If the previous cycle was ignited by MicroStrategy in the Bitcoin bull market, then the engine of this round of market activity is undoubtedly the "Altcoin MicroStrategy." Companies like SBET and BMNR, which are treasury companies on Ethereum, have been continuously buying, pushing the price of ETH from $1,800 in early May all the way up to $4,700, an increase of over 160%, and playing a new leading role in market sentiment. Meanwhile, mainstream altcoins like SOL, BNB, and HYPE have also followed suit, resulting in a wave of companies centered around treasury accumulation, further amplifying market expectations for an upward trend.

However, as this model spreads, risk signals are gradually emerging. Recently, BNB treasury company Wint faced delisting risks, and Hype treasury company LGHL was reported to be selling tokens, raising market doubts about the sustainability of the "treasury strategy." What potential risks are hidden in this centralized buying approach? What concerns should investors be aware of while chasing high returns? This article will conduct an in-depth analysis.

Company Competition: Capital Will Only Choose a Few Winners

The competition among "treasury companies" can be described as a life-and-death market elimination match.

Windtree Therapeutics (WINT) made a high-profile announcement in July to establish a BNB strategic reserve, but due to weak fundamentals and a continuously depressed stock price, it ultimately received a delisting notice from Nasdaq on August 19. Following the announcement, WINT's stock price plummeted, falling 77.21% in a single day, with the current price only at $0.13, a cumulative drop of 91.7% from the $1.58 price after the announcement. For a small biopharmaceutical company that is already in the clinical stage and has not yet achieved commercialization, with quarterly losses continuously expanding, delisting almost means being completely marginalized by the market.

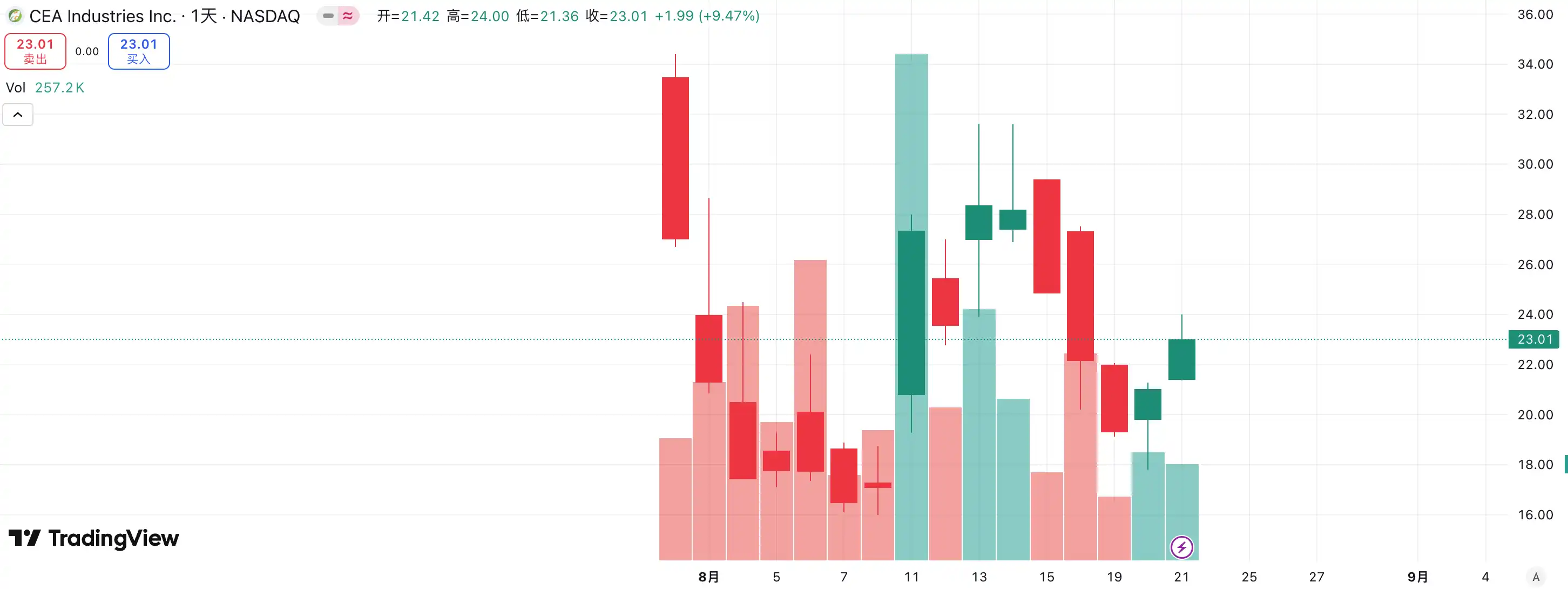

In stark contrast is another new player—BNB Network Company (BNC, formerly CEA Industries). With the support of YZi Labs, BNC completed a $500 million private placement from late July to early August, with CZ personally involved, and a total of 140 participating institutions, including top-tier capital like Pantera Capital, Arrington Capital, and GSR. The company also invited David Namdar, former co-founder of Galaxy Digital, to serve as CEO, and former CalPERS Chief Investment Officer Russell Read to lead investment decisions, almost overnight completing the leap from a traditional small-cap stock to a "BNB legitimate treasury company."

