Author: Nancy, PANews

Huma is a legendary divine bird that appears in Middle Eastern and Persian mythology, symbolizing hope, divinity, and luck. According to legend, Huma never lands, and whoever is fortunate enough to be passed by its shadow will receive the mandate of a king, which is the inspiration behind the name Huma Finance.

As one of the currently popular PayFi protocols, discussions around Huma Finance's product mechanisms and development paths have been heating up recently, with both affirmations of its innovative model and questions regarding its transparency and profit mechanisms.

Recently, PANews interviewed Richard Liu, co-founder of Huma Finance, to help everyone gain a more comprehensive understanding of Huma's operational logic, current development status, and views and judgments on the future of the entire PayFi sector.

Breaking Financial Barriers with On-Chain Technology, Supported by the Solana Foundation

Richard is a multifaceted entrepreneur with experience spanning entrepreneurship, venture capital, and top tech companies, possessing a strong technical background and insights into the financial industry.

During his nearly eight years at Google, Richard led several "from 0 to 1" innovative projects, including Google Fi, which is used by many cross-border users. In 2016, he left Google to dive into the entrepreneurial wave, co-founding the smart career development platform Leap.ai and serving as CEO, using AI technology to accurately match thousands of job seekers with positions; this project was later acquired by Facebook (Meta).

Subsequently, Richard joined the fintech company EarnIn as CTO, a platform that helps users "advance their wages." This experience planted the crucial seed for his later founding of Huma Finance.

"Chinese people like to save, but many Americans live paycheck to paycheck. If a child has a birthday or an unexpected event occurs, they might not be able to come up with that money. When they can access their wages early through an app, the gratitude and happiness they feel is the motivation we experience every day," Richard recalled in the interview.

EarnIn's annual lending scale reaches as high as $10 billion, but even such a large and healthy profit-making company faces rejection from the traditional financial system when it comes to financing emerging fintech companies. "You can't get money from the bank; you can only turn to PE (private equity), but when they find out you only have one or two lending channels, they will 'squeeze your neck.' The terms are harsh, and the space is very small."

This experience made Richard aware of a serious imbalance: high-quality financial assets are often held by a few, such as PE, funds, and family offices, while ordinary users cannot participate. Meanwhile, these assets could provide more liquidity to the market and create returns for the public.

Richard began to ponder whether it was possible to use blockchain to bring these assets on-chain? On one hand, it would provide companies with broader financing channels, and on the other hand, it would allow ordinary people to access high-quality investment opportunities that were previously excluded. However, he also realized that not all assets are suitable for blockchain. "Many crypto users can accept the volatility risk of cryptocurrencies, but have zero tolerance for credit risk." Therefore, he chose to focus on the payment financing sector, which has extremely low credit risk and clear cycles.

In April 2022, Richard officially co-founded Huma Finance. The project initially entered the market as a DeFi lending protocol, attempting to bring the vast financial needs of the real world on-chain and targeting fintech companies as the main service group. Through continuous exploration, the team gradually focused on payment financing, with the core consideration being its extremely low credit risk and clear cycles.

In 2024, when the Solana Foundation listed PayFi as a strategic priority, during a meeting with the foundation's chair, Lily Liu, she clearly stated, "You understand the underlying logic of payment financing, which perfectly aligns with Solana's strategy. You should build on Solana, and we will fully support you."

"We are a multi-chain architecture platform, but currently, Solana is our main battlefield." Richard emphasized in the interview that Solana provides an ideal environment for Huma Finance's high-frequency PayFi clearing business. What truly surprised the team was the Solana Foundation's active response and substantial support during the collaboration process. For instance, when Huma Finance first integrated into the Solana ecosystem and was still unfamiliar with the technology, Solana arranged for an excellent engineering team to assist with development. Additionally, during the early on-chain financing phase, Solana introduced many early LPs (liquidity providers), and the involvement of large institutions established trust for on-chain financing. Furthermore, Huma Finance and the Solana Foundation plan to jointly organize five PayFi ecosystem conferences to promote industry progress.

"Whether it's technical issues or institutional resource connections, Solana has delivered, and many things have even exceeded our expectations," Richard admitted. Today, Huma Finance has become a flagship of PayFi within the Solana ecosystem.

