The actions of major companies are far from simply "riding the wave."

Written by: Mia, Zhao Qirui

"On the surface, PayFi represents the ideal of a decentralized protocol, but in practice, especially within the CEX ecosystem represented by OKX Pay, it manifests more as a cleverly packaged SocialFi marketing tool. OKX Pay attracts users through the PayFi concept, strengthens the binding of social interaction and payment behavior, enhances user stickiness and ecosystem activity, reflecting the important role of major companies in promoting the popularization of Web3 payments."

### I: The Past and Present of PayFi, Redefining Web3 Payments

Since the birth of the internet, it has evolved from the Web1.0 "read-only" era to the Web2.0 "read + write" interactive era, and is gradually moving towards Web3.0, a new era based on blockchain technology, centered around users, decentralized, and achieving self-ownership of value. This evolution is not only a technological iteration but also a profound transformation of network philosophy, value distribution, and user rights. Within this grand narrative, payment—the fundamental function that sustains economic activity—is also undergoing a "redefinition" driven by underlying technologies and concepts.

(1) The Evolution of PayFi: An Inevitable Advancement of Value Interconnection

Traditional payment systems are rooted in a centralized trust model. Intermediaries such as banks and credit card companies act as "gatekeepers" of value flow. This model greatly facilitated commercial circulation during specific historical periods but also exposed many inherent pain points: high transaction costs, especially the cumbersome processes and layered fees in cross-border payments; inefficient settlement speeds, with international remittances potentially taking days to complete; lack of transparency, with users lacking clear control over the flow of funds; and a high dependence on infrastructure, leaving billions of people globally without access to basic financial services. The dominance of Web2 platforms has also led to centralized control of user data and content, as well as potential issues of censorship and abuse of power.

Bitcoin, as the first widely recognized cryptocurrency, was defined in its white paper as a peer-to-peer (P2P) electronic cash system aimed at enabling online payments without third-party intervention. This marked the germination of the decentralized payment concept. However, Bitcoin's extreme value volatility severely limited its potential as a medium for everyday transactions.

Subsequently, the emergence of stablecoins significantly alleviated the price volatility issues of crypto assets, making them one of the main payment methods in the blockchain space. Stablecoins like USDC and USDT play the role of "on-chain dollars," widely used in payment, trading, and DeFi scenarios, becoming important tools in the digital economy.

It is against this backdrop that the concept of PayFi (Payment Finance) emerged. Lily Liu from the Solana Foundation is considered the proponent of the PayFi concept, which she defines as "the process of creating new financial markets around the time value of money." PayFi is not a completely independent concept but rather integrates innovative applications of Web3 crypto payments, decentralized finance (DeFi), and real-world assets (RWA). It aims to leverage blockchain technology to innovate payment systems, achieving higher efficiency and lower transaction costs, while combining financial services with payment functions to provide new financial experiences and application scenarios.

The evolution of PayFi clearly reflects the trajectory of Web3 payments from theory to practice, from a single function to an integrated ecosystem. It starts from Bitcoin's vision of peer-to-peer payments, uses stablecoins to solve the value volatility problem, and further absorbs the advantages of DeFi in liquidity, programmability, and yield generation, while bringing real-world assets on-chain through RWA. The core goal of PayFi is to promote the application of digital assets in real-world scenarios and improve financial transaction efficiency by unlocking the time value of money (TVM). It is not merely about payment; it integrates payment, financing, investment, and other financial activities into a unified decentralized framework.

From a technical architecture perspective, PayFi is typically understood to include multiple layers: a settlement layer based on high-performance blockchains (such as Solana, Stellar, or Layer2 solutions); an asset issuance layer responsible for issuing payment mediums (such as stablecoins); a currency acceptance layer connecting fiat and crypto assets; and a user-facing front-end application layer. Additionally, there are supporting layers responsible for custody, compliance, financing, etc. This layered architecture provides a technical foundation for the robust development of PayFi.

(2) Web3 vs. Web2: Reshaping Power and Value

The core difference between Web2 payments and Web3 payments lies in the fundamental differences in underlying trust mechanisms and value transfer methods. This is not merely a difference in technical details but a redefinition of user rights and system architecture.

At a deeper level, Web3 payments build a "machine trust" network through blockchain technology. Transaction rules are written into smart contracts and executed automatically, rather than relying on manual processes. Users' identities (via DID) and assets (via tokens) truly belong to the users, stored in their blockchain addresses rather than being hosted on centralized platforms. This model fundamentally challenges the data and value distribution monopoly of Web2 platforms, empowering users with greater autonomy and value capture capabilities.

