Editor’s Note: Michael Egorov, the founder of Curve Finance, launched a new project called Yield Basis in February, raising $5 million with a token valuation of $50 million. Investors from SevenX Ventures wrote about the current state of BTC yield sources and analyzed the operational process of the Yield Basis protocol and the potential opportunities in the future BTC yield layer. Below is the original content, translated by Odaily Planet Daily:

BTC APR sounds enticing, but it may be a house of cards built on layers of altcoin incentives that could collapse at any moment.

When faced with BTC APR, people usually ask several questions: Is the yield settled in BTC or altcoins? What risks are involved? What is the potential principal loss? Is this yield sustainable? Will it be diluted as TVL grows?

This article focuses on sustainable BTC settlement yields in CeFi and DeFi, divided into three parts:

Original BTC yield sources: quantitative trading, DEX LP, lending, staking, collateral, LST, and Pendle;

New venues for BTC yield: Yield Basis protocol;

Outlook: small errors can lead to catastrophic failures; the scarcity of elite quantitative teams; the fusion of TradFi, CeFi, and DeFi, and IPO opportunities.

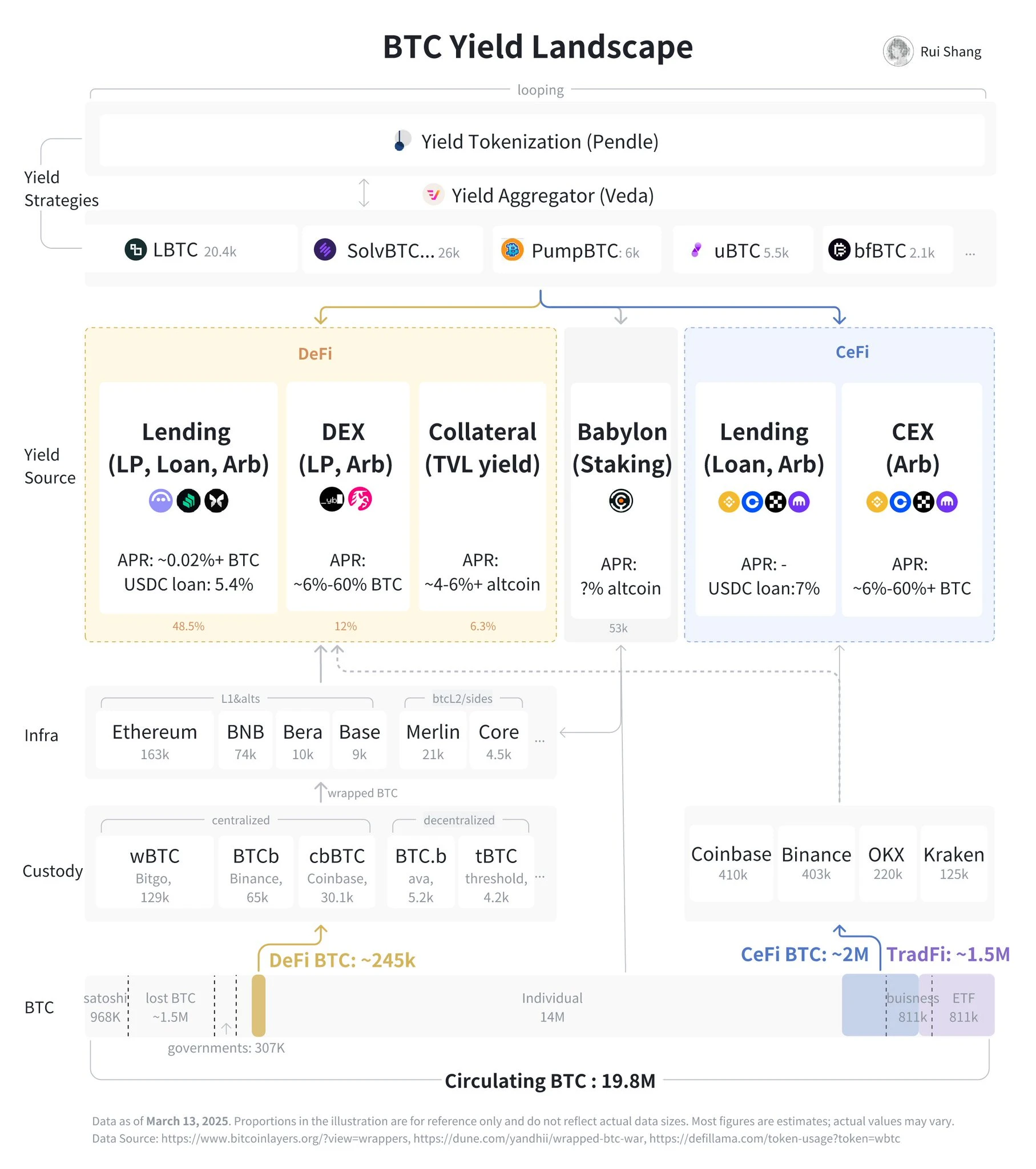

Original BTC Yield Sources

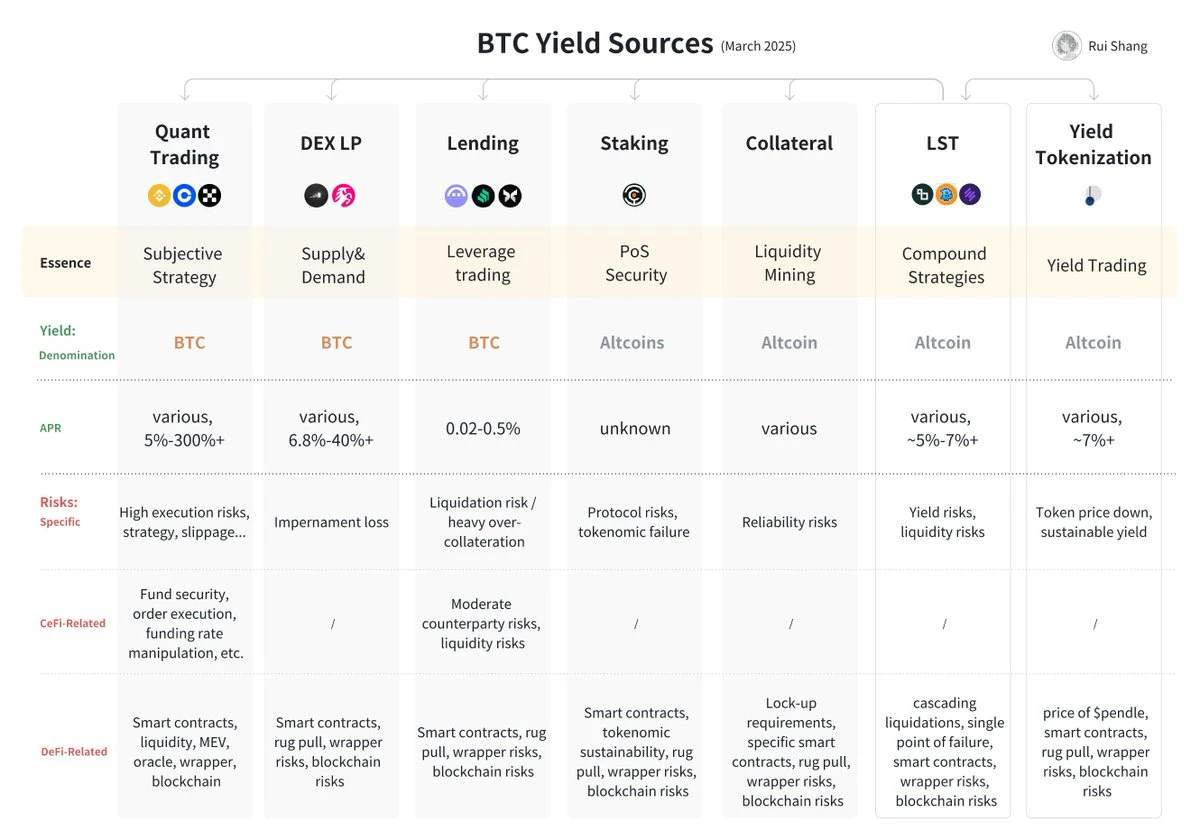

Although there are many ways to cycle and compound, we can categorize original yields into five main types: quantitative trading, DEX LP, lending, staking, and collateral. (The following image compares yield and risk.)

