Author: FinTax Carlton

I. Introduction

As a significant international financial center, Singapore has long attracted global capital and innovation with its open market environment, sound legal system, and efficient regulatory framework. In recent years, with the rapid development of digital assets and blockchain technology, this city-state has gradually become an important hub for crypto assets in the Asia-Pacific region. It not only gathers a large number of startups and international trading platforms but also attracts institutional investors, technology developers, and policymakers to explore the future of digital finance. Driven by diversified market demand and proactive policy support, Singapore's crypto ecosystem is gradually maturing.

According to the Independent Reserve Cryptocurrency Index (IRCI) Singapore 2025 report, the awareness of cryptocurrency in Singapore has reached a historical high, with 94% of respondents aware of at least one crypto asset, and 29% having owned crypto assets, among which 68% of crypto investors hold Bitcoin, and 46% have ever held or are currently holding stablecoins, with the usage rate of stablecoins for actual payments and cross-border transfers reaching 53%. Additionally, 57% of crypto asset holders believe that the crypto industry will achieve mainstream status in the future, and 58% of the public calls for further clarification of government regulation… These data collectively depict a market with widespread awareness, diverse applications, and clear expectations for regulation.

In this context, understanding Singapore's cryptocurrency tax system and regulatory framework is not only a legal compliance necessity but also a key to insight into market development potential and risk patterns. This study will focus on the two main lines of the basic tax system and regulatory framework, presenting the interaction between institutions and markets in Singapore's crypto ecosystem, and providing investors with a clear picture of the current state of the crypto industry in Singapore, aiming to provide reliable basis for business decisions.

II. Regulatory Framework

Cryptocurrencies are often associated with terms like risk. Unlike most jurisdictions, where unique regulatory provisions exist for cryptocurrencies among different states, Singapore's cryptocurrency regulatory system is known for its clarity and balance. Although obtaining relevant qualifications and licenses in Singapore is not easy for many Web3 companies, this has significantly controlled the risks for local Web3 enterprises.

In Singapore, the tax and financial regulation of crypto assets are carried out by the Inland Revenue Authority of Singapore (IRAS) and the Monetary Authority of Singapore (MAS), respectively.

The tax administration of cryptocurrencies is primarily the responsibility of IRAS. As the national tax authority, IRAS formulates and implements policies related to income tax and Goods and Services Tax (GST) concerning crypto assets, covering the tax obligations of businesses and individuals in various activities such as holding, trading, paying, and issuing. IRAS has published several specialized e-Tax Guides, specifically addressing the income tax treatment of digital tokens and the GST treatment of digital payment tokens, clarifying the tax classification, taxable events, and tax principles for different types of tokens (payment, utility, security). Additionally, IRAS is leading the implementation of the Crypto Asset Reporting Framework (CARF) in the country, playing a core role in cross-border tax information exchange.

MAS primarily exercises financial regulatory authority over cryptocurrencies. It not only performs central bank functions but also serves as a comprehensive regulatory body for the financial industry and payment services, significantly influencing the licensing, compliance, and risk control of crypto asset-related businesses. For instance, MAS's licensing requirements for Digital Payment Token Service Providers (DPTSP) and its regulatory framework for stablecoins indirectly affect the tax treatment and compliance pathways for related businesses.

III. Basic Research on Singapore's Crypto Tax System

Singapore's tax system is known for its simplicity and concentrated tax base, with its most prominent feature being the absence of capital gains tax globally, along with the abolition of estate tax and gift tax. This means that in Singapore, the appreciation of asset value itself typically does not constitute an independent taxable event; whether tax is levied depends on the nature and frequency of the transaction. Coupled with relatively low income tax rates, Singapore's tax system maintains a high level of inclusivity for capital flows and innovative activities while ensuring stable fiscal revenue.

Within this institutional framework, Singapore's taxation scope for crypto assets is relatively concentrated, primarily focusing on income tax and Goods and Services Tax. The former emphasizes taxing income from regular or commercial nature crypto transactions, while the latter regulates the indirect tax treatment of digital payment tokens in goods and services transactions. Other taxes, such as withholding tax and employment income tax, are triggered only in specific transaction structures or payment scenarios.