On this basis, PayFi pushes the programmability of Web3 payments and the deep integration with DeFi/RWA to the extreme. It is not just a tool for achieving low-cost, fast transfers but an ecosystem built on payment processes that can provide complex financial services such as real-time financing, yield generation, and asset management. This integration makes "payment" no longer an isolated link but a bridge connecting real-world assets and on-chain financial services, unlocking the time value of money. This marks a paradigm shift in payments from simple accounting and settlement functions to a value transfer infrastructure with rich financial attributes.

(3) Major Companies' Layout: The Entry of Giants and Paradigm Confirmation

Web3 payments, especially the blueprint of "payments as finance" depicted by PayFi, are attracting the attention of various giants due to their enormous transformative potential. This includes not only the deep expansion of crypto-native forces but also the notable entry of traditional payment, finance, and even internet technology giants. Their involvement is a strong endorsement of the value of the Web3 payment track and indicates that this field is accelerating from early exploration to mainstream application.

1. "Defense and Evolution" of Traditional Payment and Financial Giants

Visa & Mastercard: These two credit card network giants are not sitting idly by. They have already begun experimenting with using stablecoins (such as USDC) for settlements and exploring how to connect their vast global merchant networks with blockchain payments. For example, Visa has partnered with several crypto platforms to issue cards that support cryptocurrency spending and is testing USDC settlements within its network, which can significantly reduce the complexity and cost of cross-border transactions. This is a typical strategy of "embracing innovation to avoid being disrupted."

PayPal: As a pioneer in online payments, PayPal has launched its own stablecoin PYUSD and allows users to buy, sell, hold, and transfer specific cryptocurrencies on its platform, even for payments to some merchants. This marks its strategic extension from the Web2 payment territory into the Web3 realm, attempting to bring the advantages of crypto payments into its existing ecosystem within user experience and compliance frameworks.

SWIFT: Even SWIFT, which serves as the core of traditional international interbank communication and payment instructions, is actively exploring the interoperability of central bank digital currencies (CBDCs) and tokenized assets, trying to find its position in the new financial infrastructure.

2. "Cross-Border and Empowerment" of Internet Technology Giants

Chinese Internet Giants: In the context of a settled domestic payment market, cross-border e-commerce and overseas business have become new growth points. The pain points of traditional cross-border payments—high costs, slow speeds, and exchange rate risks—are particularly pronounced for them. Therefore, leveraging policy windows in places like Hong Kong to explore the use of stablecoins and other Web3 payment tools to optimize international fund settlements has become a strategic choice. JD.com, through its Hong Kong subsidiary, is positioning itself to capitalize on the disruptive potential of stablecoins in enhancing cross-border payment efficiency and reducing operational costs, attempting to "overtake" in the overseas payment track.

Overseas Technology Giants: Meta (formerly Facebook) once ambitiously promoted the Diem (originally Libra) stablecoin project, aiming to build a global, low-cost payment network, especially targeting unbanked populations. Although it faced setbacks due to regulatory pressure, its attempts profoundly revealed the desire of technology giants with vast user bases and social scenarios to enter the payment and even financial sectors, as well as the potential of Web3 technology in realizing this vision.

3. "Ecological Closed Loop" of Crypto-Native Exchanges

- Coinbase & OKX, etc.: These large centralized exchanges naturally possess users, assets, and trading scenarios. They are actively laying out payment businesses, such as Coinbase Commerce providing cryptocurrency payment services for merchants and OKX launching OKX Pay. Their logic lies in constructing a complete ecological closed loop from deposit, trading, storage to payment consumption by integrating fiat deposit and withdrawal channels, stablecoins, custodial wallets, and payment solutions. Obtaining payment licenses is, on one hand, for compliance in trading businesses, and on the other hand, lays the foundation for the expansion of their payment businesses.

(4) Deep Insights from the Layout of Giants: From "Testing the Waters" to "Strategic Positioning"

The actions of major companies are far from simply "riding the wave." They see the strategic value embedded in Web3 payments, particularly in the PayFi concept:

Efficiency Revolution: The near real-time, low-cost characteristics of blockchain payments pose a dimensional reduction attack on existing payment systems.

New Financial Paradigm: The combination of payments with DeFi and RWA opens up vast spaces for financial service innovation, such as instant settlement, programmatic financing, and automated market making.

