Abstract

In the past decade, stablecoins have gradually moved from a little-known development experiment to the spotlight of global finance. From the collapse of the algorithmic stablecoin TerraUSD (UST) in 2022, which led to the evaporation of about $60 billion in market value overnight, to the traditional giant Binance's BUSD stablecoin being forced to halt new issuances in 2023 due to regulatory pressure, and to the high-profile emergence of the USD 1 stablecoin founded by the Trump family in early 2025—these iconic events all indicate that stablecoins have become a hot topic at the intersection of the crypto world and traditional finance. Whether it is Wall Street institutions, internet giants, or ordinary investors, everyone is closely watching the stablecoin sector. However, despite the heat surrounding stablecoins, the entry barriers are not low, and technical and compliance challenges deter many from participating.

This article will analyze the driving forces and obstacles behind the current stablecoin boom from three perspectives: institutions, retail investors, and on-chain innovations, and explore why many are eyeing stablecoins but find it difficult to enter the market.

Table of Contents

1. Why are stablecoins so popular?

- Rapid market growth

- Policy driving industry mainstreaming

- Public enthusiasm and cognitive gap

- Payment giants and financial institutions actively entering the field

2. How are global institutions positioning themselves in stablecoins?

- JD Group: Driven by cross-border payments

- JPMorgan (JPM Coin): Corporate treasury settlement

- PayPal (PYUSD): Consumer-level applications

- Fintech companies (Stripe, Revolut, etc.): Payment bridging

- Cross-border financial pilots: Public-private cooperation

- Mainstream bank executives expressing support

3. Those eager to enter but unsure how: Obstacles and dilemmas

- High technical barriers and expensive development costs

- Economic model design and liquidity challenges

- Financing and liquidity support becoming increasingly difficult

- Compliance pressure and regulatory fog

- Insufficient credit endorsement, making trust hard to establish

- User experience barriers, cumbersome entry operations

4. Native Chain × Stablecoin: One-click issuance + smooth experience

- Native one-click issuance

- Stablecoin payment Gas

- Ultimate user experience (UX)

- Security and decentralization guarantees

5. In conclusion: Observations from Bixin Ventures

1. Why are stablecoins so popular?

Stablecoins, as crypto assets pegged to fiat currencies, have become a bridge connecting traditional finance and the blockchain economy. Their popularity in recent years is reflected in several aspects:

Rapid market growth

- Growth in active addresses: The number of stablecoin users and transaction volumes has surged explosively. The number of active stablecoin wallet addresses increased from 19.6 million in February 2024 to 41 million in August 2025, with an annual growth rate exceeding 100% (source: Artemis).

