000 active wallets and 6,000 merchants, millions of Shopify merchants can settle payments using cryptocurrency via the Solana Pay plugin and instantly convert USDY to other stablecoins like USDC, EURC, and PYUSD.

- Web2 payment applications like Apple Pay, PayPal, Cash App, Nubank, and Revolut also allow users to make payments using stablecoins, further broadening the application scenarios for stablecoins.

The field of payment gateway providers can be clearly divided into two categories (with some overlap):

1) Developer-focused payment gateways; 2) Consumer-focused payment gateways. Most payment gateway providers tend to focus more on one category, thereby shaping their core products, user experience, and target market.

Developer-focused payment gateways aim to serve businesses, fintech companies, and enterprises that need to embed stablecoin infrastructure into their workflows. They typically provide application programming interfaces (APIs), software development kits (SDKs), and developer tools for integration into existing payment systems, enabling features like automated payments, stablecoin wallets, virtual accounts, and real-time settlement. Some emerging projects focused on providing such developer tools include:

- BVNK: Provides enterprise-level payment infrastructure for easy integration of stablecoins. BVNK offers API solutions for seamless processes, a payment platform for cross-border commercial payments, and enterprise accounts that allow businesses to hold and trade various stablecoins and fiat currencies, along with merchant services that provide tools for businesses to accept customer stablecoin payments. It processes over $10 billion in annualized transaction volume, with a growth rate of 200%, and is valued at $750 million, serving clients in emerging regions like Africa, Latin America, and Southeast Asia.

- Iron (in beta): Provides APIs to seamlessly integrate stablecoin transactions into existing businesses. It offers businesses global deposit and withdrawal channels, stablecoin payment infrastructure, wallets, and virtual accounts, supporting customized payment workflows (including recurring payments, invoicing, or on-demand payments).

- Juicyway: Offers a range of APIs for enterprise payments, payroll, and bulk payments, supporting currencies including Nigerian Naira (NGN), Canadian Dollar (CAD), US Dollar (USD), Tether (USDT), and USD Coin (USDC). It primarily targets the African market and currently has no operational data.

Consumer-focused payment gateways prioritize users, providing easy-to-use interfaces for stablecoin payments, remittances, and financial services. They typically include mobile wallets, multi-currency support, fiat deposit and withdrawal channels, and seamless cross-border transactions. Some well-known projects focused on providing this simple payment experience for users include:

- Decaf: An on-chain banking platform that enables personal consumption, remittances, and stablecoin transactions in over 184 countries; Decaf collaborates with local channels, including MoneyGram, in Latin America to achieve nearly zero withdrawal fees, with over 10,000 South American users and high ratings among Solana developers.

- Meso: A deposit and withdrawal solution that integrates directly with merchants, allowing users and businesses to easily convert between fiat currencies and stablecoins with minimal friction. Meso also supports Apple Pay for purchasing USDC, simplifying the process for consumers to obtain stablecoins.

- Venmo: Venmo's stablecoin wallet feature utilizes stablecoin technology, but its functionality is integrated into its existing consumer payment application, allowing users to easily send, receive, and use digital dollars without directly interacting with blockchain infrastructure.

b. U Cards

Cryptocurrency cards are payment cards that allow users to spend cryptocurrencies or stablecoins at traditional merchants. These cards are typically integrated with traditional credit card networks (such as Visa or Mastercard) and enable seamless transactions by automatically converting cryptocurrency assets to fiat currency at the point of sale.

Projects include:

- Reap: An Asian card issuer with clients including Infini, Kast, Genosis Pay, Redotpay, Ether.fi, and over 40 other companies, selling white-label solutions and primarily relying on transaction volume for revenue (e.g., Kast 85%-Reap 15%). It collaborates with banks in Hong Kong and can cover most regions outside the U.S., supporting multi-chain deposits; projected transaction volume will reach $30M by July 2024.

- Raincards: A card issuer in the Americas that supports companies like Avalanche, Offramp, and takenos, with a key feature of serving U.S. and Latin American users. It has issued a USDC corporate card for expenses like travel, office supplies, and other daily business costs using on-chain assets (e.g., USDC).

- Fiat24: A European card issuer and web3 bank, with a business model similar to the above two, supporting companies like ethsign and safepal for card issuance; it has a Swiss license and primarily serves users in Europe and Asia, but does not yet support full-chain transactions, only allowing deposits on Arbitrum. It has slow growth with a total user base of 20,000 and monthly revenue of $100K-150K.