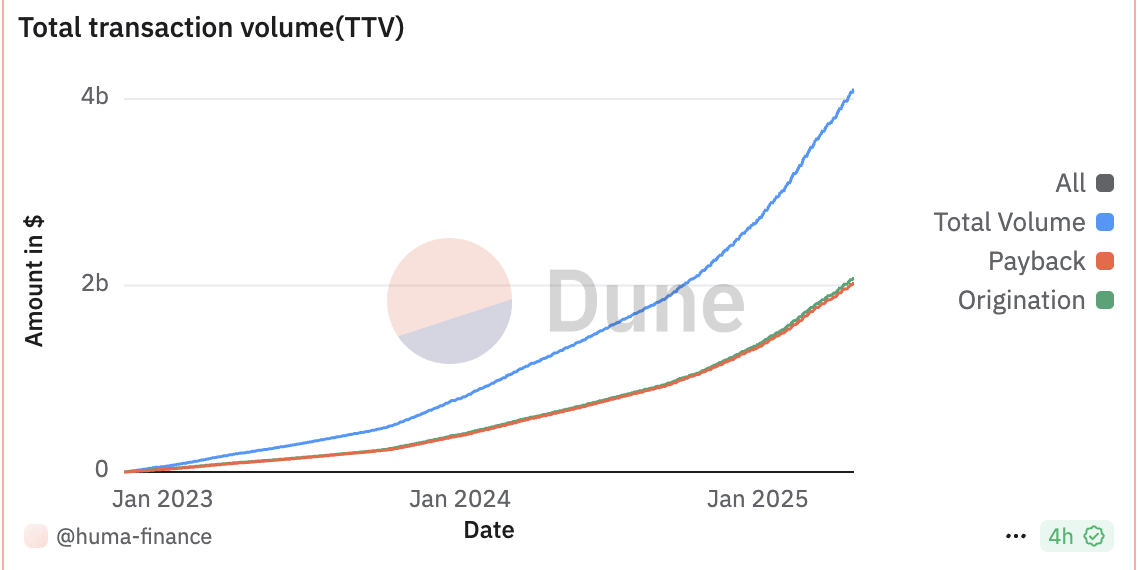

For Richard, Huma Finance is not only a continuation of the mission from the EarnIn era but also a natural extension of his years of cross-disciplinary experience in technology and finance. So far, Huma Finance has publicly secured over $46 million in financing, and its on-chain transaction volume has surpassed $4 billion.

Focusing on Cross-Border Payment Financing and Credit Card Business, Creating a Strategic Closed Loop of Platform + Application

In the interview, Richard introduced that Huma is the first PayFi network, primarily featuring a robust PayFi infrastructure, especially in the financing layer, along with a series of self-operated and third-party applications. The core application scenarios of the PayFi ecosystem can be divided into three major sectors: cross-border payment financing, credit cards, and trade financing. Currently, Huma Finance mainly focuses on cross-border payment financing and credit cards.

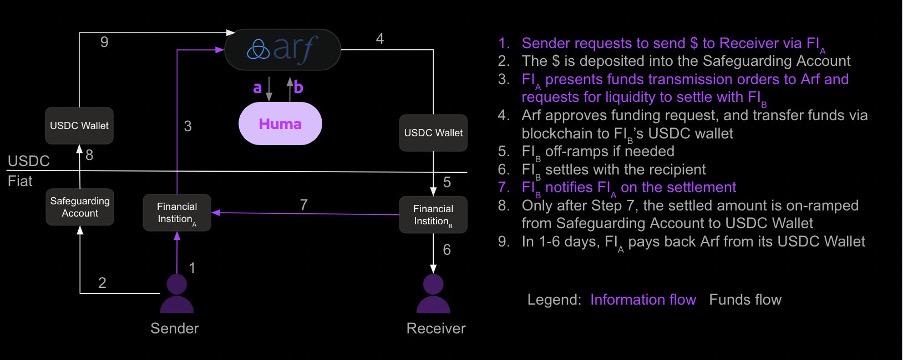

In response to external questions about Huma's profit mechanism, Richard pointed out that in the area of cross-border payment financing, Huma Finance, through its subsidiary Arf, focuses on providing short-cycle financing services to payment companies. The payment terms for this type of business are usually only a few days, offering higher capital efficiency and more controllable risk characteristics. Richard noted in the interview that this industry has already formed a stable pricing structure: through SWIFT remittances, the fee for a single transaction is usually between 20 to 60 RMB; while using payment company channels for remittances, the handling fee ranges from 2% to 5%. The daily borrowing rate between payment institutions is around 10 basis points.