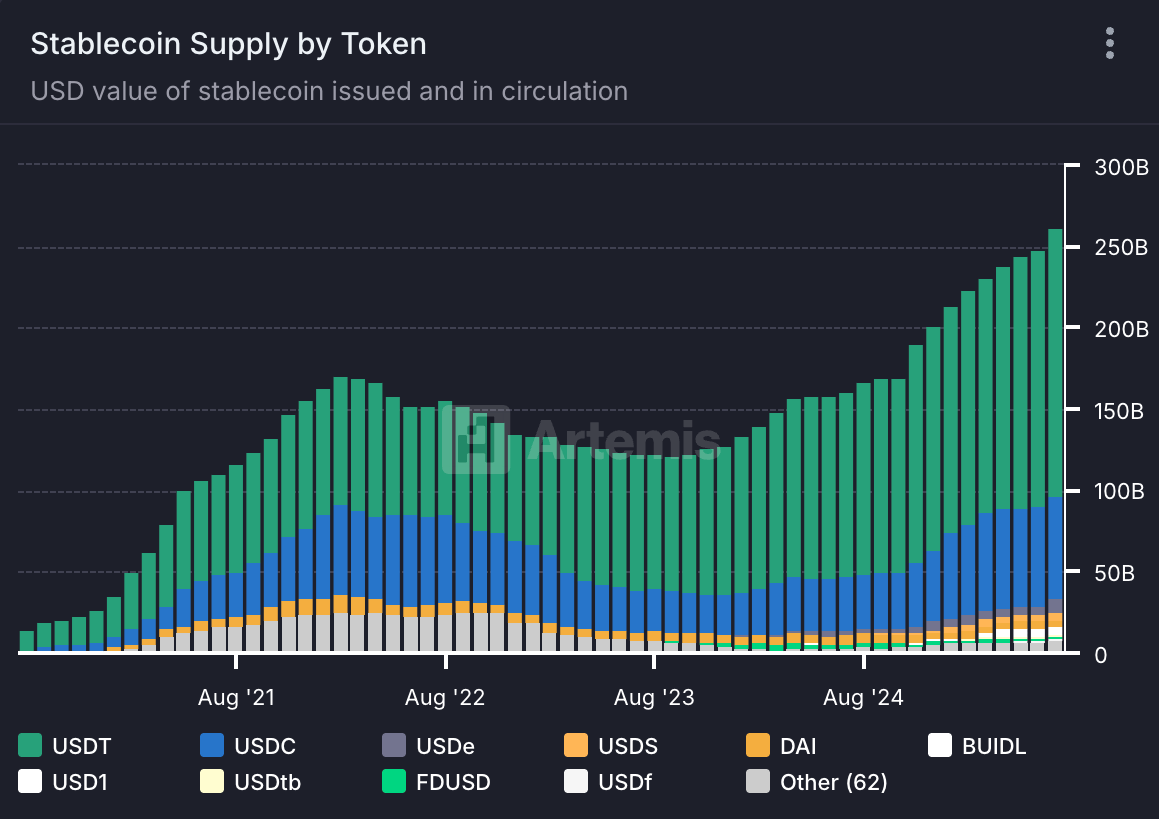

- Supply growth: During the same period, the total global supply of stablecoins rose from about $138 billion to $275 billion, achieving a 99% year-on-year increase.

(Source: Artemis)

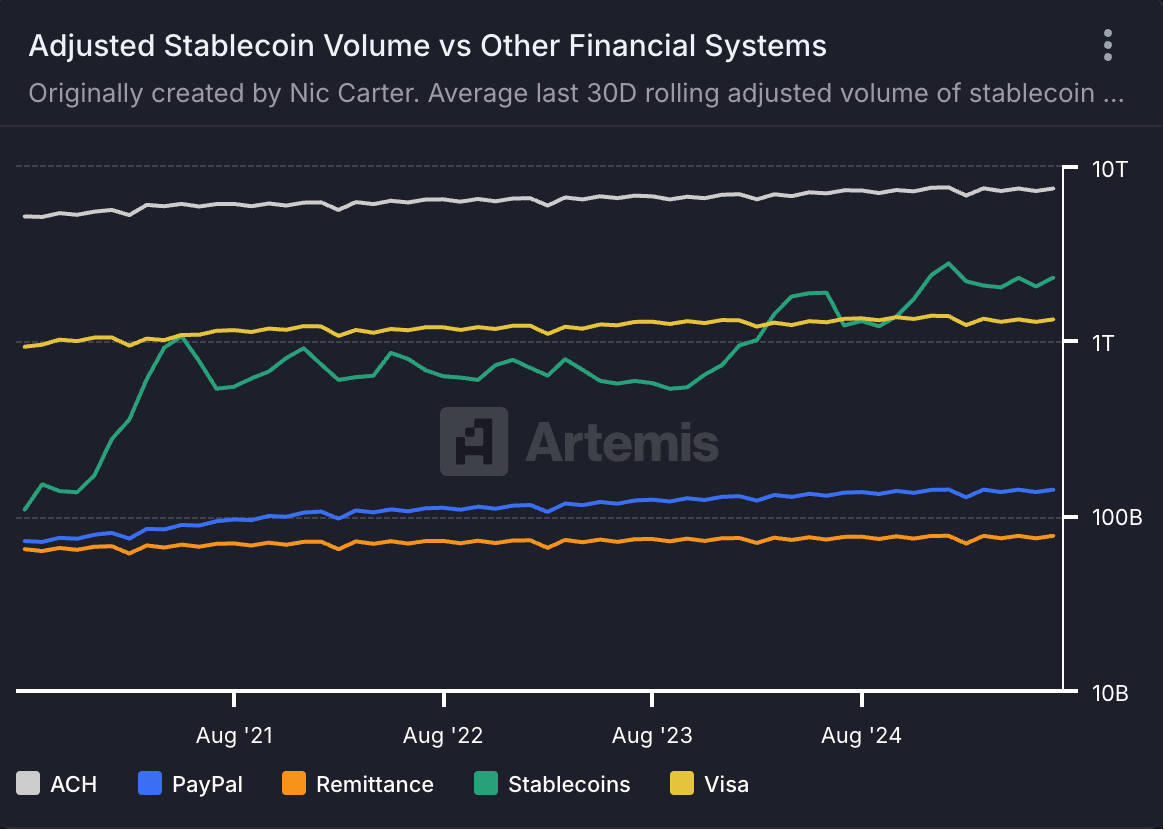

- Transaction volume surpassing payment giants: Since September 2024, the daily transaction volume of stablecoins has consistently exceeded that of VISA channels, even reaching a peak of $5.1 trillion at one point.

