Author: Web3 Farmer Frank

Compliance ascension, DEX explosion, offshore squeeze, the ultimate fate of Crypto exchanges has no middle ground.

Have you ever thought that Crypto trading will also be taxed in the future?

Since this spring, many users from mainland China who have been trading U.S. stocks through Tiger Brokers, Futu Securities, and others have gradually received back tax notices. This is no coincidence; with the implementation of CRS global information exchange, offshore accounts and investments are being monitored from high-net-worth individuals to ordinary middle-class citizens.

The reasoning is similar; the "sovereign vacuum period" in finance is often very short. Today's U.S. stock brokers are not a rehearsal for tomorrow's Crypto trading—once the wild era is over, Liangshan will inevitably be incorporated into the regular army:

From the invisible freedom of offshore U.S. stock accounts to the global information exchange of CRS, from the barbaric growth of third-party payments to the strict control of central bank licenses, financial innovations that drift outside mainstream regulation are moving from gray to standardized, an irreversible one-way street.

Especially since this year, with the entry of Web3 and the involvement of power, Crypto exchanges can be said to be at a crossroads of fate. Compliance localizers are firmly in control, the offshore gray space is rapidly shrinking, and on-chain DEX is gaining momentum.

There is no middle ground, only clear directional distinctions.

Offshore CEX, the feast is over

Centralized exchanges (CEX) remain the top predators in the current Crypto ecosystem.

