Original author: 1912212.eth, Foresight News

Rock singer Cui Jian once sang in "The Pretender": "I want people to see me, but not know who I am." In the unpredictable crypto market, there are many similar "roles" that attract countless curious eyes.

In 2017, a young man left Wall Street, using his savings to build mines, read white papers, and stay up late to adjust algorithms. He brought in two colleagues from the globally renowned market maker and high-frequency trading firm Optiver: one skilled in trading architecture and the other proficient in risk control. The brutal bear market of 2018 tested many exchanges, projects, and media, and during the toughest times, without external financing, they could only rely on personal belief and algorithmic models to hold on. Until the global financial market experienced severe fluctuations due to the pandemic, their arbitrage algorithm earned them $120,000 overnight. A few months later, he began to achieve seamless arbitrage across multiple trading platforms.

A year later, the quietly operating team behind him managed funds amounting to hundreds of millions of dollars, completing countless trades under the algorithms he designed. He became the kind of "you can't see him, nor know who he is" role, yet you can always feel his presence from the buying and selling prices.

He is Evgeny Gaevoy, the founder of Wintermute, now one of the largest algorithm-driven crypto market makers in the world. He lives in London and enjoys traveling to the United States. He likes to use images and memes, and he speaks frankly, even retorting to market manipulation allegations with "If you treat me as a hypothetical enemy, don't blame me for spitting back at you."

So what exactly is the role of a crypto market maker?

Typically, if a project team issues a token, they can publish it on a DEX. The general steps involve creating a trading pair on the DEX, such as X/ETH or X/USDT, and then injecting two assets to form an initial liquidity pool, such as 1 million X tokens and 100 ETH. However, when a project team wants to list on exchanges like Coinbase or Binance, they cannot simply issue the token and expect people to trade it, as they often face the dilemma of insufficient trading volume. These exchanges need to ensure trading liquidity. This means there must always be someone willing to buy and someone willing to sell. Typically, this role is undertaken by market makers.

Compared to exchanges and crypto VCs that are often discussed in public, market makers conceal their mysterious veil. They hold an important position in the crypto industry but are occasionally the driving force behind token price declines, making them a subject of controversy.

The Old Pattern Disintegrates

Since the last cycle, a group of professional market makers has entered the crypto market.

At that time, the market was dominated by established institutions like Alameda Research, Jump Crypto, and Wintermute. These players, leveraging high-frequency algorithmic trading and substantial capital, dominated the liquidity supply of CEXs. Alameda, as the sister company of FTX, provided depth for mainstream assets like Bitcoin and Ethereum during the peak of the 2021 bull market, with trading volume at one point exceeding 20% of the market total.

Alameda Research, as a top market maker in the crypto field, began to collapse due to the liquidity crisis of its sister company FTX. In November 2022, CoinDesk exposed Alameda's balance sheet, prompting CZ to announce the sale of all FTT, leading to FTX's liquidity depletion and a user bank run. Investigations revealed that FTX misappropriated customer funds amounting to $10 billion to lend to Alameda for high-risk trading and to cover losses, creating a fatal cycle. FTX, Alameda, and over 130 affiliated entities filed for bankruptcy, and SBF resigned as CEO.

Looking back at its glory, Alameda was founded by SBF in 2017, initially focusing on crypto arbitrage and quantitative trading, rapidly rising due to its algorithmic advantages. After launching FTX in 2019, Alameda became its main liquidity provider, helping FTX's valuation soar to $32 billion. Alameda managed hundreds of billions in assets, profiting handsomely through leveraged trading and market making during the bull market, with SBF becoming a crypto billionaire, promoting industry philanthropy and regulatory advocacy.

Caroline Ellison

The ultimate collapse stemmed from internal governance issues, with Alameda partner Ellison admitting to misappropriating customer funds during an employee meeting, shocking the industry. Her relationship with SBF added drama: in 2023, she became a key witness for the prosecution, testifying that SBF orchestrated an $8 billion fraud, while she pleaded guilty to seven counts of fraud and was sentenced to two years in prison in 2024. In court, she tearfully apologized: "I feel heartbroken for the people I have hurt every day."

Alameda's high leverage exposed it to market volatility, with FTX customer funds being improperly lent to fill gaps. In 2023, SBF was sentenced to 25 years in prison, and Alameda's assets were liquidated, marking its complete disintegration.

The exit or contraction of established market makers was a direct cause of the vacuum period.