(Source: Artemis)

This series of data indicates that whether in exchanges, DeFi, or payment scenarios, the penetration and influence of stablecoins are significantly increasing.

Policy driving industry mainstreaming

The rapid follow-up of regulations in various countries has laid the foundation for the legal and compliant development of stablecoins.

- United States: In July 2025, the "Guidance and Establishment of the U.S. Stablecoin National Innovation Act (GENIUS Act)" was officially signed, which specifies that only federally insured deposit institutions can issue payment stablecoins, and they must maintain 100% reserves, disclose monthly, and undergo annual audits while adhering to strict KYC/AML measures.

- Hong Kong: The Legislative Council passed the "Stablecoin Ordinance" in May 2025, requiring issuers to apply for a license from the Hong Kong Monetary Authority and meet requirements for high-quality assets with 1:1 full reserves, sound redemption mechanisms, and regular audits.

- Europe: The MiCA (Regulation on Markets in Crypto-Assets) regulation was officially implemented at the end of 2024, bringing stablecoins under strict regulatory scrutiny, requiring issuers to meet stringent standards for capital adequacy, liquidity, and transparent disclosure.

Major global financial centers have made their stance clear on stablecoins, and compliance is driving stablecoins from the gray area into mainstream finance.

Public enthusiasm and cognitive gap

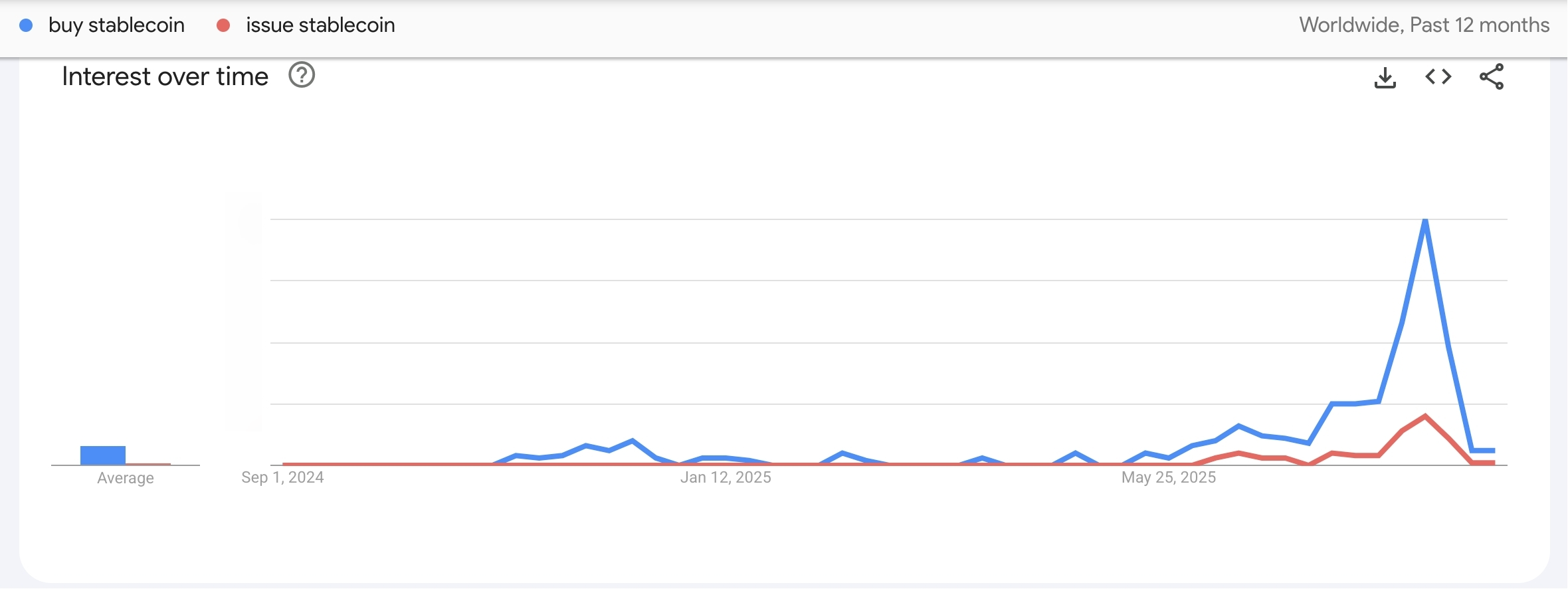

Search engine trends also reveal the public's strong interest in stablecoins. Over the past year, the search volume for keywords like "how to buy stablecoins" and "stablecoin yields" on Google has surged several times, while queries for "how to issue stablecoins" are almost nonexistent. This contrast indicates that the public is very interested in using stablecoins but still has limited understanding of creating them, leading to high market demand but significant barriers on the supply side, further stimulating calls within the industry to lower entry barriers and innovate issuance methods.