- Kast: A rapidly growing U card on Solana, having issued over 10,000 cards, with 5-6K monthly active users, and projected transaction volume of $7M and revenue of $200K by December 2024.

- 1Money: A stablecoin ecosystem that recently launched a credit card supporting stablecoins and provides a software development kit for L1 and L2 integration, currently in beta with no data available.

There are many cryptocurrency card providers, which mainly differ in the regions they serve and the currencies they support, and they typically offer low-fee services to end users to encourage the use of cryptocurrency cards.

2. Second Layer: Payment Processors

As a key layer in the stablecoin technology stack, payment processors are the backbone of payment channels, primarily covering two categories: 1. Deposit and withdrawal service providers 2. Stablecoin issuance service providers. They act as a critical intermediary in the payment lifecycle, connecting Web3 payments with traditional financial systems.

a. Deposit and Withdrawal Processors

- Moonpay: Supports over 80 cryptocurrencies, providing various deposit and withdrawal methods and token swap services to meet users' diverse cryptocurrency trading needs.

- Ramp Network: Covers over 150 countries, providing deposit and withdrawal services for over 90 cryptocurrencies. The network handles all KYC (Know Your Customer), AML (Anti-Money Laundering), and compliance requirements, ensuring the compliance and security of deposit and withdrawal services.

- Alchemy Pay: A hybrid payment gateway solution that supports bidirectional exchange and payment between fiat currencies and crypto assets, achieving the integration of traditional fiat currency and crypto asset payments.

b. Stablecoin Issuance & Coordination Processors

- Bridge: The core products of Bridge include coordination APIs and issuance APIs. The former helps businesses integrate multiple stablecoin payments and exchanges, while the latter supports rapid stablecoin issuance for enterprises. The platform is currently licensed in the U.S. and Europe and has established significant partnerships with the U.S. State Department and Treasury, boasting strong compliance operational capabilities and resource advantages.

- Brale (in beta): Similar to Bridge, Brale is a regulated stablecoin issuance platform that provides stablecoin coordination and reserve management APIs. It has compliance licenses in all U.S. states, and partner companies must undergo KYB (Know Your Business) verification, while users need to set up accounts for KYC (Know Your Customer) at Brale. Brale's clients are primarily on-chain OGs (such as Etherfuse, Penera, etc.), and compared to Bridge, its investment backing and business development are slightly weaker.

- Perena (in beta): Perena's Numeraire platform lowers the issuance threshold for niche stablecoins by encouraging users to provide concentrated liquidity in a single pool. Numeraire employs a "central hub-radiating" model, where USD* serves as the central reserve asset, acting as a "hub" for stablecoin issuance and exchange. This mechanism allows for the efficient minting, redemption, and trading of various stablecoins pegged to different assets or jurisdictions, with each stablecoin connected to USD* as similar "spokes." Through this system structure, Numeraire ensures deep liquidity and enhances capital efficiency, as small stablecoins can interoperate through USD* without needing to provide separate liquidity pools for each trading pair. The ultimate design goal of this system is not only to enhance price stability and reduce slippage but also to achieve seamless conversion between stablecoins.

3. Third Layer: Asset Issuers

Asset issuers are responsible for creating, maintaining, and redeeming stablecoins. Their business models typically center around balance sheets, similar to bank operations—accepting customer deposits and investing funds in high-yield assets like U.S. Treasury bonds to earn interest spreads. At the asset issuer level, stablecoin innovation can be divided into three tiers: static reserve-backed stablecoins, yield-bearing stablecoins, and revenue-sharing stablecoins.

1. Static Reserve-Backed Stablecoins

The first generation of stablecoins introduced the foundational model of digital dollars: centralized issued tokens backed 1:1 by fiat reserves held by traditional financial institutions. Major participants in this category include Tether and Circle.

Tether's USDT and Circle's USDC are the most widely used stablecoins, both backed 1:1 by dollar reserves in Tether and Circle's financial accounts. These stablecoins are currently integrated with multiple platforms and serve as a base currency for a significant portion of cryptocurrency trading and settlement. Notably, the value accrual of these stablecoins belongs entirely to the asset issuers themselves. USDT and USDC primarily generate revenue for their issuing entities through interest spreads rather than sharing profits with users.

