Written by: Charles Edwards, Founder of Macro Hedge Fund Capriole Investments

Translated by: Golden Finance

The era of treasury companies has arrived. Today, over 150 publicly listed companies worldwide have declared themselves as Bitcoin treasury companies, going to great lengths to raise capital with the sole purpose of purchasing more Bitcoin.

On average, they are scooping up $300 million worth of Bitcoin from the market every day. The speed is so rapid that Bitcoin treasury companies now hold 5% of the total Bitcoin supply (valued at $111 billion).

And it's not just Bitcoin; this trend has also spread to Ethereum (holding 3.4% of the supply) and a host of other altcoins, such as Ethena (ENA) and Tensor (TAO). How did we get here? Why are dozens of companies betting everything on Bitcoin every month? How far can the era of treasury companies go?

Chart: Bitcoin treasury companies hold 5% of the supply

In the past two years, the adoption of Bitcoin treasuries by publicly listed companies has grown exponentially, with over 150 companies actively purchasing Bitcoin. Source: Capriole Charts

The Success Story of Strategy

MicroStrategy (now renamed "Strategy," ticker: MSTR) adopted Bitcoin in August 2020. Initially, this was merely a means to combat the massive inflation triggered by the U.S. printing trillions of dollars to fill the deficit caused by the COVID-19 pandemic. Soon, Michael Saylor (CEO of Strategy) went all in. He raised capital at all costs through debt and equity issuance, with the sole purpose of buying Bitcoin. Before long, Strategy's original business disappeared from its homepage, becoming a distant sidekick to its new "only buy Bitcoin" model. As Bitcoin skyrocketed from $10,000 to $60,000 by the end of 2020, MSTR's stock price surged by 800%. Saylor raised billions of dollars, effectively taking advantage of the low capital costs in traditional financial markets and leveraging investments in the highest-return asset of our generation—Bitcoin.

MicroStrategy's stock price soared

Since adopting Bitcoin, MSTR's stock price has soared over 2500%, currently holding 3% of the total Bitcoin supply. Source: Capriole Charts

The Legend of Saylor

Michael Saylor's tech company had been struggling since the dot-com bubble burst, but due to his high conviction views on Bitcoin, sharp insights, and remarkable ability to break down complex topics into easily digestible pieces describing Bitcoin's value proposition, he became a star in the Bitcoin ecosystem. He became the spokesperson for Bitcoin. Some of his famous quotes include: "Laura, it will go up forever." (2021) and "How many chairs are you sitting on? Are you all in on chairs?" (2023), illustrating his belief in Bitcoin and the reasoning behind not needing diversification. By 2025, Saylor had become a meme. He posts AI-generated personal images spanning all time and history daily on X.com. He even depicts himself as a floating monk.

Michael Saylor's meme image on social media

Michael Saylor has become a meme on social media. Source: X.com

While amusing, Saylor's meme status is a significant factor behind Strategy's success. We live in a world where worthless tokens and stocks can soar under community-driven movements, often centered around memes. Think of GameStop (2020: +2000%), Dogecoin (2021: +10000%), AMC (2021: +300%), Shiba Inu (2021: millions %), Pepecoin (2023: 20000%), and dozens of other examples. Today, there are over 4000 meme coins with a total market cap of $66 billion, which have nothing behind them but an image and a community. People love communities and need a reason to collectively support an idea.

In a digital world with an annualized currency inflation rate of 10%, is this really surprising?

If an idea is attractive and enduring, it can attract billions of dollars at an astonishing speed. Michael Saylor's near-fanatical belief and cartoonish image fit many of these criteria.

Saylor's meme status is an important factor in his ability to attract capital and instill belief and confidence in the public, but this is just a small part of his $100 billion Strategy empire. How did he do it?

The Path to Strategy's Success

At its core, it’s about arbitrage. Bitcoin has an average annual return of 30-50%, while the cost of debt and equity Saylor uses to acquire Bitcoin is typically 0-5% per year. His debt instruments usually have a maturity of 5 years, so as long as Bitcoin maintains a high growth rate and Saylor does not over-leverage, he can withstand the brutal Bitcoin bear markets and win in the long-term arbitrage. He has employed nearly every possible method to raise funds, including issuing stocks, debt, convertible bonds, and warrants, orchestrating various deals to acquire capital at low costs. Saylor has also uniquely met market demand, satisfying the yield-hungry fixed-income market and providing them with avenues to achieve substantial Bitcoin returns.

In addition to developing a meme cult-like following of investors, Saylor has proven several things over the past 5 years:

His conviction is unwavering: Unlike many in the industry, Michael has explicitly stated and (so far) adhered to his commitment to "never sell" Bitcoin. Over the years, he has instilled confidence in investors regarding Strategy, its roadmap, and expected future actions. This has built trust in the investment community, alleviating much uncertainty and unlocking billions of dollars in capital for him.