(Google Trends search volume comparison Source: Google)

Payment giants and financial institutions actively entering the field

Faced with the efficient and low-cost advantages of stablecoins, traditional payment networks and internet financial platforms are competing to test them, viewing them as an opportunity to upgrade the global payment system. BIS (Bank for International Settlements) research shows that if cross-border payments use stablecoin settlement, the speed can increase by two orders of magnitude, and costs can be reduced by over 90%. This makes stablecoins a potential solution to the "slow and expensive" pain points of cross-border remittances. In recent years, both Visa and Mastercard have announced plans to support stablecoin settlements: Visa has piloted the acceptance of stablecoins like USDC for settling funds from some issuing banks in its global settlement network, while Mastercard has launched an end-to-end stablecoin payment solution, preparing to incorporate compliant stablecoins into its merchant network. Payment service provider Stripe has been offering USDC payment options for content creators since 2022 to enable global instant micropayments, while e-commerce platform Shopify has also supported users in settling product payments with stablecoins through partnerships. Notably, PayPal not only issued its own dollar stablecoin PYUSD but also announced in 2025 that it would provide an annual 3.7% yield incentive for users holding PYUSD to encourage them to hold and use stablecoins in PayPal and Venmo wallets. These initiatives reflect that traditional payment giants view stablecoins as an important component of the next generation of payment channels: on one hand, using stablecoins to achieve near-instantaneous cross-border fund transfers at a cost that is only one-tenth of SWIFT wire transfers, and on the other hand, leveraging stablecoins to tap into the new growth of the crypto payment market. In summary, from internet giants to bank payment networks, stablecoins are increasingly being treated as "financial infrastructure" in the digital age, significantly boosting their industry popularity.

In conclusion, whether it is the rapidly expanding user base and transaction volume, the gradually clarifying regulatory environment, or the public's heightened interest and the embrace of mainstream institutions, multiple factors combined have made stablecoins one of the hottest topics in the current crypto space. The heat surrounding stablecoins is backed by their potential as digital cash anchored in value, showcasing immense potential in connecting tradition and innovation.

2. How are global institutions positioning themselves in stablecoins?

The prospects for stablecoins are broad, and various leading institutions are already gearing up, entering this sector through different strategies. From tech giants to Wall Street banks, many are launching their own stablecoin projects or collaboration plans to secure a leading position in this new financial infrastructure.

Here are several typical institutions' layouts:

JD Group - Driven by cross-border payments

JD Technology's subsidiary has entered the Hong Kong Monetary Authority's stablecoin sandbox, planning to issue a Hong Kong dollar-pegged "Jcoin" for cross-border trade and e-commerce payments. The goal is to significantly reduce cross-border payment costs and improve settlement efficiency while exploring offshore RMB stablecoins to promote the internationalization of the RMB.

JPMorgan (JPM Coin) - Corporate treasury settlement

Launched in 2019, JPM Coin is primarily used for instant fund transfers between institutional clients, based on the Quorum consortium blockchain. It processes an average daily amount of about $1-2 billion, becoming an important infrastructure for large enterprises' liquidity management and cross-border settlement.

PayPal (PYUSD) - Consumer-level applications

PayPal launched PYUSD in 2023 in collaboration with Paxos to issue a dollar stablecoin, which has been integrated into PayPal and Venmo wallets. Starting in 2025, it will offer a 3.7% yield for holding the coin, targeting payment, settlement, and fund management scenarios for small and medium-sized merchants and freelancers.

Fintech companies (Stripe, Revolut, etc.) - Payment bridging

Stripe provides USDC payment services for creators, while Revolut is developing multi-currency stablecoins to reduce remittance and exchange costs. Both represent typical cases of emerging fintech expanding the global payment market using stablecoins.

Cross-border financial pilots - Public-private cooperation

Initiatives like mBridge and Project Agorá led by BIS, as well as the Canton Network composed of investment banks and tech companies, are promoting the co-construction of on-chain settlement networks by central banks, commercial banks, and financial institutions, exploring the compliant application of stablecoins in cross-border payments and financial markets.

