Led by Michael Saylor, Strategy (formerly MicroStrategy), the U.S. company holding the most Bitcoin, is currently in distress due to the dual pressures of falling Bitcoin prices and massive debt. According to an 8-K filing submitted to the SEC on April 7, Strategy stated that if it cannot address its current financial difficulties, it may be forced to sell its Bitcoin holdings.

Strategy in Financial Distress

Strategy's current financing model for purchasing Bitcoin relies on the market's long-term bullish expectations for Bitcoin. If Bitcoin prices enter a prolonged period of stagnation or decline, the company will face dual pressures: it must pay interest on existing debt while also dealing with the risk of equity dilution from issuing new shares.

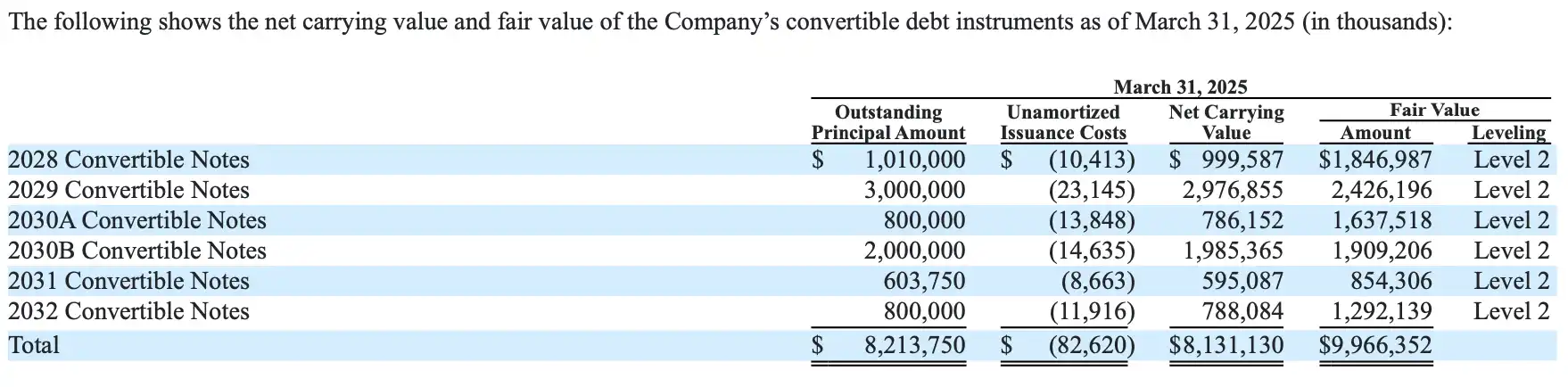

According to the 8-K filing, Strategy currently holds 528,185 Bitcoins, with a total value exceeding $40 billion and an average purchase cost of $67,458 per coin. Since transforming into a "Bitcoin company" in 2020, the company has continuously increased its holdings through financing methods, becoming a benchmark for cryptocurrency investment in the U.S. stock market. However, as Bitcoin prices have fallen from a peak of $100,000 at the end of 2024 to around $76,400, combined with a debt burden of $8.22 billion, Strategy's financial situation is facing severe challenges.

Strategy's Bitcoin strategy was once the engine behind its soaring stock price, but now it hangs over the company like the sword of Damocles. The SEC filing clearly states that Bitcoin constitutes "the vast majority" of the company's balance sheet, and its price fluctuations directly determine the company's financing ability and debt repayment prospects. If certain key factors spiral out of control, selling Bitcoin may become an unavoidable reality.