According to Kaiko data, a week after FTX's collapse, global crypto liquidity halved, with Bitcoin's 2% depth dropping from hundreds of millions to less than $100 million.

In the early liquidity battleground of the crypto market, Jump Crypto and Wintermute were once the two hottest forces.

Jump originated from the traditional high-frequency trading giant Jump Trading, leveraging its deep algorithmic foundation and capital strength to make a significant entry into the crypto market in 2021, being present in everything from the Solana ecosystem to the Terra stablecoin system. However, following the collapse of Terra, in 2023, Jump Crypto scaled back its operations due to an investigation by the U.S. Securities and Exchange Commission (SEC), exiting parts of the U.S. market and laying off over 10% of its staff.

Wintermute rapidly rose with flexible algorithmic market making and OTC business, becoming one of the most influential liquidity providers in both CeFi and DeFi. A hacker incident in 2022 caused it to lose nearly $160 million, exposing the risks behind its rapid expansion; thereafter, Wintermute gradually shifted towards refined operations, no longer blindly expanding.

The trajectories of both companies encapsulate the entire process of crypto market makers from wild growth to cautious contraction over the past five years: from high-frequency arbitrage to ecosystem support, from aggressive risk-taking to prudent survival. Market makers once supported the market's prosperity but have now learned to seek a balance between risk and liquidity.

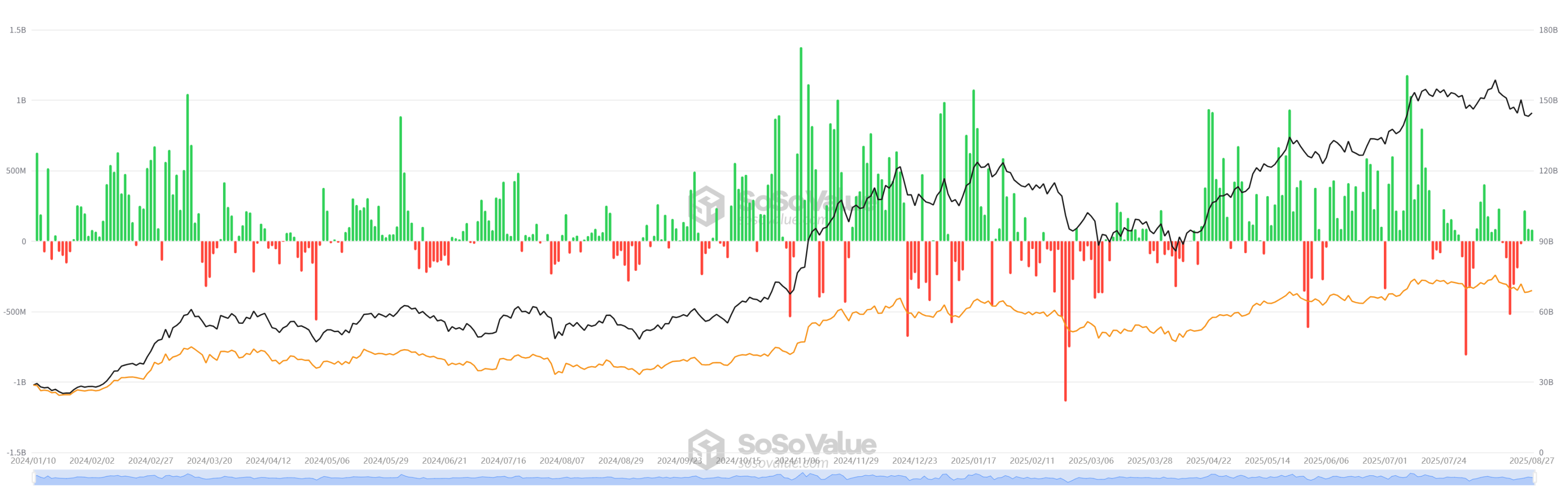

However, at a time when the contraction of the front lines has become cautious, both macro and micro factors have once again facilitated the entry of new players. The Federal Reserve's interest rate cuts in 2023-2024 stimulated capital inflow, and after Bitcoin's halving in 2024, the market cycle was initiated. A new wave of token issuance emerged: inscriptions, re-staking, meme coins, AI agents, stablecoin booms, RWA, and on-chain U.S. stocks, among other hot topics, took turns to play out. Additionally, the U.S. spot ETF also attracted a large amount of capital, with data showing very bright performance.