The choice of capital has already provided an answer: WINT has become a "discard," while BNC has become the new market flagbearer. Data shows that BNC's stock price rose 9.47% yesterday, currently at $23.01, further strengthening its leading position in the "BNB treasury company" sector. It can be said that this competition is not only a showdown of company fundamentals but also a vote on narrative and resource integration capabilities.

Related Article: "The First BNB Reserve Company WINT Delisted, Is the 'Token Hoarding Strategy' No Longer Effective?"

In the ETH treasury company sector, competition is equally fierce. SBET, led by Joseph Lubin, was the first publicly listed company to propose the "ETH MicroStrategy" concept, quickly triggering strong FOMO in the early market due to its first-mover advantage and the narrative of being an ETH spokesperson, soaring from $3 to over $120, becoming a benchmark case for the altcoin treasury model.

However, the rise of BMNR quickly changed the landscape. As a latecomer, it not only surpassed SBET in buying intensity and capital scale but also boldly proclaimed the slogan "Hold 5% ETH," instantly elevating market imagination. More critically, BMNR has the public backing of Wall Street veterans like Tom Lee and Cathie Wood, allowing it to quickly dominate in institutional and media circles. In contrast, while SBET has the endorsement of a Web3 newcomer like Joseph Lubin, it is clearly at a disadvantage in terms of discourse power and influence compared to BMNR, which has allied with "old money" from Wall Street.

The stock price trends of the two also confirm this differentiation. In August, SBET's stock price rose from $17 to a peak of $25, an overall increase of about 50%; BMNR, on the other hand, rose from $30 to a peak of $70, an increase of over 130%, significantly outperforming the former. As BMNR gradually gains recognition from mainstream capital and opinion leaders, the competitive landscape among ETH treasury companies has shown a clear trend of mutual decline.

The insight behind this competition is that the "treasury company" sector has entered a phase where the strong get stronger. With the participation of institutional investors and leading capital, market resources are accelerating towards a few companies that possess capital integration capabilities, narrative driving force, and governance abilities. Small companies find it hard to survive in this model; even if they promote the "treasury" concept, they cannot withstand the market's scrutiny of performance and capital strength. Ultimately, the sector will only leave a few true winners capable of absorbing capital and narrative, while bubbles and followers will be quickly eliminated.

Token Selling Concerns: Strategic Reserves Do Not Equal Permanent Holding

If Bitcoin's bull market has the faith of Michael Saylor backing it, then the "treasury bull" of altcoins seems more realistic. Saylor has consistently claimed that MicroStrategy "will never sell" its Bitcoin and has continued to buy through ongoing financing, bringing a steady stream of buying pressure and confidence to BTC. Nevertheless, the question of "Will MicroStrategy sell tokens?" has always been a focal point of market discussion. While altcoin treasury companies have emulated this model, they have never made a "no selling" commitment, leaving the market with greater concerns about their stability.

Recently, HYPE treasury company Lion Group Holding Ltd. was reported to have sold $500,000 worth of HYPE tokens. Just a month ago, the company announced the launch of its HYPE treasury strategy after completing $600 million in financing, aiming to position $HYPE as a core reserve asset and build a next-generation Layer-1 treasury portfolio through the allocation of tokens like $SOL and $SUI, clearly stating that it would continue to increase its holdings of these tokens. However, the recent reduction in holdings has led to speculation about its asset allocation logic: is this a tactical diversification adjustment or a risk response to the recent market downturn? Although the sell-off amount is only $500,000, which is negligible compared to the $600 million financing, it still serves as a wake-up call for the market.

Similar examples are not uncommon. Meitu Inc. once spent about $100 million to buy BTC and ETH, and then cashed out when BTC broke $100,000 at the end of 2024, selling at nearly $180 million, making a profit of about $79.63 million. Although Meitu is not a treasury strategy company, this operation illustrates that when prices rise to a certain level, the so-called "strategic reserves" can completely transform into tools for profit-taking.

Currently, there has not been a large-scale collective sell-off by treasury companies, but potential risks cannot be ignored. Whether due to profit motives or fear of future market conditions, treasury companies could become sources of selling pressure. Lion Group's reduction in holdings is a reflection of this concern: as one of the first entrants in the HYPE treasury strategy, its sell-off undoubtedly sounds the alarm—once the "treasury army" chooses to sell off collectively, the stampede effect could ignite instantly, and the bull market may come to a sudden halt under its own engine pressure.

mNAV Flywheel: Infinite Bullets or a Double-Edged Sword?