Mainstream bank executives expressing support

Large financial institutions' attitudes towards stablecoins have shifted from observation to action. Several banks have revealed their stablecoin plans during earnings calls: Citigroup stated it is exploring the issuance of a "Citi Stablecoin"; Bank of America has also been reported to be internally incubating a dollar stablecoin for corporate client payment settlements. JPMorgan's CEO admitted that customer demand is driving banks to participate in the competition. Standard Chartered not only joined the Hong Kong sandbox to test stablecoins but also partnered with Singapore's StraitsX to provide custody and cash management services for its newly issued coins and dollar stablecoins. Even asset management giant BlackRock has indirectly entered the stablecoin space through investments in Circle and collaborations with Coinbase. It can be said that from banks to payments, from e-commerce to social networks, various institutions are forming a surrounding momentum to enter the stablecoin sector. Their participation not only brings substantial capital and user bases but also empowers the stablecoin ecosystem in terms of compliance, security, and global networks. This is why the current development speed of stablecoins is so rapid—backed by giants, stablecoins are moving from grassroots innovation to a new stage of mainstream adoption.

(Stablecoin industry chain map Source: As shown)

3. Those eager to enter but unsure how: Obstacles and dilemmas

Despite the giants making significant strides in the stablecoin field, many small and medium players (individual developers, startup teams, small and medium enterprises, and even traditional industry companies) face numerous difficulties in entering the market. They see the opportunities and potential of stablecoins but often find it hard to participate due to various barriers.

Here, we outline several common obstacles that hinder these potential participants:

High technical barriers and expensive development costs

Creating a stablecoin project is no easy task. First, blockchain development itself poses a significant barrier for ordinary teams, requiring expertise in smart contracts, security audits, multi-chain interactions, and other specialized skills. According to estimates from blockchain development consulting firms, developing and deploying a stablecoin contract from scratch, along with supporting wallets and website backends, can cost anywhere from $30,000 to $50,000, and can go as high as $500,000, depending on team size, functional complexity, and compliance requirements. This represents a huge investment for small startup teams. Additionally, security audits are an unavoidable step, with each audit typically costing between $10,000 and $100,000; to prevent hacking attacks, many projects also need to purchase smart contract insurance, with annual premiums ranging from a few thousand to tens of thousands of dollars. Conservatively calculated, audit and security investments often account for 20%-30% of the project's initial budget. Not to mention that ongoing operations require continuous upgrades and iterations of code to adapt to new hacking techniques. These high upfront financial and technical investments leave many ideas on paper—many individuals or small teams, despite having creativity and enthusiasm, can only helplessly give up when faced with budget sheets and technical stacks.

Economic model design and liquidity challenges

The success of a stablecoin project is not only about programming but also depends on the underlying financial engineering. Issuing a pegged coin requires careful design of collateral mechanisms or algorithmic adjustment mechanisms to ensure price stability. If the market experiences severe fluctuations and users redeem en masse, the system needs to have contingency plans to avoid a death spiral. This means that small teams must possess the ability for economic model modeling and stress testing, simulating whether the stablecoin can maintain its peg under various extreme scenarios. For example, the collapse of Terra UST serves as a cautionary tale: algorithmic stablecoins lacking asset backing can collapse instantly during a crisis of confidence, with hundreds of billions of dollars in market value evaporating in just a few days. However, many startup projects often overlook the importance of modeling, focusing only on the superficial aspect of "technically achieving 1:1 pegging" without delving into the stability after scaling. As a user in the crypto community aptly put it: "Writing code to issue coins is technically simple… the hard part is how to scale to billions of dollars and how to redeem every dollar at that point." In other words, a small team may be able to develop a functioning stablecoin contract, but it may not withstand the tests of the real market. On the other hand, stablecoin projects often face liquidity traps in their early stages: without sufficient funds to provide market making and depth, stablecoins struggle to maintain circulation value and stable exchange; yet, if no one is willing to provide liquidity, how can there be funding support? In this chicken-and-egg dilemma, many small projects find their coin prices and pegging mechanisms rendered meaningless in the absence of trading volume. Once someone sells, the stablecoin may instantly deviate from its peg without the ability to adjust, leading to a collapse of trust.