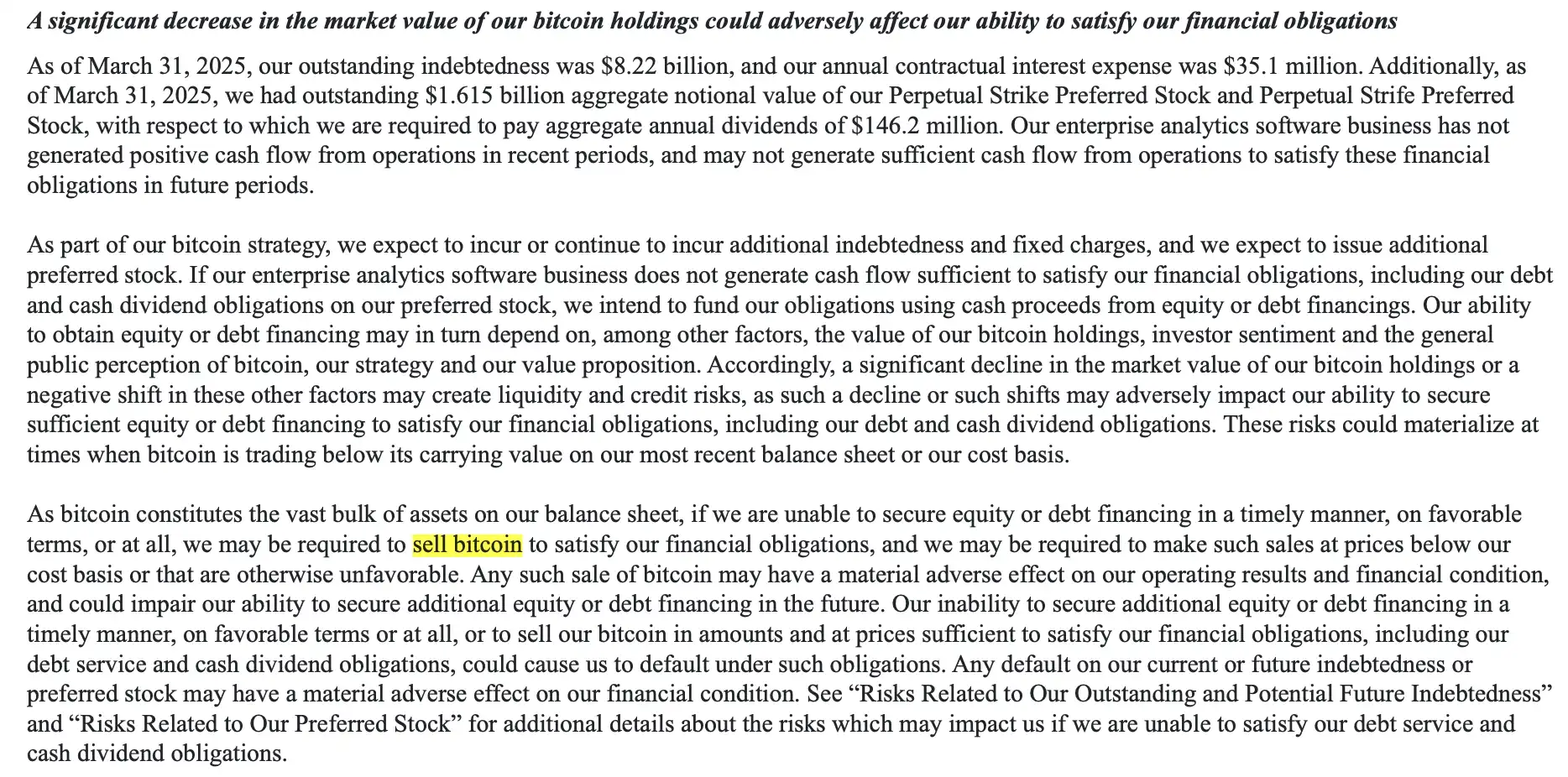

The greatest risk comes from the continued decline in Bitcoin prices. If the price falls below the cost price of $67,458, or even slides toward the recent low of $74,500, the company's asset value will significantly shrink. The filing warns that if Bitcoin drops below its book value, Strategy may struggle to raise funds through issuing stocks or bonds. Since November 2024, following Trump's election victory, the company has purchased 275,965 Bitcoins at an average price of $93,228 each, spending $25.73 billion, and is now facing an unrealized loss of $4.6 billion. Worse still, in the first quarter of 2025, the unrealized loss on Bitcoin reached as high as $5.91 billion, exacerbating the risk.

At the same time, the cash flow crisis has put the company on thin ice. Strategy's core business—data analytics software—has failed to generate positive cash flow for several consecutive quarters. However, the company still has to pay $35.1 million in debt interest and $146 million in dividends each year, totaling $181.3 million. If external financing does not keep pace, selling Bitcoin may be the only way out. The filing mentions that the $8.22 billion in debt (as of the end of March 2025) creates immense repayment pressure, and if the market environment worsens, the company may even be forced to sell at a "loss" below the cost price.

Finally, market and security factors could become unexpected triggers. If Bitcoin custodians (such as banks or third-party custodians) go bankrupt or suffer a cyberattack leading to asset loss, Strategy may be forced to sell its remaining holdings to cover the losses. The filing specifically notes that its insurance only covers a small amount of Bitcoin, highlighting the reality of this risk.

Of course, Strategy is not sitting idly by. The company plans to alleviate pressure by issuing new shares or new debt, having already spent $7.7 billion in the first quarter of 2025 to increase its Bitcoin holdings at an average price of $95,000 each. However, as April progresses and the market declines, this aggressive buying strategy has noticeably slowed. If financing channels are blocked, selling Bitcoin becomes the last lifeline.

Related: Is Strategy Restarting the "Buy, Buy, Buy" Model? A Comprehensive Analysis of the New Financing Plan

What will be the potential impact of selling pressure on the market?

