In this war without gunpowder, whoever can expand their channels wider will become the true king.

Written by: Deep Tide TechFlow

Recent events in the crypto market have once again put stablecoins in the spotlight.

On the evening of April 2, a revelation by Sun Yuchen regarding the Hong Kong trust company First Digital Labs caused the stablecoin FDUSD issued by the company to lose its peg, with the price dropping to as low as $0.87, sparking heated discussions in the community.

As the main trading platform for FDUSD, Binance quickly responded that the stablecoin could be redeemed 1:1, which gradually helped the price of FDUSD regain its peg.

Almost on the same day, the giant behind the stablecoin USDC, issuer Circle, submitted an IPO application to the U.S. SEC, attempting to capture the global market through listing and compliance.

These two events may seem unrelated, but they point to a core issue:

The success of stablecoins today relies not on technology, but on channels.

FDUSD faced the risk of being abandoned by channels at a critical moment—without Binance's strong endorsement, FDUSD might have long been ignored, becoming a "valuable but illiquid" token.

Behind Circle's IPO, you may not know that the S-1 document submitted for the listing shows that exchanges can earn substantial interest income from holding USDC, meaning Circle is paying for channels, encouraging major exchanges to hold USDC.

This is the power of channels: they not only determine the visibility and liquidity of stablecoins but also directly affect user trust and adoption.