Difficulties in financing and liquidity support

Stablecoin projects also face the challenge of "raising investment" commercially. Unlike ordinary application-based startups, stablecoins are capital-intensive: not only do they burn cash during the development phase, but they also require substantial reserves to provide liquidity and respond to redemptions during operations. Therefore, small teams often seek VC investment or market maker loans to expand their capital pool. However, the reality is harsh—most investment institutions are not interested in stablecoin startups. As analyst Anthony DeMartino pointed out, even if small projects offer enticing conditions like 40% annual interest, it is still difficult to secure market-making funds, as venture capitalists seek returns of over 10 times and are not swayed by a few percentage points of interest; market makers also face high capital costs, typically around 20% opportunity cost for their own funds, and considering risk premiums, they are rarely willing to lend at fixed rates to an uncertain stablecoin project. He describes many of these startup teams as "going to battle with toy knives," severely lacking ammunition while attempting to challenge well-funded existing stablecoin giants, with predictable results. Many founders are repeatedly questioned during fundraising roadshows: "How large is your liquidity pool? Where is your community? Is your market budget sufficient?" Ultimately, they often find themselves turned away for failing to provide convincing numbers. As one entrepreneur lamented in a forum: "Without funds for market making and marketing, without a user community and a strong team, the success rate is very low." The lack of funding and insufficient self-sustenance quickly trap small stablecoin projects in a vicious cycle: lack of funds—lack of users—unable to establish credit—further lack of funds, ultimately leading to abandonment.

(Source: medium.com/@anthonydemartino)

Compliance pressure and regulatory fog

As mentioned earlier, clear regulations have been introduced for stablecoins in various major jurisdictions. For small teams, this presents another mountain to climb. The U.S. requires stablecoin issuers to be regulated financial institutions, Europe mandates registration as electronic money institutions with capital requirements, and Hong Kong requires licensing and statutory audits… just preparing compliance documents and processes can overwhelm a batch of developers. Obtaining a license not only takes a long time and involves complex processes but also incurs significant costs. For example, establishing a regulated trust company in the U.S. can require millions of dollars in capital and a professional legal team to handle the application. Similarly, applying for a stablecoin license in Hong Kong must meet strict shareholder qualifications and risk management requirements. Some regions (like Canada) even classify stablecoins directly as securities, subjecting projects to cumbersome registration and disclosure obligations under securities laws. For small projects with limited budgets, they either choose to take risks by skirting regulations (which can easily lead to shutdowns or penalties) or abandon the idea altogether due to compliance barriers. Regional regulatory differences also leave teams at a loss—going to the U.S. raises fears of violating federal laws; heading to Southeast Asia lacks clear definitions; moving to Europe requires establishing entities, audits, and white papers under MiCA, which is not feasible for most startups in the short term. The result is that many ideas remain underground, afraid to push into the market for fear of regulatory pitfalls. The uncertainty of compliance makes ordinary people feel that stepping into the stablecoin field is "fraught with pitfalls," leaving them unsure of where to start.

Insufficient credit endorsement, making trust hard to establish

As value-pegged assets, stablecoins rely heavily on credit. However, small teams often lack the endorsements needed to gain public trust. First is the team background: many small project teams are anonymous or semi-anonymous, lacking notable industry experience and without backing from large institutions. Users find it hard to exchange real money for tokens issued by an unfamiliar team. In community forums, there are often reminders to check whether the project has a publicly available company entity, who the responsible parties are, whether they have undergone audits, and whether the code repository is active. Many small stablecoins, upon investigation, reveal team members without introductions, GitHub repositories that haven't been updated for a long time, and social media activity that is inconsistent, naturally raising doubts among potential users. Additionally, transparency is also an issue—mainstream stablecoins like USDC regularly disclose reserve asset proofs, while small projects often struggle to afford audit costs, and even if they claim to have 1:1 reserves, users have no way to verify this. This leads to a trust black box: people do not know if you are "printing money out of thin air" to exploit them. Once doubts arise, without a credible third party to prove their innocence, small stablecoins can easily face a run on the bank. It can be said that in the trust-based stablecoin field, new entrants are inherently at a disadvantage: without a brand, without regulation, and without substantial financial backing, why should users believe that your coin can maintain stable redemption? This trust deficit causes many potential users to "watch more than act."

