Written by: Bright, Foresight News

On July 5, according to Financefeeds, the Turkish Capital Markets Board (CMB) has taken legal action to block 46 cryptocurrency-related websites, including the decentralized exchange PancakeSwap. The reason given by the CMB is quite simple: these platforms provide "unauthorized cryptocurrency services" to Turkish residents.

As the fourth largest cryptocurrency market in the world, with a trading volume that once approached $200 billion, Turkey, which has legalized cryptocurrency trading, has tightened its grip on the cryptocurrency market once again.

Starting from March 2025, the CMB will begin comprehensive regulation of cryptocurrency service providers operating in Turkey and will establish a new licensing and compliance framework. Meanwhile, the anti-money laundering regulations for cryptocurrencies issued by the Turkish government in December 2024 have officially come into effect in February. When users conduct cryptocurrency transactions exceeding 15,000 Turkish Lira (approximately $425), they are required to submit complete identity information to the service provider. Additionally, wallet addresses not registered on the platform are also subject to strict regulation, making it difficult to utilize native cryptocurrency functions.

A Stone to Test the Waters Amid High Inflation

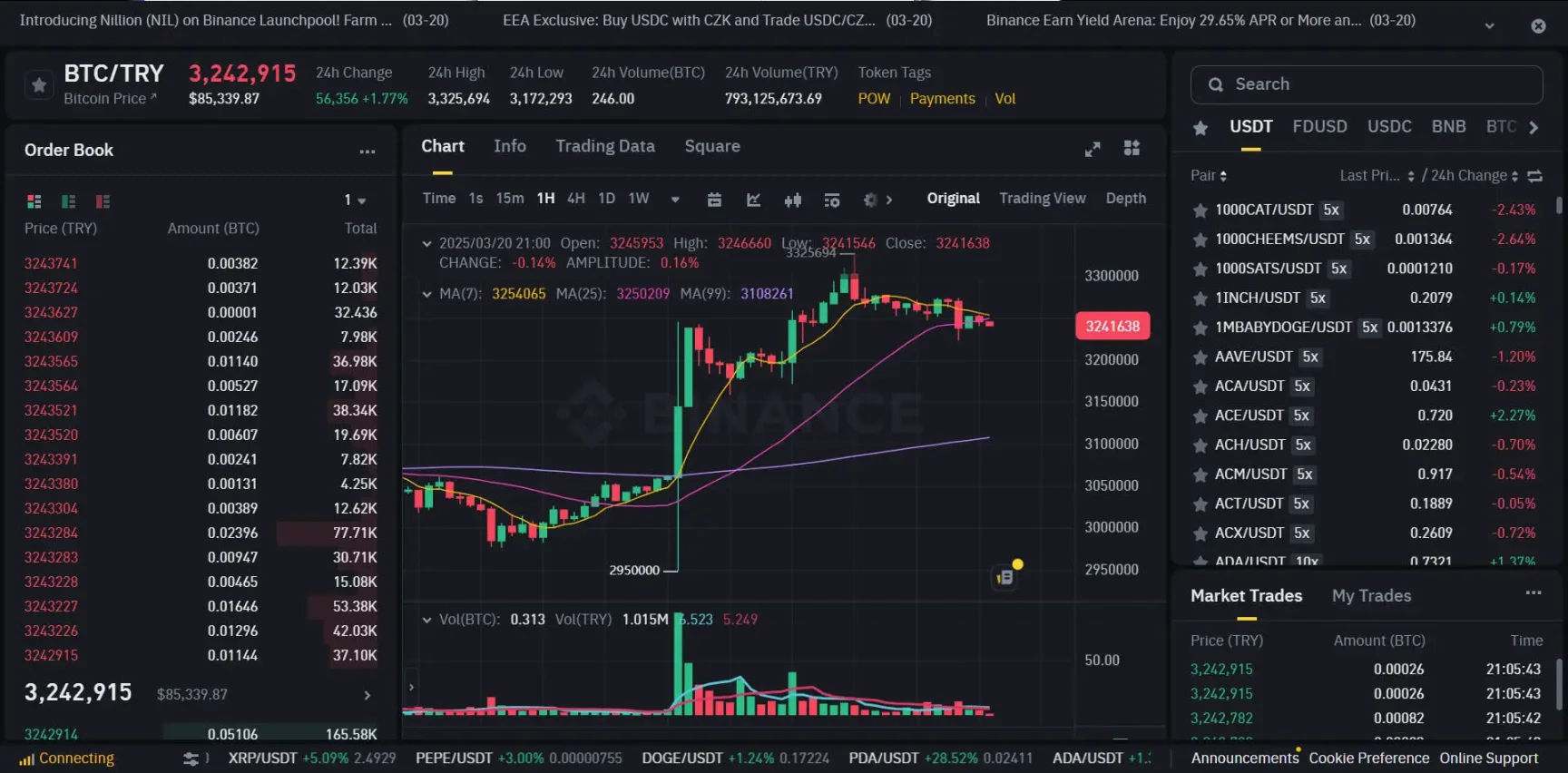

On March 19, 2025, Ekrem Imamoglu, the mayor of Istanbul and a competitor of President Erdogan, was arrested, triggering panic among local investors. The Turkish Lira (TRY) plummeted by 10% around 4 PM, reaching a new historical low of 41:1 (TRY:USD). About an hour later, a flight to safety into cryptocurrencies occurred in the market, with a significant surge in BTC/TRY trading volume on Binance.

In fact, under Turkey's "Erdoganomics"—which promotes low interest rates to stimulate investment and currency depreciation to boost exports—the Turkish Lira has depreciated by over 80% in five years; extreme inflation and the withdrawal of international capital have frequently battered the Turkish economy. In this regard, The Economist commented: "He (Erdogan) is trying to treat cancer with stimulants."