According to SoSoValue data, as of August 28, the total net inflow for Bitcoin spot ETFs reached $54.19 billion, while Ethereum spot ETFs saw a total net inflow of $13.64 billion. The easing of the regulatory environment is also one of the important reasons. Since Trump took office in January 2025, he has emphasized support for the responsible growth of digital assets, blockchain technology, and related technologies, while revoking the relevant policies of the Biden administration. This order also established a digital asset working group within the National Economic Council, aimed at proposing a federal regulatory framework, including market structure, oversight, consumer protection, and risk management.

Moreover, the industry's technical barriers are continuously lowering, and the demands of project teams are changing, prompting a reshuffle in the industry.

The Rise of New Nobles

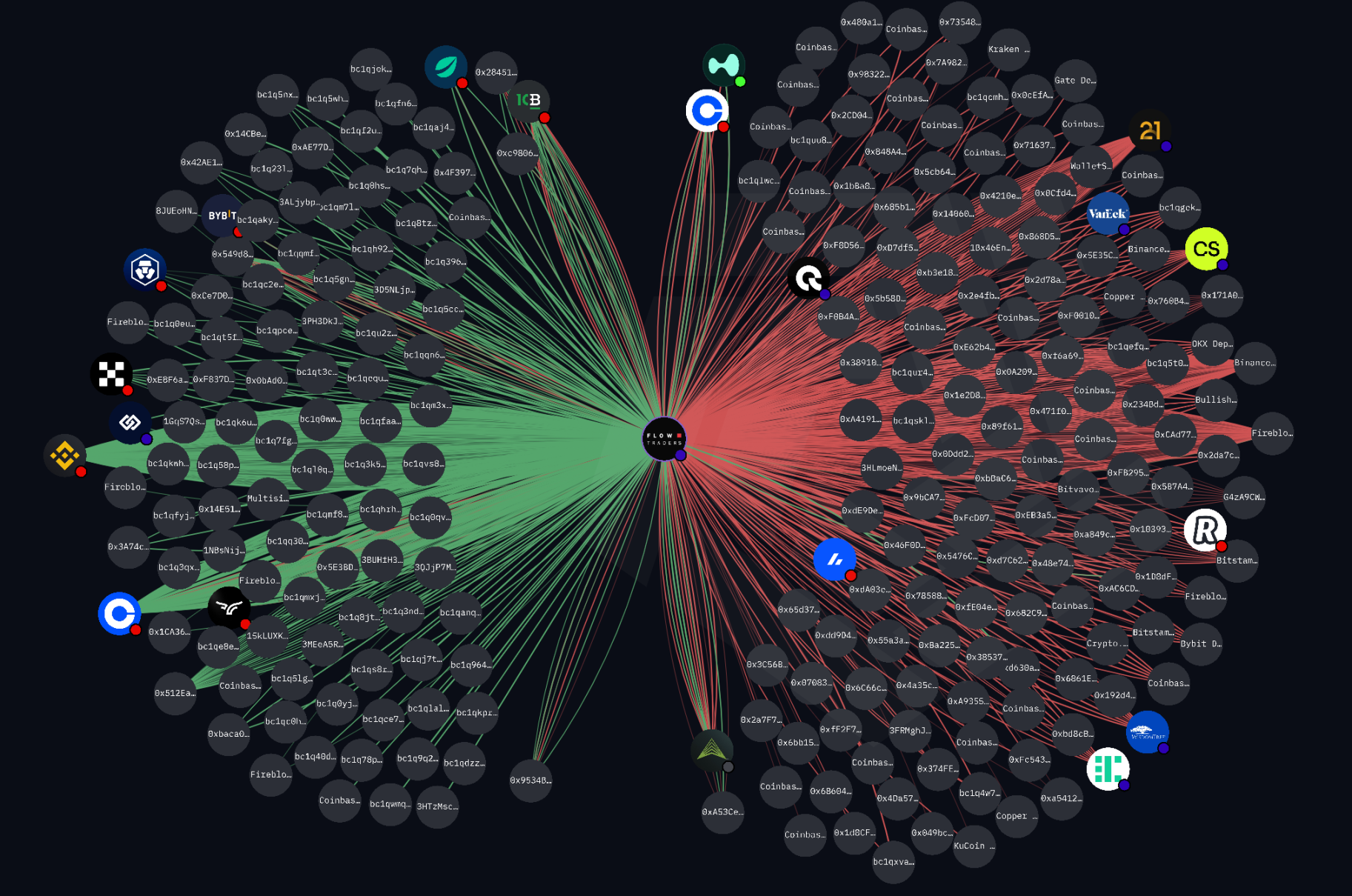

The significance of the vacuum period lies in the vast space it leaves for new players. Representative players include Flow Traders, GSR's new department, and DWF Labs. The core members have diverse backgrounds, and their business scope covers CEX/DEX market making, OTC, and structured products.