User experience barriers, cumbersome entry operations

Even if technical and funding issues are resolved, small teams often overlook the importance of user experience. In the current multi-chain ecosystem, users often face numerous obstacles when using stablecoins: for example, to use a stablecoin on Ethereum, they must first have Ethereum's native coin ETH as Gas; if they want to use it on BSC, they need to prepare BNB to pay transaction fees. New users often feel confused: "I want to issue or use a stablecoin, but I'm required to buy another coin to pay fees." Additionally, switching networks between different chains, adding contract addresses, and calculating slippage fees are extremely unfriendly to non-professional users. A topic hashtag "#GasInUSD" has even emerged in the community, reflecting users' strong desire to pay on-chain Gas directly with dollar stablecoins. The reality, however, is that most public chains do not support this experience. Many small teams have issued new stablecoins but have not provided accompanying wallets and user-friendly tools, forcing users to navigate multiple exchanges and bridges to obtain and use these tokens. This disjointed experience often leads first-time users to abandon their attempts due to mistakes or inconvenience. For instance, some teams reflected that they lost a large number of potential users on their launch day because many newcomers got stuck trying to switch RPC networks, or a single exchange failed due to excessive slippage, ultimately leaving disappointed. Complex entry operations inadvertently block many ordinary people interested in stablecoins from getting in.

In summary, these real dilemmas create a portrait of many groups eager to invest in the stablecoin wave but struggling to find an entry point: among them are innovative developers, entrepreneurs embracing new finance, small and medium enterprises seeking cost reduction and efficiency, and ordinary merchants looking forward to digital asset payments… They see the opportunities in stablecoins, yet they suffer from lack of funds, lack of technology, lack of compliance pathways, lack of trust endorsements, and lack of useful tools, leaving them to watch from the sidelines. Their voice might be: “The prospects of stablecoins are enticing, I don’t want to miss out, but how exactly should I participate? Who can help me overcome these hurdles?” These pain points are precisely what lead to the key question in the next chapter—Is there a solution that can pave the way for these hesitant individuals?

(Illustration of stablecoin issuance barriers Source: Created by the author)

4. BenFen Chain × Stablecoin: One-Click Issuance + Smooth Experience

From the perspective of investment and infrastructure development, lowering the barriers to issuing and using stablecoins is key to expanding the future market. We note that BenFen Chain (本分链) attempts to address several common pain points faced by small teams and new users in its design:

Native One-Click Issuance

On BenFen Chain, any authorized user can issue their own stablecoin as easily as filling out a form. The platform provides a user-friendly UI: users simply select the type of collateral asset they want to peg (e.g., USD, gold, or other compliant assets), input the desired issuance amount, and click the “Mint” button to generate the corresponding stablecoin token in seconds. The entire process requires no smart contract coding, no complex protocol deployment, and no additional high audit fees—technical risks are managed by BenFen's underlying Move smart contract security model, with contract templates having undergone rigorous audits and long-term operational validation, allowing issuers to enjoy out-of-the-box security without reinventing the wheel. It can be said that BenFen has reduced the technical barriers to stablecoin issuance to nearly zero cost: development investment drops from tens of thousands of dollars to just a few dollars in Gas fees, and the time required shrinks from months to minutes. For project parties lacking development teams, the one-click issuance tool provided by BenFen is undoubtedly revolutionary. This means that whether it’s merchants with cross-border payment needs or creative startup teams, they can easily create their own stablecoins to serve specific communities or business scenarios without being troubled by technical bottlenecks.

Stablecoin Payment Gas

BenFen is well aware of the long-standing Gas payment experience issues troubling users, and has made breakthroughs at the architectural level: allowing direct payment of on-chain fees with stablecoins. On BenFen Chain, stablecoins are no longer just a medium of exchange; they can also be used to pay for on-chain operation fees. For example, when users transfer or call contracts on BenFen Chain, they can directly use stablecoins like BUSD or BJPY to pay Gas, without needing to hold the native governance token of BenFen Chain. This design completely eliminates the cumbersome requirement for new users to "first buy a bunch of chain tokens to pay Gas" when using dApps. Even better, BenFen's average transaction fee is extremely low, at about $0.05, far below the Gas costs of $0.3–0.5 on Ethereum/BSC. To optimize the experience for newcomers, BenFen even supports Gas sponsorship: project parties or third parties can sponsor transaction fees for users, allowing them to not pay Gas when using designated applications. This series of improvements means that within the BenFen ecosystem, whether it’s newcomers to blockchain or seasoned users coming from other chains, they can enjoy a “stablecoin as fuel” smooth experience. Here, stablecoins truly become a universal value carrier on-chain—serving as both transaction principal and network fuel. Users can set aside complicated exchanges and use stablecoins directly in various on-chain scenarios, just like spending dollars in internet applications.