2. Yield-Bearing Stablecoins

The second evolution of stablecoins goes beyond simple fiat-backed tokens, embedding native yield generation features. Yield-bearing stablecoins provide on-chain returns to holders, typically sourced from short-term Treasury yields, decentralized finance (DeFi) lending strategies, or staking rewards. Unlike traditional static stablecoins that passively hold reserves, these assets actively generate yield while maintaining price stability.

Notable protocols providing on-chain yields for stablecoin holders include:

- Ethena ($6B): A stablecoin protocol issuing USDe—an on-chain synthetic dollar backed by hedged Ethereum (ETH), Bitcoin (BTC), and Solana (SOL). Ethena's unique design allows USDe holders to earn organic yields derived from perpetual futures market funding rates (currently an annualized yield of 6.00%), attracting users through its unique collateral and yield mechanisms.

- Mountain ($152M): A yield-bearing stablecoin with a current annualized yield of 4.70%. Mountain allows users to earn interest daily simply by depositing USDM into their wallets, appealing to users seeking passive income without additional staking or complex DeFi participation, providing a simple and convenient way to earn.

- Level ($25M): A stablecoin composed of liquid re-staked dollars. Level explores a new method of yield generation for stablecoins; it uses lvlUSD to provide security for multiple decentralized networks and collects additional yields from these networks, which are then passed on to lvlUSD holders, innovating the yield model for stablecoins.

- CAP Labs (Beta): Built on the highly anticipated megaETH blockchain, CAP is developing the next generation of stablecoin engines aimed at providing new sources of yield for stablecoin holders. CAP stablecoins leverage external income sources (such as arbitrage, maximum extractable value (MEV), and real-world assets (RWA)) to generate scalable and adaptive yields—these income streams have traditionally been reserved for complex institutional participants, opening new directions for stablecoin yields.

3. Revenue-Sharing Stablecoins

Revenue-sharing stablecoins integrate built-in monetization mechanisms that directly distribute a portion of transaction fees, interest income, or other revenue streams to users, issuers, end apps, and ecosystem participants. This model aligns incentives among stablecoin issuers, distributors, and end users, further transforming stablecoins from passive payment tools into active financial assets.

- Paxos ($72M): As an evolving stablecoin issuer, Paxos announced the launch of USDG in November 2024, which will be regulated under the upcoming stablecoin framework by the Monetary Authority of Singapore. Paxos shares stablecoin yields and interest income generated from reserve assets with partners that help expand network utility, including Robinhood, Anchorage Digital, and Galaxy, thereby expanding the revenue-sharing model through collaboration.

- M^0 ($106M): The M^0 team consists of veterans from MakerDAO and Circle, with a vision to serve as a simple, trusted, neutral settlement layer that enables any financial institution to mint and redeem M^0's revenue-sharing stablecoin "M." The M^0 protocol shares most interest income with approved distributors known as "beneficiaries." However, one distinction of "M" from other revenue-sharing stablecoins is that "M" can also serve as a "raw material" for other stablecoins (such as Noble's USDN).

- Agora ($76M): Similar to USDG and "M," Agora's AUSD also shares revenue with applications and market makers that integrate AUSD. Agora has received strategic support from several market makers and applications, including Wintermute, Galaxy, Consensys, and Kraken Ventures. Agora's revenue-sharing ratio is not fixed, but most will be returned to partners.

4. Fourth Layer: Settlement Layer

The settlement layer of the stablecoin technology stack is the foundation of the stablecoin ecosystem, ensuring the finality and security of transactions. It consists of payment channels (blockchain networks) that process and verify stablecoin transactions in real-time. Today, many well-known L1 and L2 networks serve as key settlement layers for stablecoin transactions:

- Solana: Known for its excellent throughput, fast finality, and low fees, this high-performance blockchain has become a key settlement layer for stablecoin transactions, especially in consumer payments and remittances. The Solana Foundation actively encourages developers to build on Solana Pay and hosts PayFi conferences/hackathons to strongly support off-chain PayFi innovations, promoting the application of stablecoins in real payment scenarios.

- Tron: A first-layer blockchain that occupies a significant market share in stablecoin payments; USDT on Tron is widely used for cross-border payments and peer-to-peer (P2P) transactions due to its efficiency and deep liquidity. Tron places a strong emphasis on B2C transactions, but currently lacks support for B2B scenarios.