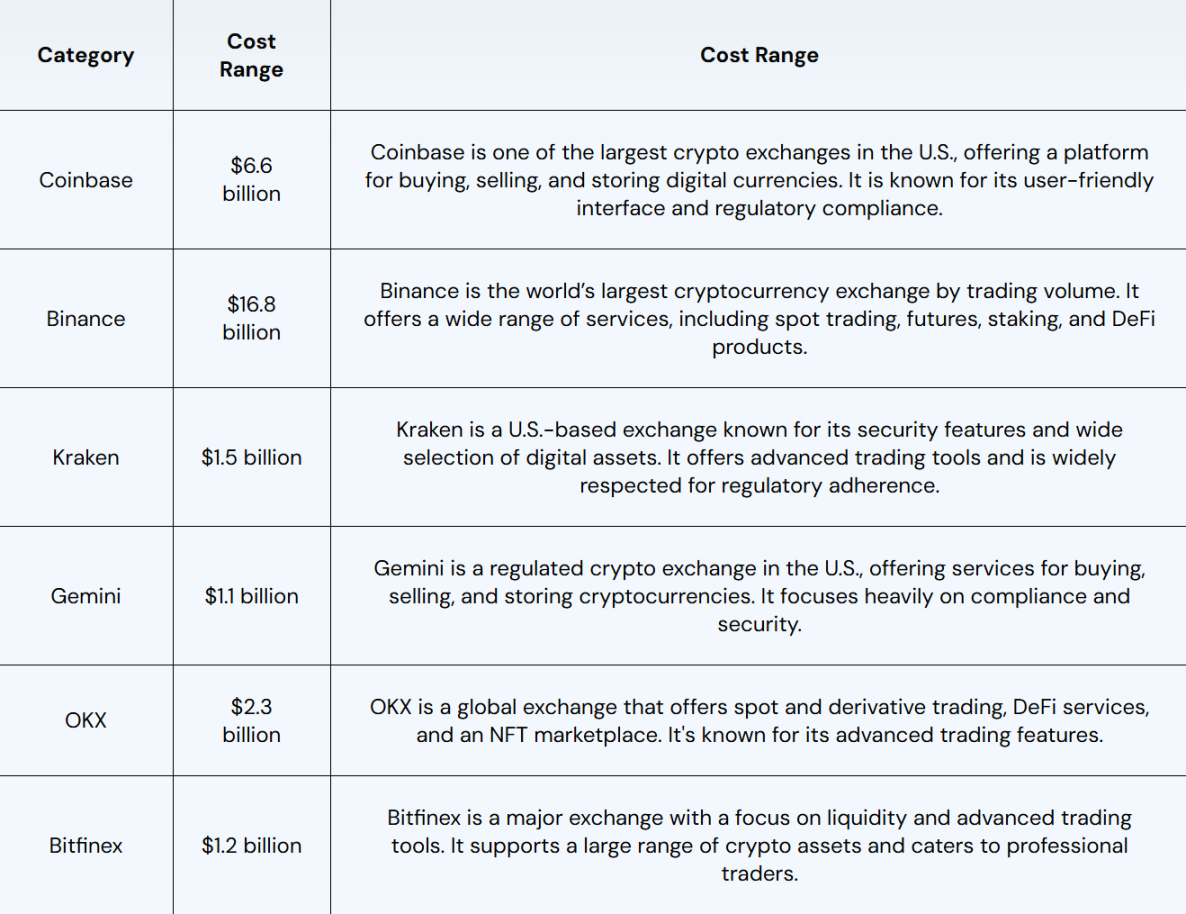

It can be said that CEX, which relies on trading fees as its core revenue source, has reaped the largest dividends from the explosive growth of Crypto. According to public market estimates, the current annual revenue and profit of leading offshore CEXs like Binance and OKX are in the tens of billions to over a hundred billion dollars, for instance, Binance's annual revenue in 2023 reached 16.8 billion dollars, with annual cryptocurrency trading volume exceeding 3.4 trillion dollars.

This means that even in a turbulent global macro environment, offshore CEX remains one of the most profitable businesses.

Source: Fourchain

However, the golden age of the offshore model has clearly come to an end.

Compliance pressure and tax storms are extending from traditional finance to the Crypto field. Similar to the recent uproar over back taxes on U.S. stock trading, observant users should have noticed that in the past year, offshore CEXs like Binance and OKX have also gradually stirred up public controversies:

Including but not limited to restricting accounts by treating cryptocurrency assets as the sole source of income and requiring users to provide proof of annual income and tax payments, etc.

Objectively speaking, offshore giants like Binance and OKX have paid a high price to "go onshore." In addition to the legal accountability faced by their founders, significant funds have also been invested—Binance has publicly disclosed that it invested hundreds of millions of dollars in compliance and security in 2024, and its internal compliance team has grown to 650 experts.

Especially since 2025, companies have been accelerating compliance and potential listings during the "political dividend window."

For example, Kraken first had the U.S. SEC withdraw its securities violation charges against it, and the FBI also ended its investigation into its founder, subsequently hinting at potential IPO plans. Recently, there have been reports of raising 500 million dollars at a valuation of 15 billion dollars, fully turning towards compliance.

OKX is similar; it first reached a settlement with the U.S. Department of Justice in February this year, paying over 500 million dollars in fines, and then actively promoted its IPO in the U.S., even adjusting its compliance department in the U.S. to the highest priority among all departments.

These actions send a clear signal that the survival space of the offshore model has been compressed to a historical low, and CEXs are racing to seize the last compliance window.

It can be said that this Crypto political honeymoon period, catalyzed by Trump's reshaped policy narrative, the "balance sheetization" of BTC, and the stablecoin boom, is almost the last window for offshore CEX transformation.

Once the opportunity to "go onshore" is missed, they may fall from top predators in the ecosystem to targets cleared by the times.

The foreseeable pattern of "three kingdoms"

If we compare today's Crypto market to the Hong Kong and U.S. stock markets that Chinese investors participated in ten years ago, then the evolution of regulation and the market is merely a few years behind.

As global tax compliance, capital controls, and the entry of financial institutions overlap, the future landscape of exchanges can almost be foreseen as "three kingdoms":

- Localized licensed compliant CEX: Represented by Coinbase, Kraken, HashKey, OSL, etc., characterized by having banking connections and compliance clearing capabilities, primarily serving local users and institutions/high-net-worth individuals, building long-term brand value through compliance moats;

- Offshore gray CEX: Represented by Binance, Bitget, Bybit, etc., serving global retail and some high-risk users, will inevitably be compressed, eroded, and marginalized under the current global compliance trend and on-chain experience;

- Pure on-chain decentralized exchanges (DEX / DeFi native): No KYC required, permissionless access, natively supporting on-chain asset settlement and multi-chain composite trading, may become a new global liquidity hub in the future;

Among them, compliant exchanges are undoubtedly the "upward curve players" benefiting from policy dividends. In markets like the U.S. and Hong Kong, compliant exchanges can not only engage in partnerships with institutions and banks but also be incorporated into local tax systems. The strategic goal of such platforms is clear—to become the next generation of digital asset exchanges and clearinghouses.