In response, the Turkish public has long had a strategy, namely "gold under the mattress." In the third quarter of 2024, the Turkish Central Bank estimated that Turkish households owned physical gold worth over $311 billion, while the Central Bank itself had only $86.5 billion in gold reserves. From January to April 2025, Turkey's current account deficit was $20.3 billion, compared to $14.5 billion a year earlier, with $6.27 billion attributable to gold trade. This gold disappears into private households once it flows into Turkey, no longer circulating.

Since 2022, apart from gold, Turkish investors have quickly turned to cryptocurrencies in search of a more stable and convenient means of value storage. Although Bitcoin fell into a bear market in 2022 due to factors such as the Federal Reserve's interest rate hikes and the collapse of FTX, dropping 64% over the year, Turkish investors, discovering a new frontier, remained very active in the cryptocurrency market. DOGE became one of the most popular trading assets in Turkey, with its trading volume even surpassing the combined total of BTC and ETH, reaching $380 million between October and November 2022. Despite early warnings from the Erdogan government for the public to stay away from cryptocurrencies, local residents have already viewed cryptocurrencies as a tool against inflation.

Subsequently, Turkish authorities also joined the wave of promoting the widespread use of cryptocurrencies to break free from dependence on external economies and SWIFT, seeking autonomy and stability in the financial system.

Embracing EU Compliance but Already Outdated

The background for Turkey's proposal to legalize cryptocurrencies is complex and varied. On one hand, the rapid growth of the cryptocurrency market and global regulatory trends have forced Turkey to confront the legitimacy and regulatory issues of this emerging financial tool. On the other hand, Turkey aims to enhance financial inclusion through cryptocurrencies, especially in areas lacking banking services, where financial tools like cryptocurrency debit cards can help users bypass traditional banking systems for convenient financial services.