- Codex (beta): An OP L2 for cross-border B2B payments, Codex aggregates deposit and withdrawal service providers, market makers, exchanges, and stablecoin issuers to provide enterprises with one-stop stablecoin financial services. Codex has strong distribution channels and shares 50% of its sorter fees with Circle to acquire traffic for its deposit and withdrawal services.

- Noble: A USDC native asset issuance chain designed for the Cosmos and IBC ecosystems. Cosmos is the fourth-largest USDC issuance chain and has integrated with Coinbase. Projects integrating Noble can deposit USDC into over 90 IBC modular chains (dYdX, Osmosis, Celestia, SEI, Injective) for native minting and circulation of USDC in a multi-chain ecosystem.

- 1Money (beta): An L1 built specifically for stablecoin payments. Transactions are processed in parallel with equal priority and fixed fees, meaning there is no transaction reordering, and users cannot "jump the queue" by paying higher fees. The network also offers gas-free transactions through ecosystem partners to enhance user experience, providing a fair and efficient network environment for stablecoin payments.

III. Expanding Stablecoin Applications: Serving Non-Crypto Native Users

1. Current Bottlenecks

- Regulatory Uncertainty: Banks, enterprises, and fintech companies urgently need clearer policy guidance from regulators before fully adopting stablecoins to effectively manage risks.

- User Side: The lack of use cases for stablecoins limits their adoption among ordinary consumers. The payment scenarios that consumers use daily are relatively fixed, and stablecoins have yet to deeply integrate into them, leaving many consumers without actual demand or motivation to hold stablecoins.

- Enterprise Side: The level of acceptance of stablecoin payments by enterprises greatly affects the promotion process of stablecoins. Currently, enterprises face dual challenges of willingness and capability when accepting stablecoin payments. On one hand, some enterprises have limited understanding of this emerging payment method and harbor doubts about its security and stability, leading to low acceptance willingness. On the other hand, even if enterprises are inclined to accept stablecoin payments, they may encounter various challenges in practical operations, such as technical integration, financial accounting, and compliance regulation, limiting their acceptance capabilities.

Despite these bottlenecks, we believe that U.S. regulation is gradually becoming clearer, which will encourage more traditional users and enterprises to adopt compliant stablecoins. Although both parties may face potential friction such as KYC (Know Your Customer) and KYB (Know Your Business), the long-term market potential is enormous.

If we segment the market into 1. Crypto-native users and 2. Non-crypto-native users, most of the interviewed projects target on-chain markets, serving crypto-native users, while the non-crypto-native market remains largely undeveloped. This market gap presents significant opportunities for innovative companies to establish a first-mover advantage in guiding new users into the crypto space.

In the on-chain aspect, the stablecoin market competition has become intense. Many participants are dedicated to increasing use cases, locking total value locked (TVL) through higher yields, and incentivizing users to hold stablecoins. As the ecosystem develops, the future success of projects will depend on expanding real-world applications, promoting interoperability between different stablecoins, and reducing friction faced by enterprises and consumers.

2. Enterprise Side: How to Increase Stablecoin Payment Adoption?

Integrating stablecoins into mainstream payment applications: Major payment platforms like Apple Pay, PayPal, and Stripe have incorporated stablecoin transactions, significantly expanding the use cases for stablecoins and notably reducing foreign exchange costs in international payment processes, providing enterprises and users with a more economical and efficient cross-border payment experience.

Incentivizing enterprises with revenue-sharing stablecoins: Revenue-sharing stablecoins prioritize distribution channels, building strong network effects through cleverly coordinating the incentive mechanisms between stablecoins and applications. They do not directly target end users but instead precisely aim at distribution channels such as financial apps. Examples of "revenue-sharing" stablecoins include Paxos' USDG, M0 Foundation's M, and Agoda's AUSD.

Enterprises and organizations can more easily issue their own stablecoins: Ordinary enterprises can more easily issue and manage their own stablecoins, which has become a key trend driving enterprise adoption of stablecoins. Perena Bridge and Brale are pioneers in this field, and as the overall infrastructure continues to improve, the trend of enterprises or countries issuing proprietary stablecoins is expected to strengthen further.