1. Quantitative Trading Strategies: A “Zero-Sum” Game

Ensure your alpha strategy is net profitable. Arbitrage strategies include funding rates, spot-futures basis, cross-exchange, and lending arbitrage, or involve event-driven trading. Quantitative trading requires deep liquidity—currently mainly in TradFi and CeFi. Additionally, there is a lack of cross-domain infrastructure for arbitrage between TradFi and DeFi.

BTC Yield: Varies based on asset size, risk profile, and execution. The goal of market-neutral strategies may be a 4-8% annualized rate based on Bitcoin with about a 1% stop loss. The best-performing quantitative teams even pursue annualized rates of 200-300%+, with complex risk control at around 10-30% stop loss.

Risks: Highly subjective, with model, judgment, and execution risks—market-neutral strategies can still fall into directional bets. Real-time monitoring, robust infrastructure (e.g., latency, custody, and delivery protocols), loss insurance, and venue risk control are necessary.

2. DEX LP: Limited by Supply and Demand

In addition to arbitrage, DEX also facilitates actual trading volume. Due to limited supply and demand, only about 3% of wrapped BTC is currently on DEX. In volatile LPing currency pairs (e.g., WBTC-USDC), supply is limited by impermanent loss, while demand faces wear and tear of wrapped BTC and limited utility in DeFi.

BTC Yield: Highly volatile, with Uniswap currently offering an annualized rate of 6.88%, potentially reaching double digits.

Risks: Due to impermanent loss, simply holding BTC is often better than providing liquidity. However, new LPs are often misled, reflecting a common psychological bias: fee income and APR are obvious indicators that entice LPs to maximize short-term gains while ignoring less obvious long-term capital erosion; DeFi risks apply here as well.

3. Lending: BTC Lending

BTC is primarily used as collateral for borrowing USD or stablecoins for circular or leveraged trading, rather than focusing on the APR of lending BTC—because current borrowing demand is low.

BTC Yield: CeFi and DeFi loan rates are generally low, around 0.02%-0.5% annualized. Loan-to-value (LTV) ratios vary: TradFi has LTVs of 60-75%, with current promotional rates of 2-3%; CeFi has LTVs of 33-50%, with current USDC rates at 7%; DeFi has LTVs of 33-67%, with current USDC rates at 5.2%.

Risks: Liquidation risk, although low LTV ratios help improve capital efficiency, hedging strategies can provide additional protection, but there are still CeFi and DeFi risks.

4. Staking: Earning Altcoin Rewards

Babylon is in a unique position where staking helps secure related PoS chains.

Altcoin Yield: Valued in altcoins, APR unknown.

Risks: The Babylon protocol should undergo multiple security audits and disclose expected staking yields after the system goes live. If the Babylon token issuance fails, the sustainability of the ecosystem will be at risk.

5. Collateral: Liquidity Mining

When you provide BTC to DeFi, BTC L2, and other protocols as TVL to earn altcoins.

Altcoin Yield: Varies, generally around 5-7%, but whales always get better rates.

Risks: The reliability of protocols and verifiable records varies, with different lock-up periods and capital requirements for each protocol.

6. Liquid Staking Tokens: Compound Yield

BTC “LST” is similar to LST protocols like Lombard, PumpBTC, Solv Protocol, and BitFi, which originate from the Babylon ecosystem, now featuring complex yield strategies for cross-chain BTC. Veda acts like an aggregator.

Yield is primarily presented in altcoins: combining Babylon staking rewards, points from different chains, Pendle, and some introducing quantitative strategies through third parties. Additionally, it offers its own tokens as incentives.

Risks: LST liquidity is low, with chain liquidation risks. There are single points of failure in the minting, redemption, staking, and bridging processes. It heavily relies on both self-generated and external altcoin yields, indicating significant yield volatility.

7. Yield Tokenization: Yield Trading

Pendle is the main platform for LSTs to earn more yield, currently managing $444.17 million in BTC TVL, allowing traders to obtain fixed income from principal (like spot substitutes), hedge against interest rate fluctuations, and gain yield liquidity, long/short yield positions.

Altcoin Yield: Yield may be unstable. YT holders can earn the underlying yield of LST, exchange fees, fixed yield rates, and PENDLE tokens.