(A) Income Tax

Singapore's income tax system adopts a territorial source principle, meaning that only income sourced from Singapore and income remitted to Singapore from overseas is taxed. Personal income tax operates on a progressive tax rate system, with resident rates ranging from 0% to 22% (up to 24% for the 2024 tax year), while non-residents are typically taxed at a fixed rate of 15% or the higher resident rate. The corporate income tax rate is a uniform 17%, with tax exemptions for startups and specific industry reductions.

On April 17, 2020, IRAS released the Income Tax Treatment of Digital Tokens, aimed at providing guidance on the income tax treatment of transactions involving digital tokens.

The guide categorizes digital tokens into three types: payment tokens, utility tokens, and security tokens.

The guide covers the following five types of transactions:

i. Receiving digital tokens as payment for goods and services;

ii. Receiving digital tokens as employment compensation;

iii. Using digital tokens as payment for goods and services;

iv. Buying and selling digital tokens; or

v. Issuing digital tokens through an Initial Coin Offering (ICO).

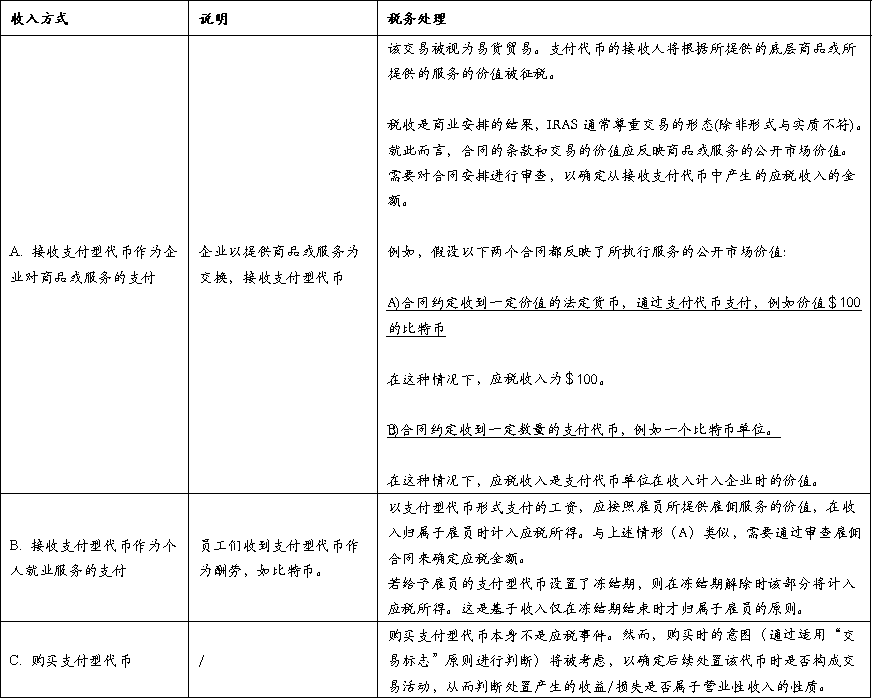

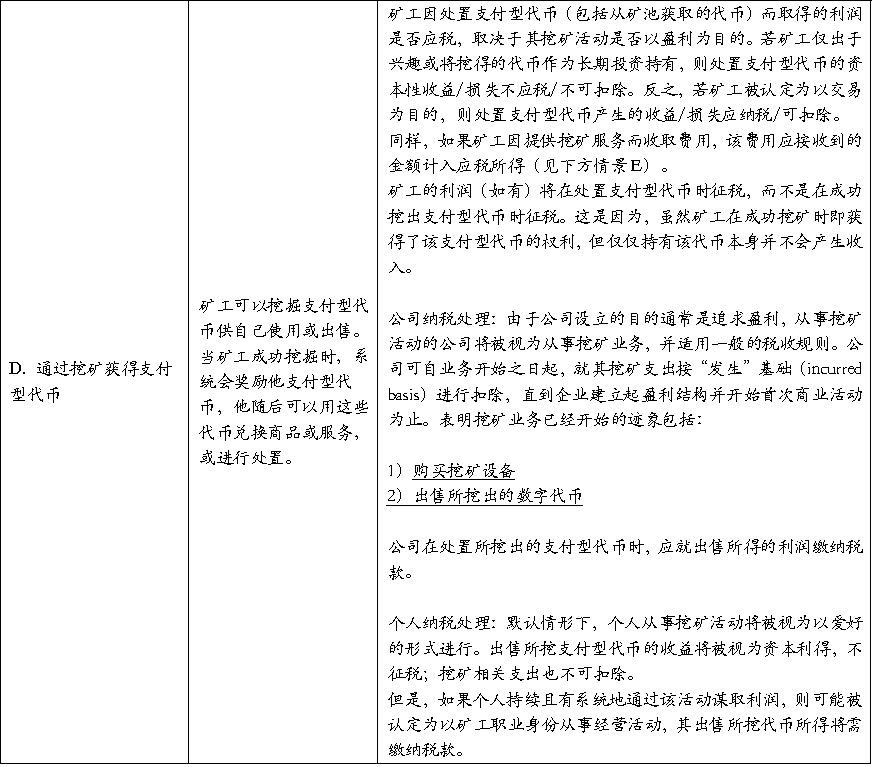

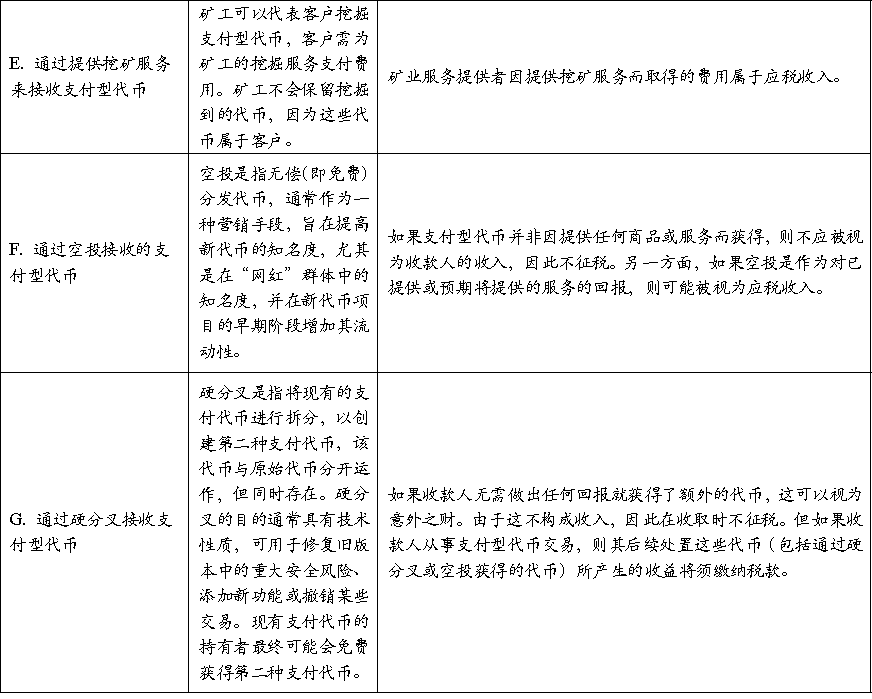

1. Tax Treatment of Payment Tokens

Payment tokens are synonymous with cryptocurrencies, having no other function besides payment.

Although payment tokens serve as a means of payment, they are not issued by the government and do not qualify as legal tender. For tax purposes, IRAS treats payment tokens as intangible property, typically representing a set of rights and obligations. Transactions involving goods or services using payment tokens are considered barter transactions, and the value of the goods or services transferred should be determined at the time of the transaction.

