Author: Awang

Stablecoins are the most representative practical tools in the field of digital currency, showcasing how blockchain can provide a new and efficient infrastructure for traditional financial payment systems. Over the past year, the total market value of stablecoins has grown by more than 50%; since Trump's re-election in November, it has accelerated even further. Currently, the total market value of stablecoins exceeds $250 billion, and it is on the brink of an explosive period. This scale has already facilitated the efficient circulation of trillions of dollars in global payment funds.

Industry insiders are well aware of the value of stablecoins: they vividly embody the core capability of blockchain to "transfer funds and value instantly," making it possible to build a business closed loop on-chain—payments. However, payments go far beyond the "peer-to-peer transfer" stage; real enterprise-level scenarios are much more complex than simply "sending money from A to B."

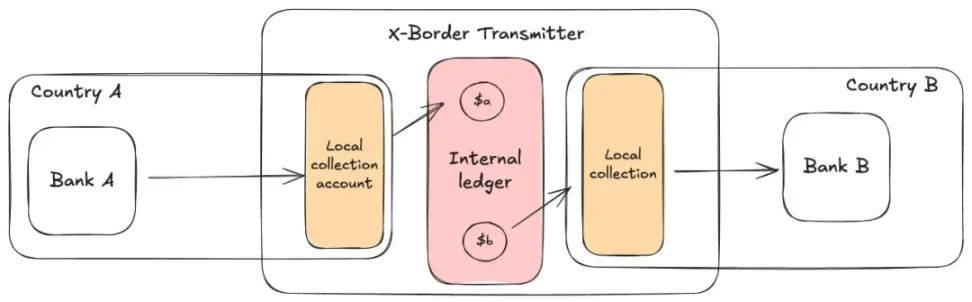

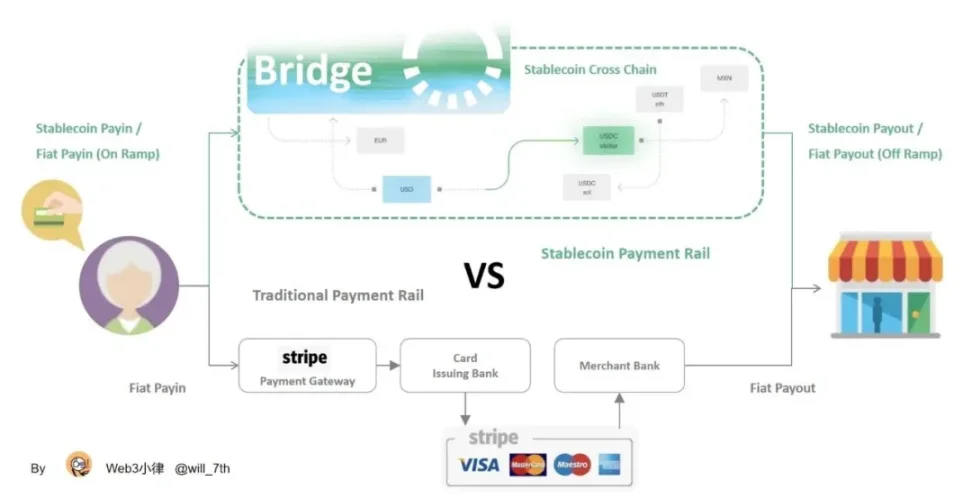

Currently, most enterprise-oriented stablecoin applications adopt a "Stablecoin Sandwich" architecture, a term first proposed by Fireblocks' Senior Vice President of Payments and Networks, Ran Goldi, in 2021: using blockchain to replace traditional payment channels for horizontal value/fund transfer, while still relying on outdated financial payment systems at both ends.

This design, while bringing significant improvements, also limits the full release of blockchain advantages. This is also the point that Airwallex CEO Jack criticized, noting that stablecoin payments have not demonstrated cost reduction and efficiency improvement.