Risks: A decline in PENDLE token prices can significantly affect participation. Pendle relies on sustainable yield volatility—when most of its assets depend on multi-layer competitive coin incentives (including Pendle itself), it becomes tricky.

New Venues for BTC Yield: Yield Basis

As mentioned above, while altcoin-denominated yields are unsustainable, true BTC-based yields are scarce and highly risky. Quantitative teams need sufficient liquidity, but DEXs are lacking.

What is Yield Basis: YB is an automated market maker (AMM) designed to minimize impermanent loss and facilitate BTC LP, cross-venue arbitrage, and real trading.

BTC Yield Base Layer: Based on simulations of the past six years, YB can provide an average APR of 20% (net profit), even higher in bull markets. Additionally, it can be combined with any LST wanting exposure to actual BTC-based yields, and Pendle can collaborate with the yields generated by YB.

Venue for complex trading strategies: Gradually building a venue with sufficient liquidity for meaningful quantitative trading. It also offers a profitable compounding opportunity to enhance BTC lending rates in lending protocols; currently, there is $3.286 billion in WBTC on Aave, with lending rates around 0.02%.

Retail BTC Trading Venue: YB's long-term goal is to create the deepest on-chain liquidity for wrapped BTC and compete with CeFi trading.

Mechanism: Addressing Impermanent Loss

Mechanism: One AMM embedded within another AMM

When BTC LP deposits into YB, it creates LP by borrowing half the value of the LP and continuously re-leveraging. This will create a stablecoin to BTC pool with a rebalancing model, where borrowing rates and 50% of the pool production fees will be used to subsidize the pool's rebalancing.

APR is double the pool yield (borrowing rate + re-leveraging loss), with fixed costs related to borrowing interest for crvUSD, which is controllable as the system uses it to generate more yield. Higher volatility increases re-leveraging losses but also increases pool income, so this strategy remains effective unless volatility exceeds the selected maximum liquidity concentration. Parameter selection is crucial: more aggressive parameters can increase yield but carry greater risks of re-leveraging losses, and vice versa.

Ways YB Enhances APR

LPs can choose to earn pool fees or stake to earn YB tokens. When YB tokens are attractive, more LPs choose to exit the pool, leading to higher APR.

Future Outlook

BTC yield generation will become increasingly complex, focusing on risk management, BTC-denominated products, and institutionalization. The winners will be those who can provide deep liquidity and fair yields without excessive risk exposure and innovate within regulatory frameworks.

Small Errors Can Lead to Catastrophic Losses

“Nothing is unbreakable—it's just that it hasn't been attacked yet.” BTC faces increasingly complex attacks from multiple risk layers: CEX trust delegation, self-custody phishing, smart contract vulnerabilities (permissions, logic, algorithms), and mechanism risks (liquidation, principal loss). Social engineering poses a serious threat by exploiting relationships and interfaces, with major BTC LPs even requiring chain pauses and bridging blocks. Although it sounds counterintuitive, public chains and highly liquid, permissionless protocols are not ideal for their security. Aquarius proposes a security framework that enables comprehensive testing, monitoring, and risk tracking.

Scarcity of Elite Quantitative Teams

Clearly, true yields denominated in BTC are more attractive. While DEX LPs are still in their infancy, quantitative trading remains dominant. Some teams package their strategies into yield-generating BTC products and raise funds from external LPs. However, the ability for high-frequency arbitrage may be limited, and top teams often keep these strategies internal, reducing external capital—creating a form of “adverse selection.” That said, market-neutral and other low-risk strategies as productized BTC yield products make sense.

Fusion of TradFi, CeFi, and DeFi, with IPO Opportunities

As BTC liquidity deepens, we witness the fusion of TradFi conservatism, CeFi accessibility, and DeFi innovation. In January 2025, Coinbase launched BTC-backed loans through Morpho Labs. This is a signal: CeFi is implementing DeFi mechanisms for a broader audience. In this process, institutional-grade asset management firms will have opportunities to emerge and potentially go public. Companies combining security-first infrastructure, transparent risk disclosures, and trustworthy governance will build strong brands, providing recurring revenue needed by TradFi asset managers and serving all sectors from high-net-worth clients to pension and endowment funds.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。