Flow Traders

Flow Traders, a global liquidity provider originating from the Netherlands, was initially known for exchange-traded products (ETPs) but decisively shifted to the crypto field in 2023, as if a seasoned sailor had caught the digital wind. The team has a strong background, composed of a group of quantitative trading experts and financial engineers, emphasizing a "strong team-driven culture." The Amsterdam office resembles a precision laboratory, gathering elites from Wall Street and Silicon Valley.

Thomas Spitz

In July 2025, Flow Traders appointed Thomas Spitz as the new CEO. This former executive at Crédit Agricole CIB has over 20 years of illustrious career experience, having held multiple senior roles and possessing deep international team management and cross-cultural leadership experience. He led the MiCAR compliant stablecoin AllUnity and collaborated with DWS and Galaxy Digital to reshape the tokenized asset landscape.

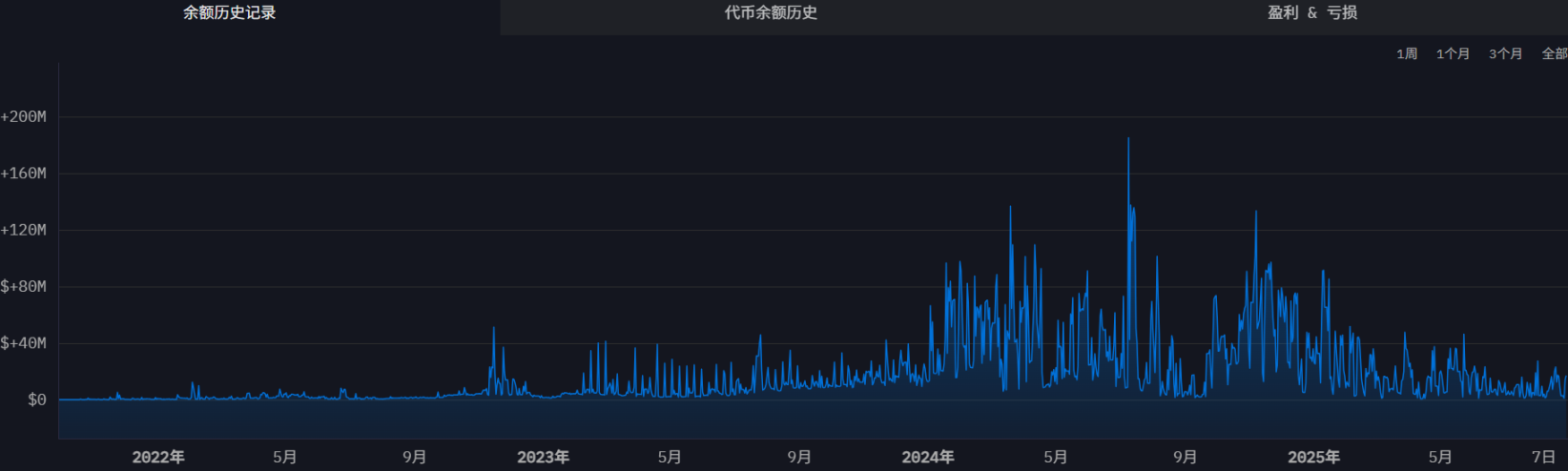

In the second quarter of 2025, its net trading income reached €143.4 million, an 80% year-on-year increase. In terms of market making characteristics, Flow Traders excels in cross-chain and institutional-level support, providing continuous liquidity. Currently, third-party data monitoring shows that it includes tokens such as AVAX, LINK, DYDX, GRT, STRK, PROVE, WCT, PARTI, ACX, and EIGEN. Notably, in mid-2024, Flow Traders also helped the German government smoothly handle confiscated BTC, without triggering significant downturn risks in the secondary market.

Flow Traders expands its profits using its own funds and algorithms, while GSR obtains some funding through VCs like Pantera Capital.

Monitoring data shows that its market-making funds currently amount to $16.94 million, with its fund balance having fallen back to historical low ranges.