Ultimate User Experience (UX)

To further lower the barriers to using Web 3, BenFen has also put significant effort into wallet and payment experiences, striving to make it “as simple as traditional applications.” First, BenFen supports the zkLogin social login solution: users can register a blockchain wallet account with just their phone number, email, or social account, eliminating the need to memorize complex mnemonic phrases or private keys. This greatly facilitates ordinary users' onboarding and reduces asset losses due to poor private key management. Secondly, around stablecoin payments, BenFen provides comprehensive social payment features: for example, through the BenPay application, users can transfer money via phone numbers, send friend red envelopes, and accept payments via QR codes. Merchants can generate payment codes to accept stablecoin payments from customers, and users can send red envelopes or split payments just like using WeChat/PayPal, but the stablecoin transfer is actually completed on-chain. Additionally, BenFen integrates a built-in cross-chain bridge, supporting cross-chain exchanges of mainstream assets, allowing users to easily convert USDT/USDC on Ethereum or Tron into stablecoins like BUSD on BenFen Chain. The entire operation process has been meticulously refined to be simple and intuitive: users do not need to understand any on-chain terminology and can complete wallet creation, deposits, and transfers with just a few clicks. For developers, BenFen also provides a rich SDK, enabling them to easily build user-friendly front-end applications. In BenFen's view, stablecoins, as the “stable value bearers” in digital currencies, should be paired with user experiences comparable to Web 2 to truly reach the masses.

Security and Decentralization Assurance

While lowering barriers, BenFen has not sacrificed its commitment to security and decentralization. The underlying architecture employs the Move smart contract language, whose resource types and linear logic naturally avoid some common vulnerabilities (such as reentrancy attacks), providing strong type safety guarantees for stablecoin contracts. Furthermore, BenFen combines a DAG + BFT consensus mechanism to build a high-performance chain, achieving a single-chain TPS in the tens of thousands with confirmation times under 1 second. The DAG's parallel accounting ensures high throughput, while the BFT consensus guarantees finality and resistance to forks, achieving industry-leading network fault tolerance. In actual operation, the mainnet of BenFen Chain has maintained a 99.99% availability since its launch, with no downtime or rollbacks due to consensus issues. This is crucial for stablecoin applications involving funds, allowing users to trust the system's reliability. Additionally, BenFen considers the needs of different scenarios and supports flexible identity models: users can choose to participate in decentralized trading with anonymous addresses or opt for KYC completion to gain regulated permissions, thus accessing specific compliant applications or fiat deposit and withdrawal channels. At the network level, multiple authoritative institutions jointly maintain verification nodes to prevent any single party from acting maliciously, ensuring the entire chain's decentralization and resistance to censorship. In summary, BenFen pursues “stability”—reflected both in its commitment to the value of stablecoins and in the secure and robust operation of the system. Through innovative underlying technology architecture, BenFen Chain creates a safe, efficient, and trustworthy environment for stablecoin issuance and use, lowering barriers without compromising trust.

Through the design of the above four aspects, BenFen Chain aims to build a “stablecoin infrastructure that everyone can participate in.” Here, project parties do not need to be proficient in programming, do not need huge funds, and do not need to worry about complex on-chain operations— as long as they have legally compliant assets and clear application scenarios, BenFen can help project parties issue stablecoins with one click and provide user-friendly payment and management tools. This undoubtedly provides a new opportunity window for countless potential participants who were previously kept out. As the name "BenFen" implies: doing things earnestly and returning to the essence of financial services—allowing more people to equally enjoy the dividends brought by stablecoins and blockchain innovation.

BenFen solution and industry pain points correspondence table

5. Final Thoughts: Observations from Bixin Ventures

As an investment institution that has long focused on blockchain infrastructure, Bixin Ventures' core judgment in the stablecoin field is: Compliance and ease of use will be key variables driving the next wave of adoption.

Today, stablecoins have become an asset class of common interest to both institutions and retail investors, but the vast majority of potential participants still face multiple barriers related to contract development, compliance qualifications, liquidity of funds, and user experience. Projects like BenFen attempt to encapsulate complex processes at the underlying level through technology and product design, enabling more small teams and ordinary users to enter with low barriers.

From our perspective:

- For developers, it means faster experimentation and iteration;

- For small and medium enterprises, it provides viable cross-border payment and settlement tools;

- For investors, it represents an early exploration of the “popular layer” of the stablecoin ecosystem.

We understand that the future landscape of stablecoins will not be determined by a single project, but will be shaped by compliance policies, institutional participation, and the evolution of infrastructure. BenFen's current positioning is more about filling the “overlooked gaps” and helping those who originally lacked resources find their way into the world of stablecoins.

Therefore, we believe that attempts like BenFen are worth paying attention to and continuously observing. Whether it can become an important piece of the stablecoin ecosystem still needs to be validated by the market and time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。