Therefore, we will rely on Jesse's article "Unpacking the Stablecoin Sandwich" to examine how stablecoins can be applied to global cross-border payments from the perspective of global fund transfer. This article will:

- Dissect the existing global cross-border payment system;

- Analyze the specific improvements of the stablecoin sandwich architecture in fund management, B2B payments, and card network settlements;

- Explore how to overcome the challenges at both ends of the stablecoin sandwich, allowing the value of blockchain to permeate the entire process.

I. Background of Stablecoin Payments

Among the many applications of stablecoins, B2B enterprise payments are the most noteworthy. The latest Artemis report provides data from frontline payment companies: last year, the monthly B2B enterprise payment amount grew from $770 million to $3 billion. Fireblocks also reported that stablecoins accounted for nearly half of its platform's transaction volume, with 49% of customers actively using stablecoins for payments.

The internal data of leading companies can better reflect the scale of the segmented market. According to a report by FXCIntelligence, BVNK (considered one of the largest players in this field) processes about $15 billion annually, with approximately half coming from B2B enterprise payments—this is also the largest segment in cross-border payments. Conduit has an annualized transaction volume of $10 billion, which the company estimates accounts for about 20% of the global B2B stablecoin cross-border payment market; Orbital reported an annualized scale of $12 billion.

Specifically, the use of global payments is becoming increasingly widespread, as the shortcomings of financial payment infrastructure become more pronounced, amplifying the advantages of stablecoins based on blockchain infrastructure. SWIFT and correspondent banking networks successfully facilitate over $100 trillion in global payments each year; however, enterprises and banks still face significant complexity and delays.

II. Various Models of Global Cross-Border Payments

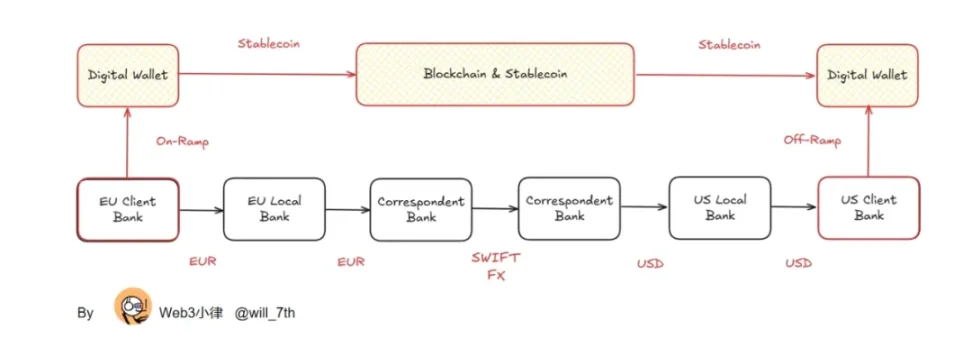

2.1 SWIFT-Based Banking Infrastructure

First, let’s look at how the current SWIFT-based global payment operates.

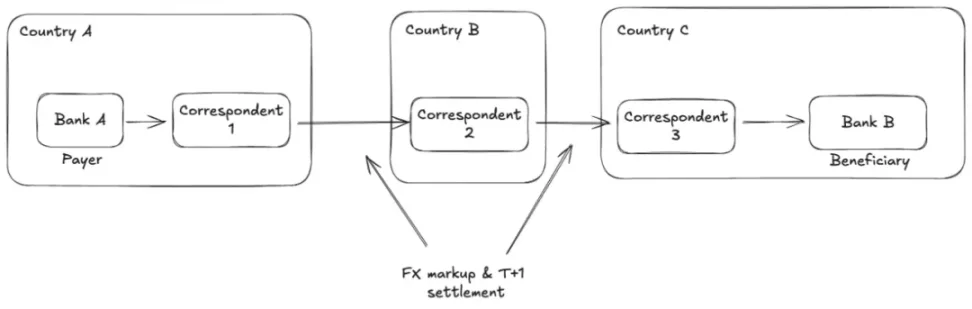

For transactions between banks in different countries, the entire process is divided into two parts: "message clearing" and "fund settlement": SWIFT is responsible for transmitting transfer instructions between banks, while the actual flow of funds only occurs between banks that have pre-established correspondent accounts and can directly conduct debit/credit transfers.