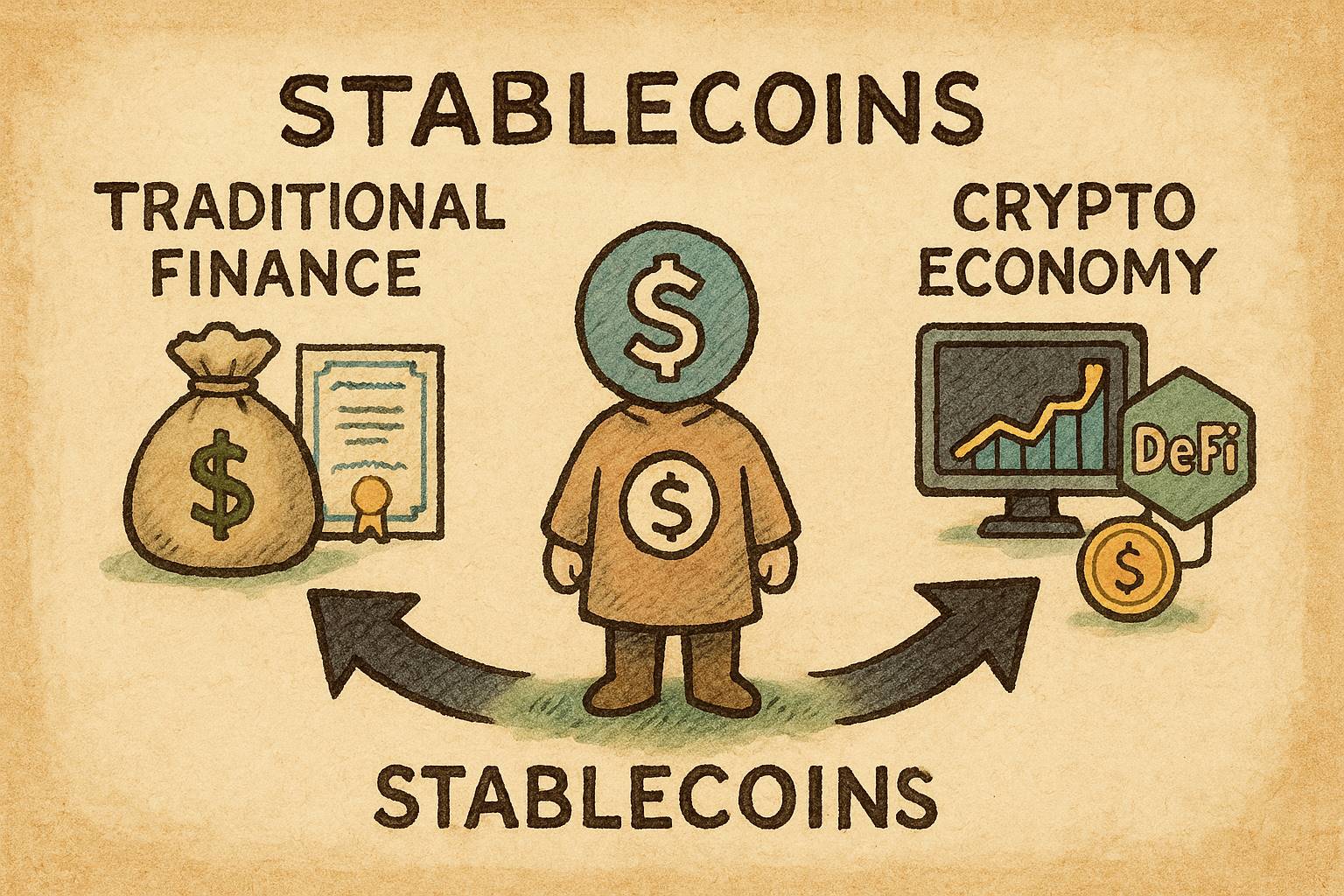

The Two Ends of Stablecoins: Asset Reserves and Channel Expansion

In a world where stablecoins, traditional finance, and the crypto economy are gradually merging, the survival logic of a stablecoin can be broken down into "two ends":

One end is sufficient asset reserves, addressing the trust issue of "you can use it with confidence." For example, both USDC and USDT are backed by short-term U.S. Treasury bonds or dollars, and the large reserves make you believe you are not using a worthless token;

The other end is channel expansion, addressing the usage issue of "you have a place to use it." In the crypto world, channels mean the endorsement of exchanges, integration with DeFi protocols, and coverage of payment scenarios. If a stablecoin cannot enter trading pairs on mainstream exchanges, DeFi liquidity pools, or the over-the-counter (OTC) market, it cannot form a true usage closed loop.

To draw an analogy with traditional industries, channel expansion is like brands vying for exposure and traffic. Stablecoins need to "make their presence felt" in the most active user scenarios to stand out among numerous competitors.

Previous data showed that in April 2024, the monthly trading volume of stablecoins on centralized exchanges (CEXs) reached $2.18 trillion, a significant increase from $995 billion in December 2023, demonstrating their core position in the crypto ecosystem.

Industry trend predictions suggest that if the market continues to grow, the monthly trading volume of stablecoins could reach $1.2 trillion by February 2025, with active addresses potentially increasing from 27.5 million in May 2024 to 30 million.

Additionally, data from September 2024 indicated that about 90% of stablecoin trading volume was concentrated in leading exchanges and DeFi protocols. This means that the breadth and depth of channels directly determine the adoption rate of stablecoins.

While asset reserves and channel expansion may seem equally important, in reality, channels often play a more decisive role.

The reason is simple: user trust in stablecoins comes not only from the transparency of reserves but also from their visibility and liquidity in the market.

If a stablecoin has ample reserves but lacks channel support, and users cannot conveniently use or trade it, it can only become a "visible but unusable dead coin."

After all, for each of us, Tether and Circle's reserve funds are more like distant reports; whether USDC and USDT can be purchased is something that can be seen at a glance.

Exchanges as Channels

Returning to the examples mentioned at the beginning of the article.

When Sun Yuchen revealed that FDUSD issuer First Digital Trust (FDT) could not redeem, the price of FDUSD quickly fell to $0.87.

The transparency of FDUSD's reserves is also relatively insufficient, as its custodian bank and asset composition have never been disclosed; the only support for its stability may be Binance's endorsement.

According to Coinmarketcap data, the trading platform with the highest liquidity for FDUSD remains Binance.

When Binance's official announcement stated that FDUSD could be redeemed 1:1, market confidence rebounded, and the price gradually regained its peg.

This event indirectly illustrates that when the transparency of a stablecoin's asset reserves is insufficient, the endorsement of channels can become a "lifeline" for the stablecoin. Without Binance's strong support, whether FDUSD could regain its peg amidst public opinion is still uncertain.