Table 1: Classification and Tax Treatment of Payment Tokens under Income Tax

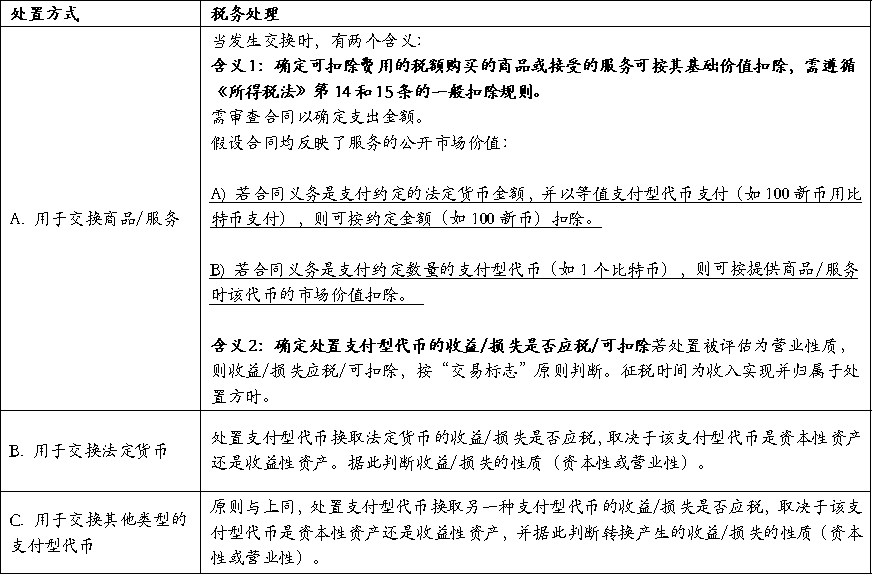

Table 2: Tax Treatment under Different Disposal Methods

2. Tax Treatment of Utility Tokens

Utility tokens grant token holders explicit or implied rights to use or benefit from specific goods or services, and the tokens can be used to exchange these goods or services.

They come in various forms, such as vouchers (granting holders the right to obtain services from the ICO company in the future) or keys (granting holders access to the ICO company's platform). When someone (hereinafter referred to as "user") acquires utility tokens to redeem goods or services in the future, the expenditure incurred by the user to purchase the utility tokens will be considered a prepayment. According to tax deduction rules, when the tokens are used to redeem goods or services, deductions can be claimed based on the amount of expenditure incurred.

The tax treatment of utility tokens issued during the ICO will be explained in the fourth section on ICO tax treatment.

3. Tax Treatment of Security Tokens

Security tokens grant token holders partial ownership or rights to an underlying asset and typically come with explicit or implied control or economic rights. The more common types of issued security tokens are recorded in the form of debt or equity. However, since security tokens are essentially tokenized forms of traditional securities, they may also take other forms of securities or investment assets/tools, such as units in a Collective Investment Scheme. The nature of security tokens depends on the rights and obligations associated with them, which will further determine the nature of the income received by the holders, which may be interest, dividends, or other distributions, and must be taxed accordingly.

When holders dispose of security tokens, the tax treatment of the gains/losses from the disposal depends on whether the security tokens are considered capital assets or income-generating assets for the holders. Accordingly, the gains/losses will be treated as either capital or business income.

Security tokens are subject to relatively lenient policies similar to other securities in Singapore, and no tax will be levied on security tokens that are capital assets. Depending on the issuer of the security tokens, taxes may be levied on income such as dividends that belong to the income-generating asset category.