Jesse, Unpacking the Stablecoin Sandwich

Only when both banks are connected to the SWIFT system and are partners can the final transfer—fund settlement—be completed. If the two parties have not established a direct partnership, they must connect through correspondent banks that have the appropriate interfaces and positions to complete the fund settlement.

The following diagram illustrates a typical transaction on the SWIFT network: connecting two unrelated banks through a common correspondent bank.

Jesse, Unpacking the Stablecoin Sandwich

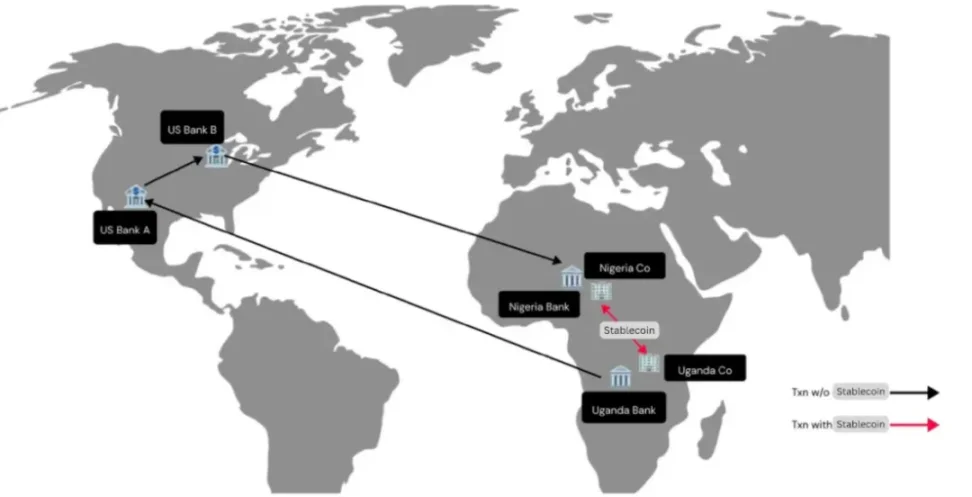

As more intermediary banks are required, settlement times can extend to several days, leading to rising costs, tracking challenges, and other issues. This also results in cross-border payments between neighboring countries with underdeveloped financial infrastructure needing to route through banks in the global north, causing significant inconvenience.

Stablecoins: Leapfrogging Africa's Financial System, Ayush Ghiya and Uchenna Edeoga

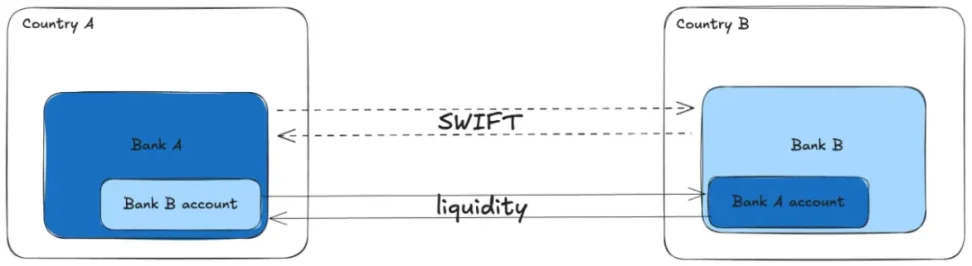

2.2 PSP-Based Cross-Border Fund Pool Model

The process described above is precisely the path that enterprises must go through when handling international wire transfers today: banks must connect to SWIFT and have clearing and settlement capabilities in the target payment corridor.