GSR Markets

GSR Markets is an algorithmic digital trading company based in Hong Kong. It utilizes its own software to provide order execution solutions for several categories of digital assets, thereby offering liquidity. The team has a diverse background, with many members being former hedge fund traders and blockchain engineers. With offices in New York and London, they gather global talent to provide institutional-level market making, OTC trading, and risk management. GSR's market making characteristics lie in precise risk hedging and global connectivity, connecting dozens of exchanges to provide bidirectional liquidity for buyers and sellers, excelling in high-frequency algorithms to respond to volatility.

In 2023, GSR reduced its trading in the U.S. to avoid regulatory storms, leading to the departure of its CFO and other executives. In 2024, GSR transitioned from pure trading to becoming an ecosystem partner. At the 2025 Consensus Summit, its partner Josh Riezman stated, "The integration of DeFi and CeFi is the future, and we are preparing for the next phase."

Riezman mined Ethereum using his own server, accumulating his first pot of gold. His past experience is impressive, having worked for several years at Deutsche Bank, Société Générale, Circle, and both traditional and crypto sectors. Under his leadership, GSR became the first crypto liquidity provider in the industry to obtain licenses from both the UK's FCA (Financial Conduct Authority) and Singapore's MAS (Monetary Authority of Singapore).

Josh Riezman

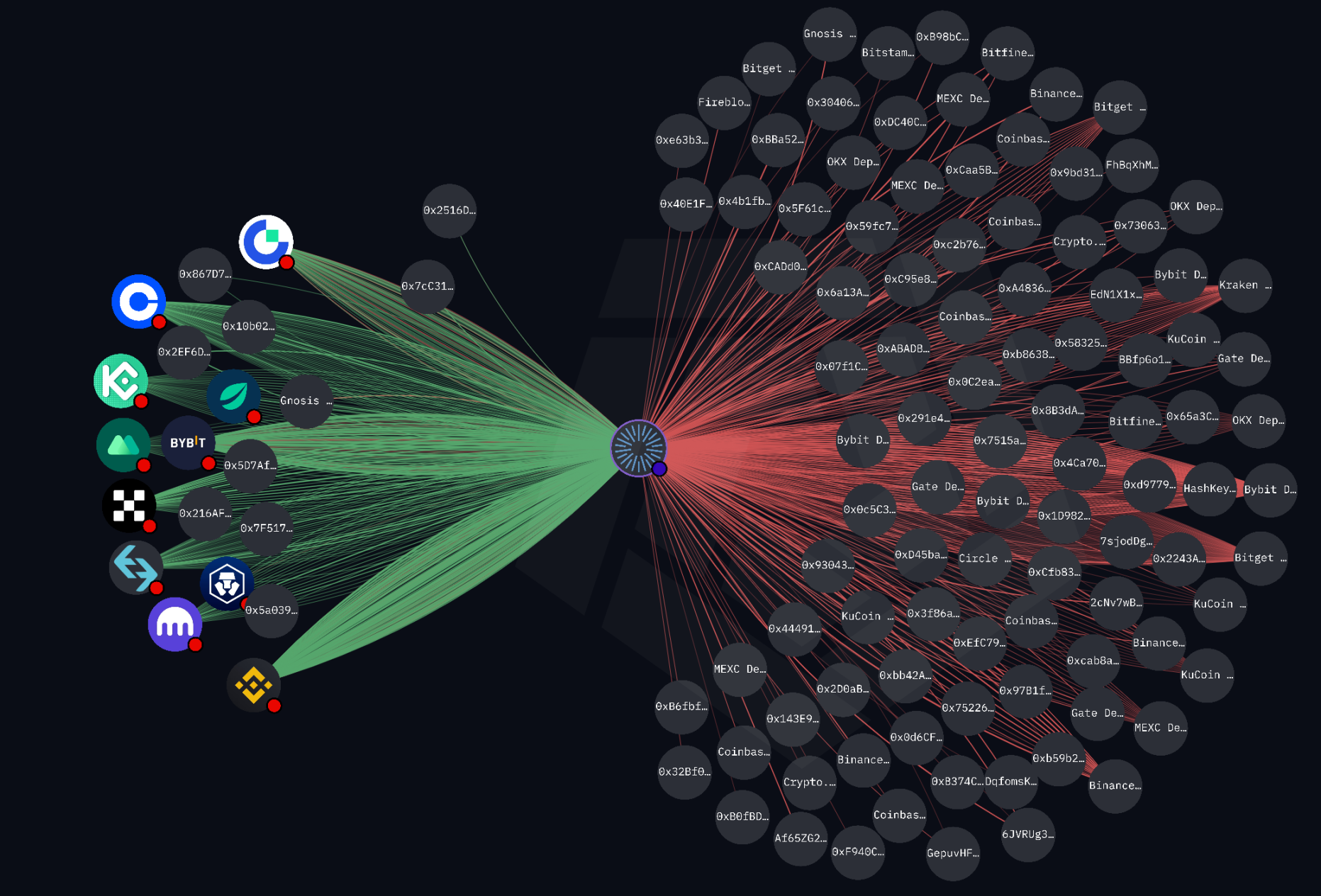

According to publicly available information, the altcoins that GSR markets include: WCT, RNDR, FET, UNI, SXT, SPK, RSC, GALA, HFT, PRIME, ARKM, BIGTIME, USUAL, MOVE, BAN, TAI, PUFFER, ZRO, IINCH, ENA, WLD, etc. If you observe carefully, it is not difficult to find that among some altcoins listed on Binance, the tokens that GSR markets often experience a period of price increase after listing, rather than a drop immediately.

According to Arkham data, the current market-making fund volume of its public address is $143.76 million. Its main market-making exchange is Binance. The fund balance remains at a moderate level.