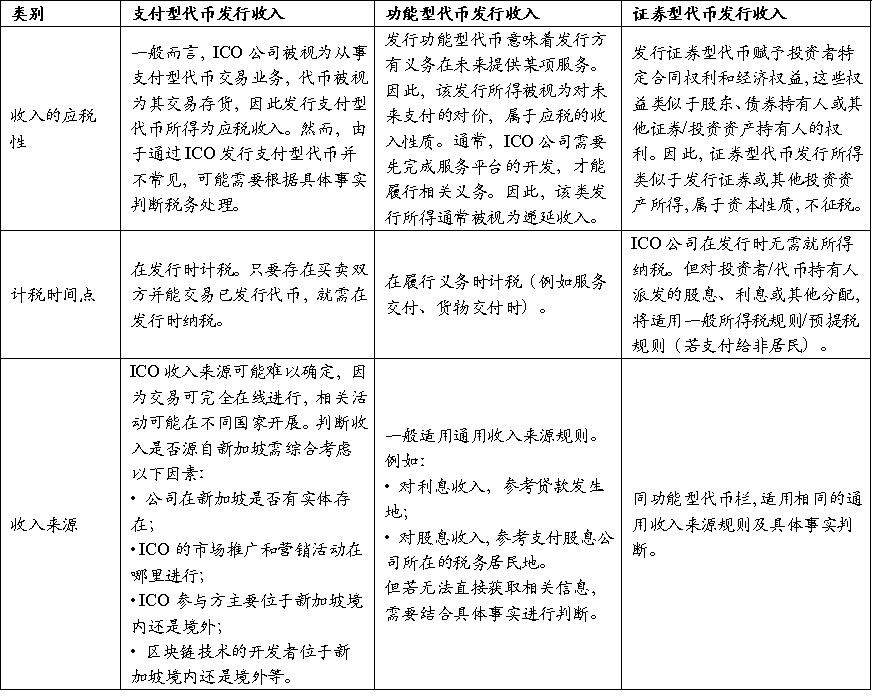

4. Tax Treatment of ICOs

An ICO, or Initial Coin Offering, involves the issuance of a new token, which is typically issued in exchange for other payment tokens or, in some cases, in fiat currency. ICOs are often used by token issuers to raise funds or provide means to access existing or future specific goods or services.

The taxability of the funds raised through an ICO in the hands of the token issuer depends on the rights and functions attached to the tokens issued to investors:

The taxability of funds from issuing payment tokens depends on the specific facts and circumstances;

Funds from issuing utility tokens are generally considered deferred income;

Funds from issuing security tokens are similar to those from issuing securities or other investment assets/tools, and their nature is capital income, thus not taxable.

For payments of interest, dividends, or other distributions related to security tokens, the deductibility of such payments by the issuer should be executed according to Sections 14 and 15 of the Income Tax Act.

See Table 3 for details.

Additionally, there may be the following special circumstances:

ICO Failure: If a company issues utility tokens through an ICO and uses the raised funds to develop a platform or service but ultimately fails to deliver, the tax treatment will depend on the destination of the funds: if the raised funds are returned to investors, the company does not need to pay tax on the refunded amount; if the funds are not returned, it will be necessary to determine whether the ICO is a capital transaction or an income transaction, with tax authorities considering factors such as the company's main business, the reasons for issuing tokens, and contractual obligations.

Pre-operational Expenses: Reasonable business expenses incurred by a company during an ICO before formal operations can be declared according to current pre-operational expense deduction rules. Under Section 14U of the Income Tax Act, eligible expenses can be deducted in the baseline period before the commencement of business, and unused losses can be carried forward to future years or utilized through Group Relief. This provision helps alleviate the tax burden on businesses in the startup phase.

Founder Tokens: ICO companies can reserve a portion of tokens to grant to founding developers as recognition for their contributions to the design and implementation of the tokens. If these "founder tokens" are issued as service compensation, they are considered taxable income and are taxed when the founders actually gain control over them; if there is a lock-up or restriction period, they are taxed at their value upon expiration; if they are obtained not as compensation for services, they are not treated as taxable income.

Note: The Inland Revenue Authority of Singapore (IRAS) explicitly requires taxpayers to maintain complete transaction records related to digital tokens and provide them when necessary. These records should include transaction dates, the quantity of tokens received or sold, the value and exchange rate of tokens at the time of the transaction, the purpose of the transaction, customer or supplier information (applicable to buying and selling transactions), ICO details, and receipts or invoices for business expenses. This information is not only the basis for tax reporting but also an important proof for dealing with tax audits and ensuring compliance.

Table 3: Taxability of Different Types of Tokens in ICOs

(B) GST - Goods and Services Tax

Goods and Services Tax (GST) is the main form of indirect tax implemented in Singapore since 1994, broadly categorized as a consumption tax, as it is levied on final consumption. Essentially, it is a value-added tax (VAT) applied at a uniform rate to most goods and services supplied and imported. As of 2024, the standard GST rate is 9%. GST is collected and remitted by businesses and applies to domestic transactions and cross-border digital services, with certain financial services, exports, and specific international services eligible for exemption or zero-rate treatment.

On August 3, 2022, IRAS released a new version of GST: Digital Payment Tokens (initially published on November 19, 2019), which stipulates the treatment of consumption tax for transactions involving digital tokens and cryptocurrencies (hereinafter referred to as digital payment tokens).

The core change is that, starting from January 1, 2020, the supply of qualifying digital payment tokens (DPT) is exempt from GST to avoid double taxation at both the purchase and usage stages of the tokens. This adjustment significantly reduces tax friction for cryptocurrencies in payments and transactions, enhancing Singapore's competitiveness as a crypto asset-friendly jurisdiction. However, it is important to note that this exemption is limited to situations that meet the DPT definition and does not affect the normal collection of related intermediary service fees, platform fees, and other taxable items.