Strategy's Bitcoin holdings account for about 2.5% of the total Bitcoin supply, and if it sells, the market is unlikely to remain calm. The scale of the sale will depend on the company's specific needs, with impacts cascading accordingly.

If the sale is merely to cover short-term expenses, such as paying the annual interest and dividends totaling $181.3 million, it would require selling about 2,318 Bitcoins. This is less than 0.5% of its total holding of 528,185 Bitcoins, and the market impact would be relatively limited, likely only causing minor fluctuations, and investors may not panic too much. However, if Strategy needs to repay part of its debt, such as $1 billion, the sale scale would expand to about 12,800 Bitcoins, accounting for 2.4% of its holdings. In an environment where the daily trading volume of Bitcoin is only $10-30 billion and liquidity is low, such a sale could push prices down by 5% to 10%, enough to create noticeable pressure on the market.

A more severe situation would arise if Strategy must repay the entire $8.22 billion debt at once, leading to a sale scale of about 105,000 Bitcoins, equivalent to 20% of its holdings. Such a large-scale sale would be nearly impossible to absorb in the current market and could trigger a price crash, especially considering the Bitcoin market's sensitivity to large transactions—recently dropping from $83,000 to $74,500 has proven this point.

The most extreme scenario would be the company's bankruptcy or forced liquidation, which could mean selling all 528,185 Bitcoins, valued at over $40 billion. This would be a devastating blow to the market, potentially halving the Bitcoin price or worse. However, the likelihood of such a complete sell-off is low unless the company faces a systemic crisis, such as a debt default combined with regulatory forced liquidation. In any scenario, Strategy's actions could become a significant turning point for the Bitcoin market, warranting close attention.

Another aspect of market impact is the potential for a chain reaction. If Strategy sells, other institutions or retail investors may follow suit, leading Bitcoin prices into a vicious cycle. The tariff policies implemented after Trump's election have already intensified the selling sentiment for risk assets, and Strategy's actions could become the "last straw" that breaks the market.

What is even more controversial is that this situation also involves the credibility of Michael Saylor himself. As a staunch supporter of Bitcoin, Michael Saylor has repeatedly claimed in media outlets like CNBC that he would "never sell Bitcoin," even stating that he would bequeath his Bitcoin to organizations that support the asset after his death. However, the wording in the SEC filing—"may sell Bitcoin at a loss"—seems to break that promise.

Will they really sell Bitcoin?

Strategy's Bitcoin strategy began in 2020 when Saylor positioned it as "digital gold" to combat inflation. Through issuing convertible bonds, preferred stock, and ATM increases, the company has cumulatively invested $35.6 billion in Bitcoin, with holdings once showing unrealized gains of several billion dollars. However, the recent decline in Bitcoin prices combined with debt pressure has led the company to fail to turn a profit for three consecutive quarters.

In fact, the risk of selling mentioned in this SEC filing is not the first time it has been brought up. Strategy has submitted 25 8-K filings this year, with the 8-K filings labeled "operating results and financial condition" typically submitted at the beginning of each month. The monthly "operating results and financial condition" report is standard practice. As early as the 8-K filing on January 6, the risk of "potentially selling Bitcoin" was mentioned; however, the filings in February and March did not reference this, making this the first mention of the risk in three months. Nevertheless, the straightforward wording in this 8-K filing—"may sell at an unfavorable price"—reflects the intensifying pressure to some extent, likely directly related to the recent significant drop in Bitcoin prices and the $5.91 billion unrealized loss.

Looking back at the last bear market, Strategy also faced severe tests, with negative net assets, yet it was not forced to sell Bitcoin. This was mainly due to two key factors: first, the debt maturity dates are far off (the earliest being 2028), and second, founder Michael Saylor holds 48% of the voting rights, making it difficult for liquidation proposals to pass. Therefore, even if Bitcoin falls below the cost price, the likelihood of triggering a "death spiral" of selling is relatively low. Compared to the last bear market, Strategy now has various tools to respond: issuing bonds, increasing stock issuance, or using its $40 billion Bitcoin holdings as collateral for financing.

Moreover, from a macro trend perspective, Bitcoin is gaining recognition from more sovereign funds and institutions, with a positive long-term outlook. Although short-term price fluctuations may bring financial pressure, Strategy's debt has a long maturity, and with an improving market environment, the actual risk of selling is limited.

Related: Michael J. Saylor's Strategic Bet: Premium Issuance of Bitcoin and Capital Manipulation

In the short term, the market will closely monitor its first-quarter report and subsequent financing plans. As for whether they will sell, the market will hold its breath in anticipation. The next steps for this company not only concern its own survival but may also influence the future landscape of Bitcoin.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。