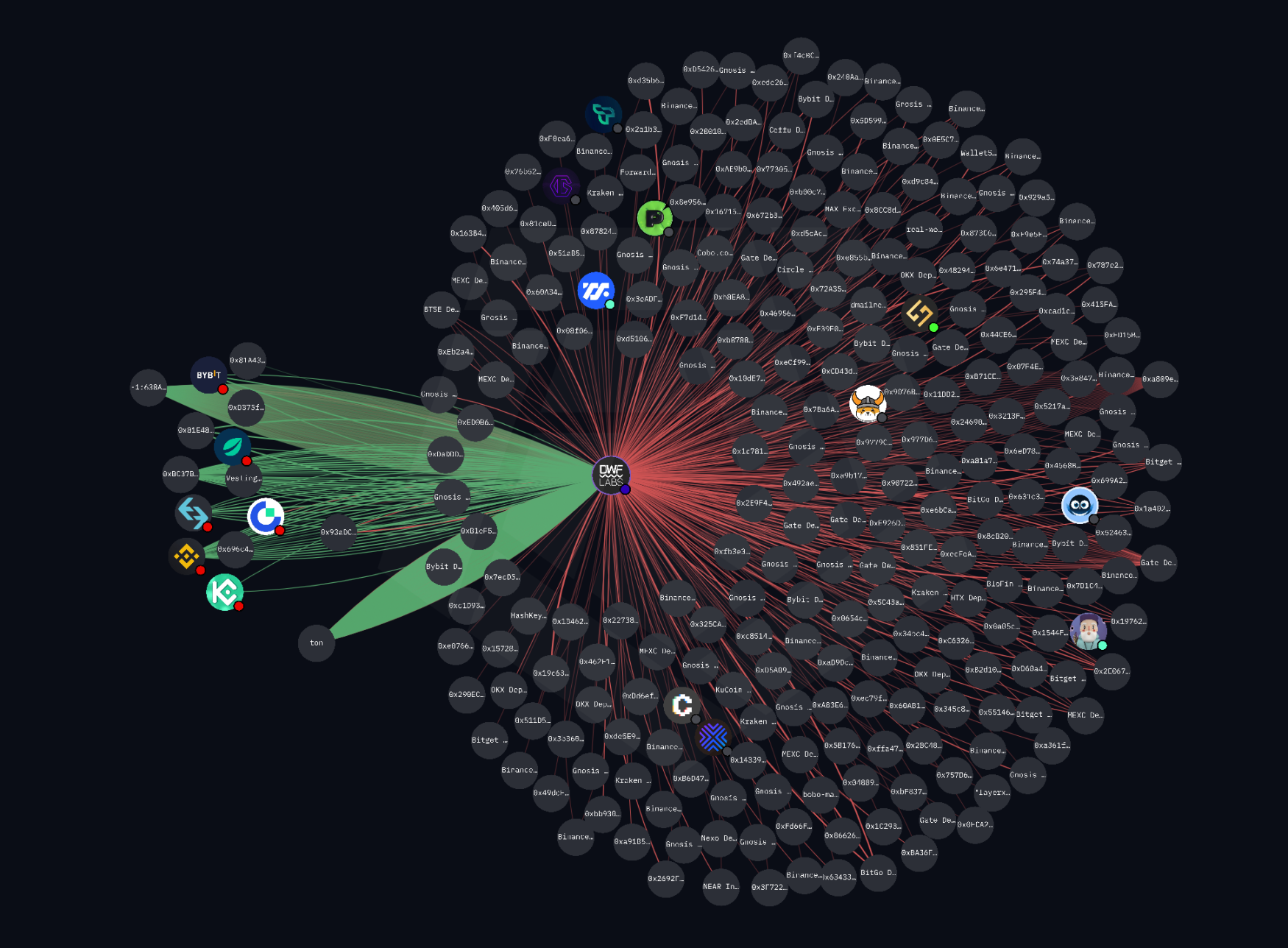

DWF Labs

DWF Labs was established in 2022, with managing partner Andrei Grachev coming from a traditional trading background, having previously served as the head of Huobi Russia. He entered the logistics industry at 18, then began trading in traditional markets in 2014, later transitioning to e-commerce, making a profit when ETH rose from $7 to $350, thus starting his crypto journey.

He has five tattoos of Chinese characters, and under his leadership, DWF is controversial in the market but takes pride in it. Moreover, DWF plays multiple roles, encompassing VC, OTC, incubators, ecosystems, fundraising, event branding, TVL providers, DeFi takers, consultants, token listing agents, HR, PR/marketing companies, KOLs, RFQ request platforms, and more.

From 2023 to 2025, it invested in over 400 projects, totaling more than $200 million.

DWF primarily targets East Asian projects and various new and old sentiment-themed assets for market making. According to publicly available information, the altcoins that DWF markets include SOPH, MANTA, YGG, IOST, JST, MOVE, CAT, MONKEY, ID, XAI, LADYS, etc. Interestingly, as of now, DWF Labs' official market maker address has less than $9 million remaining.

Emerging players often receive support from Web 3 venture capital or expand through trading profits. DWF Labs' own capital snowballs, making it the most active investment institution from 2023 to 2024. By 2025, its "venture capital + market making + incubation" model has covered multiple narrative fields. These funding sources allow newcomers to quickly establish themselves during the vacuum period; for example, DWF Labs invested in AI and RWA projects through its own capital in 2024, showing significant snowball effects.