In the specific rules, IRAS first strictly defined DPT and clarified the categories of tokens that do not fall under the exemption (such as utility tokens, security tokens, closed-loop virtual currencies, etc.). Subsequently, the guidelines differentiate between different types of tokens and their GST treatment in transactions, exchanges, and payments. For example, the buying, selling, and payment behaviors of compliant DPT can enjoy exemption, but related services provided by platform operations, wallet custody, payment intermediaries, etc., still need to be calculated as taxable supplies under GST. Through this dual judgment of "asset attributes + business types," Singapore maximizes the reduction of tax barriers for crypto transactions while maintaining the fairness of the tax system.

1. Classification of Digital Payment Tokens

The guidelines stipulate that a digital payment token (DPT) is a digital representation of value that possesses all of the following characteristics:

(a) Represented in units;

(b) Designed to be interchangeable (homogeneous);

(c) Not priced in any currency, and the issuer does not peg it to any currency;

(d) Can be electronically transferred, stored, or traded;

(e) It is, or is intended to be, accepted as a medium of exchange by the public or a part of the public, and there are no significant restrictions on its use as consideration.

However, digital payment tokens do not include the following situations:

(f) Legal tender;

(g) If a supply can be considered exempt under Part I of the Fourth Schedule of the Goods and Services Tax Act, and the reason is not that the supply itself is a digital payment token with the above characteristics (a) to (e), then that supply does not belong to digital payment tokens;

(h) Any rights that grant the recipient or indicate a specific individual or group to provide goods or services, and after that right is exercised, it no longer serves as a medium of exchange.

IRAS lists typical DPTs, including Bitcoin, Ether, Litecoin, Dash, Monero, Ripple, and Zcash, all of which possess core characteristics such as homogeneity, not being pegged to any fiat currency, electronic transferability, and public recognition as a medium of exchange. Additionally, tokens like IdealCoin, which can be used for payments within a specific smart contract framework and freely outside that framework, as well as StoreX tokens, which can continue to circulate as a means of payment even after exercising certain specific rights, also meet the DPT definition.

Conversely, situations that do not qualify as DPT include stablecoins, which are pegged to fiat currencies and therefore do not meet the requirements of homogeneity and non-pegging; virtual collectibles like CryptoKitties, which lack homogeneity due to being non-fungible; game points or virtual currencies limited to specific environments; and points or loyalty points issued by retailers or platforms that can only be redeemed for specific goods or services, as these tokens cannot serve as a widely accepted medium of exchange.

There are also some cases that may initially appear similar to DPT but will be excluded under specific conditions. For example, StoreY tokens were initially designed as the sole means of payment for purchasing distributed file storage services, but once users exercise that specific right, the token no longer functions as a medium of exchange, thus no longer qualifying as a DPT.

For more detailed rules, characteristics, and case explanations, please refer to Section 5 of the guidelines (especially paragraphs 5.2–5.13 and examples).

2. General Trading Rules for Digital Payment Tokens

When DPT is used as a means of payment for goods or services (excluding conversion into fiat currency or other DPT), that payment behavior itself is not considered a supply and therefore is not subject to GST. The payer does not need to pay GST when using DPT for payment, but if the payee is GST registered, they should calculate output tax for the goods or services provided, unless the supply is exempt, zero-rated, or outside the scope of taxation. For example, GST registered company A purchases software using Bitcoin; A does not need to pay GST on the outgoing Bitcoin, but if seller company B is GST registered, they must calculate GST for the software supply.

Secondly, the exchange between DPT and fiat currency, as well as the exchange between one DPT and another DPT, is considered exempt supply and does not require GST payment. However, businesses must still list the relevant transactions as exempt supplies in their declarations and report net realized gains or losses. For example, if company C exchanges Bitcoin for Ether, neither party needs to pay GST, and it should only be treated as an exempt supply in the report.

Additionally, if a GST registered company issues DPT through an Initial Coin Offering (ICO) and exchanges it for fiat currency, the proceeds from that issuance are also considered exempt supply and should be reported as exempt income in the GST return. For example, if company E issues DPT and sells it to the public for Singapore dollars, the proceeds are reported as exempt supply income.