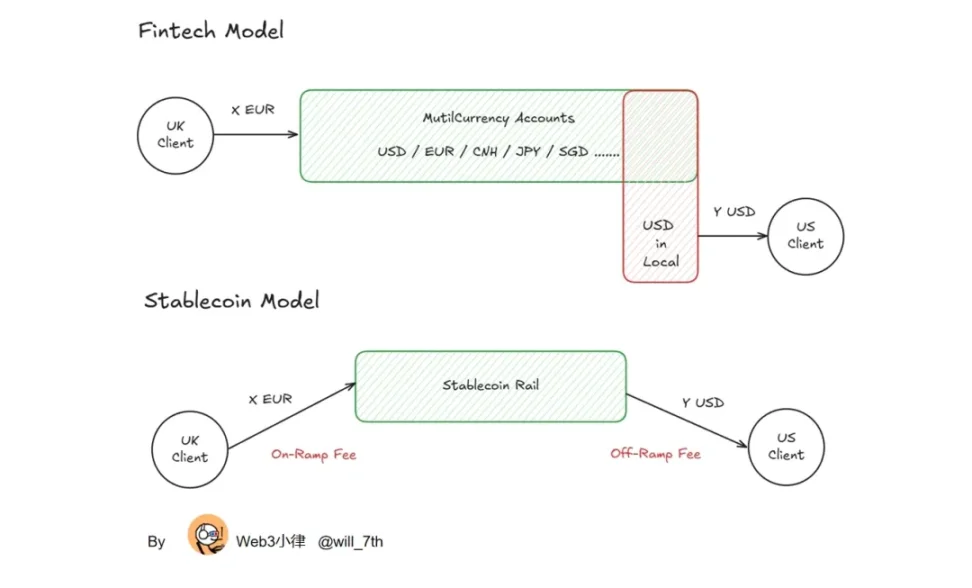

Thus, the service model of cross-border money transmitters (XBMT), also known as the cross-border payment companies we are familiar with, has emerged. They aim to enable enterprises to complete global payments without directly going through the SWIFT channel, a capability also referred to as "global multi-currency accounts" or "local receiving accounts."

Its essence is: the cross-border fund pool model.

The core of its service: providing enterprises with multi-currency fund pools, allowing them to make flexible payments between different countries.

XBMT is responsible for managing compliance and banking relationships, while enterprises or individuals receive a single multi-currency banking product, forming a "closed loop," meaning there are no external operators or dependencies to increase costs or complexity. If we compare it to a sandwich, the internal ledger is the meat in the sandwich, while the local receiving accounts in each region are the bread. Liquidity is managed internally between the accounts:

Jesse, Unpacking the Stablecoin Sandwich

XBMT has now secured an important position in the global B2B enterprise payment and corporate fund management market. They operate in a closed-loop model, preparing and dispatching the required liquidity in advance, then distributing it to enterprise clients as needed. By controlling the end-to-end process, XBMT sets strict limits and risk control rules for clients.

Despite appearing polished, XBMT still operates on the rails of SWIFT, relying on sophisticated liquidity management techniques to "manufacture" an instant payment experience. However, the speed and scale of such designs are always constrained by the available liquidity of XBMT in specific countries and the settlement efficiency of their underlying settlement rails.

Considering banking account capabilities and liquidity management, Airwallex has built a relatively complete "global multi-currency account" or "local receiving account" in the currently developed G10 countries, enabling relatively "zero-cost" fund disbursement. This presents a greater cost advantage compared to the "stablecoin sandwich" model, which incurs costs at both ends for inflows and outflows.

Therefore, the adoption of stablecoin payments requires clear situational advantages and cannot be generalized.

2.3 Stablecoin Model

If XBMT is a carefully designed "structured product" for B2B enterprise payment scenarios, then stablecoins represent a more fundamental leap: they leverage blockchain technology to reconstruct the operation of internet commerce.

The settlement cycle of stablecoins is equivalent to the block time of their issuing blockchain—this is an order of magnitude faster compared to SWIFT and correspondent bank transfers. Any system relying on traditional methods can be replaced by a shared, verifiable ledger that can track the issuance and ownership of stablecoins.

More critically, stablecoins are typically deployed on smart contract platforms, enabling innovative systems and workflows that traditional banking rails cannot achieve. For example, if XBMT wants to overlay a certain logic, it must do API integration with banks in various countries one by one; whereas on open, verifiable protocols (such as Ethereum's ERC or Solana's SPL standards), anyone can add functionality to stablecoins without permission.