B2B stablecoin liquidity and fund management solutions: Helping enterprises properly hold and manage stablecoin assets to meet working capital and yield generation needs. For example, the Mountain protocol's on-chain yield platform provides enterprises with professional fund management solutions, effectively enhancing the operational efficiency of enterprise funds.

Payment infrastructure for developers (enterprises): It is evident that some of the most successful platforms currently position themselves as crypto-native versions of traditional financial services, aiming to provide innovative financial solutions for enterprises. For instance, many enterprises currently must manually coordinate liquidity providers, exchange partners, and local payment channels, making large-scale adoption of stablecoins inefficient. BVNK addresses this issue by automating the entire payment workflow, introducing a multi-rail solution that combines local banks, crypto liquidity providers, and fiat off-chain into a single payment engine. BVNK does not require enterprises to manage multiple intermediaries but automatically routes funds through the "fastest, cheapest, and most reliable channel," optimizing each transaction in real-time. As the adoption of stablecoins by enterprises continues to accelerate, solutions like BVNK will play a key role in making stablecoin payments frictionless, scalable, and fully integrated with global commerce by addressing the inefficiencies that hinder large-scale adoption.

Settlement networks designed for cross-border payments: Proprietary L1 and L2 solutions covering scenarios such as enterprise-to-enterprise cross-border payments or enterprise-to-consumer retail transfers. They have significant advantages in ease of integration and comprehensive regulation, effectively meeting enterprises' payment needs in complex business scenarios. For example, Codex, built specifically for cross-border transactions as an L2, aggregates deposit and withdrawal service providers, market makers, exchanges, and stablecoin issuers to provide enterprises with one-stop stablecoin financial services; Solana fully supports PayFi, actively promoting products to partners and local businesses, guiding Shopify, PayPal enterprises, and offline merchants to use Solana Pay for payments (especially in regions with relatively weak banking services, such as Latin America and Southeast Asia). A major trend is that competition among L1 and L2 settlement networks will not only focus on technology but will also involve multi-faceted competition in developer ecosystems, business development merchants, and collaborations with traditional enterprises.

3. Consumer Side: How to Expand Non-Crypto Native Users?

As stablecoins become more accessible and integrated into traditional financial applications, non-crypto native users will begin to use them without awareness. Just as today's users can use digital payments without understanding the underlying banking system, stablecoins will increasingly become invisible infrastructure, providing faster, lower-cost, and more efficient transaction support across various industries.

Embedded stablecoin payments in e-commerce and remittances

Applying stablecoins to everyday transactions is a key driver of their adoption, especially in e-commerce and cross-border remittance sectors where traditional payment systems are inefficient, costly, and reliant on outdated banking networks. Embedded stablecoin payments provide the following value in these scenarios:

- Faster, lower-cost payment experience: Stablecoins significantly reduce transaction fees and settlement times for merchants and consumers by eliminating intermediaries. When integrated into mainstream e-commerce platforms, they can replace credit card networks, achieving instant finality for transactions and saving payment processing costs.

- Gig economy, cross-border freelance salary payments, and currency preservation needs in Latin America and Southeast Asia: The demand in these specific scenarios has created a need for seamless cross-border payments. Compared to traditional banks and remittance services, stablecoins enable gig workers and freelancers to receive funds almost instantly at a lower cost, making them the preferred payment solution in the global labor market.

As stablecoin payment channels become deeply embedded in mainstream platforms, their application scope will break through the crypto-native user circle. In the future, consumers will seamlessly use blockchain-driven transaction services in their daily financial activities.

On-chain yield products for non-crypto users

Earning yields through digital dollars is another core value proposition of stablecoins, a function that remains underdeveloped in traditional finance. While DeFi-native users have long been exposed to on-chain yields, emerging products are bringing these opportunities to mainstream consumers through simplified, compliant interfaces.

The key is to introduce traditional financial users to the on-chain yield space in a seamless and intuitive manner. In the past, obtaining DeFi yields required technical knowledge, self-custody capabilities, and experience with complex protocols. Today, compliant platforms abstract technical complexities, providing intuitive interfaces that allow users to earn yields by holding stablecoins without delving into crypto knowledge.