User Sovereignty Trend: Although some giants still adopt centralized or semi-centralized models, the idea of returning user data and asset ownership advocated by Web3 is an irreversible trend. They must consider how to adapt to this trend.

Globalization Accelerator: For companies with international ambitions, Web3 payments offer a possibility to bypass traditional complex financial intermediaries, achieving more efficient global capital flows.

The explorations and investments of these giants not only bring funding, technology, and users to Web3 payments, but more importantly, they are educating the market through practical applications, promoting the maturity of regulatory frameworks, and accelerating the transition of Web3 payments from "niche geek tools" to "mainstream infrastructure." Every action they take in the PayFi space contributes to the eventual shaping of this payment revolution, collectively validating the immense potential of Web3 payments to reshape the global financial landscape.

### II: The Product Structure of OKX Pay: New Wine in Old Bottles

"The industry's first payment application that truly integrates non-custodial and compliance," is how OKX founder Star Xu positions OKX Pay, which provides a decentralized payment path through the centralized exchange ecosystem. While users enjoy the convenience of the OKX platform account system, they can also complete on-chain payments through non-custodial wallets, creating a hybrid experience of "self-control + platform endorsement." Let's break down the underlying product logic:

(1) Multisig + ZK Email + AA: The "Security + Usability" Combo Behind OKX Pay

The multisignature mechanism (Multisig) was standardized in the Bitcoin protocol in 2012 and is one of the mainstream non-custodial asset security strategies today. It reduces systemic risk caused by the loss or theft of a single private key by splitting transaction authorization among multiple signature holders (i.e., multiple private keys or recovery permission setters). In simple terms, an account can be jointly controlled by multiple people, and assets can only be accessed if everyone "signs" together. OKX Pay adopts a dual-signature approach, one being the user's Passkey signature, and the other provided by OKX as the "account guardian."

The Passkey signature, based on asymmetric cryptography, incorporates device and biometric recognition, helping users utilize on-chain services without mnemonic phrases, providing a very user-friendly experience. Meanwhile, the OKX signature integrates ZK Email and Account Abstraction (AA) into the product architecture to enhance identity privacy and transaction flexibility, aiming to solve the problems of high entry barriers, difficult key management, and fragmented payment experiences.

ZK Email (Zero-Knowledge Email): Through zero-knowledge proof mechanisms, it encrypts and protects user identity verification information, allowing users to perform on-chain identity operations without exposing specific email addresses, making it one of the friendlier entry mechanisms in the Web3 world. It simplifies the management of access permissions for users' on-chain identities and lowers the traditional mnemonic phrase barrier. In simple terms, by using encrypted emails, friends can input your email to send you money. You receive an encrypted email, click it, and the payment is completed. Technical details like wallet addresses and private keys are all handled automatically in the background, eliminating the worry of mistaking the transfer wallet address.

Account Abstraction (AA): By "abstracting" the Ethereum account model, it allows wallets to implement smart contract control permissions, custom transaction logic, multi-factor authentication, and other functions, greatly enhancing transaction flexibility and programmability, without requiring users to directly sign complex transaction data. In simple terms, it turns "wallets into customizable smart accounts."

In summary: ZK Email makes using a wallet as simple as using an email, AA makes your wallet as smart and secure as an app, and OKX Pay packages all of this together, making on-chain payments truly suitable for ordinary people.

(2) Compliance Integration: Finding Balance Between On-Chain Payments and Regulation

Although OKX Pay uses self-custodial wallets and on-chain settlements, it still incorporates embedded compliance designs in key areas such as user access, transaction analysis, and merchant audits, including mechanisms like real-name authentication (KYC) and anti-money laundering (AML). This may seem contradictory, but in essence, OKX Pay adopts a "accessible means regulatory" strategy: the platform does not directly control user assets but can impose restrictions on high-risk behaviors within the ecosystem through "service entry," "ecosystem access," "account binding," and "limit management."

Specifically, this manifests as:

User identification through OKX login or account binding, effectively establishing a centralized user profile;

High-frequency transfers, merchant payments, and community creation require identity binding or risk control review;

The platform reserves the ability to "block entry" for malicious addresses, sensitive regions, and illegal product payments;

Although funds flow on-chain, the platform can still suspend support for aggregators, recommendation pages, and other traffic.

This mechanism is referred to as "platform-level compliance constraints," which completes part of the regulatory functions based on ecosystem entry and API permissions without using user private keys. It represents a realistic intermediate form—a "fusion model of Web2 legal logic + Web3 technical architecture." Truly decentralized products with centralized compliance management.