"At Huma, users typically pay a funding cost of 6 to 10 basis points per day, which is a very conventional price in the current industry. In addition to reasonable price advantages, we also use stablecoins as the underlying settlement, combining the natural advantages of blockchain and stablecoins into the system to build an efficient and secure settlement system, which is also a technological innovation to the existing order," Richard stated. Cross-border payment financing is a super market with a scale of up to $40 trillion. Because the market base is extremely large, and the scale of the financing business that Huma Finance currently handles is still small, it will not significantly impact the overall price level of the industry for the time being. Only in the future, as the platform's transaction volume grows to hundreds of billions or even trillions, will it potentially drive changes in the industry's cost curve. Of course, by then, in addition to Huma Finance, other competitors will also gradually leverage more low-cost funding sources by enhancing brand trust and optimizing capital cost structures, leading to changes in the market landscape.

In addition to cross-border payment financing, Richard believes another larger opportunity exists in the credit card financing sector—a massive market worth $16 trillion. For example, in the United States, after consumers swipe their cards, the issuing bank must settle the funds to the merchant's account through the payment network within 2-3 days, while in some emerging markets like Brazil, it can take up to 30 days. During this period, before the user actually repays, the bank effectively bears the financing responsibility. Meanwhile, merchants also experience a waiting period for funds. However, many merchants are willing to pay a fee to receive funds immediately.

Richard mentioned that he and co-founder Erbil have experience in card issuance, whether through collaborations within the Google Pay system or leading card issuance at EarnIn, they have been deeply involved in the design and execution of the credit card payment chain. This means the team not only has the capability to understand the complexity of this industry but also possesses experience in refining products and models from the ground up.

Regarding trade financing, Richard pointed out in the interview that although Huma Finance's system technically has the capability to support trade financing, due to the generally longer payment terms and slower capital turnover of such businesses, it does not align with Huma Finance's current "high-frequency, short-cycle" strategy, and therefore will not directly engage in it for now.

On the funding side, before Huma 2.0, Huma Finance primarily targeted professional investors or institutions. The recent launch of Huma 2.0 opens up participation for retail investors under compliance, allowing users to choose between Classic mode or Maxi mode. Richard believes this is not only an expansion at the product level but also deeply aligns with the core concept of community ownership.

At the same time, considering that users generally do not want their funds to be forcibly locked, Huma has also made design balances: although B-end assets usually have fixed payment terms (such as three months) and cannot be exited at any time, the platform allocates about 80% of funds for payment transaction financing and configures about 20% of assets as high liquidity assets to meet users' needs for immediate redemption.

"We will not force users to lock their funds; this is a clear request they have given us. To ensure smooth redemptions, we will reserve a certain proportion of liquid assets, usually completing the redemption process within 1 to 2 days," Richard emphasized.

Additionally, regarding Huma Finance's choice to actively embrace DeFi mechanisms in the early financing stages rather than only dealing with traditional financial institutions, Richard explained that unlike the low efficiency and long response cycles of traditional financial institutions, DeFi provides a highly transparent and fast financing path. "Anyone involved in financial asset allocation understands that scaling up asset size is not easy, especially in the early stages. Traditional financial institutions have slow processes and complex connections, and the snowball effect often moves slowly. There is a lot of capital in the market willing to support high-quality assets, but under the traditional system, there is a lack of transparent and convenient participation channels. We are willing to display asset data completely transparently on-chain, thereby gaining the trust and financial support of the DeFi community, which greatly aids our development speed."

In addition to efficiency and transparency, Richard also emphasized the value of community co-construction. He stated that Huma Finance highly recognizes the power of the community, especially under the premise of compliance, empowering retail investors to participate in high-quality asset opportunities together. "What attracts me most about Web3 is that it enables true community co-construction and sharing. Such mechanisms are almost impossible to exist in the traditional financial system," Richard added.

"Google currently supports platform growth and user stickiness through its Android platform, as well as core applications like Gmail, YouTube, and Search as ecological anchors. Similarly, we hope the PayFi platform provides both underlying capabilities and scalability, along with core products that can drive real demand and capital flow." Richard also emphasized in the interview that Huma Finance aims not just to build a single product, but rather a PayFi infrastructure platform that can run various products and applications, with a value far exceeding that of any standalone application.