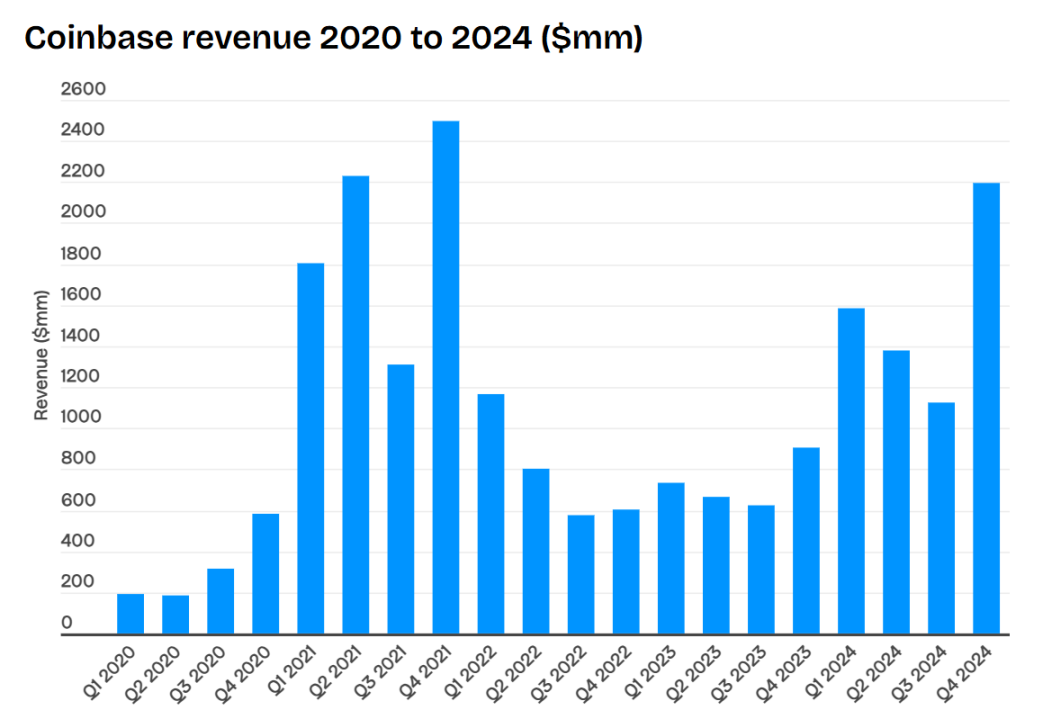

For example, an easily overlooked signal is that compliant exchanges represented by Coinbase are ushering in their golden moment—projected revenue for Coinbase in 2024 is 6.564 billion dollars, more than double year-on-year, with a net profit of 2.6 billion dollars, nearly approaching 50% of offshore leader Binance (according to market estimates).

More critically, Coinbase hardly needs to worry about enforcement actions from mainstream jurisdictions or risks of bank freezes, making it a natural "safe haven" for institutions and high-net-worth users.

On-chain DEXs belong to the "global market players" with the greatest potential and highest ceilings. They do not rely on national licenses and serve as a 24/7 global liquidity hub, especially with native support for on-chain asset settlement and cross-asset composite strategies, offering strong programmability.

Although their current market size is still less than 10% of CEXs, the growth elasticity is enormous. Once the on-chain derivatives market matures, the market depth and strategic space of DEXs will attract a large influx of high-frequency funds, arbitrageurs, and institutional liquidity.

For instance, Hyperliquid saw its capital grow rapidly in July, increasing from just below 4 billion dollars at the beginning of the month to 5.5 billion dollars, and at one point approaching 6 billion dollars in mid to late July.

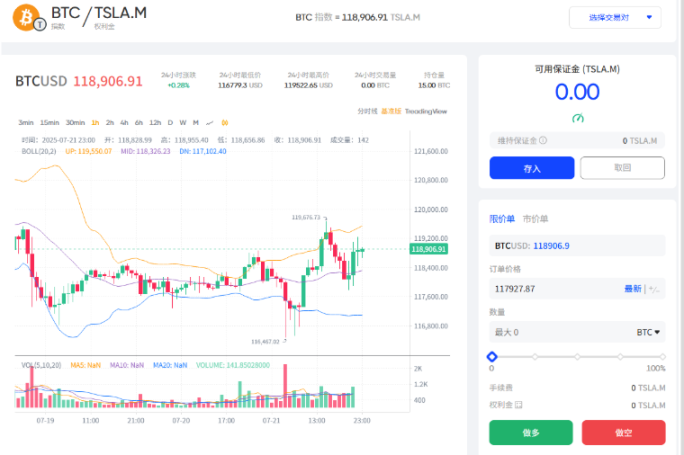

Moreover, the DEX model is not only a carrier of DeFi innovation but may also become the cornerstone of decentralized pricing for global commodities and crypto assets, just like Fufuture's newly launched TSLA.M/BTC index trading pair based on "coin-based perpetual options":

Allowing users to use TSLA.M as collateral to participate in BTC/ETH perpetual options trading not only explores new liquidity paths for tokenized U.S. stocks but can also be used to help build pricing pools for tokenized gold/oil products or other small market cap meme assets.