He can weather the storm: Michael endured the brutal 80% bear market of 2022, multiple industry frauds, and bankruptcies. Strategy's Bitcoin holdings were once underwater (at a loss), but Saylor did not waver, sell, or "get liquidated" (as many speculated he might). Saylor proved he could withstand the blows of Bitcoin. He demonstrated he could manage risk and run his Bitcoin strategy long-term. This survival test added significant credibility to Strategy and Saylor's innovative Bitcoin treasury model.

I respect Michael Saylor. When he began his Bitcoin strategy in 2020, I remember telling my wife (then fiancée) while walking in Boxhagener Square in Berlin that it was a genius move that would bring tremendous returns to MicroStrategy. Especially since Bitcoin was severely undervalued at the time, and we were in the midst of the largest monetary inflation in history.

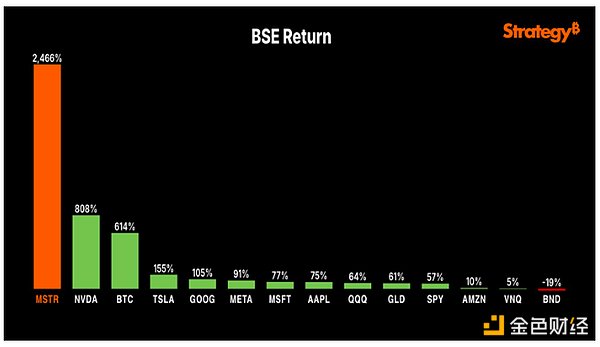

Fast forward 5 years, Strategy has outperformed the S&P 500, all asset classes, and all of the Magnificent 7 stocks, including the renowned Nvidia.

MicroStrategy outperforms the S&P 500 and Magnificent 7

Since adopting Bitcoin in 2020, MicroStrategy has outperformed the S&P 500 and all "Magnificent 7." Source: X.com

Given Strategy's immense success and Saylor's rising fame, it is no surprise that many imitators have flooded into this space. Where there is success, imitation follows. After the 2008 financial crisis, Warren Buffett made a piercing comment that may serve as a good warning for today's crypto industry: "First come the innovators. Then come the imitators. Finally, the idiots… People do not get smarter when it comes to greed, such a basic thing."

An Inevitable Story of an Era

Strategy is a story of success and motivation. But a series of other events have pushed Bitcoin treasury companies to the center stage and fueled their rapid rise, with two specific factors that cannot be overlooked: (1) rising global liquidity and (2) significant policy and regulatory drivers.

1. Rising Global Liquidity

When net liquidity is positive, Bitcoin tends to rise. Capriole measures net liquidity by subtracting capital costs (10-year interest rates) from the year-on-year growth of the global broad M3 money supply to determine when global markets are in a phase of liquidity expansion or contraction. In short; when more money is injected into the system, and its velocity exceeds the cost of debt capital, market participants tend to inject this fiat currency into assets like stocks, Bitcoin, gold, and real estate. All historical bear markets for Bitcoin have occurred during periods of decline in this indicator, while all deep bear market lows have occurred when this indicator is below zero (red). All exponential price appreciations in Bitcoin's history have occurred during phases of net liquidity expansion (green).

After spending most of the past few years in the red zone, net liquidity entered a growth phase in mid-2024 and is expected to grow again at a higher rate in the first quarter of 2025. This net growth in the money supply is the fuel for Bitcoin, which began just before the Bitcoin treasury company model took off.

When global money supply net liquidity is positive, Bitcoin performs well. Recent growth also coincides with the rise of treasury companies. Source: Capriole Charts

2. Significant Policy and Regulatory Drivers

With Trump's inauguration, we transitioned from an anti-Bitcoin U.S. regime to a pro-Bitcoin one. Under the previous administration, the U.S. banking channels to crypto businesses and funds underwent "Operation Choke Point 2.0" in 2023 and 2024, which has now finally been shut down. However, over the past year, we have gradually witnessed a dramatic positive shift towards a pro-Bitcoin and digital asset regime, instilling confidence in institutional investments in Bitcoin and treasury companies:

January 2024: The U.S. SEC approves all 11 Bitcoin ETFs.

January 2025: Anti-crypto SEC Chairman Gensler resigns.

March 2025: Trump establishes a U.S. strategic Bitcoin reserve.

March 2025: The White House officially terminates "Operation Choke Point 2.0," reopening U.S. crypto banking channels.

May 2025: The SEC withdraws its anti-crypto lawsuits against companies like Ripple and Binance.

July 2025: The "GENIUS Act" provides a robust regulatory framework for stablecoins.

August 2025: 401K pension plans are approved to purchase Bitcoin, opening a $10 trillion market to digital assets.