From a macro perspective, faster and more interactive financial payments can directly amplify global GDP: enterprises can receive payments more quickly, allowing funds to enter downstream processes faster, thereby reducing management costs and capital occupation caused by settlement delays. When the settlement cycle is compressed from "days" to "seconds" or "minutes," its ripple effect will sweep through the entire economy. At the same time, the existence of verifiable standards allows financial innovation to occur globally without permission for the first time—this is a qualitative change that traditional financial systems cannot reach.

III. Applications of Stablecoins in Global Payments

Given the aforementioned advantages of stablecoins, we can now see some specific global payment use cases that benefit from stablecoins. We will explore how global fund management, B2B enterprise payments, and card organization network settlements operate today, and discuss the applications and advantages of stablecoins in various fields.

3.1 Enterprise Fund Management

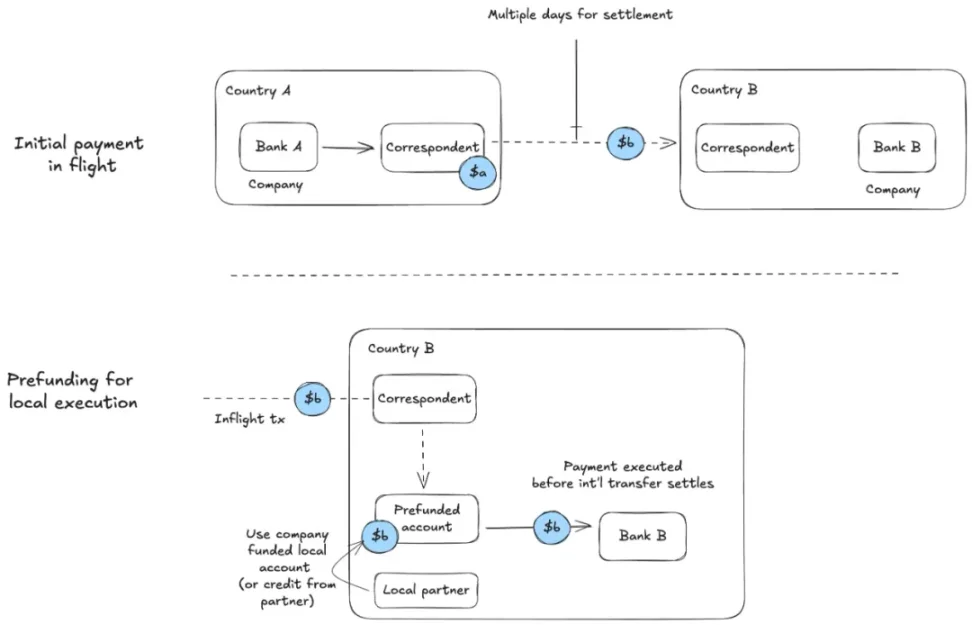

Taking enterprise fund management as an example: for instance, a company has an obligation to make a payment in currency b in country B on a certain date. They must prepare for a fund transfer from country A in currency a before the payment is due:

Jesse, Unpacking the Stablecoin Sandwich

This is a prepayment process, and the enterprise finance team must consider the preparation time required to execute the payment in a timely manner.

The team must open a local bank account to execute payments on time. Sometimes, to support this, the company may seek short-term loans from partners in the region. The longer the global fund settlement is delayed, the greater the foreign exchange risk exposure, and the higher the capital requirements for the enterprise finance department. For companies that only want to execute global payments, managing derivatives to hedge currency risks and calculating short-term liquidity will significantly increase operational expenses.