In simple terms, this is a stablecoin being passively saved by its channels during a FUD.

Of course, some stablecoins actively seek to please channels.

Public data shows that USDT occupies a large share of the stablecoin market, with a market share exceeding 60%, while USDC only accounts for about 25%.

Therefore, to stabilize USDC's market share, Circle, as its issuer, has extended olive branches to major exchanges in hopes that they can hold more USDC.

For example, from the recent IPO documents Circle submitted to the SEC, it can be seen that Circle paid Binance a one-time advance fee of $60.25 million and agreed to pay monthly incentive fees based on the USDC balance held by Binance.

"Binance must promote USDC on its platform and hold USDC in its financial reserves. Monthly incentive fees are only paid when Binance holds at least 1.5 billion USDC, and Binance commits to holding 3 billion USDC."

On the other hand, Circle has also offered similar terms to the U.S. crypto exchange Coinbase, which will receive 50% of the remaining income from USDC reserves.

In terms of specifics, the proportion of revenue shared from Circle's reserves is directly related to the amount of USDC held on the Coinbase platform.

If more USDC is stored on the Coinbase platform, the proportion of reserve income shared with the exchange will increase; conversely, if users hold USDC directly through Circle or other platforms, Coinbase's share of income will decrease.

So, you can understand that Circle is paying channel fees to encourage exchanges to hold and promote its USDC as much as possible.

Catching Mice Makes a Good Cat

Austrian economist Friedrich Hayek once proposed a revolutionary idea in his work "The Denationalization of Money":

"Let the market compete freely, with the survival of the fittest, ultimately selecting the best currency."

Hayek believed that currency should not be monopolized by the government but should allow multiple currencies to coexist, with the market competition filtering out the most stable and trustworthy forms of currency. The emergence of stablecoins seems to be a practical application of this theory: USDT and USDC are trying to compete to become the best "digital dollar" in users' minds.

But the reality is that the market's free choice is often profoundly influenced by channels.

The competition among stablecoins is not solely based on the transparency of asset reserves or the superiority of technology, but more on who can occupy more channel resources.

Why is USDT so popular?

Certainly, its large reserve scale is one of its seemingly good fundamentals, but more importantly, it may have already secured a unique ecological niche in certain "special channels."

Gray markets, money laundering, scams… in these under-the-table businesses, USDT has become the unspoken underground hard currency; you rarely see someone actually exchanging USDT back to dollars at a 1:1 ratio, but it seems to be widely used as the preferred medium for "special business" settlements.

In internet slang, this is finding its vertical track.

And even though USDC is not as popular, its dominant position on Binance and Coinbase is not a result of natural market selection; as mentioned in Circle's IPO documents, it is essentially bought by Circle.

Two types of stablecoins, two paths to adoption, neither statutory nor predestined, are the historical routes of the crypto industry gradually forming a climate from its marginal and wild growth.

In this gray area-filled crypto world, USDT and USDC have proven one thing in different ways: whether it is underground hard currency or bought positions, the ones that can catch mice are the good cats.

The Winning Hand of Global Expansion

Ultimately, the survival logic of stablecoins is, at its core, a game of trust and scenarios.

Channels are not only the lifeblood of survival but also the key to victory.

Just as Hayek envisioned a market of free competition, stablecoins may eventually select the "best digital dollar."

But in this war, whoever can occupy more trading pairs on exchanges, DeFi liquidity pools, and payment scenarios will win user trust and market dominance.

USDT is favored by gray channels, USDC buys its way through compliance, while other emerging stablecoin competitors struggle to survive under the endorsement of their respective DeFi protocols, exchanges, and chains—different paths, the same truth: channels are king.

In the future, as regulations tighten, DeFi rises, and central bank digital currencies (CBDCs) compete, the global expansion path of stablecoins will become even more complex.

But regardless of how the rules change, the logic of channels remains eternal.

In this war without gunpowder, whoever can expand their channels wider will become the true king.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。