All of these measures provide the regulatory rigor sought by banks, institutional allocators, and investors. These collective actions reduce industry risk and enable capital to flow into Bitcoin and digital assets at lightning speed in 2025, propelling the rise of Bitcoin treasury companies.

The Fuel is Ready, the Spark is Lit

In the past six months, rising global liquidity, policy green lights, and validated corporate strategies have occurred in sync. This has created a reflexive flywheel for digital asset treasury companies to take off. For these reasons, investors have driven up the stock prices of treasury companies. Capital markets have opened their doors. Higher prices create higher valuation multiples for treasury companies; this, in turn, allows for more equity issuance and purchases of Bitcoin (and other digital assets).

A fierce flywheel accelerating the adoption of digital asset treasury companies has emerged.

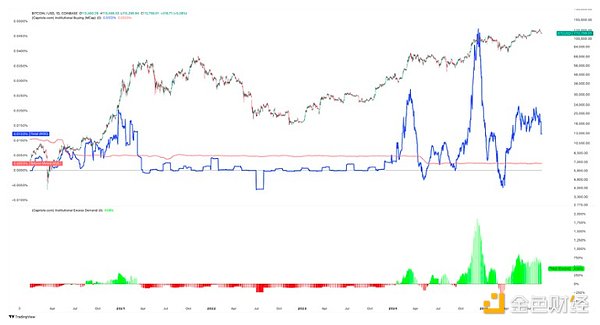

The Most Important Chart

If we had to choose just one data point to track the impact of Bitcoin treasury companies, it would be the chart below showing the percentage of institutional purchases relative to Bitcoin's market value. Today, the amount of Bitcoin purchased by institutions is over 400% of the daily mining new supply. When demand far exceeds supply, Bitcoin has historically surged in the following months. In fact, every time this has happened in Bitcoin's history (a total of 5 times), the price has averaged a 135% increase.

This metric is not only important for predicting Bitcoin's future price but also for monitoring potential risks in market sentiment towards digital asset treasury companies themselves.

Institutional Bitcoin Purchases vs. Mining Supply Comparison Chart

Today, institutions driven primarily by treasury companies are purchasing 400% of the daily Bitcoin mining supply. Source: Capriole Investments

House of Cards (Fragile System)

Digital asset treasury companies are not without risks. There are two significant risks worth discussing to understand where this market may head next.

1. De-leveraging

The most obvious risk for treasury companies is over-leverage caused by excessive use of debt. Bitcoin is known for its historical volatility and 80% crashes every 3-4 years. While we expect Bitcoin's volatility to continue to decrease in the coming years (as it has so far each year), treasury companies must build debt and collateral requirements to prepare for the worst-case scenario.

Even if only a relatively small portion of treasury companies become over-leveraged, it could put the entire asset class at risk. For example, imagine that only 5-10% of treasury companies over-leverage themselves to compete by offering investors more aggressive Bitcoin yields. We call this group "The Gamblers." If these "gamblers" are forced to liquidate their loans when Bitcoin drops by 40-50%, they will be compelled to sell Bitcoin to repay their debts, further driving down Bitcoin prices, which would then trigger further sell-offs of their stocks and additional Bitcoin sales. This is the reverse effect of the treasury company flywheel. The result is often referred to in the crypto space as a "liquidation cascade" (which we have seen many times in the futures markets over the years). In this scenario, while most treasury companies may technically be safe and not liquidated, the flight of investors could stifle the entire treasury company ecosystem for years. For this reason, Capriole has integrated debt data and multiples into our charts and is actively monitoring this risk.

2. The Silent Killer: mNAV Compression

The second key risk lies in the dynamic relationship between premium and net asset value (premium-to-NAV). This risk is more insidious but equally important.

The most popular treasury company metric is "mNAV" (market cap to Bitcoin holding value ratio), which represents the ratio of a company's market cap to the value of its Bitcoin holdings. When a treasury company's trading price is above its Bitcoin holding value (mNAV > 1), issuing new shares is Bitcoin accretive, allowing the company to issue stock and increase the per-share Bitcoin content for investors. A win-win situation. But if the mNAV premium evaporates and the stock price falls below NAV (mNAV < 1), problems arise. Now, issuing stock becomes dilutive and destroys value, hindering financing. Companies in this position may face pressure (from internal governance, activist shareholders, or market forces) to liquidate digital asset holdings to repurchase discounted stock, hoping to create positive "Bitcoin yields" and drive mNAV back up. However, this strategy would shrink the treasury's size and undermine investor confidence. The sell-off by treasury companies would also suppress the crypto market, creating the aforementioned negative reverse flywheel effect. Essentially, maintaining a valuation above NAV is crucial; once the narrative breaks and mNAV collapses, these companies lose their primary mechanism for expansion—leading to a simultaneous contraction of the entire digital asset market.