### III: SocialFi Dressed in PayFi's Cloak

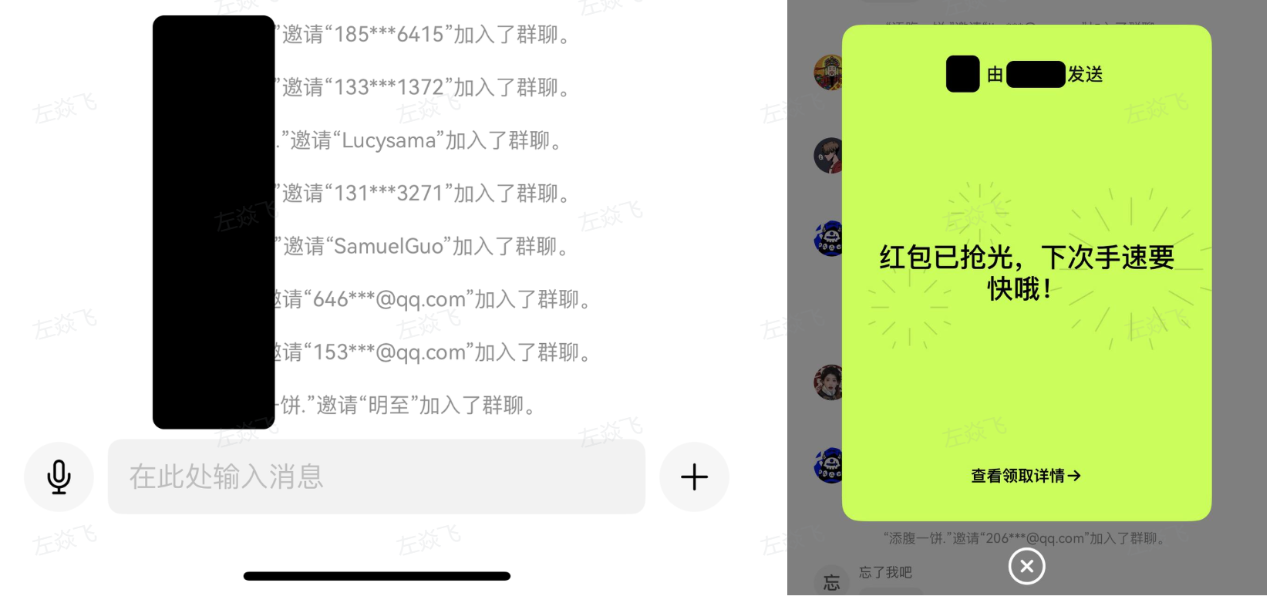

Currently, the PayFi component of OKX Pay is focused solely on internal user transfers within OKX, without integrating third-party merchants, relying more on OKX subsidies to maintain operations, including 0 transaction fees on the X Layer chain and passive staking rewards. Its true value lies in being an ecosystem enhancer, namely "payment + red envelope fission," promoting deep binding between OKX users and communities through socialized payments.

In the transfer step, OKX Pay requests access to the user's contacts. If the phone number in your contacts matches an existing OKX account, the transfer can be completed with one click, saving the hassle of finding a wallet address. If the other party has not registered yet, the system will automatically initiate a 48-hour "frozen period," temporarily suspending the transfer while guiding you to invite friends to register for OKX and create OKX Pay, activating their accounts.

This design is actually a smarter way to attract new users. Compared to traditional "referral code + reward" mechanisms or various promotional activities to bring in users (where acquiring a new user can cost up to $20), OKX Pay's transfer invitations naturally carry social trust relationships, making them not only more natural but also cheaper, representing a "zero-cost social customer acquisition" strategy that is more aligned with the growth logic of the Web3 ecosystem.

OKX's real ace is actually building KOL communities based on Pay group chats, similar to the communication mechanism of "WeChat groups," where KOLs can create group chats and share QR codes, allowing users to join with one click. In these groups, KOLs can send red envelopes, discuss crypto trends, and bypass traditional chat software's regulation of sensitive words, allowing for freer communication that is more in line with the Web3 atmosphere.

Insiders have revealed that OKX specifically recruited a product manager from the veteran SocialFi project DeBox to tailor this system based on WeChat group functionalities. This move is very "in tune with Chinese users"—low barriers, high activity, enhancing user stickiness with almost no operational investment. Compared to the overseas market dominated by Twitter as a public opinion arena, this design, which leans towards "familiar circle fission," is clearly more compatible with the Chinese community ecosystem and can better meet the growth needs of the integration of payments and social interactions.