Overall, the strategic significance of Fufuture's DEX derivatives mechanism, which integrates options and perpetual contracts, lies in transforming long-tail assets (such as SHIB, TSLA.M, etc.) that could only sit in wallets into usable collateral, activating cross-asset liquidity, forming a natural positive cycle of "holding positions equals participating in liquidity construction," and making the on-chain market closer to the capital efficiency and depth of traditional derivatives markets.

In contrast, offshore CEXs have already reached their peak, and their survival space is being sharply compressed. On one hand, they are caught between compliance and on-chain, lacking long-term survival space; on the other hand, the tightening of global regulation, CRS tax information exchange, and the bank KYC system make it difficult for gray traffic to sustain.

It can be said that the feast of the offshore model has come to an end. In the past, it served as a "gray buffer zone" to accommodate regulatory arbitrage space; in the future, it may linger on the policy edge for a long time, being eroded by both compliant exchanges and on-chain markets: either integrate into the tax and compliance system to become localized licensed institutions; or completely transition to on-chain, becoming a borderless global market.

The middle ground is destined to be cleared.

New Proposition for DEX: Decentralized Pricing of Global Assets

From a longer-term perspective, the future competition among exchanges is not merely a contest of traffic and fees, but a battle over the rewritten rules of the global market.

If the first phase of DEX was more of a testing ground for DeFi innovation, then with licensed localized exchanges in the U.S., Hong Kong, and elsewhere accommodating compliance needs, integrating into tax systems, and fully aligning with the banking system, the mission of DEX may be completely reshaped:

It may take on the role of "price discovery and pricing power" for the global permissionless market.

Why should the pricing power of global assets belong to on-chain DEXs?

- Because unlike stocks and bonds, which have obvious regional attributes (except for U.S. stocks and bonds), commodities like gold, oil, copper, and crypto assets like BTC and ETH are inherently global trading targets;

- At the same time, traditional commodity futures are concentrated in places like Chicago, London, and Shanghai, which have time zone and trading hour limitations, while on-chain operates 24/7, providing time-zone-free, permissionless liquidity;

- Even better, stablecoins can serve as globally accepted settlement tools—if users open positions using stablecoins as collateral, all profits and losses are settled in stablecoins, meaning price discovery will no longer be limited by geography or banking systems;

With these three characteristics, DEX is naturally expected to become the cornerstone of decentralized pricing for crypto assets and commodities.

Source: CoinGecko

Of course, for DEX, what truly supports price discovery is never just simple spot trading, but rather the trading depth and price discovery mechanisms constructed by derivatives systems such as futures and options.

