JPMD is deployed on the Base blockchain supported by Coinbase and will be piloted for several months, with potential interest-bearing features in the future.

Written by: Weilin, PANews

On June 18, JPMorgan Chase announced the pilot launch of a deposit token called JPMD, deployed on the Base blockchain supported by Coinbase. In the coming days, JPMorgan is expected to transfer a certain amount of JPMD from its digital wallet to Coinbase, the largest cryptocurrency exchange in the U.S.

Initially, the token will be available only to JPMorgan's institutional clients, and it will gradually expand to a broader user base and more currencies after receiving regulatory approval in the U.S.

JPMD will be piloted for several months, with potential interest-bearing features in the future

The launch of JPMD is not a hasty decision. As early as 2023, JPMorgan began researching the feasibility of deposit tokens within its blockchain division, Kinexys. The day before the announcement of the JPMD pilot, it was discovered that the bank had applied for the "JPMD" trademark, which covers functions such as cryptocurrency trading, payments, and custody. At that time, there was speculation that this would signal JPMorgan's entry into the stablecoin market.

However, JPMorgan chose not to issue a stablecoin but emphasized "deposit tokens" as a more robust and regulated alternative.

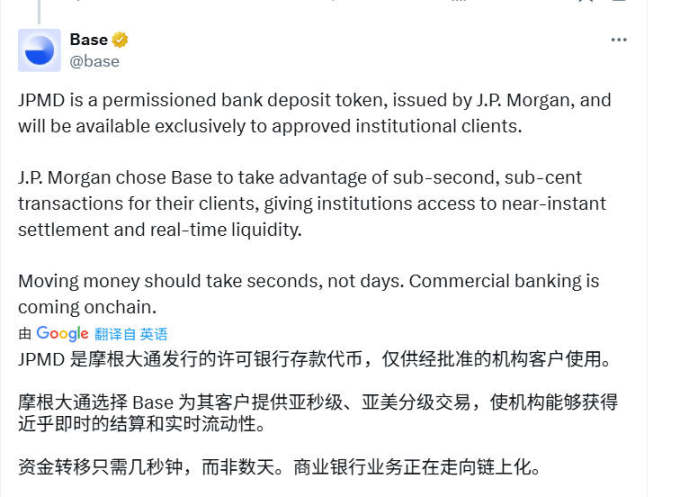

Naveen Mallela, global co-head of JPMorgan's blockchain division Kinexys, stated in an interview with Bloomberg that the issuance and transfer of the token will occur on the public blockchain Base associated with Coinbase and will be denominated in U.S. dollars. In the future, Coinbase's institutional clients will be able to use this deposit token for transactions. He added that JPMorgan plans to run the pilot for several months and gradually expand to other users and currency types after obtaining regulatory approval.

Mallela stated, "From an institutional perspective, deposit tokens are a superior alternative to stablecoins. Because they are based on a fractional reserve banking system, we believe they are more scalable." He pointed out that deposit tokens like JPMD may have interest-bearing features in the future and could be included in deposit insurance, which mainstream stablecoins typically do not have.

The JPMD pilot indicates that the bank is expanding the use of digital asset products beyond its internal systems. JPMorgan has been at the forefront of promoting blockchain technology applications on Wall Street and currently operates a network called Kinexys Digital Payments (formerly JPM Coin), allowing corporate clients to transfer U.S. dollars, euros, and British pounds from their bank accounts.

According to Bloomberg, JPMorgan stated that after the transaction volume on this network grew tenfold last year, it currently processes over $2 billion in transactions daily. However, this still only represents a small portion of the approximately $100 trillion in transactions processed daily by the bank's payments division.

Mallela indicated that JPMorgan will continue to operate and expand the Kinexys Digital Payments network, but initially, the user base for JPMD is expected to differ, with JPMD likely to be more popular among clients seeking bank-supported stablecoin alternatives.

The JPMD pilot also further supports the development of Base. "Funds transfers should be measured in seconds, not days," Base stated in an announcement on social media platform X on June 18, "Commercial banks are going on-chain."

Although JPMD is designed to operate on a public blockchain, Mallela stated that it will still be a permissioned token, available only to JPMorgan's institutional clients.