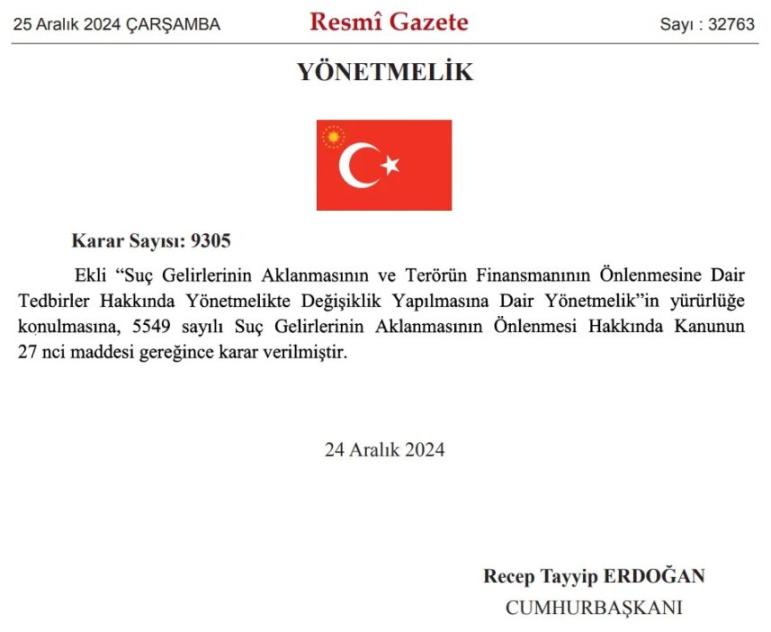

On December 25, 2024, the Turkish government announced the main provisions of the new anti-money laundering regulations, focusing on transaction thresholds, risk transaction handling, and restrictions on unregistered wallets, aiming to enhance the transparency and security of cryptocurrency transactions.

The introduction of this regulation coincides with the European "Markets in Crypto-Assets Regulation" (MiCA) coming into effect on December 30, 2024. MiCA is regarded as the world's first comprehensive regulatory framework covering crypto assets. It provides detailed regulations on the issuance of crypto assets, the authorization, operation, reserve and redemption management of service providers, and anti-money laundering (AML) supervision. Additionally, MiCA integrates the travel rules of the "Transfer of Funds Regulation" (TFR), requiring cryptocurrency service providers (CASPs) to include sender and receiver information in each transfer to enhance traceability.

Turkey's regulatory framework has copied these regulations. However, as the United States gradually becomes a high ground for cryptocurrency compliance, continuously "loosening" regulations for the crypto industry, Turkey's compliance process has clearly fallen behind historical progress.

At least in the application of stablecoins, Turkey has yet to show any signs of "loosening." Since 2021, the Turkish government has recognized the trading attributes of cryptocurrencies, but the use of cryptocurrencies as payment tools has remained prohibited. This means that while investors can trade freely, they cannot directly apply cryptocurrencies in daily consumption scenarios, leaving the trillion-dollar payment market for stablecoins still on hold.

However, although the new regulations impose restrictions on certain trading activities, the Turkish government remains open regarding cryptocurrency tax policies. The Turkish government does not tax profits from crypto assets but only levies a 0.03% transaction tax, which is quite friendly to traders.

In summary, like countries such as Argentina, where fiat currencies are rapidly depreciating, Turkey's focus on cryptocurrencies remains on hedging against fiat currency depreciation risks. The demand for cryptocurrencies among Turkish residents is more about exchanging visibly depreciating Lira for on-chain stablecoins pegged to the dollar. After all, the Turkish Central Bank's foreign exchange reserves have already turned negative. Compared to the high fees and low security of traditional black markets, on-chain high liquidity stablecoins have become the preferred means of value storage. Compared to Turkey's traditional "gold under the mattress" reserves, "stablecoins under the pillow" have also begun to gain popularity. The extensive layout of Tron in payments, exchanges, and other areas in Turkey is enough to illustrate the broad market demand in Turkey.

However, regarding the application of stablecoins for cross-border payments and stock tokenization, Turkey has yet to become an innovative hub.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。