There are many reasons for the decline in mNAV. The cause may simply be the exhaustion of capital markets; too many Bitcoin treasury company stocks are available to meet too little institutional demand. As NYDIG points out: "These premiums must persist without fundamental reasons. This 'trade' reminds us of the 'GBTC arbitrage,' which ultimately exploded and dragged down nearly the entire crypto industry. Our intuition is that these premiums relative to NAV seem to be positively correlated with price. If crypto assets experience a price correction, we suspect these premiums will also collapse."

Percentage of Treasury Companies Trading Below NAV (mNAV < 1)

Recently, the percentage of Bitcoin treasury companies trading below 1 mNAV reached a historic high of 27%. This is a concerning trend worth monitoring. Source: Capriole Charts

While the risk of individual treasury companies collapsing may be low, problems arise when you multiply that risk across hundreds of treasury companies, combined with the competitive spirit required for each company to stand out. Over time, these companies have the incentive to move outside the risk curve, selling investors dazzling Bitcoin yield multiples and stock returns. Here, we recall Buffett's quote about imitators and greed mentioned above.

The Collapse of Speculative Investment Trusts

The rise of Bitcoin treasury companies echoes another chapter in history, namely the rise of speculative investment trusts in the 1920s. These trusts allowed people to pool funds into an entity, which the management would then invest at their discretion in a leveraged common stock portfolio. "By 1929, new trusts were being launched daily, valued at 2-3 times their underlying assets. The trusts of the 1920s and Bitcoin treasury companies both had huge mNAV premiums and embraced leverage." (BeWater).

We all know what happened in 1929. Driven by rampant stock market speculation and high leverage, the stock market crashed by 90%, exacerbated by investment trusts.

The Investment Company Act of 1940 (ICA) was primarily a response to the abuses of investment trusts in the 1920s, imposing strict regulations on entities "engaged in the investment, reinvestment, or trading of securities," requiring them to register with the SEC and meet certain regulatory and leverage constraints.

Today's digital asset treasury companies are exempt from the ICA because digital assets are not considered "securities." Therefore, while the activities of treasury companies are broadly similar to those of speculative trusts, they are unregulated.

"History does not repeat itself, but it often rhymes." — Mark Twain

The Endgame

At some point, the current Bitcoin treasury company hype cycle will reach saturation, potentially triggering severe liquidations. It is difficult to say when this will happen, but some of the indicators and data highlighted above will be key to managing that risk accordingly. If you want to read more, there is an article that highlights 8 important indicators for monitoring the liquidation risk of treasury companies.

While the treasury company flywheel is the biggest driver of this round of Bitcoin price increases, it also constitutes the largest downside risk. The fate of the crypto industry largely rests in the hands of over 150 publicly listed treasury companies.

But will this be the end? Or will treasury companies thrive in the long term?

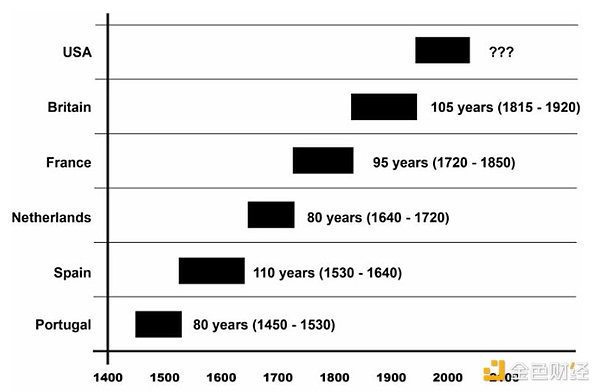

The answer to this question largely depends on whether you believe Bitcoin will succeed in achieving its ultimate mission of becoming the "peer-to-peer electronic cash system" as described by Satoshi Nakamoto. Today, Bitcoin is a $2 trillion asset, approaching gold's $22 trillion market cap. Beyond that, the global fiat currency value is $113 trillion and is growing at a rate of 9% annually due to central bank money printing. At its core, Bitcoin is a better form of gold. Instant, decentralized, interchangeable, programmable, and with an inflation rate lower than gold (annualized at 0.4% and continuously decreasing). This makes Bitcoin the ultimate store of value and inflation hedge. Gold was once the world's currency, and every 100 years, the world's reserve currency changes. So why can't Bitcoin go further?

With the abandonment of the gold standard in 1971, the next decade is a golden time for the rise of the next reserve asset.

Historical Reserve Currency Chart, Highlighting the Duration of the Dollar

The average length of reserve currency status is 94 years. The dollar is "aging." Source: Dalio (Bridgewater Associates)

In a digital, AI-driven world, will Bitcoin become a contender for the next world reserve asset? This is a philosophical question we all need to answer. I know where my bets are placed.

The road will be bumpy, but if Bitcoin succeeds, every company in the world will one day become a Bitcoin treasury company, whether they call themselves that or not.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。