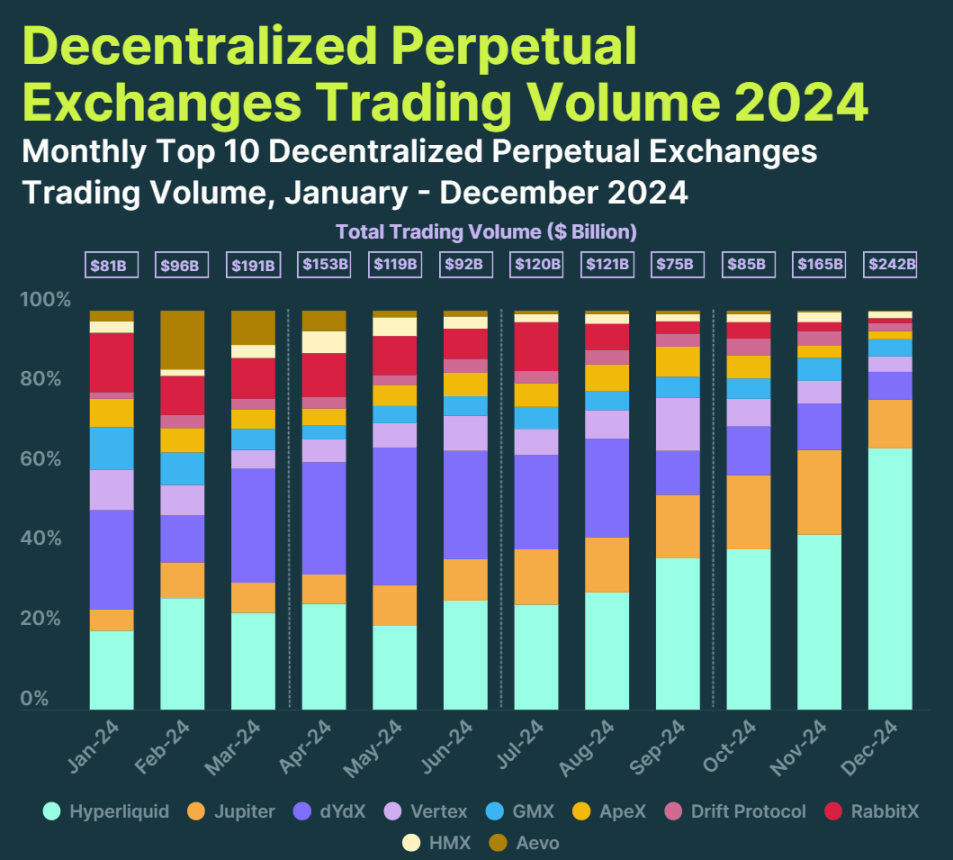

This is also why the derivatives DEX is experiencing explosive growth in 2024, with total trading volume for Perp DEX reaching 1.5 trillion dollars, more than doubling from 647.6 billion dollars in 2023.

Among them, futures contracts are primarily represented by Hyperliquid, with annual trading volume skyrocketing from 21 billion dollars in 2023 to 570 billion dollars in 2024, achieving a growth of 25.3 times. Recently, Hyperliquid has also entered the top five derivative platforms by daily trading volume, peaking at over 10 billion dollars in daily trading volume, on par with some mid-tier CEXs.

Source: Hyperliquid

On a more complex level of cross-asset strategies and on-chain derivatives pricing logic, Fufuture also provides a concrete example. Its "coin-based perpetual options mechanism" has no fixed expiration date and dynamically charges premiums based on holding time, balancing the non-linear returns of options with the trading rhythm of perpetual contracts.

If you have truly experienced Fufuture's perpetual options products, you can clearly feel the innovations compared to traditional on-chain options products. Taking users holding SHIB as an example, this type of meme asset can hardly serve as any form of trading collateral in traditional on-chain derivatives protocols, but on Fufuture, simply depositing SHIB into the platform allows it to be used as margin for trading.

In practical terms, as long as SHIB is deposited as "available margin," the entire trading process is almost indistinguishable from contract trading—there is no need for stablecoins as margin, no need to weigh options for expiration dates, strike prices, or profit and loss curves. Just like regular contract trading, you can choose the underlying asset, direction (long/short), and opening quantity to start trading.

At the same time, it theoretically allows any on-chain asset, including the latest tokenized U.S. stocks, to be activated as available margin—users can use TSLA.M and NVDA.M as margin to participate in BTC and ETH perpetual options strategies (further reading: "Liquidity Considerations for Tokenized U.S. Stocks: How Should On-Chain Trading Logic Be Reconstructed?"), forming a true cross-market speculation and hedging network that traditional CEXs find difficult to provide.

From an industry perspective, on-chain derivatives DEXs like Hyperliquid and Fufuture not only avoid compliance restrictions but also provide a 24/7, borderless trading and settlement network for global commodities.

Especially for new trading mechanisms like Fufuture's that do not require prior conversion to stablecoins and allow users to open positions simply by choosing a direction, maximizing the liquidity and strategic space of on-chain assets, not only does the trading experience approach that of CEXs, but objectively, only on-chain derivatives DEXs can achieve this, with the potential to become the on-chain "entry point for pricing power" of global assets.

In Conclusion

The future of exchanges is not merely a race for immediate gains, but a distinction between the rewriters of global market rules.

One will be localized and compliant, one will be offshore and gray, and one will become the cornerstone of decentralized pricing for the next round of global commodities and crypto assets.

There is no middle ground.

At the future crossroads, the direction is set; it is only a matter of time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。