Neutrl buys locked VC tokens at a discount through OTC and then hedges by shorting. Behind the idea that everything can be a stablecoin, is the risk excessive?

Written by: Alex Liu, Foresight News

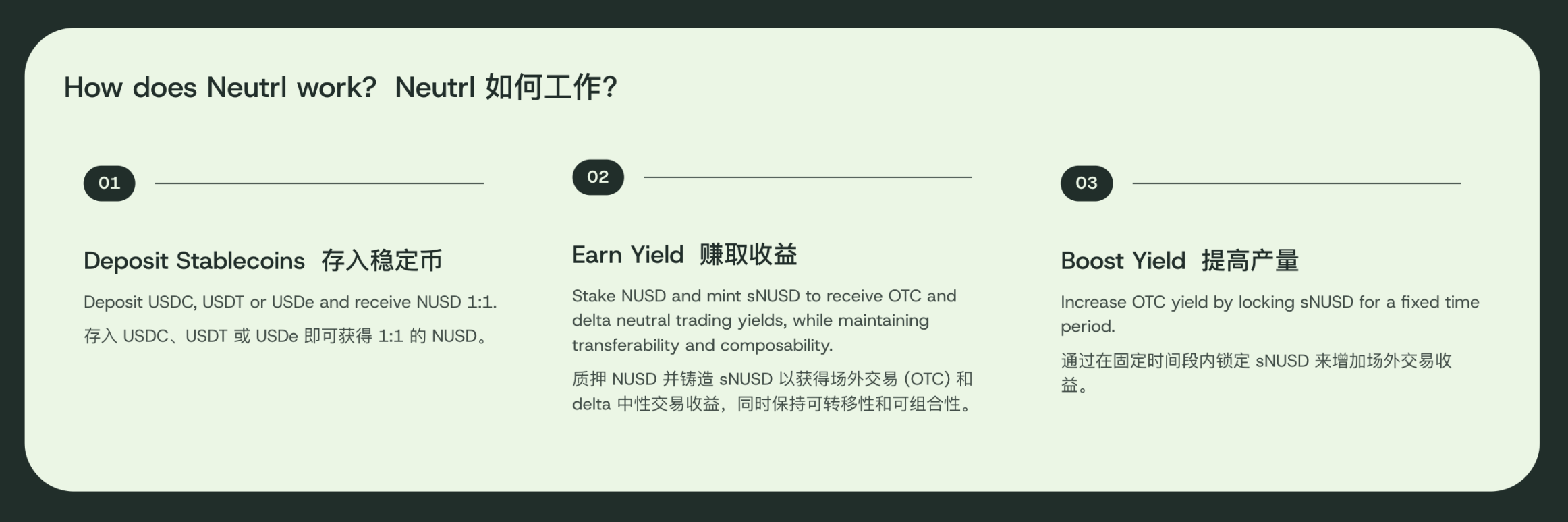

Neutrl, a Stablecoin Protocol

On April 17, the synthetic dollar stablecoin project Neutrl announced the completion of a $5 million seed round financing, led by the digital asset private placement market STIX and venture capital firm Accomplice, with participation from Amber Group, SCB Limited, Figment Capital, Nascent, and angel investors including Ethena founder Guy Young and Joshua Lim, a derivatives trader from Arbelos Markets (recently acquired by FalconX).

Neutrl's product model is similar to the leading player in the field, Ethena, featuring a synthetic stablecoin NUSD pegged 1:1 to the dollar and an interest-generating asset sNUSD, corresponding to USDe and sUSDe, respectively. The difference lies in the source of income: Ethena's income comes from arbitrage of funding rates in the crypto perpetual contract market, while Neutrl's income source is more aggressive: OTC token discount arbitrage.

Source of Income: OTC Discount Arbitrage

Institutions like VC (venture capital) can obtain project tokens at undervalued prices that retail investors cannot access, and these tokens often come with more stringent unlocking conditions. Generally, tokens have a lock-up period of six months to one year, with a linear release cycle of two to four years.

Lacking cash flow but the tokens are not yet unlocked? Afraid that the token's value will significantly decline upon unlocking? Simply want to cash out quickly to enjoy life on a yacht or in a villa? OTC (Over The Counter) provides such an option: selling the still-locked tokens in advance at a discount. The discount level is related to the project quality and unlocking conditions, but is usually quite high. For example, if a token unlocks after one year, the current OTC discount may exceed 50%.

Neutrl uses the assets deposited by users to purchase discounted locked VC tokens while simultaneously shorting an equivalent amount of tokens through contracts to achieve neutral risk (unrelated to income and token price fluctuations).

For example: buying 400,000 USD worth of tokens from the Mantra project token OM at a 60% discount before its collapse, assuming the tokens unlock in one year. At the same time, shorting 1 million USD worth of OM tokens through contracts. Ignoring contract funding rates and other complex factors, this effectively locks in a profit of 600,000 USD one year later.

Even if the OM token crashes 90% overnight, the 400,000 USD worth of OTC tokens approaches zero, but the short position profits 900,000 USD, directly closing the position shortens the profit realization cycle. If OM does not crash and rises 50% after one year, the short position incurs a loss of 500,000 USD, but the unlocked tokens are worth 1.5 million USD, thus locking in a profit of 600,000 USD.

Potential Risks: Is It a "Stablecoin"?

This strategy seems perfect, but it also has issues. Why don't VCs hedge this portion of their positions by shorting themselves, instead of choosing to sell at a discount?

First, it cannot be ruled out that some VCs are indeed operating this way. However, the reality is that VCs are usually required to disclose which projects they have invested in and the use of funds to LPs and investors. If investment institutions short their own positions, they may lose credibility. Secondly, VCs may hold more than 10% of a project's tokens, and the contract market cannot accommodate such a large short volume, leaving them with no choice but to sell at a discount.

Moreover, this strategy faces two major risks: abnormal funding rates and significant token price increases.

Regarding funding rates: if too many people are shorting, the short sellers will continuously pay funding rates to the long positions. In extreme cases of negative funding rates, the daily funding rate could reach 10% of the principal. For OTC lock-up periods that can last a year or even four years, the funding rates paid may exceed the profits brought by the OTC discount. Of course, in a bull market, positive funding rates can also bring additional profits.

If the token price rises significantly, more than double, "infinite margin" is needed to hold until the OTC tokens unlock to realize profits; otherwise, the short position may be liquidated midway, and if the token price subsequently drops again, only the actual losses from the short position remain. Not everyone can short the smooth declines of "W" and "MOVE"; if one shorts "TIA" and gets liquidated midway, it could end up being a loss.

Conclusion

Neutrl is backed by a high-risk strategy arbitrage, and they may be more professional in risk management than ordinary investors, but the potential risks cannot be ignored.

This high-risk arbitrage fund absorbs user deposits in the name of stablecoins, which seems inappropriate and requires a stronger emphasis on risk. However, Ethena is essentially also an arbitrage fund disguised as a stablecoin, without Ethena and Neutrl, retail investors would find it difficult to access the strategic profits behind them, which can be seen as an innovation and progress in the CeDeFi field, opening up more profit options for users.

Neutrl has not officially launched yet; currently, you can visit the official site to submit a Waitlist application for early access.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。