As a pioneering protocol in this field, Mountain Protocol recognizes the inclusive value of on-chain yields. Unlike traditional stablecoins that serve merely as transaction mediums, Mountain's stablecoin USDM automatically allocates yields directly to holders daily. Its current annualized yield of 4.70% comes from short-term, low-risk U.S. Treasury bonds, making it a dual alternative to traditional bank deposits and DeFi staking mechanisms. Mountain attracts non-crypto native users in the following ways:

- Frictionless passive income: Users only need to hold USDM to automatically accumulate yields without additional staking, participating in complex DeFi strategies, or actively managing.

- Compliance assurance: USDM undergoes comprehensive audits, is fully collateralized, and is designed with an isolated bankruptcy protection account structure, ensuring users receive the same level of transparency and investor protection as off-chain money market instruments.

- On-chain yield risk control: Mountain strictly limits reserve assets to U.S. Treasury bonds and simultaneously establishes USDC-denominated credit lines to minimize the risks of bank failures and stablecoin decoupling, alleviating common concerns non-crypto users have about digital assets.

Mountain brings a paradigm shift for non-crypto users: for individual users, USDM provides a low-risk digital asset yield entry point without requiring DeFi knowledge; for institutional and corporate fund management departments, USDM is a compliant, stable, and yield-generating alternative to traditional bank products. Mountain Protocol's long-term strategy includes deepening USDM's integration into DeFi and TradFi ecosystems, expanding multi-chain support, and broadening institutional collaborations (such as existing partnerships with BlackRock). These initiatives will further simplify the path to obtaining on-chain yields and promote stablecoin adoption among non-crypto users.

Optimizing KYC processes for seamless user access

For stablecoin payments to achieve large-scale consumer adoption, KYC (Know Your Customer) processes must be extremely simplified under compliance requirements. One of the key pain points hindering non-crypto users from entering the market is the cumbersome identity verification process. To address this, leading stablecoin payment service providers are embedding KYC directly into their platforms to enable smooth user access.

Modern platforms no longer require users to complete verification separately but integrate KYC into the payment process. For example:

- Ramp and MoonPay allow users to complete KYC in real-time when purchasing stablecoins with debit cards, reducing manual review delays;

- BVNK provides embedded KYC solutions for enterprises, enabling quick and secure customer authentication without interrupting the payment experience.

The fragmentation of cross-jurisdictional regulatory frameworks remains a challenge for simplifying KYC processes. Leading service providers are addressing regional compliance differences through modular KYC frameworks. For example:

- Circle's USDC platform employs a tiered verification mechanism, allowing users to complete small transactions with basic KYC and unlock higher limits through advanced verification.

In the future, automating and optimizing KYC processes to make them seamless will be key for stablecoin payment service providers to break down barriers for mainstream user entry and accelerate on-chain adoption.

IV. Stablecoin Native Economy: Will Consumers Skip Fiat Currency?

Although stablecoins have greatly accelerated global payment processes, saving significant time and cost, real-world transactions still rely on fiat currency deposit and withdrawal channels. This creates a metaphorical "stablecoin sandwich" framework, where stablecoins serve merely as bridges between fiat currencies during the transaction lifecycle. Many stablecoin payment providers focus on the interoperability of fiat currencies, essentially making stablecoins a temporary transfer layer between fiat currencies. However, a more forward-looking vision is the potential emergence of stablecoin-native payment service providers (PSPs) that enable the native operation of stablecoin payments. This means fundamentally reconstructing the payment system, assuming that transaction, settlement, and fund management functions are entirely conducted on-chain.

Companies like Iron are actively exploring innovations in this field, aiming to build a future where stablecoins are not just bridges between fiat currency systems but the foundation of the entire on-chain financial ecosystem. Unlike other payment solutions that typically replicate traditional financial tracks using stablecoins, Iron is focused on developing an on-chain-first payment and fund management stack, hoping that in the future, funds can remain entirely on-chain, achieving true interoperability in financial markets with real-time settlement on a shared public ledger.

Whether the future of funds remaining on-chain is feasible entirely depends on consumer choices: whether to convert stablecoins into fiat currency for settlement through traditional channels or to keep funds on-chain. Several key factors may drive this shift:

1. On-chain yields and capital efficiency

A compelling reason for consumers to retain funds in stablecoins is the ability to earn passive, risk-adjusted yields directly on-chain. In a stablecoin-native economy, consumers will have greater control over the use of their funds, almost instantly receiving returns superior to traditional savings accounts. However, to truly achieve this goal, users must be able to discover highly attractive yield opportunities in the future, and the protocols providing such yields must reach a level of maturity where counterparty risk is virtually nonexistent.