The financing flywheel of treasury companies is built on the mNAV mechanism, which is essentially a reflexive flywheel logic that gives treasury companies the ability to seemingly have "infinite bullets" in a bull market. mNAV refers to the Market Net Asset Value ratio, calculated as the company's market capitalization (P) relative to its net asset value (NAV) per share. In the context of treasury strategy companies, NAV refers to the value of the digital assets they hold.

When the stock price P is higher than the net asset value NAV (i.e., mNAV > 1), the company can continue to raise funds and reinvest the raised capital into digital assets. Each issuance and purchase will push up the per-share holdings and book value, further strengthening market confidence in the company's narrative and driving the stock price higher. Thus, a closed-loop positive feedback flywheel begins to turn: mNAV rises → fundraising → buying digital assets → per-share holdings increase → market confidence strengthens → stock price rises again. It is through this mechanism that MicroStrategy has been able to continuously finance and buy Bitcoin over the past few years without severely diluting its shares.

However, mNAV is a double-edged sword. A premium can represent a high level of market trust, but it may also simply be speculative hype. Once mNAV converges to 1 or falls below 1, the market shifts from "enrichment logic" to "dilution logic." If the price of the token itself drops at this time, the flywheel will switch from positive to negative feedback, resulting in a double whammy of market capitalization and confidence. Moreover, the financing of treasury strategy companies is also based on the premium flywheel of mNAV; when mNAV remains at a discount for an extended period, the space for further issuance will be blocked, and the business of small-cap shell companies that are already stagnant or on the verge of delisting will be completely overturned, causing the established flywheel effect to collapse instantly. Theoretically, when mNAV is 1, a more reasonable choice for the company is to sell holdings to repurchase shares to restore balance, but it should not be generalized, as discounted companies may also represent undervalued assets.

In the 2022 bear market, even when MicroStrategy's mNAV briefly fell below 1, the company chose not to sell its Bitcoin for buybacks but instead insisted on retaining all its Bitcoin through debt restructuring. This "defensive" logic stems from Saylor's faith-based vision for BTC, viewing it as a core collateral asset that "will never be sold." However, this path is not one that all treasury companies can replicate. Most altcoin treasury stocks lack stable core businesses, and transitioning to a "buying coins company" is merely a means of survival, without the backing of faith. Once the market environment deteriorates, they are more likely to sell off to stop losses or realize profits, triggering a stampede.

How to Avoid the Potential Risks of the DAT Treasury Model?

Prioritize Companies that "Hoard BTC"

Most current treasury models are imitations of MicroStrategy, with Bitcoin always playing the role of the "industry cornerstone." As the only widely accepted decentralized digital gold globally, Bitcoin's value consensus is nearly irreplaceable. Whether traditional financial institutions or crypto-native giants, their allocation and expectations for Bitcoin have yet to reach long-term goals. For investors, choosing "BTC treasury companies" is often more robust and carries a greater long-term confidence premium than simply mimicking the treasury logic of altcoins.

Focus on Competitive Relationships and Prefer Leading Targets

The ecological competition in capital markets is extremely brutal. Especially in narrative-driven models like treasury strategies, the market often "only knows the first, not the second." The competition between WINT and BNC illustrates that once capital and support from orthodox institutions concentrate on one side, the other is almost quickly marginalized. In this context, investors should pay close attention to the "leading effect": the first place often secures more institutional funds, media narratives, and market trust, while the second and third places can easily be overlooked.

For retail investors, if there is insufficient judgment on individual stocks, directly allocating to the coins themselves may be simpler and more effective. In fact, even amid fierce competition at the company level, both ETH and BNB have reached historical highs without being affected.

Focus on Company Fundamentals

One of the core issues with the DAT model is that many treasury companies are essentially "shell companies," with their core businesses already stagnant, weak profitability, and almost entirely reliant on "speculating on coins" to survive. This model may seem reasonable in a bull market, but once the market reverses, it will bleed out instantly due to a lack of cash flow support. Therefore, when selecting targets, investors must pay attention to:

Company Cash Flow: Does it have self-sustaining capabilities?

Buying Cost: Is the average holding price sufficient to maintain health during a pullback?

Position Ratio: Is the proportion of digital assets to the company's net assets too high?

Use of Funds: Are the raised funds primarily used for buying coins, or are they for actual business expansion?

Debt Repayment Ability: Can it remain stable when convertible bonds mature or stock prices are under pressure?

Companies lacking self-sustaining capabilities may shine in a bull market, but during a liquidity retreat, their risk resistance is extremely weak, making them likely to be among the first casualties of a stampede.

Conclusion

The treasury strategy has undoubtedly injected the strongest fuel into this bull market, with a continuous influx of off-market funds allowing altcoins led by ETH to soar. However, the more a model appears to have "infinite bullets," the more one must be wary of the underlying bubbles and hidden concerns. History has proven that liquidity and narrative can ignite the market but cannot replace real value support. For investors, while the current market conditions are certainly optimistic, it is essential to remain calm and prudent. Only by maintaining rationality amid the noise can one stand firm when the next bubble recedes.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。