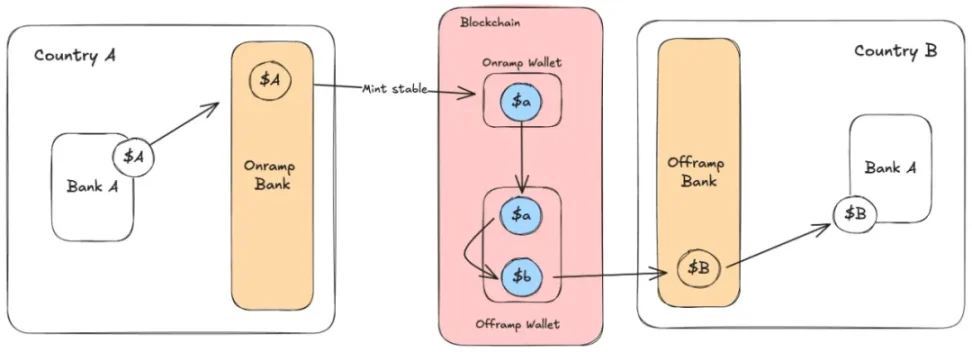

Stablecoins simplify this system by eliminating the need for control over international settlement delays:

Jesse, Unpacking the Stablecoin Sandwich

We can see the role of the "Stablecoin Sandwich" structure: although the initial inflows and outflows at both ends still need to touch the fiat currency system, the existence of stablecoins allows for smooth fund flows between the two fiat currency "ramps."

By using stablecoins, the entire processing is split into local transfers within countries A and B, while the blockchain completes the global liquidity settlement between the two parties in the middle. (Note: For this exchange to succeed, there must be sufficient liquidity on-chain to convert stablecoin A into stablecoin B.)

3.2 B2B Enterprise Payments

The process of global B2B enterprise payments is similar to enterprise fund management, but B2B scenarios can yield greater benefits because B2B payments are often more complex, and their success may affect other aspects of enterprise operations.

In these payments, banks in different countries are often directly linked to the delivery of a service or goods. This means that all parties are more sensitive to the tracking of payment progress. For example, in the "pre-financing" diagram mentioned earlier, the cost of pre-financing may depend on the real-time status of an inbound payment.

Additionally, if the payment channel required by the enterprise is relatively obscure, they often need to go through multiple international transfer paths to complete the fund allocation—such paths may lack clear progress reporting mechanisms and are subject to the non-24/7 operating hours of banks, making payment times easily prolonged.

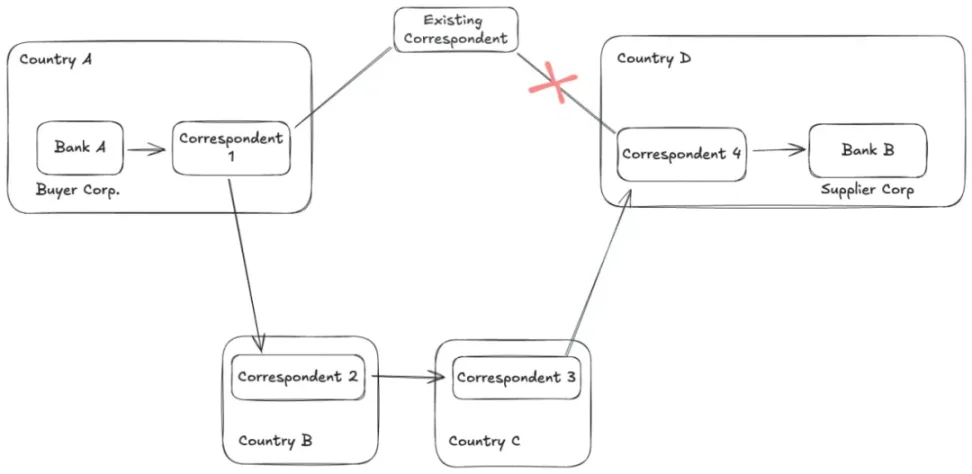

Let’s look at another example: a company in country A wants to make a payment to a company in country B, but the banks in the two countries do not frequently conduct business with each other. If the bank in country A has no direct connection on any suitable path to country B, this payment must take an additional detour:

Jesse, Unpacking the Stablecoin Sandwich

When these B2B cross-border payment processes are executed through stablecoins in the middle of the link, a series of additional benefits emerge at the enterprise level:

- Both parties can clearly and in real-time manage and monitor the payment status.