### IV: Standing Between Structural Dividends and Regulatory Gray Walls

Although OKX Pay opens the market with a "Web3 payment + social asset network" combination, its long-term development still faces multiple challenges from compliance, user behavior, business models, and geopolitical policies, with structural dividends hiding unresolved systemic issues in on-chain payments.

(1) Business Competition: Ecological Closure, Limited Paths

Although OKX Pay claims to create a Web3 payment tool, its current usage scenarios are still mainly limited to the internal exchange, functioning more like a local feature plugin rather than a payment network that can extend beyond the exchange to serve a broader ecosystem. Compared to native payment protocols or traditional payment companies, it lacks independent value and expansion paths.

Limited Usage Scenarios: Currently, OKX Pay is mainly used for asset transfers, red envelopes, and tipping within the platform. These functions are merely small adjustments to existing fund flow paths rather than true innovations in payment experiences.

Lack of External Access: Unlike some native Web3 payment protocols (like PayFi) that can be integrated by DApps or off-chain merchants, OKX Pay has not opened SDKs or system integration interfaces, nor has it progressed to support real off-chain payment scenarios.

User Habits Not Established: Products like Binance Pay are also trying to expand payment functionalities, but overall, payment services from centralized exchanges have not yet become the primary choice for users. OKX Pay faces significant challenges in breaking through in this area.

Difficulty in Inter-Ecological Connectivity: Different exchanges operate independently, and their payment systems are incompatible. Users' payment needs often depend on their trust in the platform itself, lacking interoperability and network effects.

(2) Legal Compliance: Blurred Boundaries, Not Small Risks

Although OKX Pay adheres to basic KYC/AML requirements, entering the on-chain payment field involves more complex regulatory issues. Compliance is not only a technical process issue but also relates to the platform's boundary of responsibility and legal risks.

Identity Verification May Be Insufficient: OKX's KYC may meet exchange compliance requirements, but whether it is sufficient to address higher standards for cross-border payments and anti-money laundering remains to be confirmed. Especially when users transfer assets out of the platform for on-chain payments, the effectiveness of identity tracking may diminish.

On-Chain Transparency Brings Privacy Conflicts: On-chain payments can be publicly tracked, and although they do not display real names, they can reconstruct user profiles when combined with off-chain data. Laws like the EU's GDPR impose strict limitations on such "identifiability." If privacy protection through mixing coins or zero-knowledge technology is introduced in the future, it may raise regulatory concerns about "facilitating money laundering."

Unclear Boundaries of Platform Responsibility:

If a payment fails, a transfer error occurs, or fraud happens, does OKX have to bear arbitration or compensation obligations?

In the absence of responsibility definitions like those of third-party payment institutions, can users hold the platform accountable? Should the platform take on functions like fund freezing and dispute resolution?

Regulatory Definitions Not Yet Unified:

Whether OKX Pay falls under MSB (Money Service Business) or VASP (Virtual Asset Service Provider) depends on the interpretation of its payment functions in different regions. Some countries may view it as a wallet tool, while others may consider it equivalent to a payment institution.

Significant Global Policy Differences:

The EU's MiCA regulation has begun to establish a unified framework, but it requires specific implementation by member states;

U.S. regulation is fragmented, with agencies like the SEC and FinCEN still unclear about the boundaries between trading, payments, and securities;

Southeast Asia and the Middle East have loose regulations, but many countries can later hold entities accountable under charges like "terrorist financing" or "illegal fund transfers." The lack of a clear compliance path actually increases uncontrollable risks.

### V. Conclusion: Is OKX Pay a Protocol? Or a Tool for Building Ecosystems by Big Companies?

On the surface, PayFi represents the ideal of a decentralized protocol, but in practical implementation, especially in the CEX ecosystem represented by OKX Pay, it manifests more as a cleverly packaged SocialFi marketing tool. OKX Pay attracts users through the PayFi concept, strengthens the binding of social interactions and payment behaviors, enhances user stickiness and ecosystem activity, reflecting the significant role of large companies in promoting the popularization of Web3 payments.

For the industry, PayFi is both an innovative driving force for the implementation of Web3 payments and a hidden risk of centralization driven by giant capital. Meanwhile, as legal regulations gradually improve, the PayFi ecosystem needs to find a balance between compliance and openness, which is both a challenge and a necessary path for promoting the healthy development of the industry.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。