Finally, loans, advances, or credit arrangements involving DPT are also considered exempt supplies, and the related interest income is not subject to GST but must be reported as exempt income. For example, if company F lends DPT and receives interest, that interest is listed as exempt supply in the GST return.

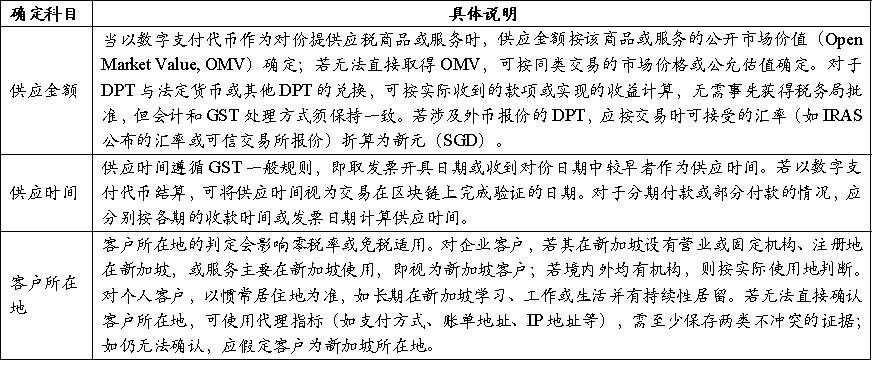

Table 4 illustrates how to determine the supply amount, supply time, and customer location in transactions involving digital payment tokens.

Table 4: Determination of Various Accounting Items

3. Specific Business Scenario Rules

(1) Mining

In general mining processes, miners provide computing power or verification services to the blockchain network but have no direct relationship with the parties involved in the transactions, and the party issuing block rewards/miner fees is unidentifiable. Therefore, obtaining digital payment tokens generated from mining (such as block rewards) does not constitute a "supply" in the GST sense, and GST does not need to be levied on that acquisition.

However, if miners provide identifiable counterparties with paid services (for example, charging commissions, transaction fees, computing power rental fees, etc.), it constitutes a taxable service supply. If miners are GST registered, they should tax and report at the standard rate; zero-rate treatment can only be applied if the zero-rate conditions are met. If the location of the trading counterpart cannot be reasonably determined, it should be treated at the standard rate.

For the subsequent disposal of mined tokens: from January 1, 2020, if miners sell or transfer the mined digital payment tokens to customers located in Singapore, it is considered exempt supply; if miners use the mined tokens to purchase goods or services, it is not considered "supplying tokens," and no tax is required on the token portion (the goods/services supplier will still be taxed according to their rules).

(2) Intermediaries

Services related to digital payment tokens provided by intermediary institutions, even if they involve token transactions, still constitute taxable supplies. If the intermediary institution is GST registered, whether it needs to report the token sales amount in the GST return depends on whether it acts as a "principal" or "agent" in the transaction. If selling tokens as a principal, it must report that sale as its own supply for GST; if acting as an agent selling tokens on behalf of clients, it should not include that sales amount in its own supply but only report the fees or margins received in the transaction as supply for GST (unless that supply is eligible for zero-rate treatment). In determining its own identity, the intermediary institution should self-assess based on contractual responsibilities and risk-bearing, payment obligations, price determination rights, and token ownership.

(3) Input Tax Credit and Reverse Charge Treatment Rules

In the course of business operations, enterprises can only claim input tax credits for expenditures used for taxable supplies; if the expenditure is used for exempt supplies (such as exchanging digital payment tokens for fiat currency or other tokens), it cannot be credited. If the expenditure involves both taxable and exempt supplies or relates to the overall operation of the enterprise, it needs to be allocated proportionally. For enterprises engaged in both taxable and exempt supplies (such as some business involving digital payment token exchanges), input tax must be allocated and attributed like other partially exempt enterprises, unless the de minimis rule is met, in which case the supply of digital payment tokens may be treated as an ancillary exempt supply if relevant conditions are satisfied. Finally, as a partially exempt enterprise, if services or low-value goods are obtained from overseas suppliers, it may still be subject to reverse charge obligations and should refer to the relevant guidelines from the Inland Revenue Authority of Singapore.