More flexible token incentive protocol cooperation models are common, with some directly binding investment + market making. For instance, in 2025, DWF Labs provided stablecoin support for Falcon Finance, offering annual returns of 12-19%, but this sparked bad debt controversies. GSR aggregates liquidity through the 0x API, helping projects achieve efficient trading on the Ethereum mainnet. Jupiter Aggregator routes the best paths on Solana, with newcomers like Flow Traders utilizing it to lower technical barriers. These innovations allow newcomers to stand out in a fragmented market, contrasting with the centralized models of established players.

Controversies

The rise of market makers is always accompanied by controversy. The most rapidly rising and controversial player in this cycle is undoubtedly DWF Labs.

During the Token 2049 forum held in September 2023, its co-founder Andrei Grachev tweeted after the "Web 3 Connect" meeting, expressing gratitude for the invitation. Unexpectedly, market maker GSR angrily retorted on Twitter, stating that DWF Labs was not qualified to sit with the forum's speakers: market makers GSR, Wintermute, and OKX, calling it an insult to them.

GSR stated that it is very sad that by the end of 2023, bad actors like DWF Labs can still receive so much attention. Another market maker, Wintermute's CEO Evgeny Gaevoy, liked the tweet. Interestingly, in the event photos shared by market maker GSR, part of Andrei Grachev was deliberately cropped out. Evgeny posted a tweet exposing Andrei Grachev, delving into his extensive past experiences, which were believed to be linked to the notorious OneCoin, the largest fraud project in crypto history. However, Evgeny mainly commented on the poor investment performance summarized in the article, calling DWF Labs a "wrong market maker."

Andrei, in an interview with Foresight News, stated that he does not care about these criticisms and complaints, saying, "As long as we operate within the correct and legal framework, if a certain method proves effective, we will adopt it without worrying about what others say, and we are not afraid of criticism or complaints from competitors."

This is just one of the minor episodes in the conflicts between market makers. The collusion between market makers and project teams has left investors in shock.