- Financing can be directly linked to time-sensitive raw materials or delivery nodes, allowing enterprises that heavily rely on timely arrival of goods to avoid significant risks or delays.

- With reduced risks, capital costs decrease, and capital turnover speeds up; as stablecoin integration solutions mature, this effect will bring considerable productivity improvements globally.

Similar to the enterprise fund management scenario, the correspondent bank links, pre-financing needs, and most foreign exchange exposures are essentially removed. The entire process is compressed from the previous 3 days to just a few seconds, without considering market closures, significantly reducing and simplifying working capital requirements.

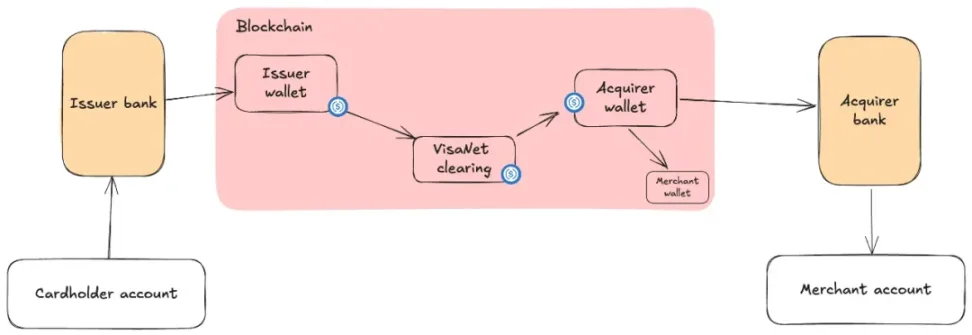

3.3 Card Organization Network Settlements

In card organization networks, issuing institutions send payments to the acquiring bank on behalf of cardholders, and the acquiring bank receives the payment and credits it to the merchant's account. These banks do not directly settle debts; they are all connected to VisaNet, which conducts net settlements between banks during business hours on weekdays. Each bank must maintain a prepaid balance to facilitate timely wire transfers.

Visa began trialing the use of stablecoins for settlements between acquiring banks and issuing banks as early as 2021. This method of using stablecoins replaces the wire transfer process, instead utilizing USDC on Ethereum and Solana. After completing card authorizations on specific dates, Visa uses USDC to debit or credit the banks of the transaction parties:

Jesse, Unpacking the Stablecoin Sandwich

Since this system operates within VisaNet, its net effect benefits the partners in the network. This is most similar to the closed-loop system of XBMT, but the large scale of the card organization network benefits issuing/acquiring institutions (as they previously had to manage global payments).

The advantages of stablecoins are similar to those in fund management, but these advantages belong to the banks within the network: they can reduce the capital requirements needed for timely international transfers, thereby avoiding foreign exchange risks. Additionally, the openness, verifiability, and programmability of blockchain lay the foundation for credit and other financial interactions between banks within VisaNet.

IV. Conclusion

Through the previous discussion, we have seen that the "Stablecoin Sandwich" is indeed useful in certain scenarios; however, most stablecoin applications currently remain at this sandwich structure and have not further broken through. Why is this the case?

In reality, very few enterprises truly use on-chain payments and stablecoins. As long as any link still needs to touch the fiat currency rails, we have to sandwich more bread at both ends of the "sandwich." We are merely adding some protein to the original vegetarian sandwich, but it remains a sandwich.

The ultimate goal of stablecoin payments is to completely remove the bread at both ends. When enterprises and consumers fully embrace stablecoins, the entire financial and commercial cycle can be completed on the blockchain, freeing us from the constraints of outdated traditional rails. Once financial institutions and enterprises settle entirely in stablecoins, it will unleash unprecedented commercial scale. With significantly reduced global friction in enterprise construction, operation, and service, the growth curve of global GDP will align more closely with the true consumption speed of goods, services, and content on the internet.

Therefore, the essence of PayFi is actually: Stablecoin Payments + On-Chain Finance. If we can completely break free from the sandwich structure and build more on-chain financial services at both ends, the speed of global fund/value transfer will reach unprecedented heights.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。