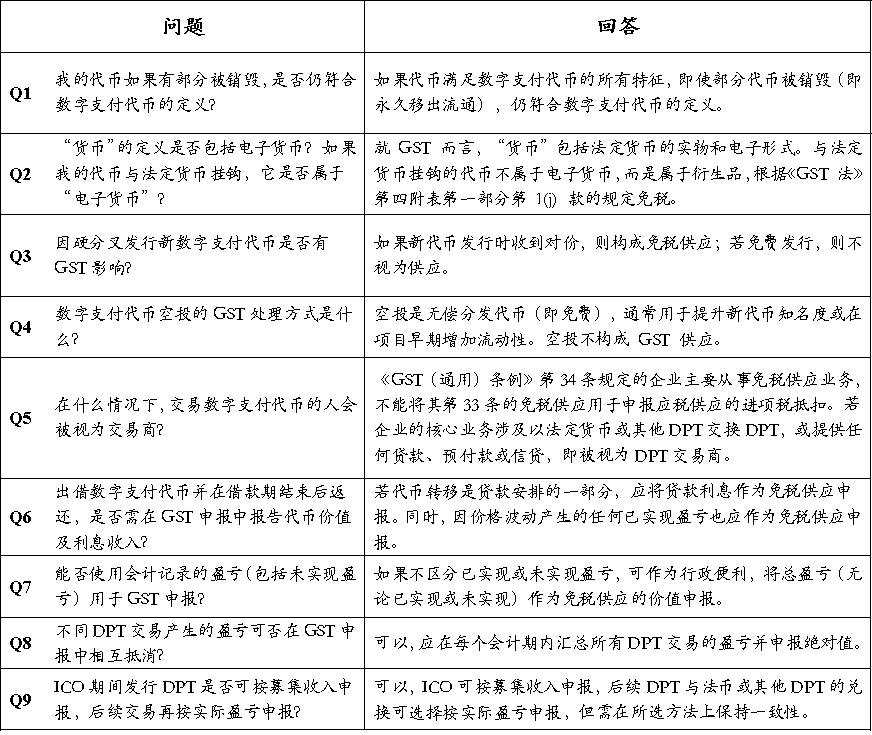

4. Frequently Asked Questions

Table 5: Common Q&A

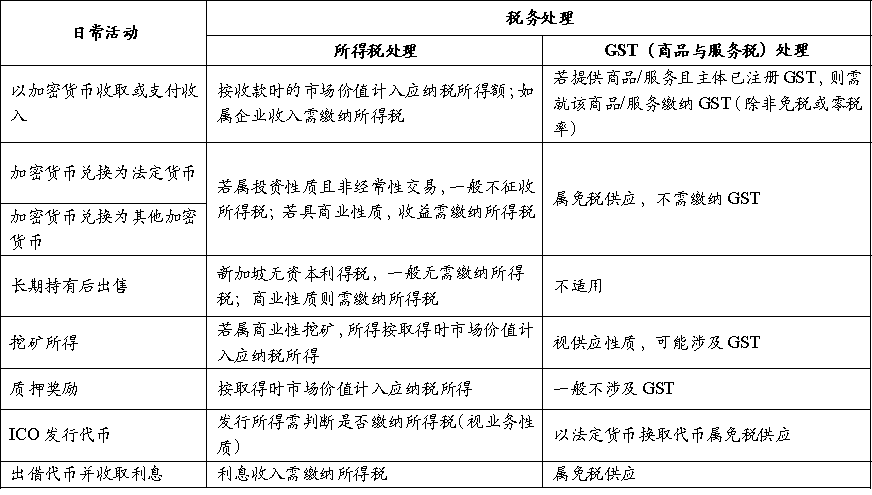

(C) Classification by Usage Activities

Table 6: Taxable Situations for Daily Usage Activities

(D) Other Taxes

Globally, most countries generally define cryptocurrencies as non-legal tender, so the main taxes associated with them typically include income tax, value-added tax, or consumption tax. In the previous sections, we have summarized in detail the main tax treatment rules for cryptocurrencies in Singapore regarding daily holding and usage activities under income tax and Goods and Services Tax (GST). In contrast, other taxes are less related to the daily application of cryptocurrencies and will not be further elaborated.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。