2. Reducing reliance on custodial intermediaries

Holding stablecoins significantly reduces the necessity of traditional banking relationships. Nowadays, users heavily rely on banks for account custody, payments, and accessing financial services. Stablecoins enable self-custody wallets and programmable finance, allowing users to hold and manage funds independently without third-party intermediaries. This holds particularly important value in regions where the banking system is unstable or access to financial services is limited. Despite the growing appeal of self-custody models, most non-crypto native users either lack understanding of them or are cautious about managing funds in this way. To further promote the development of this self-custody model, consumers may demand more regulatory protections and robust applications.

3. Regulatory Maturity and Institutional Adoption

As the regulation of stablecoins becomes increasingly clear, their acceptance will continue to rise, and consumer confidence in the long-term value retention of stablecoins will strengthen. If large enterprises, payroll institutions, and financial organizations begin to settle transactions natively with stablecoins, the demand for users to convert back to fiat currency will significantly decrease. This is akin to the gradual transition of consumers from cash to digital banking; once new infrastructure is widely adopted, the demand for traditional systems will naturally decline.

It is noteworthy that the shift towards a stablecoin-native economy may ultimately disrupt many existing payment rails. If consumers and enterprises increasingly prefer to store value in stablecoins rather than fiat currency in traditional bank accounts, this will have a significant impact on existing payment systems. Credit card networks, remittance companies, and banks primarily rely on transaction fees and foreign exchange spreads as sources of income, while stablecoins can settle instantly on blockchain networks at almost zero cost. If stablecoins can circulate freely in a country's economy like fiat currency, these traditional payment participants are likely to be excluded from the intermediary process.

Moreover, a stablecoin-native economy will challenge the fiat currency-based banking business model. In the traditional model, deposits are the foundation for loans and credit creation. If funds remain on-chain, banks may face deposit outflows, and their lending capacity and ability to earn from customer funds will decrease. This could accelerate the transformation of the financial system, prompting decentralized and on-chain financial services to gradually replace the traditional roles of banks.

Clearly, as long as incentives favor keeping funds on-chain, the theoretical stablecoin-native economy has the potential to become a reality. This transition will be gradual, as the increasing availability of on-chain yield opportunities, the ongoing presence of banking friction, and the continued maturation of stablecoin payment networks may lead consumers to increasingly choose stablecoins over fiat currency, causing certain traditional financial rails to gradually become obsolete.

V. Conclusion: How Can We Accelerate Stablecoin Adoption?

- Payment Application Layer: Fully simplify the consumer experience, building regulatory-first stablecoin solutions that offer lower prices, higher asset yields, and faster, more convenient transfer experiences than Web2 payment rails.

- Payment Processor Layer: Focus on creating enterprise-friendly, out-of-the-box infrastructure middleware. Due to their business characteristics, different regions require different licenses and compliance requirements, resulting in a relatively fragmented competitive landscape for payment processors.

- Asset Issuer Layer: Actively pass stablecoin yields to non-crypto native companies and ordinary users to incentivize users to hold stablecoins instead of fiat currency.

- Settlement Network Layer: Competition among L1 and L2 settlement networks will not only remain at the technical level but will also involve multi-faceted competition in developer ecosystems, business development merchants, and collaborations with traditional enterprises, accelerating the integration of stablecoin payments into real life.

Of course, the large-scale adoption of stablecoins relies not only on emerging startups but also on the collaborative efforts of mature financial giants. In recent months, four major financial giants have announced their entry into the stablecoin space: Robinhood and Revolut are launching stablecoins, Stripe recently acquired Bridge for faster and cheaper global payments, and Visa, despite its own interests, is also assisting banks in launching stablecoins.

Additionally, we observe that Web3 startups are leveraging these mature distribution channels to integrate crypto payment products into existing mature companies through software development kits (SDKs), providing users with diverse options for fiat and cryptocurrency payments. This strategy helps address the cold start problem by establishing trust with enterprises and users from the outset.

Stablecoins have the potential to reshape the global financial transaction landscape, but the key to large-scale adoption lies in bridging the gap between the on-chain ecosystem and the broader economy.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。