Is the stablecoin market "too crowded"? How does the JPMD deposit token differ from stablecoins?

Meanwhile, another JPMorgan executive expressed caution about the "overcrowded" stablecoin market at the DigiAssets 2025 conference held on June 17.

"I just think that as an industry, we all need to take a step back and consider whether we are ultimately going to make the market too crowded, or whether we will see more fragmentation as companies choose to use their own (stablecoins)," said Emma Lovett, executive director at JPMorgan, at the conference in London. She oversees the company's work in market distributed ledger technology and credit.

She noted that the market is currently "at the peak of stablecoin hype." However, she believes it will be "very interesting to see how the market evolves in two or three years, such as who issues their own stablecoin and who uses which."

In fact, in a white paper released a few years ago, JPMorgan introduced the concept of deposit tokens and their differences from stablecoins. The institution stated that the ongoing development of blockchain technology in commercial applications is driving the demand for blockchain-native "cash equivalents," which can serve as liquid payment means and value storage tools in a blockchain-native environment. So far, stablecoins have primarily met this demand.

At the same time, deposit tokens and central bank digital currencies (CBDCs) have become the focus of discussions about the optimal form of digital currency in the future. Deposit tokens refer to transferable tokens issued on the blockchain by licensed deposit-taking institutions, representing the holder's claim for deposits against the issuing institution. Since deposit tokens are a form of commercial bank money presented in new technology, they naturally belong to the banking system and are subject to the regulations and oversight currently applicable to commercial banks.

Deposit tokens can support various application scenarios, comparable to the functions of current commercial bank money, including domestic and international payments, trading and settlement, and the provision of cash collateral. Their token form can also enable new features, such as programmability and instant, atomic settlement, thereby speeding up transaction times and automatically executing complex payment operations.

The white paper stated that stablecoins have been an important financial innovation in recent years, driving the growth of the digital asset ecosystem. However, as on-chain trading activities continue to scale and increase in complexity, stablecoins may pose challenges to financial stability, monetary policy, and credit intermediation when used at scale.

JPMorgan believes that deposit tokens will become a widely used form of currency in the digital asset ecosystem, just as commercial bank money in the form of bank deposits currently accounts for over 90% of circulating currency. Their token form will benefit from the connection to traditional banking infrastructure and existing regulatory safeguards, which have already supported the robust operation of commercial bank deposits.

In short, deposit tokens are transferable digital currencies that represent a claim for deposits against commercial banks. Essentially, they are the digital version of customer deposits in accounts. They differ from stablecoins, which are tokens pegged to fiat currencies and are typically backed 1:1 by a basket of securities (such as government bonds or other highly liquid assets).

The GENIUS Act passes the Senate, promoting stablecoin adoption

This round of stablecoin enthusiasm is largely driven by the advancement of the U.S. GENIUS Act. This is a bipartisan-supported bill aimed at establishing a regulatory framework for stablecoins and digital assets. It is also incentivized by the listing of USDC issuer Circle.

On June 18, the U.S. Senate passed the stablecoin regulatory bill GENIUS Act with 68 votes in favor and 30 against, and the bill will be sent to the House of Representatives for consideration. The bill establishes a federal regulatory framework for stablecoins, requiring 1:1 reserves, consumer protection, and anti-money laundering mechanisms.

At the DigiAssets 2025 conference in London, an executive from asset management firm Franklin Templeton stated that the EU could become a "region that is being flown over," while the U.S. and Asia are accelerating their embrace of digital asset development.

Overall, the launch of JPMorgan's JPMD is not only an important milestone in the bank's blockchain strategy but also reflects that traditional financial institutions are accelerating their exploration of the future forms of on-chain payments.

Currently, multinational financial and technology companies, including Spain's Santander Bank, Deutsche Bank, and PayPal, are also attempting to leverage blockchain technology to achieve more efficient and cost-effective payment settlement services.

In the process of blockchain technology moving into the mainstream financial system, deposit tokens issued by commercial banks, protected by regulatory frameworks, and connected to existing account systems may become the new standard for "on-chain cash" in this new phase.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。