For this reason, Huma acquired its largest client, Arf, forming a "platform + app" closed-loop ecosystem. Richard believes that the value of the platform itself far exceeds that of any specific application, as it can connect the funding side with the asset side, supporting more scenarios for financial innovation.

It is worth mentioning that Richard also discussed Huma Finance's phased goals and implementation paths. Not long ago, Richard stated that the platform's phased goal for 2025 is to achieve a cumulative transaction volume exceeding $10 billion. He further expressed, "Currently, our main transaction growth comes from Arf's core clients. Although the platform has established strong potential client cooperation lines, the onboarding and implementation of each client require a certain period, including on-chain processes that often take several months, involving the opening of bank accounts and local regulatory approvals, with processes varying by location. Our current focus is on how to accelerate this process. The team is also exploring more efficient support systems to speed up client onboarding."

On the funding side, Huma is continuously optimizing user experience and attractiveness. "After launching the Huma 2.0 version, market feedback has been very positive," Richard stated. Under the premise of controlled deposit limits, the platform's pool was filled in a short time. The number of participating users and the participation rate in the Maxi mode exceeded expectations. Currently, the activity level on the funding side and user interest is very high. Once the limits are lifted and more large investors are introduced, there is ample room for growth. Moving forward, the team's main focus will be on accelerating the on-chain transactions of Arf clients while promoting the on-chain deployment of credit card financing scenarios.

Introducing Traditional Financial Risk Control Logic, Creating Multiple Lines of Defense for Asset Security

Huma Finance has sparked market discussions due to its PayFi model, with some investors concerned about potential default or risk of collapse.

In response to market concerns about asset security, Richard explained that Huma Finance has drawn on the classic risk control logic of traditional structured finance, introducing First-Loss Cover and a priority/subordinated structure, supplemented by multiple protection mechanisms. The goal is to create a DeFi product system with institutional-level risk control, particularly evident in its core asset Arf's cross-border payment financing business.

Specifically, regarding client selection, Huma Finance's Arf business only serves licensed financial institutions in developed countries (such as the United States, the United Kingdom, France, and Singapore), avoiding regions with complex foreign exchange controls. These institutions must meet strict compliance requirements and have low credit risk, providing a foundational risk barrier for Arf and reducing counterparty risk. At the same time, Huma Finance has established a strict internal risk control rating system for all partner institutions, classifying them based on factors such as financial status, remittance path stability, and counterparty risk (including Level 1, Level 2, and Level 3). Currently, it only serves clients rated as Level 1 and Level 2; in the operational process, the financing recipient must pre-receive the client's remittance, which will be deposited into a dedicated account that is bank-regulated and only used for that specific cross-border transaction. Huma Finance will only release funds for payment after verifying that the funds have indeed arrived and meet the preliminary risk model assessment; in terms of legal structure isolation, the assets involved with Arf are managed by an independent SPV (special purpose vehicle), completely isolating them from Huma Finance or Arf's main company assets. Even in the event of an extreme bankruptcy of Arf, user assets remain legally protected; in terms of payment response mechanisms, Huma Finance's payment terms are designed to be very short, usually completed within a few days. If any institution shows signs of delayed payment or credit changes, the system can quickly adjust its credit limit or even suspend it, ensuring that risks are identified and controlled early. Historical data shows that the bad debt rate in the financial system over the past 20 years has been only 0.25%, and Huma Finance's choice to provide short-term payment term services to developed countries means an even lower bad debt rate.

Even when facing potential large-scale redemptions or systemic risk events, Richard pointed out in the interview that Huma Finance has also designed several emergency mechanisms: for example, Arf has clearly established a 2% margin, covering several times the usual bad debt rate, which is gradually built from the platform's profit reserves and prioritized for covering potential bad debt risks; regardless of whether user funds are locked, in extreme scenarios, there will be "fair liquidation" to avoid structural unfairness caused by "first runners profiting"; if a partner institution defaults or goes bankrupt, since client funds are always in an isolated account and circulate within the regulatory system, Huma Finance has the ability to recover most or even all funds through legal means. This mechanism has not yet been triggered in practice, but from a legal structure and process perspective, it is feasible.