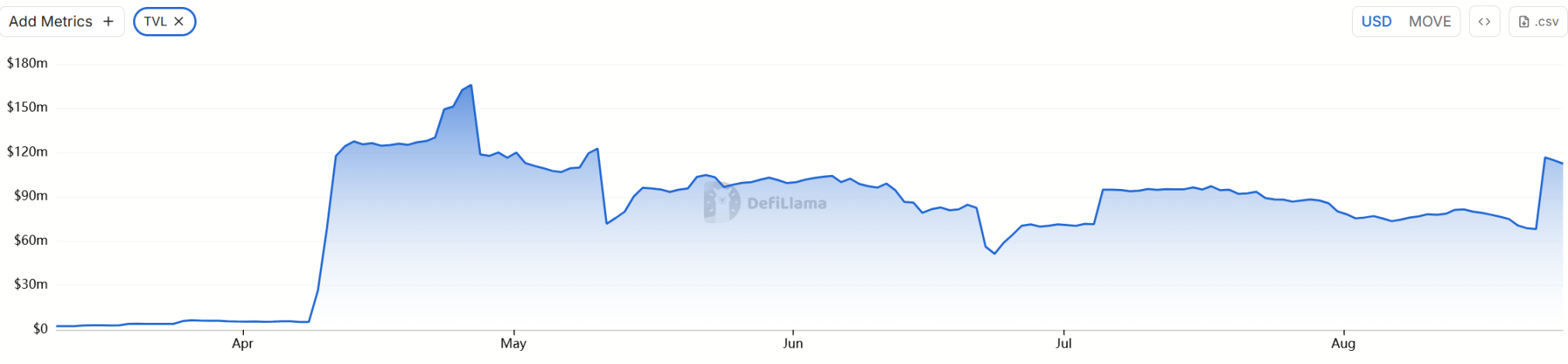

At the end of April 2025, the Layer 2 project Movement hired Web 3 Port as its official market maker and loaned them 66 million MOVE tokens to provide liquidity. However, in practice, these tokens were reported to be transferred to an entity named Rentech, which was confirmed to be an agent or shadow company of Web 3 Port. This transfer may involve internal fraud or informed execution: the contract showed that once the MOVE market cap reached $5 billion, Rentech could sell the tokens for profit sharing. This incentivized price manipulation.

After the MOVE token was officially launched, Rentech quickly manipulated the price to push it to the $5 billion market cap threshold, then sold $38 million worth of tokens the next day (about 5% of the total supply). This sell-off directly caused the MOVE price to plummet: from an initial high of $1.45, it crashed by 86%, with a single-day drop of 20-30%, evaporating billions in market cap. Once this behavior was exposed, it triggered a chain reaction. Internal sources indicated that Movement co-founder Rushi Manche might be involved in the signing of the agreement, and the project team claimed to have been "deceived," but contract details showed the involvement of hidden intermediaries and consultants.

Ultimately, Movement Labs terminated Manche's co-founder position and restructured as Move Industries. Binance also froze the market maker's related earnings and prohibited them from market making on Binance.

However, the enormous negative impact caused by this incident is irreparable. The MOVE token price has dropped more than tenfold from its peak, resulting in significant losses for most investors.

According to defiLlama data, its TVL has also plummeted from a peak of $166 million to $50 million, a drop of over 300%.

This typical negative event has unveiled the collusion between project teams and market makers.

It has also prompted the entire industry to reflect on the underlying issues, particularly regarding contracts and incentive mechanisms. Market maker agreements should avoid manipulative incentives such as market cap thresholds and need to clarify buyback obligations and transparent audits. The Movement case shows that hidden intermediaries can lead to fraud. In terms of transparency, project teams should disclose market maker details, token transfer records, and commitment executions (such as buybacks). Delayed airdrops and unfulfilled promises can amplify trust crises, leading to community attrition.

Emerging projects also need to strengthen internal supervision to avoid founders becoming involved in suspicious transactions. The integrity of the leadership is key to the project's survival; if the goal is merely to issue tokens to let retail investors exit liquidity, the final outcome will be mutually destructive.

Conclusion

When the spotlight sweeps across the trading arena of the crypto world, those who truly control the flow often hide within the torrent of data. Market makers, the "dark pool operators" of the digital finance world, prefer to let code flow silently on the chain rather than display their names in public. Among the 63 active coordinates captured by RootData, the trading volume of just the top players is enough to stir the market's winds, while more players like Web 3 Port, Kronos Research, and B2C2 are weaving a liquidity web worth trillions with algorithms.

Their offices do not have triumphal arches, only an unceasing flow of orders; their names rarely make headlines, yet they can instantly freeze or boil the order books of certain tokens. When you trace the footsteps of a mysterious large order on the chain, you may be stepping on a "liquidity trap" carefully designed by a secret market maker—this is merely the surface ripple of their vast strategic matrix.

Now, 63 known coordinates have lit up, but how many unmarked eyes remain in the dark forest?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。