Additionally, regarding transparency, Richard revealed that all funds of Huma Finance are held in Fireblocks wallets, flowing through pre-defined compliance paths and requiring multi-signature approval to ensure that funds are not misappropriated. Moreover, the flow of funds can be traced in real-time through the blockchain. Currently, Huma Finance has disclosed some information on the Dune Dashboard and plans to gradually improve the dashboard to show more detailed fund dynamics. Additionally, Huma Finance publishes a monthly fund flow report, disclosing the allocation and usage of funds within the pool, and plans to write this into smart contracts in the future to further enhance transparency and auditability through a decentralized approach.

It is evident that the core logic of Huma Finance does not rely on market sentiment or Ponzi schemes to support its liquidity, but rather establishes a DeFi financial ecosystem with high resilience and accountability through multiple risk control layers, legal structures, and self-funding buffers. While extreme risks can never be completely avoided, its systemic buffering mechanisms and liquidation principles aim to build multiple lines of defense for user asset security.

Strengthening Community Building, User Education is the Current Biggest Challenge

"Disrespect for the community and users is an absolute red line for Huma Finance; sincerity is a tool that penetrates all noise." Following recent community controversies triggered by team members' communication methods, Richard promptly issued an open letter in response and further elaborated on the team's reflections on community building and future improvement directions in the interview.

On one hand, Richard candidly admitted that communication issues arose due to a mismatch between roles. "This colleague is very hardworking and creative, but I placed her in a position that was not suitable—responsible for external community communication. This is not her strength, and I should have realized it earlier." As a result, Richard has readjusted external communication responsibilities, with Richard personally overseeing communication with the Chinese-speaking community, while another co-founder, Erbil Karaman, will handle the English-speaking community.

"We believe that community communication is one of the most critical tasks for crypto companies, and co-founders must represent the company's mission and values, leading the forefront of community communication." This adjustment is also a direct response and structural repair to past issues faced by Huma Finance.

Furthermore, Richard emphasized that the team has reached a consensus internally: every piece of feedback from the community, regardless of wording, deserves to be listened to and reflected upon seriously. "Regarding community criticisms, we need to maintain a healthy mindset and try to understand their real concerns. We either clarify or admit that we indeed did not do well enough and actively improve. For example, regarding transparency, we did not prioritize it highly enough in the past. In the future, we will enhance this aspect to ensure that information disclosure is clearer and more systematic."

At the end of the interview, Richard shared his overall views on the PayFi sector, especially the core key to bridging the gap between traditional finance and DeFi, as well as the challenges and solutions faced in user education and adoption.

"The core of PayFi is to use blockchain technology to serve the real-world payment and financing needs." Richard pointed out that while many financial institutions and payment companies are very interested in this model, the actual implementation often gets stuck in the most traditional links—compliance and banking account systems.

He further noted that compliance and the paths for capital inflow and outflow are the most critical middleware in the entire ecosystem. If Hong Kong could introduce clearer relevant legislation, allowing local payment companies to legally and conveniently access on-chain services, it would not only be a breakthrough for Hong Kong but also greatly promote the development of the entire PayFi ecosystem.

In addition to connecting interfaces with traditional finance, Richard also stated, "We not only hope that users will invest money in the Huma Finance platform, but more importantly—can these PayFi assets 'go out' in the DeFi ecosystem and become core components of the entire DeFi world?"

However, there remains the most challenging barrier to cross between ideals and reality—user education. "This is actually the biggest challenge we are currently facing," Richard admitted. For DeFi users, they are accustomed to the "token issuance logic" of high APYs, and are instead unfamiliar with the yield structure of PayFi, which is based on real lending without token subsidies. "Even if I tell them that this can genuinely generate a 12.5% return, higher than many on-chain protocols, their first reaction is often: Are you running a Ponzi scheme? Is this fake?" For traditional finance practitioners, they are filled with doubts about the entire technical path of DeFi. "Many people will directly ask me why they can't complete operations using fiat accounts. Why must they use stablecoins?" Once stablecoins or on-chain settlements are involved, they hesitate due to unclear regulations.

Richard pointed out that this "cognitive dissonance" stems from the unfamiliarity of the two circles with each other's language and logic. "This also means that our team needs to speak two 'languages' well, using both DeFi's professional terminology and traditional finance language. PayFi has a long way to go; we need to generate more content with the community so that more people can better understand PayFi, jointly build this sector, and develop PayFi into the most successful application of crypto in real life as soon as possible."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。